Gold has topped $4,200. Here’s why Yardeni thinks the rally could go even higher.

Introduction & Market Context

Meritage Homes Corporation (NYSE:MTH) presented its second quarter 2025 financial results during an analyst conference call on July 24, 2025, revealing significant profitability challenges despite modest sales growth. The homebuilder, celebrating its 40th anniversary, reported a 35% year-over-year decline in earnings per share while simultaneously expanding its community count and land position.

The company’s stock closed at $66.79 following the earnings release, up 3.2%, though it dipped 0.85% in pre-market trading to $66.22. Meritage continues to trade well below its 52-week high of $102.91, reflecting ongoing investor concerns about the housing market’s trajectory amid fluctuating mortgage rates and affordability challenges.

Quarterly Performance Highlights

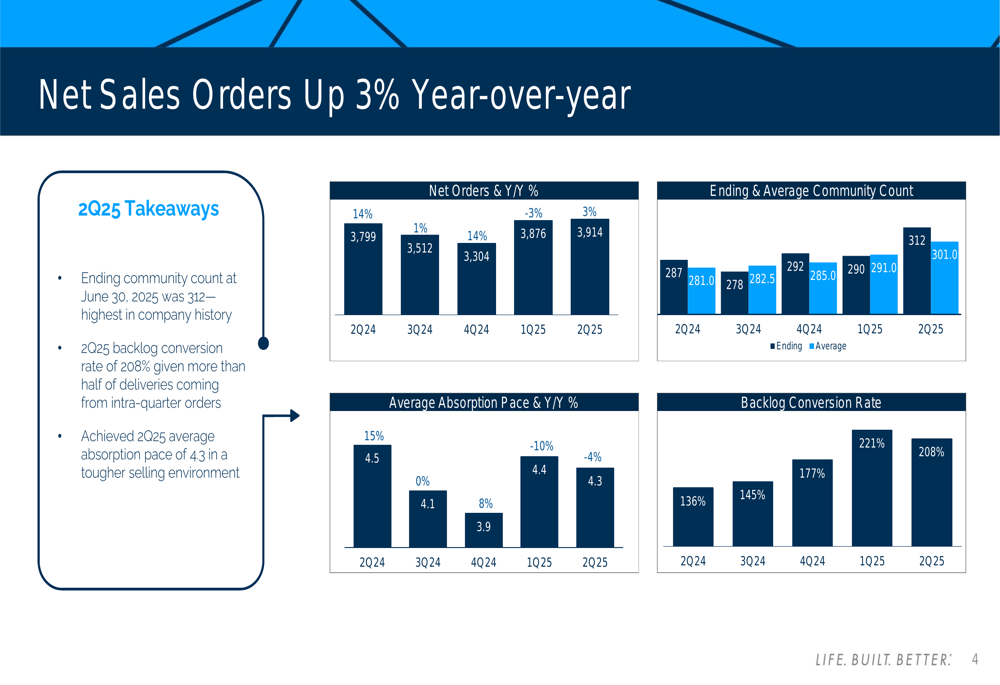

Meritage reported a 3% year-over-year increase in net sales orders to 3,914 homes for Q2 2025, while expanding its community count to 312, up from 287 in the same period last year. However, the company’s average absorption pace declined slightly to 4.3 homes per community per month, down 4% from Q2 2024.

As shown in the following chart detailing net sales orders, community count, and absorption pace:

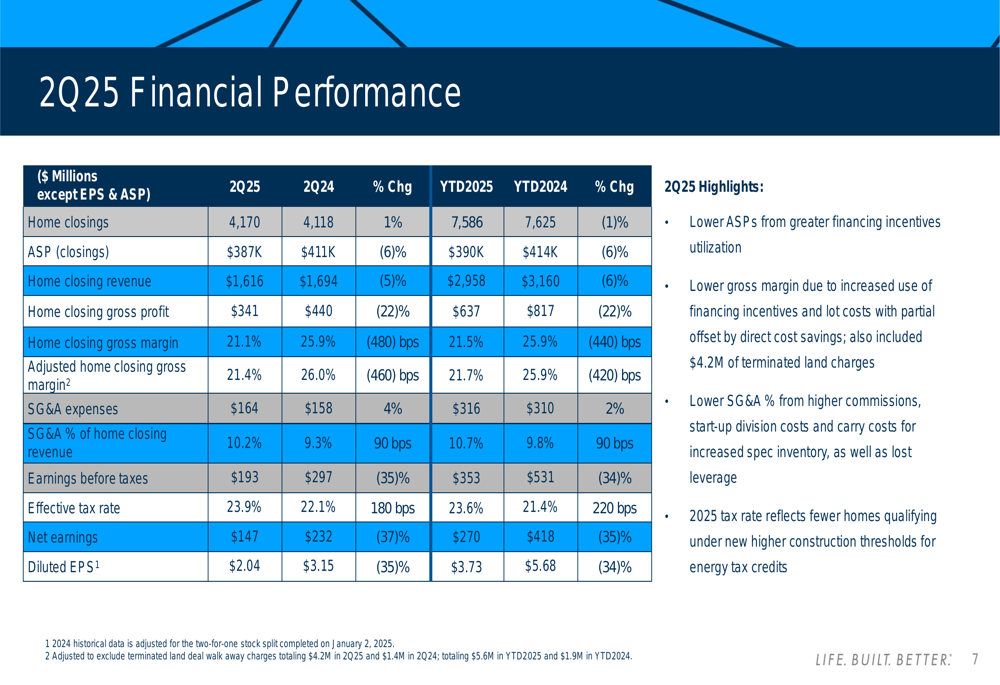

Home closings increased marginally to 4,170 units from 4,118 in Q2 2024, but the average selling price (ASP) decreased to $387,000 from $411,000 in the prior year. This pricing pressure, combined with higher costs, resulted in home closing revenue of $1.62 billion, down 5% from $1.69 billion in Q2 2024.

The company’s financial performance showed significant margin compression, with home closing gross margin falling to 21.1% from 25.9% in the prior-year period. This decline, coupled with higher SG&A expenses, drove net earnings down to $147 million from $232 million in Q2 2024, resulting in diluted earnings per share of $2.04 compared to $3.15 a year earlier.

The comprehensive financial results are illustrated in this table:

Regional Performance Analysis

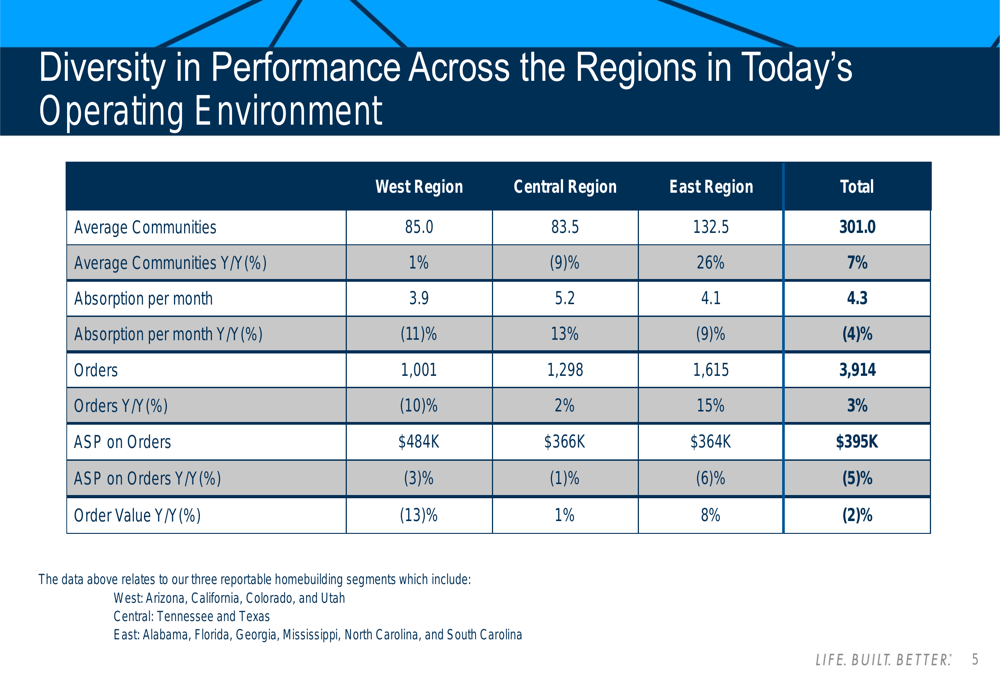

Meritage’s performance varied significantly across its three operating regions. The East region, comprising Alabama, Florida, Georgia, Mississippi, North Carolina, and South Carolina, showed the strongest performance with a 15% increase in orders and 26% growth in average communities year-over-year. Meanwhile, the West region (Arizona, California, Colorado, and Utah) experienced a 10% decline in orders despite maintaining stable community count.

The following regional breakdown illustrates these performance differences:

The Central region (Tennessee and Texas) demonstrated resilience with a 2% increase in orders despite a 9% decrease in community count, achieving the highest absorption pace at 5.2 homes per community per month. This regional variation highlights the uneven nature of the housing market recovery across different geographies.

Capital Structure and Land Position

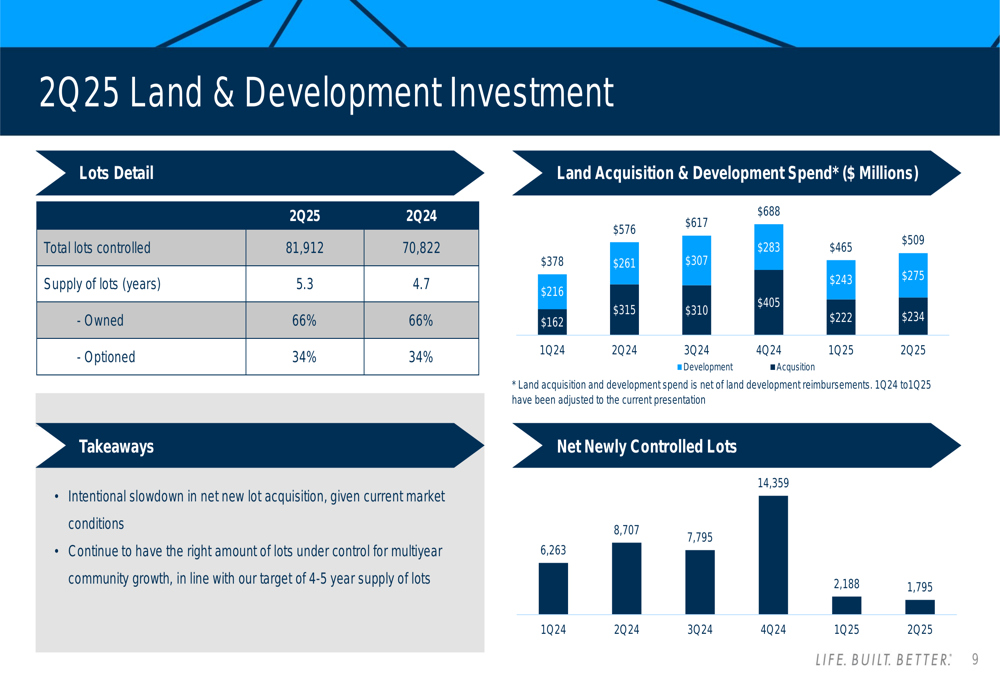

Meritage has continued to invest in future growth while simultaneously returning cash to shareholders. The company reported total lots controlled at 81,912, representing a 5.3-year supply, up from 70,822 lots and a 4.7-year supply in Q2 2024. However, the company has intentionally slowed its land acquisition pace, reducing spending compared to previous quarters.

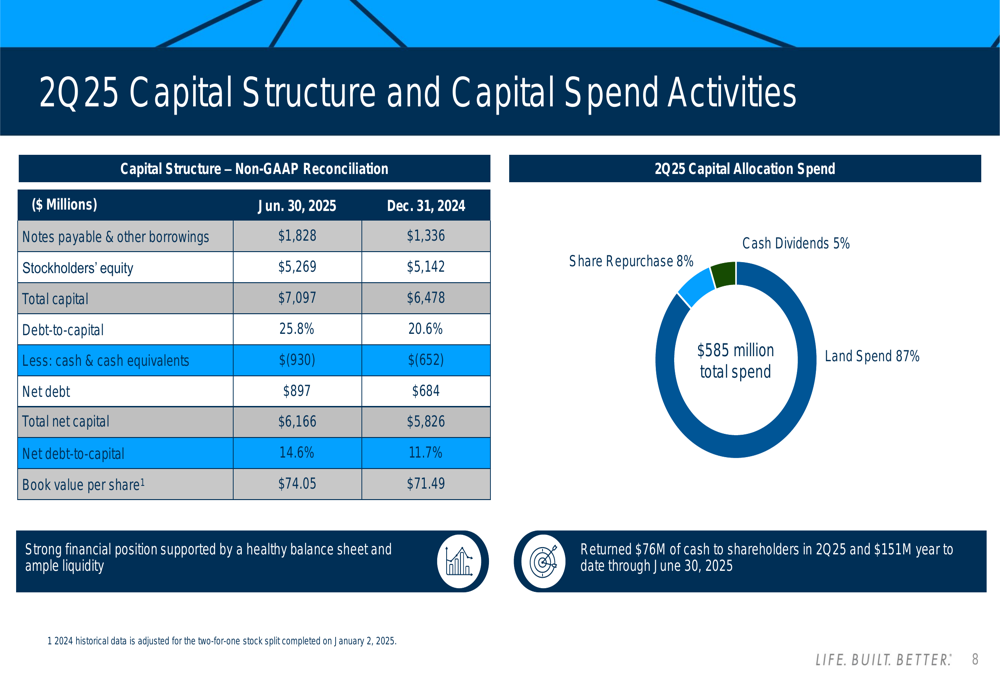

The company’s capital structure shows increasing leverage, with debt-to-capital ratio rising to 25.8% from 20.6% at the end of 2024. This reflects the company’s strategic balance between growth investments and shareholder returns, as illustrated in the following capital allocation breakdown:

Meritage returned $76 million to shareholders during Q2 2025 ($151 million year-to-date), with 87% of capital allocation directed toward land investments, 8% to share repurchases, and 5% to cash dividends. The company’s book value per share increased to $74.05 from $71.49 at year-end 2024.

The company’s land and development strategy is detailed in the following chart:

Strategic Initiatives

Meritage continues to position itself as a leading affordable homebuilder focused on entry-level and first move-up homes. The company operates across 25 markets in 12 states, leveraging its spec building strategy to provide move-in ready inventory for buyers seeking certainty in closing timelines.

As illustrated in the company overview:

The company’s strategic focus remains on its spec building approach, streamlined operations, 60-day closing commitment, and affordability-focused product offerings:

CEO Philippe Lord emphasized during the earnings call that "our go-to-market strategy provides the certainty that buyers are looking for today," while Executive Chairman Steve Hilton noted that the company’s strategy "was designed to provide certainty and weather these challenges head on."

Forward-Looking Statements

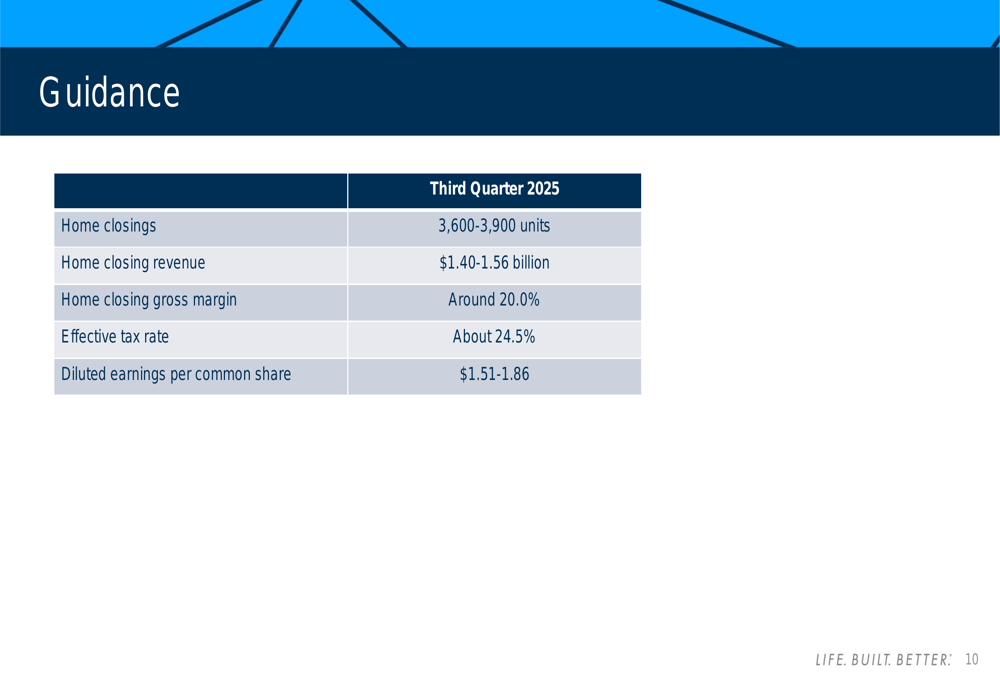

For the third quarter of 2025, Meritage provided guidance for 3,600-3,900 home closings with revenue between $1.40-1.56 billion. The company expects home closing gross margin to remain under pressure at approximately 20.0%, with an effective tax rate of about 24.5%. Based on these factors, Meritage projects diluted earnings per share of $1.51-1.86 for Q3 2025.

The detailed guidance is presented here:

Looking ahead, Meritage emphasized its flexible operations and capital allocation strategy to maximize returns throughout economic transitions. The company highlighted its Q2 community count expansion and improved cycle times as preparation for future growth opportunities, while balancing land investments with shareholder returns.

Despite current margin pressures and market challenges, Meritage appears positioned to leverage its spec-building strategy and affordable product focus to navigate the evolving housing market. However, investors will be watching closely to see if the company can stabilize margins and return to earnings growth in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.