Street Calls of the Week

Introduction & Market Context

OceanFirst Financial Corp (NASDAQ:OCFC) released its Q1 2025 earnings presentation on April 25, 2025, revealing steady financial performance and highlighting its new Premier Banking initiative. The New Jersey-based regional bank reported core diluted earnings per share of $0.35, slightly below the previous quarter’s $0.36, as the company continues to navigate a challenging interest rate environment while pursuing strategic growth initiatives.

In pre-market trading following the presentation, OceanFirst shares were down 4.24% to $15.80, suggesting investors may have expected stronger quarterly results or were reacting to broader market conditions.

Quarterly Performance Highlights

OceanFirst reported core earnings of $20.3 million for Q1 2025, with a net interest margin of 2.87% and an efficiency ratio of 65.8%. The bank’s total assets reached $13.3 billion, with net loans of $10.1 billion and deposits of $10.2 billion.

"Our first quarter results demonstrate continued stability in our core operations while we invest in strategic growth initiatives," stated Christopher Maher, Chairman and CEO of OceanFirst Financial Corp, according to the presentation materials.

The company’s balance sheet metrics showed solid capital positions with a CET1 ratio of 11.2% and tangible equity to tangible assets of 9.2%. Non-performing loans remained low at 0.29% of total loans, reflecting the bank’s conservative credit approach.

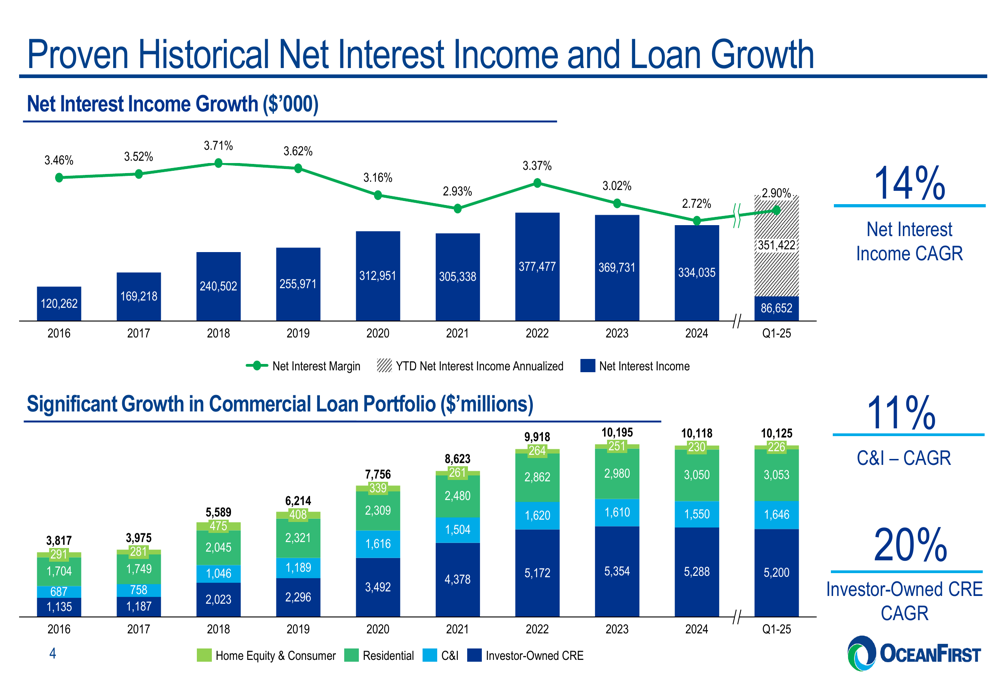

As shown in the following chart, OceanFirst has maintained consistent net interest income growth over time, with a 14% CAGR from 2016 to Q1 2025:

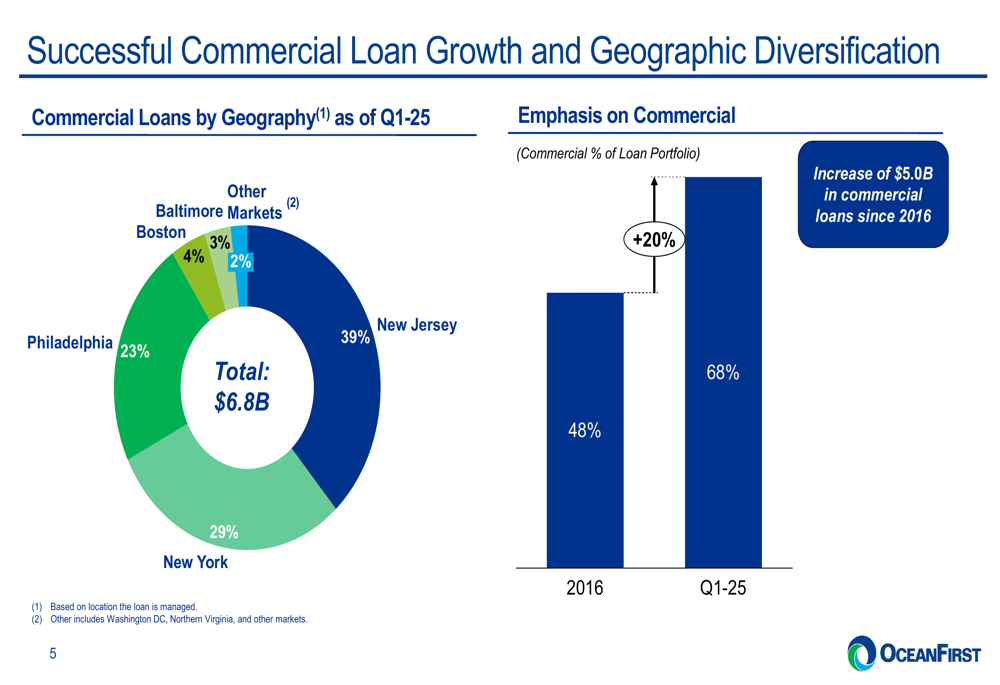

The bank’s loan portfolio continues to shift toward commercial lending, which now represents 68% of total loans compared to 48% in 2016. This strategic shift has been accompanied by geographic diversification across the Northeast corridor.

As illustrated in this geographic breakdown of commercial loans:

Strategic Initiatives

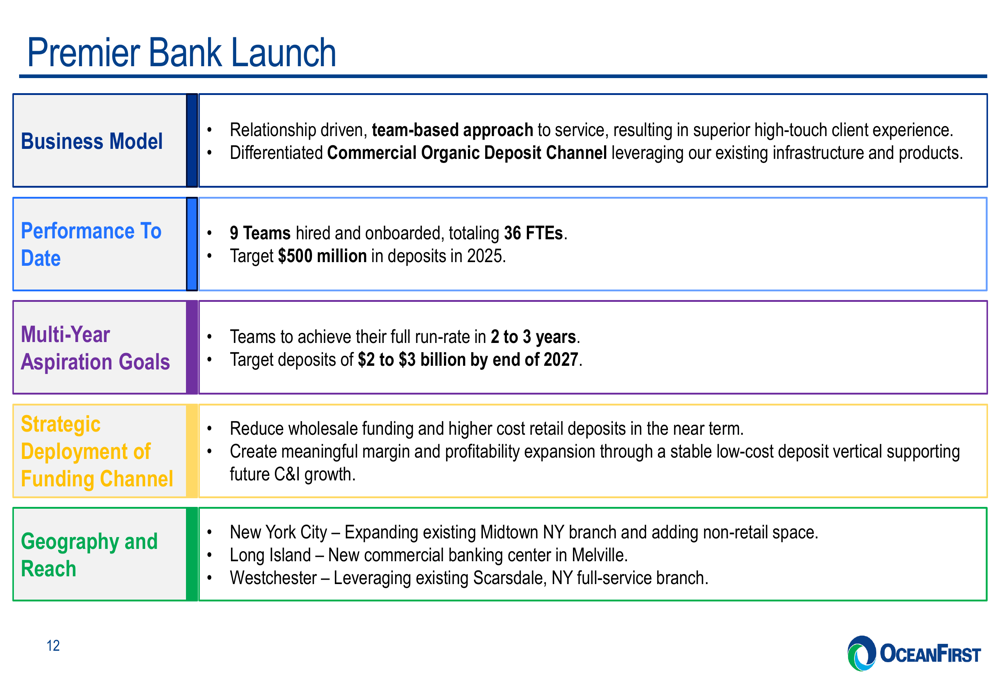

The most significant strategic development highlighted in the presentation is the launch of OceanFirst’s Premier Banking initiative. The company has already hired nine teams totaling 36 full-time employees, with ambitious deposit growth targets.

"We’re targeting $500 million in deposits in 2025 through our Premier Banking initiative, with multi-year aspirational goals of $2 to $3 billion by the end of 2027," the presentation noted. The initiative will focus on expanding in New York City, Long Island, and Westchester markets.

The following slide details the Premier Banking strategy and goals:

This initiative represents a significant investment in relationship-driven banking, with the company expecting an increase in quarterly expense run-rate of approximately 10%, including $4 million related to Premier Bank hires.

Loan Portfolio and Credit Quality

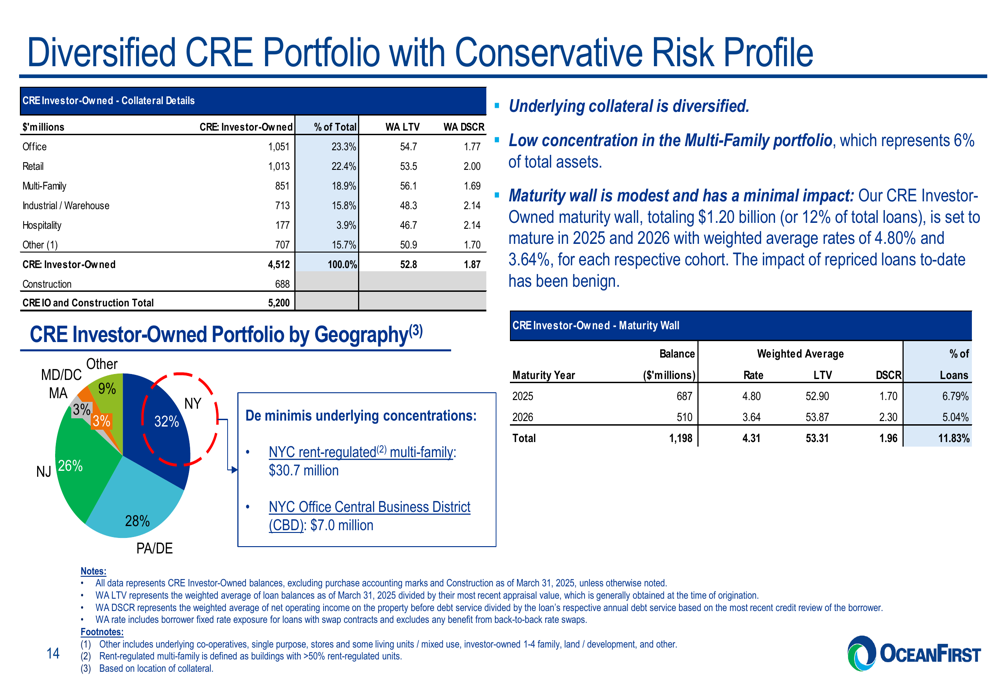

OceanFirst’s presentation emphasized its conservative approach to credit risk, particularly within its commercial real estate portfolio. The bank’s CRE investor-owned portfolio is diversified across property types, with office space representing 9.8% of total loans.

The detailed breakdown of the CRE portfolio shows the following composition:

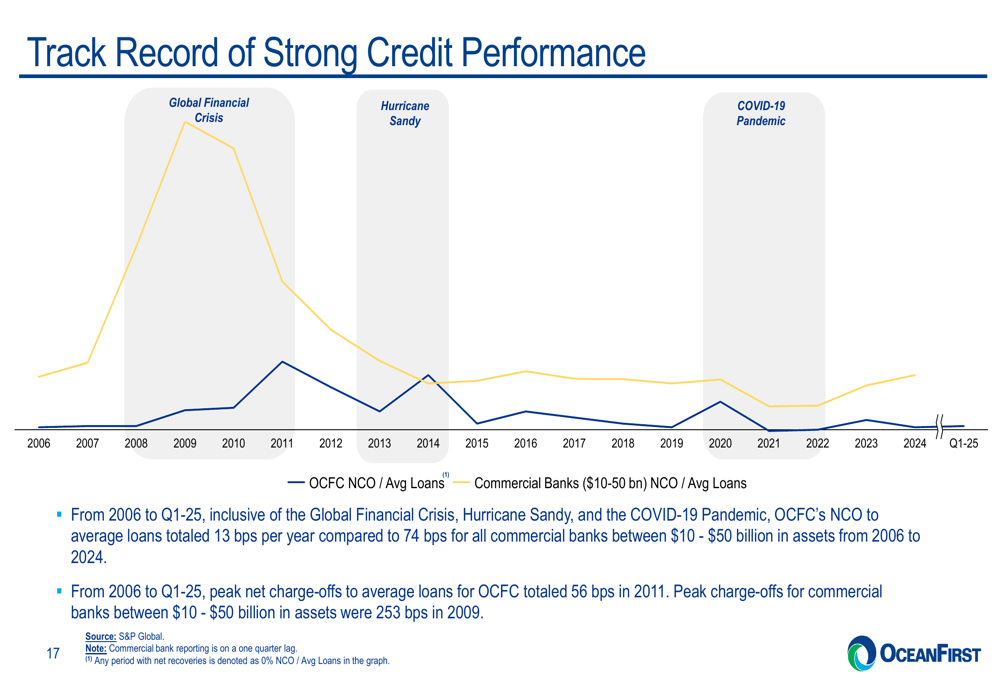

The bank highlighted its strong historical credit performance through various economic cycles, including the Global Financial Crisis, Hurricane Sandy, and the COVID-19 pandemic. OceanFirst’s net charge-offs to average loans have totaled just 13 basis points per year compared to 74 basis points for commercial banks of similar size from 2006 to 2024.

This chart illustrates the bank’s credit performance through economic cycles:

Non-performing loans and assets remained low in Q1 2025, with the allowance for credit losses at 0.83% of total loans, up from 0.73% in Q1 2024, indicating some additional provisioning for potential future credit issues.

Capital Management and Returns

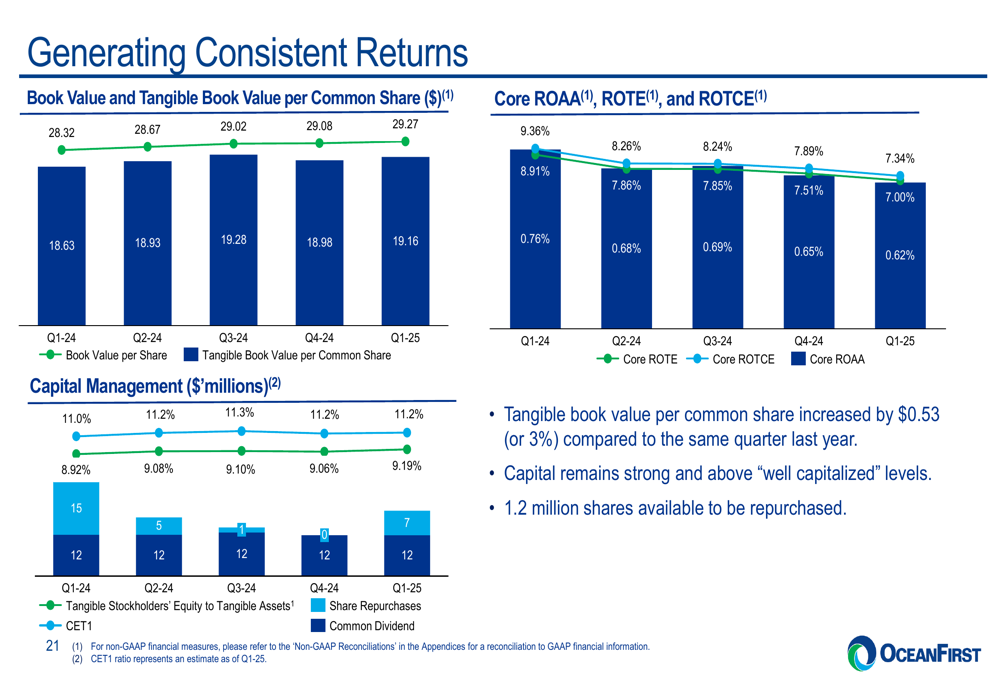

OceanFirst has demonstrated consistent growth in tangible book value per share, which has increased by 55.4% since 2013, while total capital return per share has grown by 143.0% over the same period.

The following chart shows the growth in book value and tangible book value per share:

The company reported that it repurchased 398,395 shares during the quarter ended March 31, 2025, and noted that 1.2 million shares remain available for repurchase under its current authorization. Additionally, OceanFirst mentioned the redemption of preferred equity during the quarter, which should benefit common shareholders going forward.

Forward-Looking Statements

Looking ahead to Q2 2025, OceanFirst management provided a cautiously optimistic outlook, projecting:

- Mid-single digit annualized loan growth

- Deposit growth consistent with loan growth

- Stable to modest uptick in net interest income

- Continued benign credit outlook

- Relatively stable other income

- Increase to expense run-rate

- Robust CET1 ratio (>10%)

The bank’s focus on relationship banking through its Premier Banking initiative, combined with its conservative credit approach and geographic diversification strategy, positions it to navigate the current economic environment while pursuing sustainable growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.