Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

OceanFirst Financial Corp. (NASDAQ:OCFC) released its second quarter 2025 earnings presentation on July 25, highlighting a core diluted earnings per share of $0.31 and continued progress on strategic initiatives. The company’s stock closed at $18.24 prior to the earnings release, down 2% in the most recent trading session, but still well above its 52-week low of $14.29.

The bank’s Q2 results show a slight decline from the Q1 2025 EPS of $0.35, though the company has maintained its focus on expanding its net interest margin and building out its Premier Banking initiative to drive future growth.

Quarterly Performance Highlights

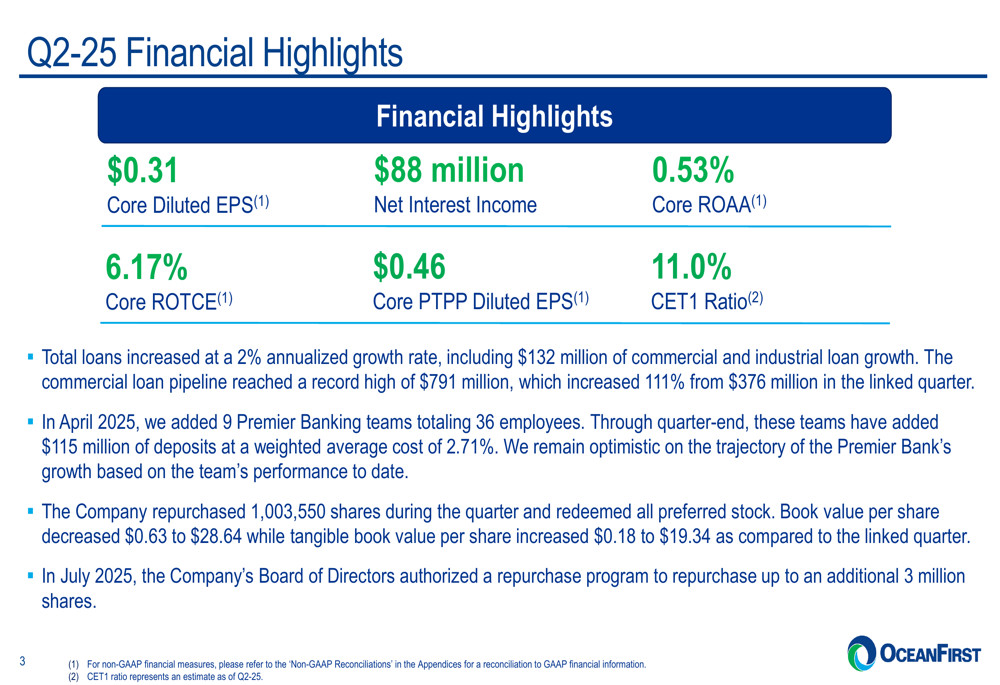

OceanFirst reported core diluted EPS of $0.31 for Q2 2025, with net interest income of $88 million. The company achieved a core return on average assets (ROAA) of 0.53% and core return on tangible common equity (ROTCE) of 6.17%. Total (EPA:TTEF) loans increased at a 2% annualized growth rate, including $132 million of commercial and industrial loan growth.

As shown in the following financial highlights summary:

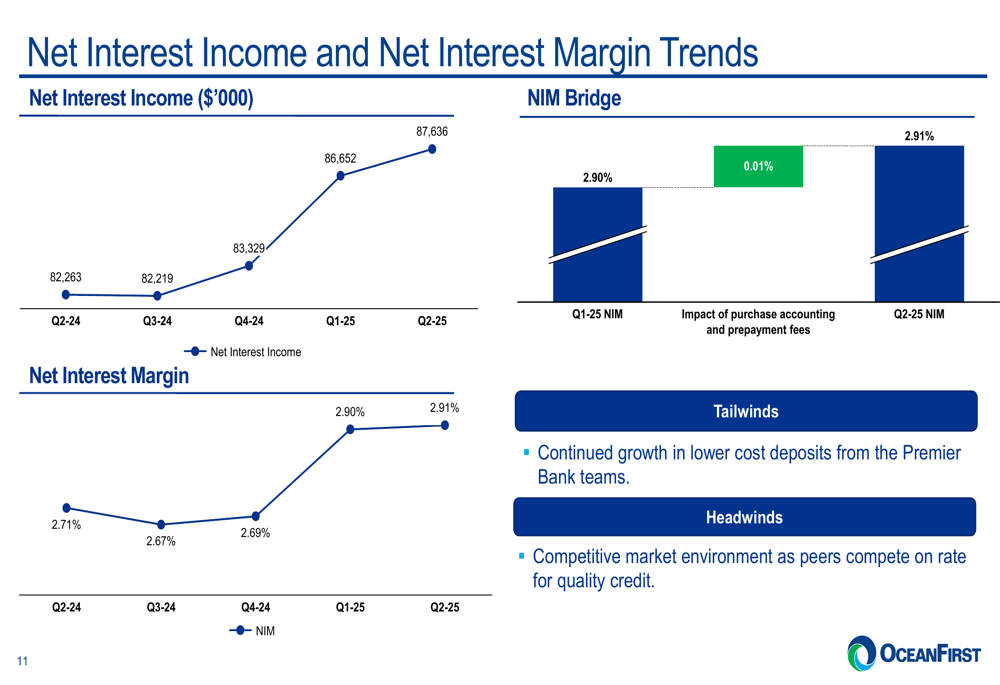

Net interest margin (NIM) improved to 2.91% in Q2 2025, up from 2.71% in the same quarter last year, continuing the positive trend seen in Q1 when the company reported a 21 basis point expansion. This improvement reflects the company’s ongoing efforts to optimize its balance sheet amid a challenging interest rate environment.

The following chart illustrates the steady improvement in net interest income and margin:

Premier Banking Initiative

A key strategic focus for OceanFirst has been its Premier Banking initiative, which added 9 teams totaling 36 full-time employees during the quarter. These teams have already generated $115 million in deposits with a weighted average cost of 2.71% and added 670 new accounts across approximately 200 relationships.

The company’s Premier Banking strategy is illustrated in the following slide:

Management expects these teams to achieve their full run-rate in 2 to 3 years, with a target of $500 million in deposits in 2025, growing to $2-3 billion by the end of 2027. The initiative focuses on a relationship-driven, team-based approach to service in the New York City, Long Island, and Westchester markets.

Loan and Deposit Trends

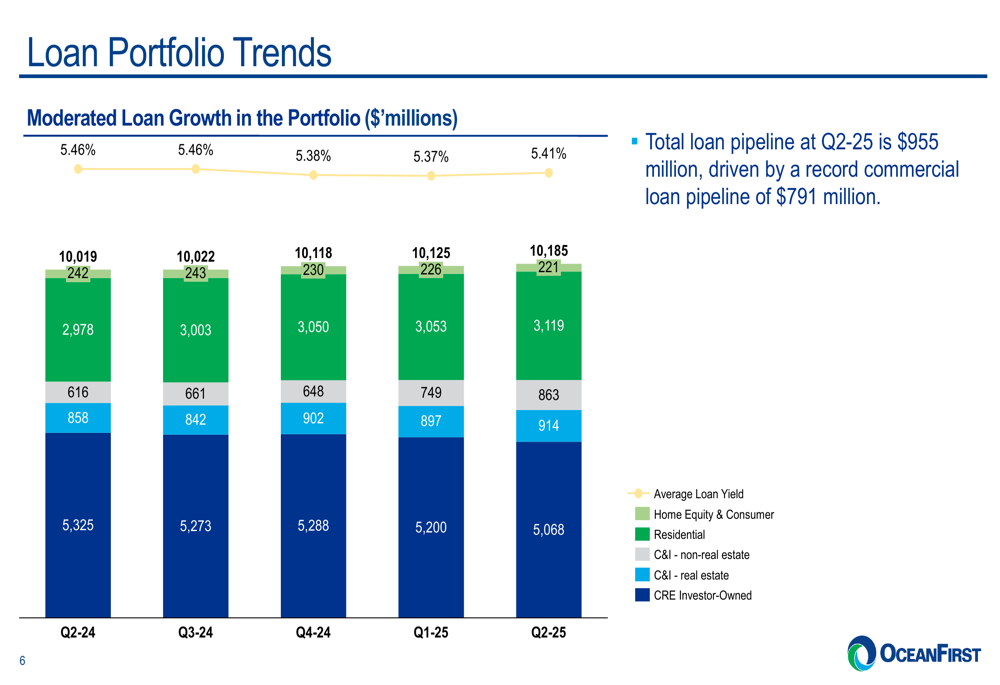

OceanFirst’s loan portfolio showed modest growth, with the total loan pipeline reaching $955 million at the end of Q2, driven by a record commercial loan pipeline of $791 million. The loan yield improved slightly to 5.41% in Q2 2025 from 5.37% in the previous quarter.

The composition of the loan portfolio is detailed in the following chart:

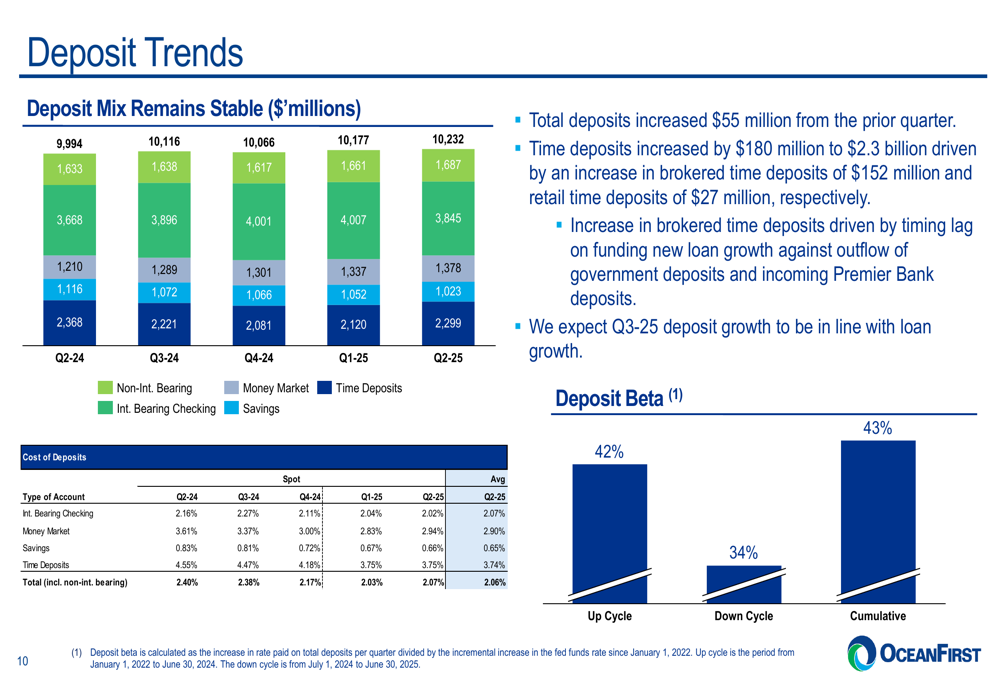

On the deposit side, total deposits increased by $55 million from the prior quarter, with time deposits increasing by $180 million to $2.3 billion. The increase in brokered time deposits was driven by timing lag on funding new loan growth against outflow of government deposits and incoming Premier Bank deposits.

The deposit trends and mix are illustrated here:

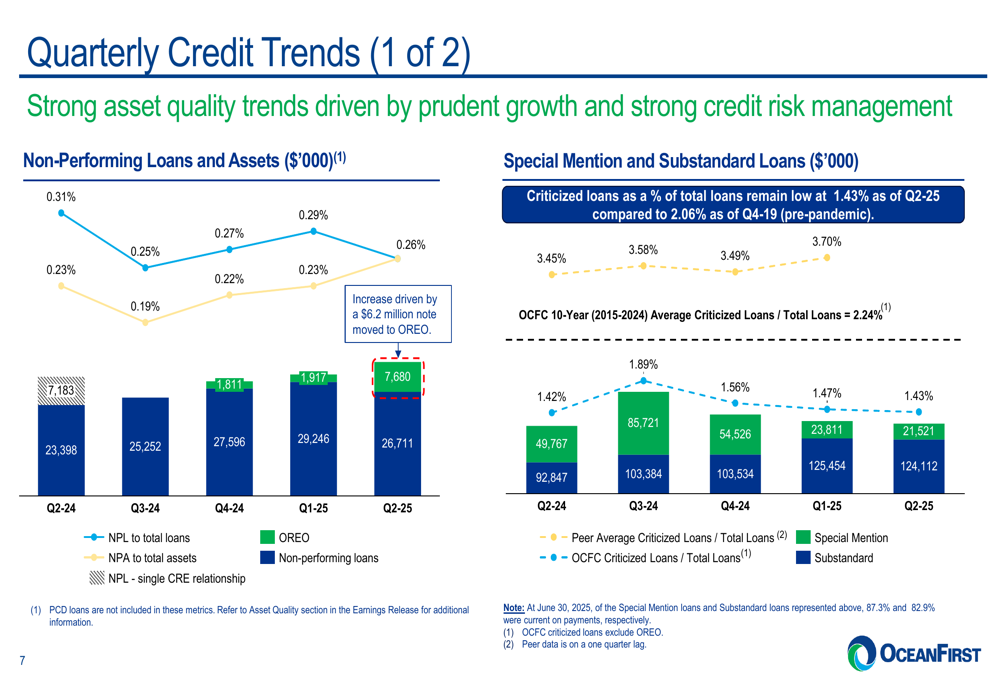

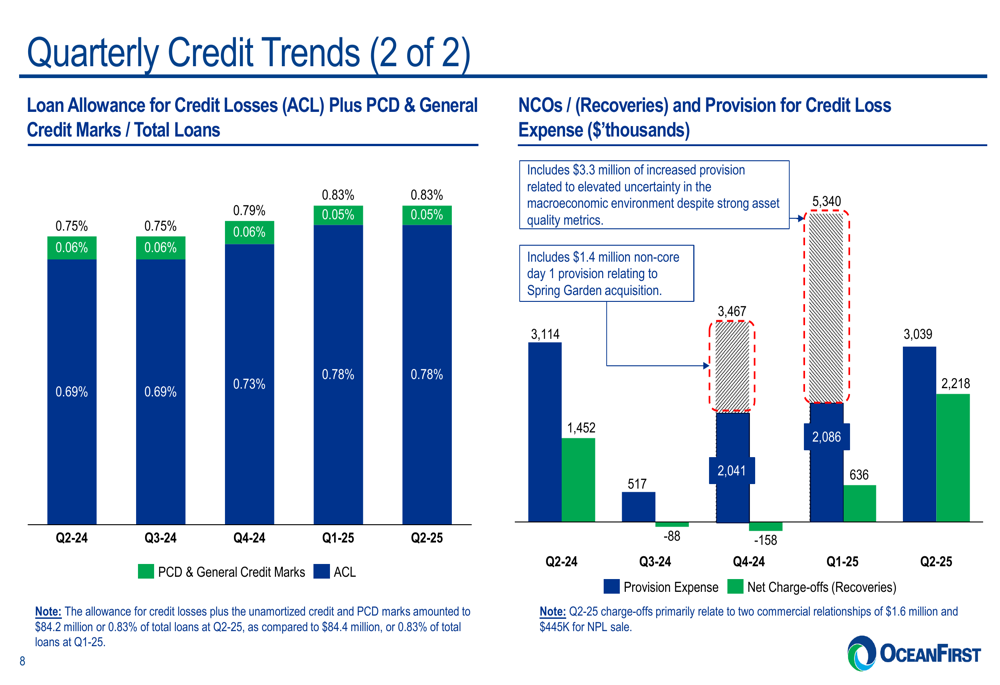

Credit Quality and Risk Management

OceanFirst maintained strong asset quality metrics in Q2 2025, with non-performing loans to total loans decreasing to 0.26% from 0.31% in Q2 2024. Criticized loans remained low at 1.43% of total loans.

The company’s credit quality trends are shown in the following chart:

The allowance for credit losses (ACL) plus purchase credit deteriorated (PCD) and general credit marks to total loans ranged from 0.69% to 0.83% across recent quarters. The Q2 2025 provision included $3.3 million related to elevated uncertainty in the macroeconomic environment despite strong asset quality metrics.

Additional credit metrics are illustrated here:

OceanFirst highlighted its historical track record of strong credit performance, noting that from 2006 to Q2 2025, its net charge-offs to average loans totaled just 13 basis points per year compared to 74 basis points for all commercial banks.

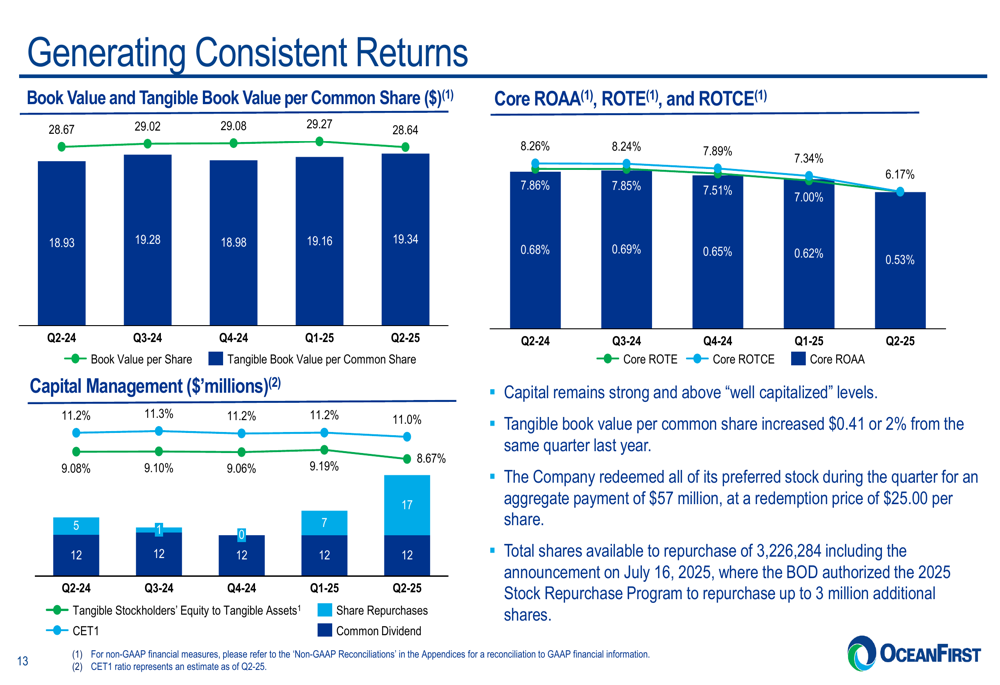

Capital Management and Shareholder Returns

The company maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 11.0%. During the quarter, OceanFirst repurchased 1,003,550 shares and redeemed all preferred stock. Additionally, the board authorized a repurchase program for up to an additional 3 million shares.

Tangible book value per common share increased by $0.41 or 2% from the same quarter last year, as shown in the following chart:

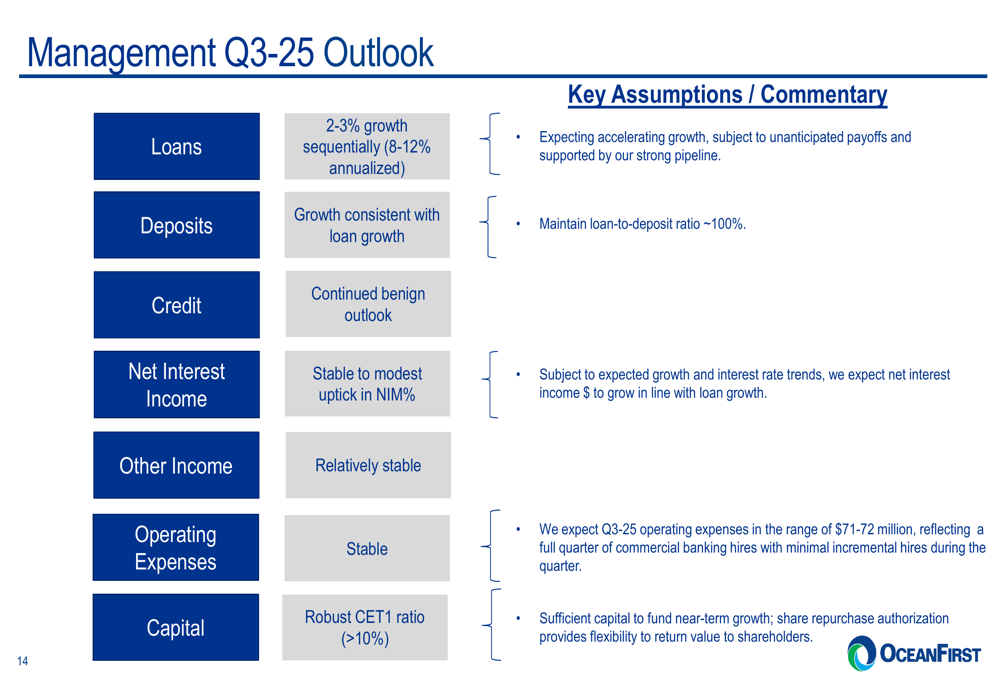

Management Outlook

Looking ahead to Q3 2025, management provided an optimistic outlook, projecting loan growth of 2-3% sequentially (8-12% annualized) and deposit growth consistent with loan growth. The company expects stable to modest improvement in net interest margin percentage and relatively stable other income.

Operating expenses are expected to remain stable at a run-rate of $71-72 million, and the company anticipates maintaining a robust CET1 ratio above 10%.

The detailed Q3 2025 outlook is presented in the following slide:

Competitive Industry Position

OceanFirst emphasized its conservative risk profile, particularly in its commercial real estate (CRE) portfolio. The company highlighted that 96% of its office and construction loans are pass-rated, and 93% are classified as non-Central Business District loans, positioning it well amid concerns about commercial real estate in major urban centers.

The bank also pointed to the historical outperformance of Northeast banks through credit cycles, noting that median net charge-offs for Northeastern headquartered banks averaged 20 basis points during the Global Financial Crisis compared to 50 basis points for banks in other regions.

Despite the slight decrease in EPS from Q1 to Q2, OceanFirst’s focus on expanding its Premier Banking initiative, growing its commercial loan pipeline, and maintaining strong credit quality suggests a strategic positioning for future growth as it navigates the current economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.