Asia stocks rise: Japan surges on Takaichi bets, China buoyed by positive GDP

Introduction & Market Context

Unicaja Banco (BME:UNI) presented its first quarter 2025 results on April 28, showing significant profit growth despite pressure on interest income. The Spanish bank reported a net profit of €158 million, representing a 43% year-over-year increase, while maintaining strong capital levels and improving asset quality metrics. This performance comes amid a challenging interest rate environment that has begun to impact Spanish banks’ net interest income.

The bank’s stock closed at €2.342 on October 14, 2025, representing a 1.65% increase, suggesting continued investor confidence in Unicaja’s performance and strategy. The Q1 results appear to have set a strong foundation for the first half of 2025, which according to recent earnings reports showed a total profit of €338 million for H1.

Quarterly Performance Highlights

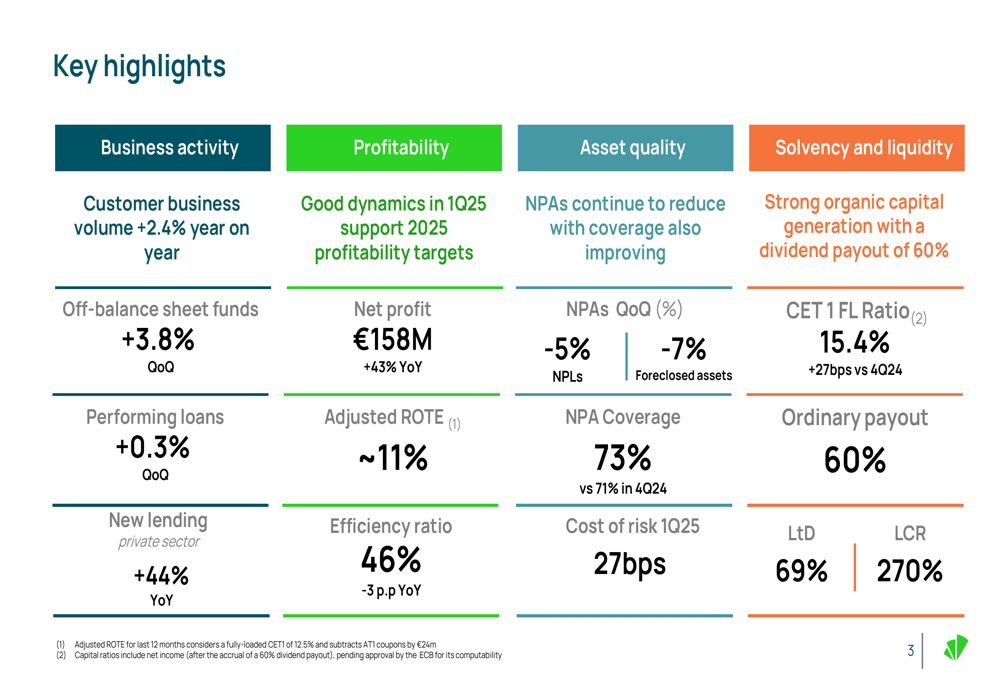

Unicaja delivered a strong start to 2025, with net profit reaching €158 million, up 43% compared to the same period in 2024. This improvement came despite a 5.6% year-over-year decrease in net interest income, as the bank benefited from growth in fee income, improved cost efficiency, and changes in banking tax accounting.

As shown in the following comprehensive overview of key metrics, the bank achieved an adjusted ROTE of approximately 11% and improved its efficiency ratio to 46%, representing a 3 percentage point improvement year-over-year:

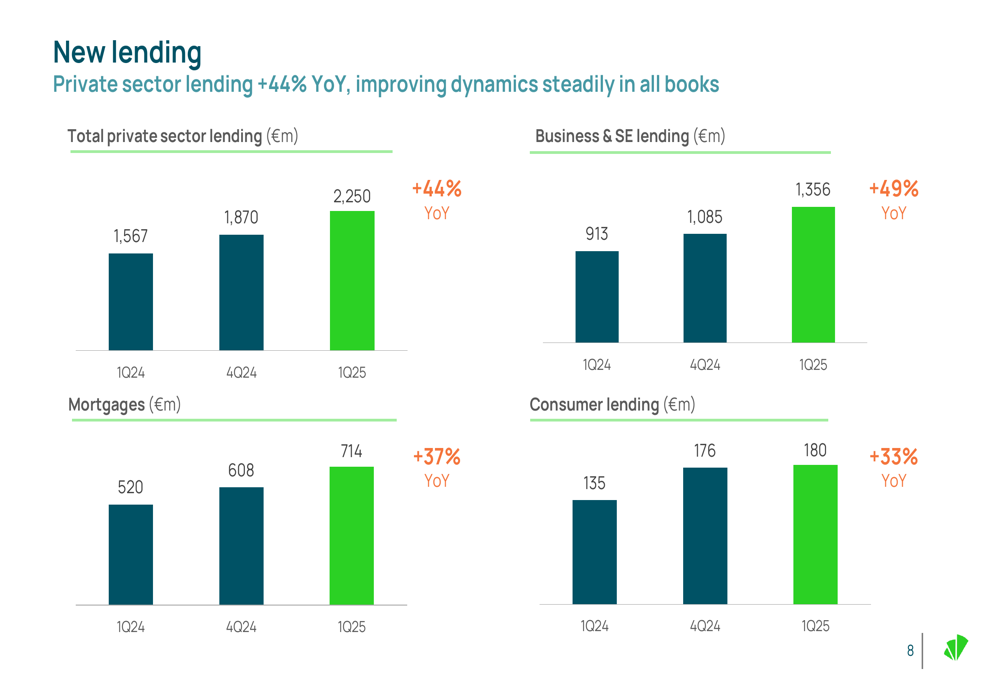

Business volumes showed positive momentum, with customer business volume increasing by 2.4% year-over-year. Off-balance sheet funds grew by 3.8% quarter-on-quarter, while performing loans increased by 0.3% quarter-on-quarter. New lending in the private sector showed particularly strong growth, increasing by 44% year-over-year.

The following chart illustrates the impressive growth in new lending across all major categories:

Detailed Financial Analysis

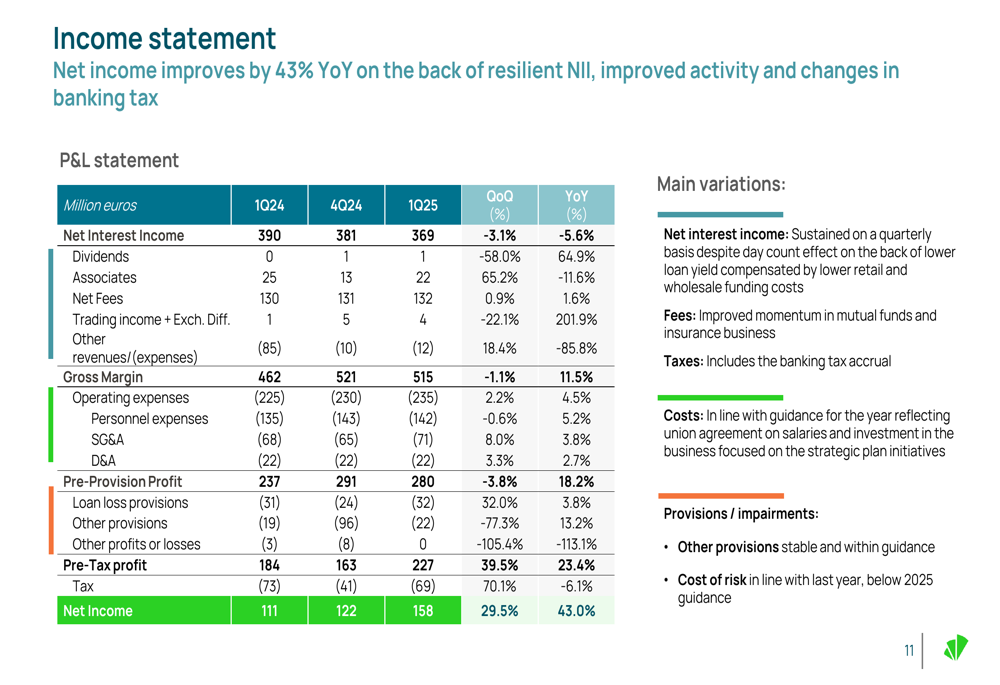

Unicaja’s income statement reflects both challenges and strengths in the current banking environment. Net interest income decreased by 5.6% year-over-year to €369 million, primarily due to the repricing of the loan book in a changing interest rate environment. However, this was partially offset by lower funding costs from both retail and wholesale sources.

The complete income statement shows how the bank managed to achieve significant profit growth despite NII pressure:

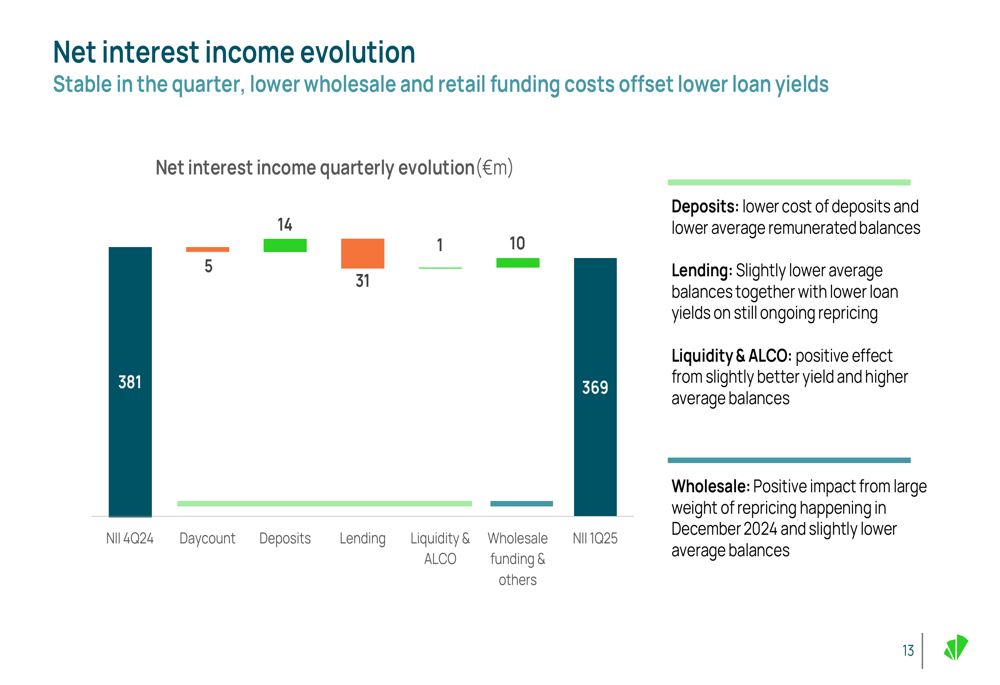

Net interest margin compression was evident, with the customer spread decreasing from 3.59% in Q1 2024 to 3.13% in Q1 2025. Loan yields declined by 46 basis points year-over-year, while deposit costs decreased by only 4 basis points during the same period.

The following waterfall chart provides a detailed breakdown of the factors influencing net interest income during the quarter:

Fee income showed positive momentum, increasing by 1.6% year-over-year to €132 million. This growth was driven primarily by non-banking fees, which increased by 11.7% year-over-year, particularly in mutual funds (+17.0%) and insurance (+6.1%). This shift toward higher-value products is part of Unicaja’s strategic focus on wealth management.

Asset Quality Improvements

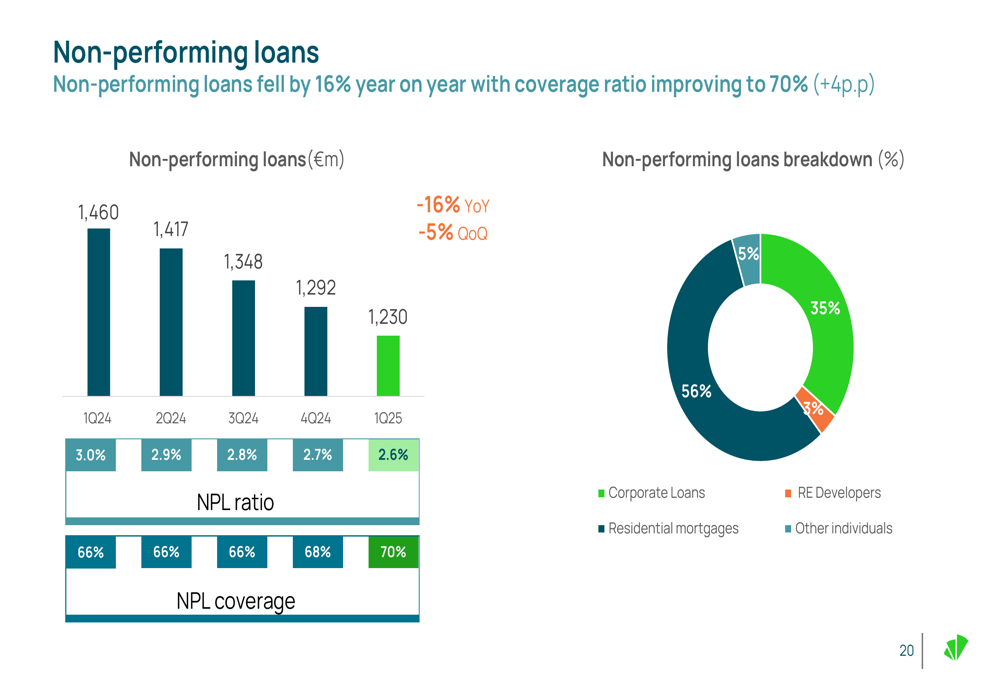

Unicaja continued to strengthen its balance sheet, with significant improvements in asset quality metrics. Non-performing loans fell by 16% year-over-year to €1,230 million, representing 2.6% of total loans, down from 3.0% a year earlier. The coverage ratio for non-performing loans improved to 70%, up 4 percentage points from Q1 2024.

The following chart illustrates the consistent improvement in the bank’s non-performing loan metrics:

Total non-performing assets (NPAs) decreased by 22% year-over-year, with foreclosed assets declining by 30%. The NPA coverage ratio improved to 73%, up from 71% in Q4 2024, providing additional protection against potential losses.

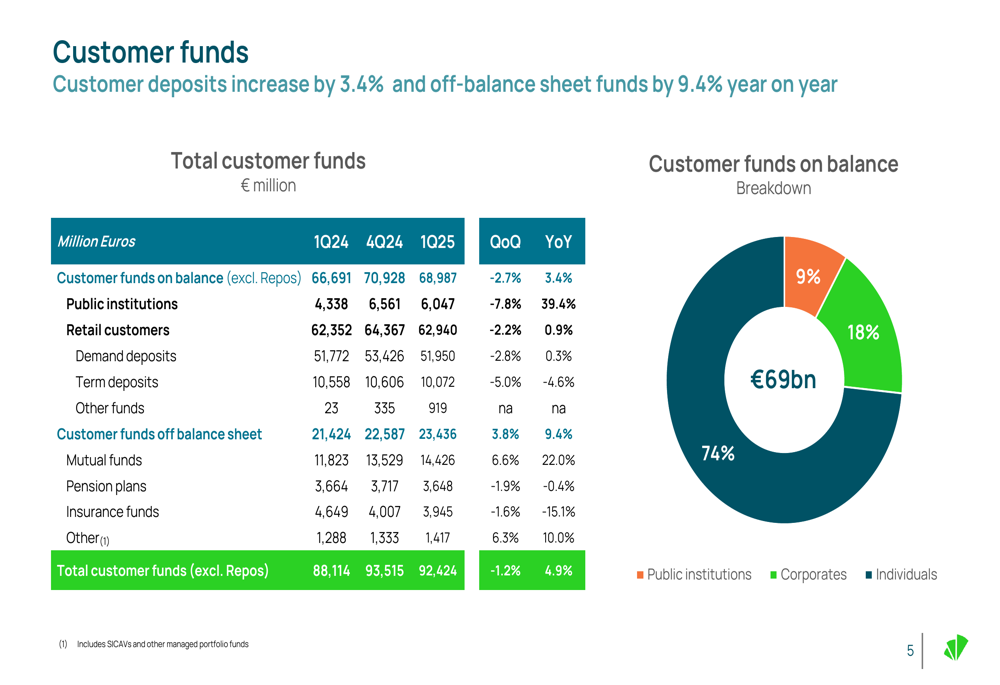

Customer funds showed solid growth, with total customer funds (excluding repos) increasing by 4.9% year-over-year to €92,424 million. Off-balance sheet funds grew by 9.4% year-over-year, driven by a 22.0% increase in mutual funds, reflecting strong performance in the bank’s wealth management business.

As shown in the following breakdown of customer funds, the bank has maintained a stable funding structure with a healthy mix of retail and institutional deposits:

Strategic Initiatives and Outlook

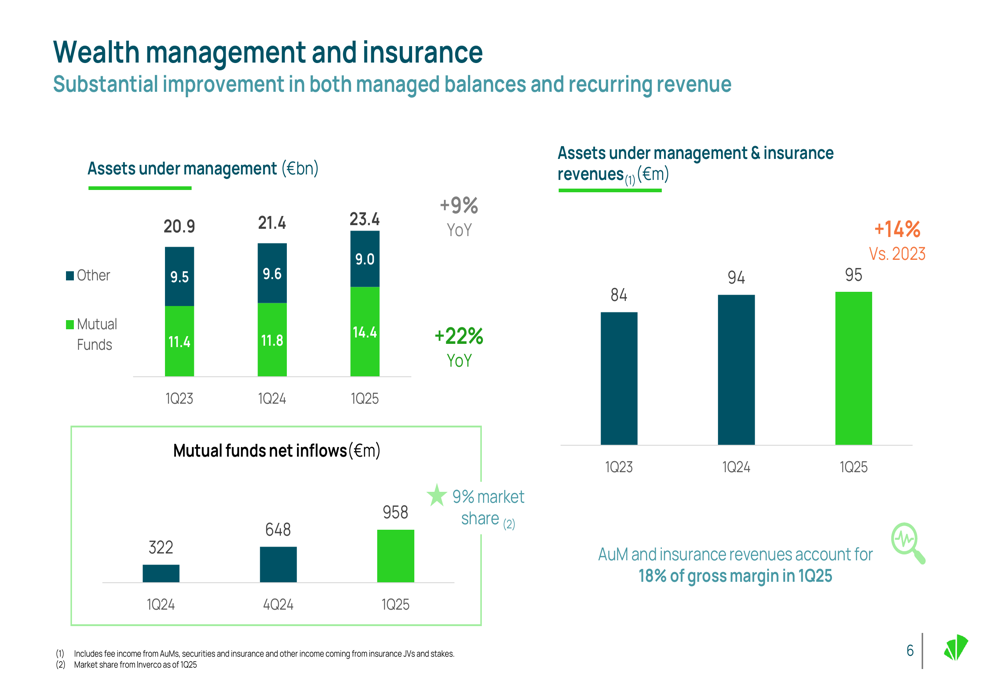

Unicaja’s strategic focus on wealth management continues to show positive results, with assets under management increasing by 9% year-over-year to €23.4 billion. The bank reported strong net inflows into mutual funds, with €958 million in Q1 2025, compared to €322 million in Q1 2024, reflecting growing customer interest in investment products.

The following chart illustrates the strong growth in assets under management and related revenues:

The bank also highlighted its progress on ESG initiatives, with 30% of new lending to corporates in Q1 2025 being classified as sustainable. Unicaja reported that 61% of its funds are now classified under Articles 8 and 9 of the EU’s Sustainable Finance Disclosure Regulation, demonstrating its commitment to sustainable finance.

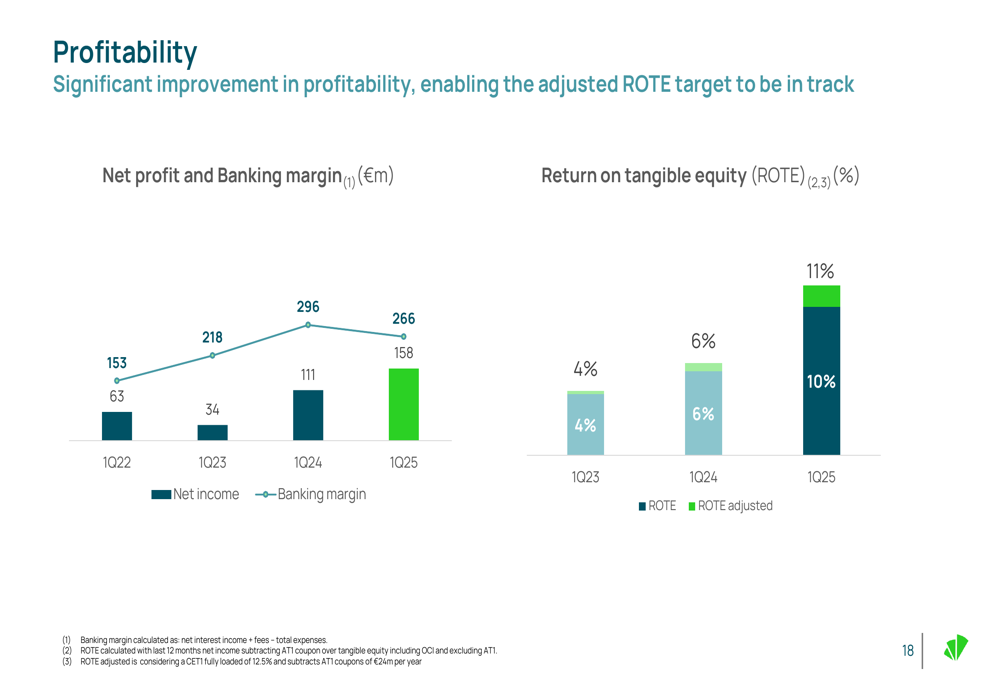

Unicaja’s profitability metrics showed significant improvement, with adjusted ROTE reaching approximately 11%, positioning the bank to achieve its 2025 profitability targets. The bank’s strong capital position, with a CET1 fully-loaded ratio of 15.4% (up 27 basis points from Q4 2024), provides a solid foundation for future growth and shareholder returns.

The following chart shows the positive trajectory in the bank’s profitability metrics:

The strong Q1 results appear to have set a positive trajectory for the remainder of 2025. According to recent earnings reports, Unicaja achieved a net profit of €338 million for the first half of 2025, representing a 15% increase year-over-year, with business volumes growing by 4% and mutual fund balances increasing by 25%. The bank has also increased its interim dividend by 10% to €0.066 per share, reflecting confidence in its financial performance and outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.