Street Calls of the Week

Introduction & Market Context

Baker Hughes (NASDAQ:BKR) delivered strong third-quarter 2025 results on October 24, exceeding analyst expectations with adjusted earnings per share of $0.68 compared to the forecasted $0.62. Despite the positive performance, the company’s stock declined 3.94% to $48.89 in after-hours trading, reflecting broader market concerns rather than company-specific issues.

The energy technology company reported robust order growth across its segments, particularly in its Industrial & Energy Technology (IET) division, highlighting the company’s strategic positioning in natural gas and LNG markets as global energy demand continues to evolve.

"This is the age of gas, and Baker Hughes is well positioned to benefit," CEO Lorenzo Simonelli emphasized during the earnings call, underscoring the company’s focus on capitalizing on strong natural gas and LNG demand fundamentals.

Quarterly Performance Highlights

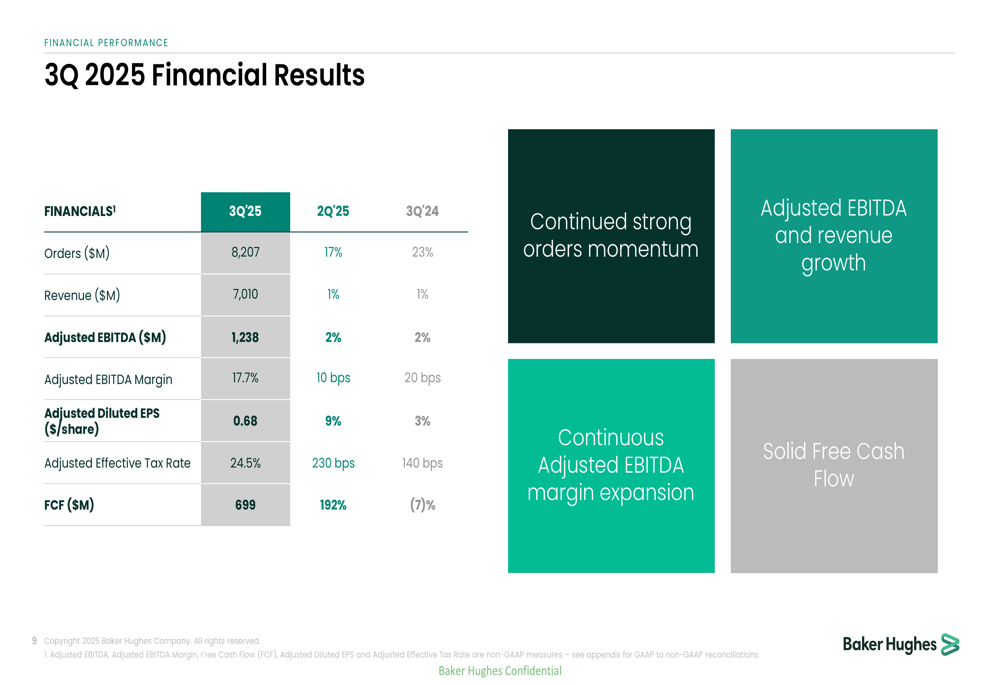

Baker Hughes reported total revenue of $7.01 billion for Q3 2025, representing a modest 1% increase both sequentially and year-over-year, but exceeding analyst expectations of $6.82 billion. The company’s adjusted EBITDA reached $1.24 billion, up 2% compared to both the previous quarter and the same period last year.

As shown in the following financial results summary:

Orders were particularly strong at $8.21 billion, surging 17% sequentially and 23% year-over-year, demonstrating robust demand for Baker Hughes’ products and services. Free cash flow generation was impressive at $699 million, up 192% quarter-over-quarter despite a 7% year-over-year decline.

The company’s adjusted EBITDA margin continued its expansion trend, reaching 17.7% in Q3, an improvement of 10 basis points sequentially and 20 basis points year-over-year. This margin progression aligns with Baker Hughes’ long-term strategy to reach 20% adjusted EBITDA margins by 2028.

Segment Performance

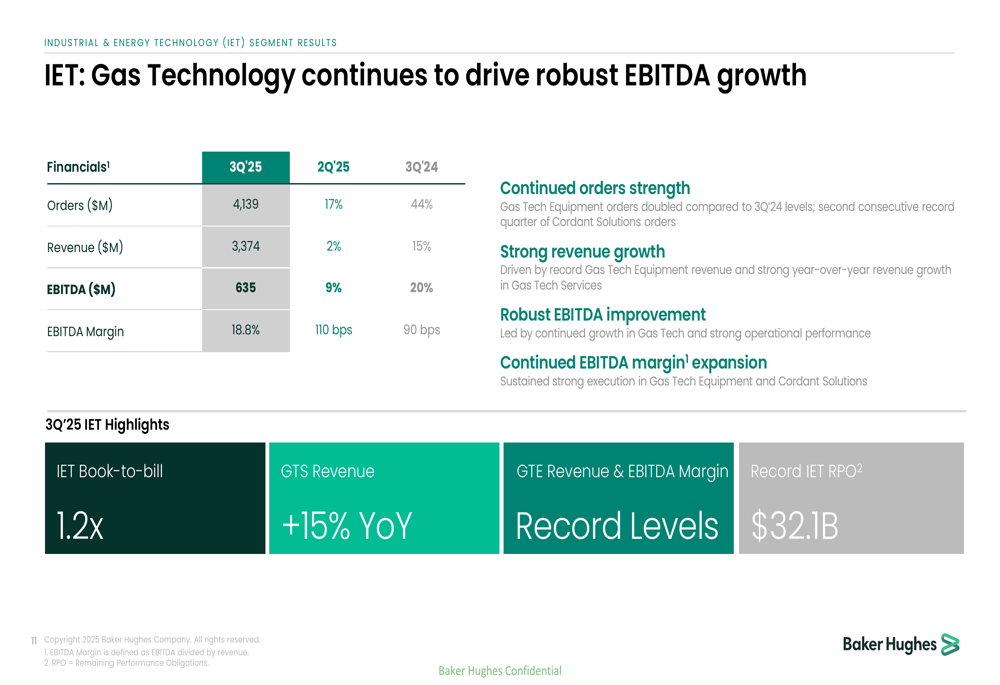

Baker Hughes’ Industrial & Energy Technology (IET) segment delivered exceptional results, with orders of $4.14 billion representing a 17% sequential increase and a remarkable 44% year-over-year growth. This performance was driven by strong demand for LNG equipment, record orders for the company’s Cordant™ technology, and accelerating power generation awards.

The IET segment’s financial performance is illustrated in the following slide:

The segment achieved record revenue and EBITDA margin levels, with revenue growing 15% year-over-year to $3.37 billion and EBITDA increasing 20% year-over-year to $635 million. The EBITDA margin expanded to 18.8%, up 110 basis points sequentially and 90 basis points year-over-year.

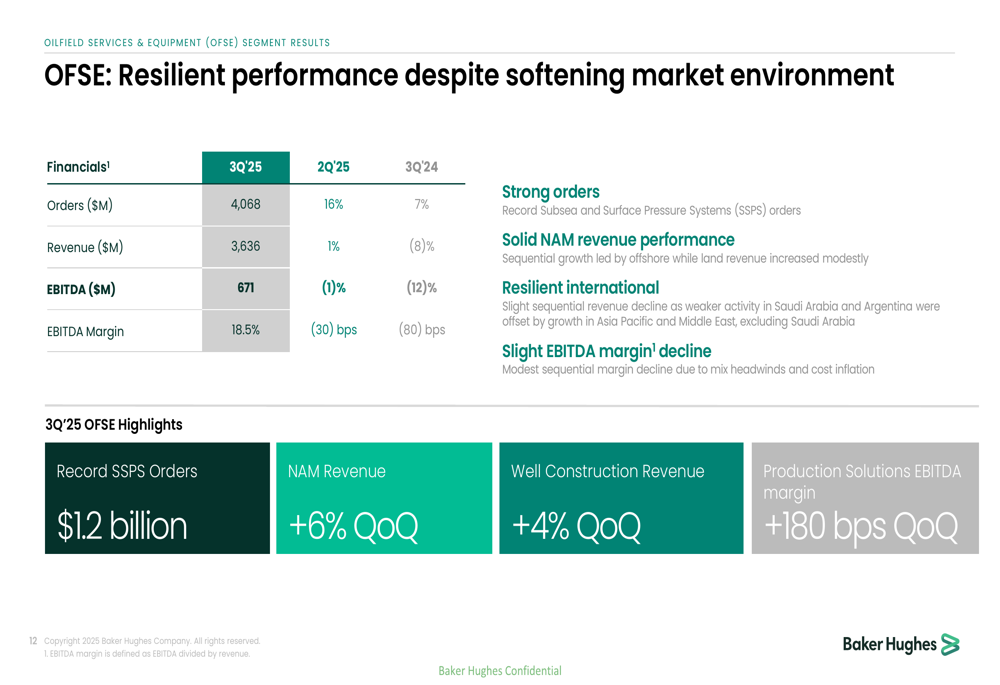

Meanwhile, the Oilfield Services & Equipment (OFSE) segment showed resilience despite challenging market conditions, with orders of $4.07 billion representing a 16% sequential increase and 7% year-over-year growth. The segment achieved record Subsea & Surface Pressure Systems (SSPS) orders of $1.2 billion, driven by large subsea tree awards in Brazil and Turkiye.

The following slide details the OFSE segment’s performance:

While OFSE revenue increased 1% sequentially to $3.64 billion, it declined 8% year-over-year, reflecting the expected softening in upstream spending. EBITDA decreased 1% sequentially and 12% year-over-year to $671 million, with margins declining slightly to 18.5%.

Strategic Initiatives

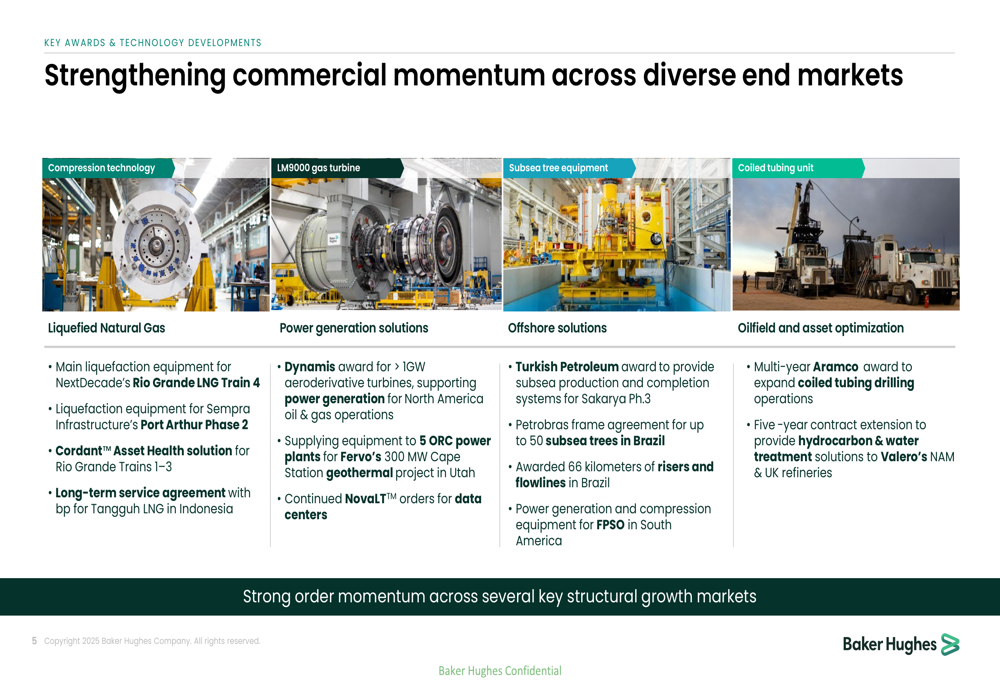

Baker Hughes continues to secure significant contract wins across various end markets, reinforcing its strategic positioning in the energy transition. The company highlighted several major awards in its presentation:

In the LNG sector, Baker Hughes secured contracts for main liquefaction equipment for NextDecade’s Rio Grande LNG Train 4 and equipment for Sempra Infrastructure’s Port Arthur Phase 2. The company also won a Dynamis award for over 1GW of aeroderivative turbines and equipment for five ORC power plants for Fervo’s 300 MW Cape Station geothermal project in Utah.

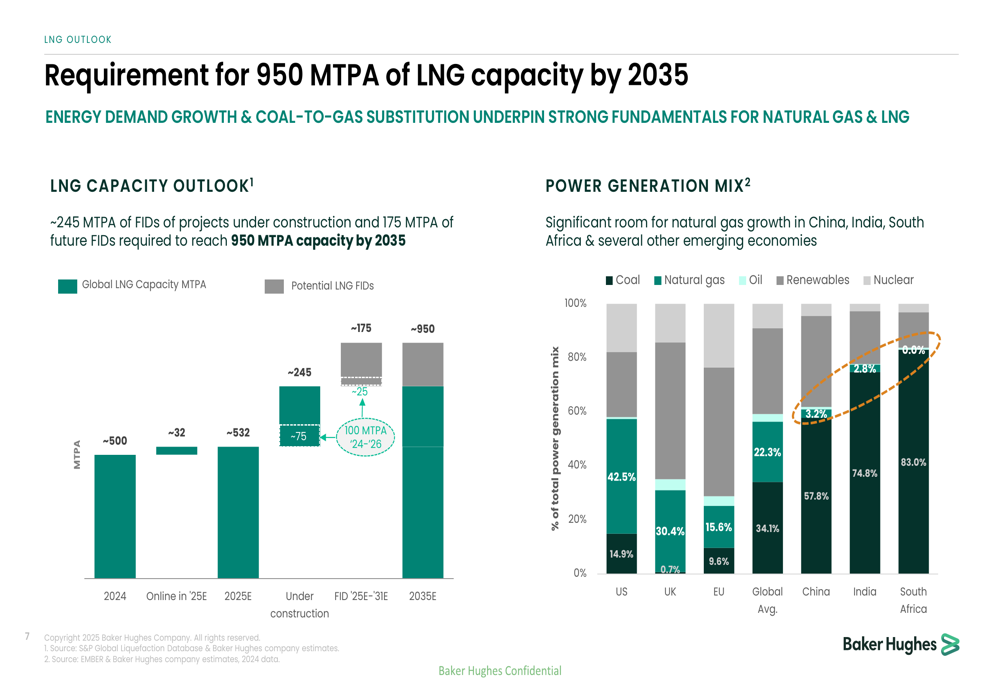

The company’s strategic focus on natural gas and LNG is supported by strong market fundamentals, as illustrated in the following slide:

Baker Hughes projects that global LNG capacity will need to reach 950 MTPA by 2035, requiring approximately 245 MTPA of projects under construction and 175 MTPA of future FIDs. The power generation mix comparison demonstrates significant room for natural gas growth in emerging economies like China, India, and South Africa.

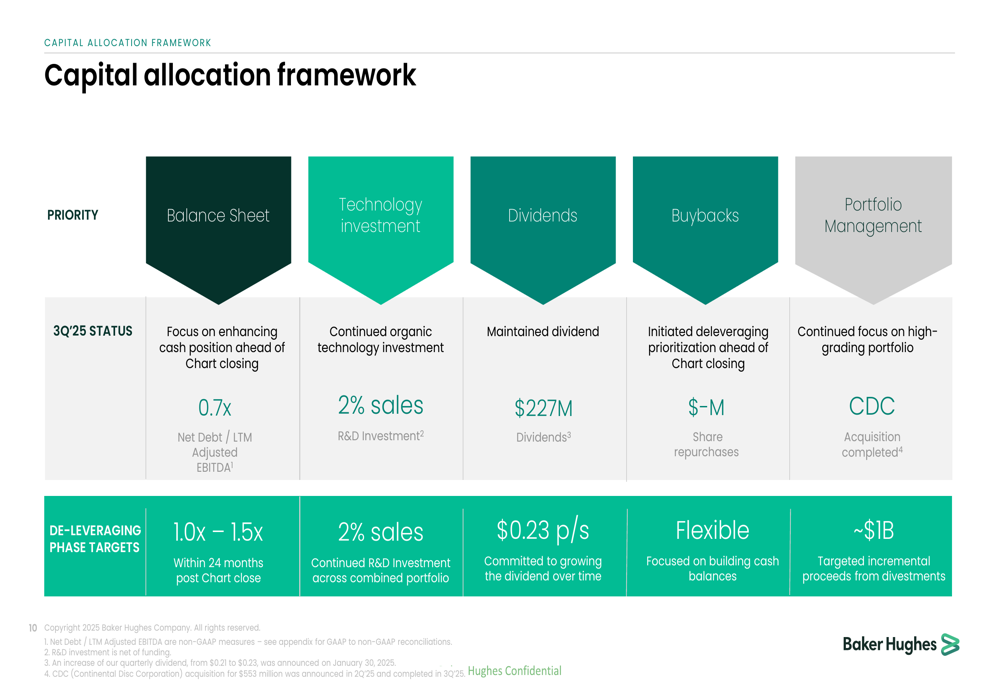

Capital Allocation and Financial Strategy

As Baker Hughes prepares for the closing of its acquisition of Chart Industries, the company is focusing on enhancing its cash position and maintaining financial flexibility. The capital allocation framework outlines the company’s priorities:

Baker Hughes is targeting a Net Debt to LTM Adjusted EBITDA ratio of 0.7x ahead of the Chart closing, with plans to deleverage to 1.0x-1.5x within 24 months post-close. The company maintained its dividend at $0.23 per share (increased from $0.21 previously) and is prioritizing building cash balances over share buybacks in the near term.

The company also continues to focus on high-grading its portfolio, having completed the CDC acquisition and targeting approximately $1 billion in additional proceeds from divestments.

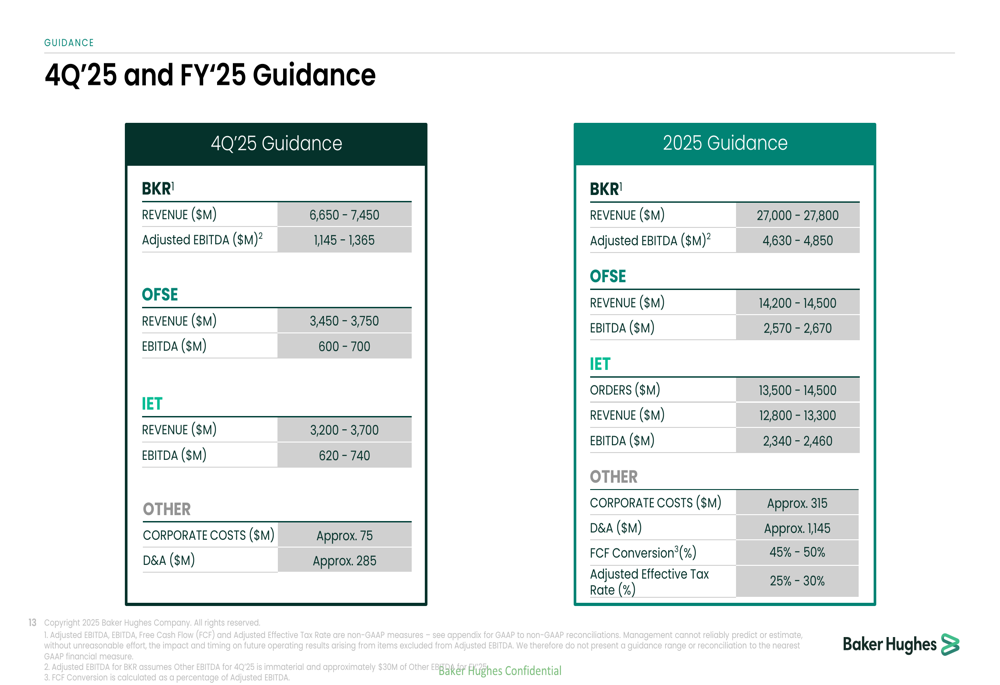

Forward-Looking Guidance

Baker Hughes provided guidance for both the fourth quarter and full year 2025:

For Q4 2025, the company expects revenue between $6.65 billion and $7.45 billion and adjusted EBITDA between $1.15 billion and $1.37 billion. For the full year 2025, Baker Hughes projects revenue of $27.0-27.8 billion and adjusted EBITDA of $4.63-4.85 billion.

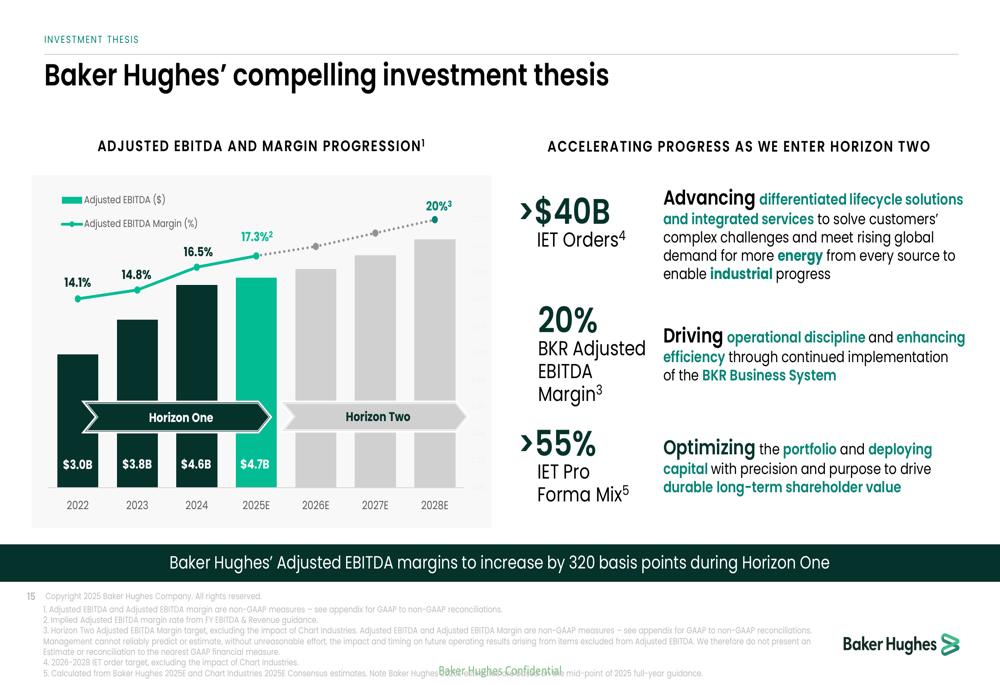

Looking further ahead, the company outlined its long-term investment thesis and targets:

Baker Hughes aims to achieve over $40 billion in IET orders by 2028, with adjusted EBITDA margins reaching 20% and IET representing over 55% of the company’s pro forma mix. The company’s strategy focuses on advancing differentiated lifecycle solutions, driving operational discipline, and optimizing its portfolio.

Market Reaction & Analyst Perspectives

Despite the strong quarterly results and positive outlook, Baker Hughes’ stock declined 3.94% to $48.89 in after-hours trading following the earnings release. This reaction appears disconnected from the company’s operational performance and may reflect broader market concerns or profit-taking after the stock’s strong performance over the past six months, during which it delivered a 25.6% return.

The stock remains near its 52-week high of $50.93, suggesting overall investor confidence in the company’s strategy and execution. According to the earnings call, analysts focused their questions on Baker Hughes’ power generation opportunities and margin expansion strategy, particularly regarding the integration planning for the Chart Industries acquisition.

CFO Ahmed Moghal emphasized the company’s margin expansion goals during the call, stating that Baker Hughes is aiming for "total company margins of 20% by 2028," which would represent a significant improvement from the current 17.7% level.

As Baker Hughes continues to execute its strategy focused on natural gas and LNG markets, investors will be watching closely to see if the company can maintain its momentum in orders and continue its margin expansion trajectory while successfully integrating the Chart Industries acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.