TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Lloyds Banking Group (LSE:LON:LLOY) presented its half-year 2025 results on July 24, showing continued momentum across its business lines amid what the bank describes as a "constructive operating environment" in the UK. The banking group reported statutory profit after tax of £2.5 billion, up 4% year-over-year, supported by growth in both net interest income and other income sources.

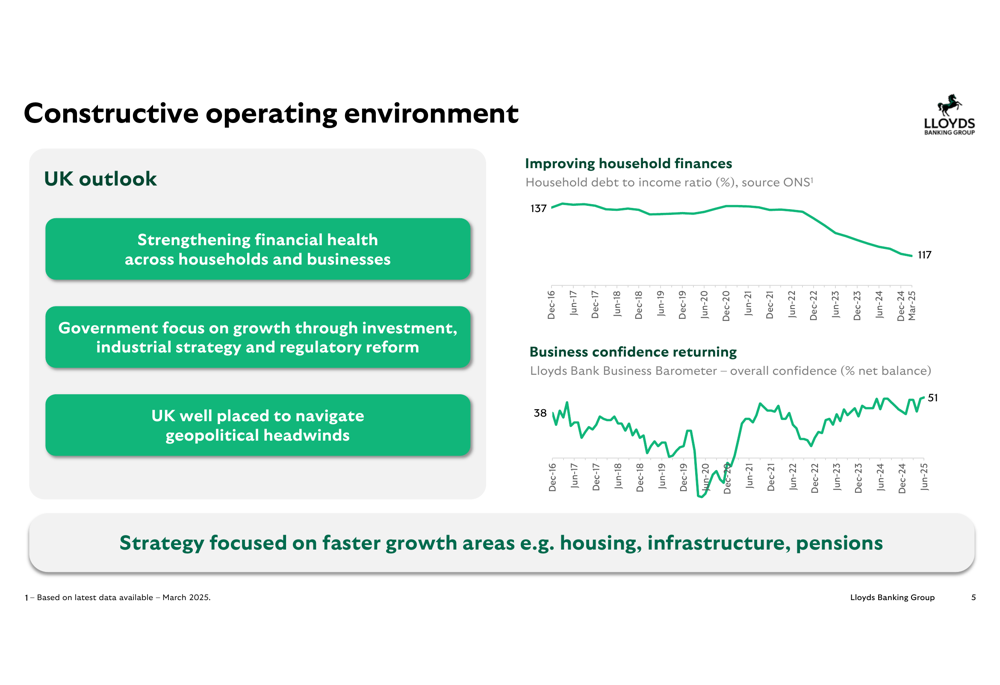

The bank’s presentation highlighted improving UK economic conditions, with strengthening household finances and returning business confidence creating favorable conditions for growth. This comes after Lloyds reported £1.1 billion in statutory profit for Q4 2024, indicating sustained positive performance into 2025.

As shown in the following chart, Lloyds is benefiting from improving household finances and business confidence in the UK market:

Quarterly Performance Highlights

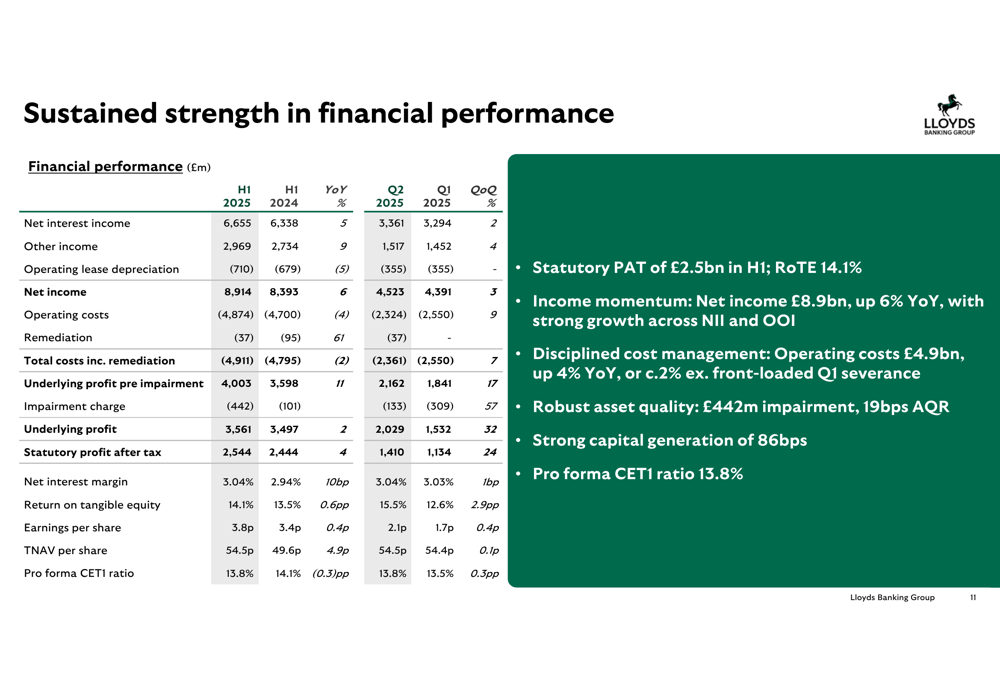

Lloyds delivered strong financial results for H1 2025, with net income reaching £8.9 billion, up 6% compared to H1 2024. This growth was driven by a 5% increase in net interest income to £6.7 billion and a 9% rise in other income to £3.0 billion. The bank maintained a net interest margin of 304 basis points in Q2, up 1 basis point quarter-on-quarter.

The comprehensive financial performance is illustrated in this table from the presentation:

Return on tangible equity (RoTE) improved to 14.1% for the half-year, up from 13.5% in the same period last year. The bank also reported strong capital generation of 86 basis points, supporting a 15% increase in the interim dividend compared to H1 2024.

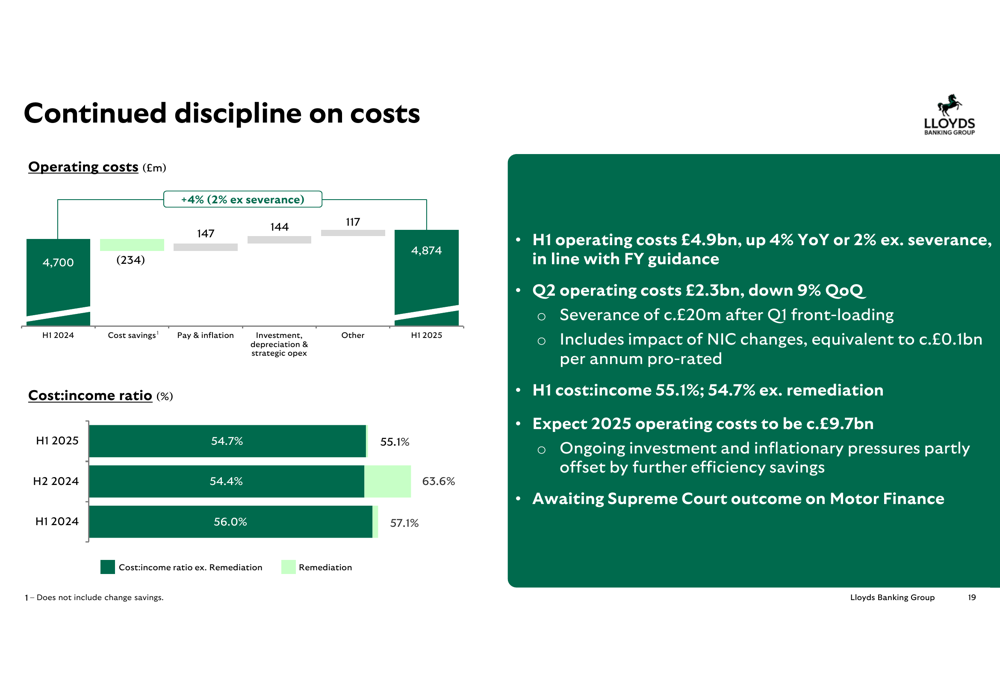

Operating costs increased by 4% year-over-year to £4.9 billion, though the bank noted this would be approximately 2% excluding front-loaded severance costs. This represents an improvement from the 6% year-over-year cost increase reported in Q4 2024, suggesting better cost control in recent months.

The following slide details the bank’s cost discipline approach:

Detailed Financial Analysis

Lloyds reported continued growth in both lending and deposits during the first half of 2025. Total (EPA:TTEF) lending increased by 3% year-to-date to £471.0 billion, with mortgage balances up £5.6 billion to £317.9 billion. Commercial banking lending grew by £1.2 billion in H1, or £2.0 billion when excluding government lending repayments.

On the funding side, deposits increased by 2% year-to-date to £493.9 billion, with commercial deposits showing particularly strong growth of 5% in H1. The bank’s loan-to-deposit ratio remains healthy, supporting continued lending growth.

Asset quality remained robust with an impairment charge of £442 million in H1, representing an asset quality ratio of 19 basis points. The bank noted stable early warning indicators and healthy customer behaviors despite the evolving economic environment.

The bank’s capital position remains strong with a pro forma CET1 ratio of 13.8%, compared to 13.5% reported at the end of Q4 2024. This provides substantial capacity for continued business growth and shareholder returns.

Strategic Initiatives

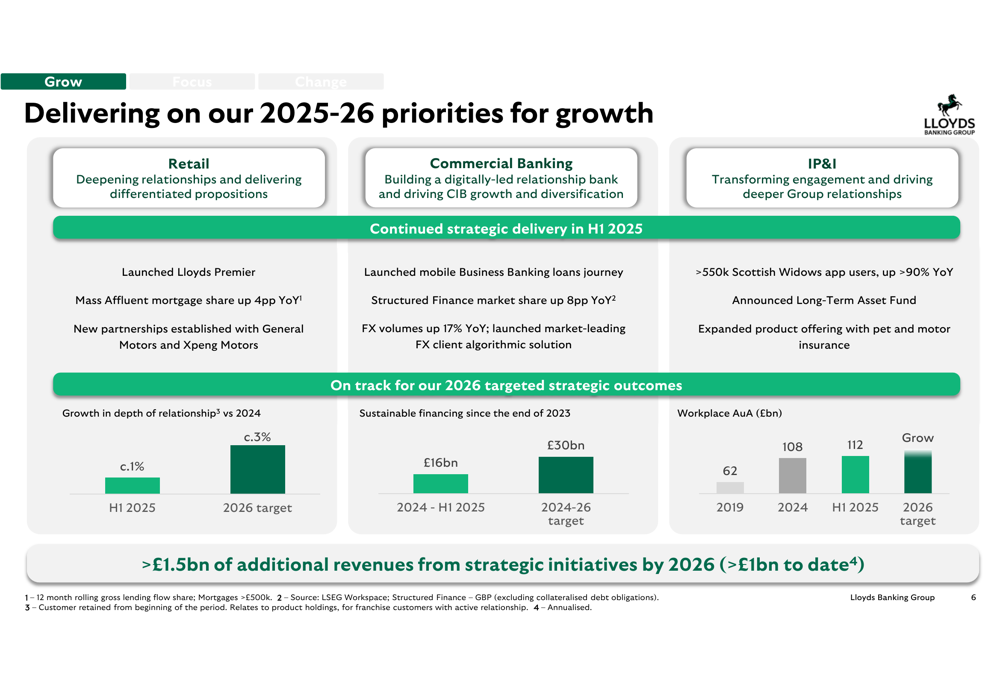

Lloyds is making significant progress on its strategic priorities for 2025-2026, focusing on deepening customer relationships and driving growth in targeted areas. The bank has launched new propositions such as Lloyds Premier and established new partnerships with General Motors (NYSE:GM) and Xpeng (NYSE:XPEV) Motors.

The following slide outlines the bank’s strategic priorities and progress across different business segments:

Digital transformation remains a key focus, with over 20.9 million mobile app users (up 3% year-to-date) and more than 95% of retail sales now conducted through digital channels. The bank is also leveraging artificial intelligence, with approximately 30 major GenAI use cases delivering benefits to customers and colleagues.

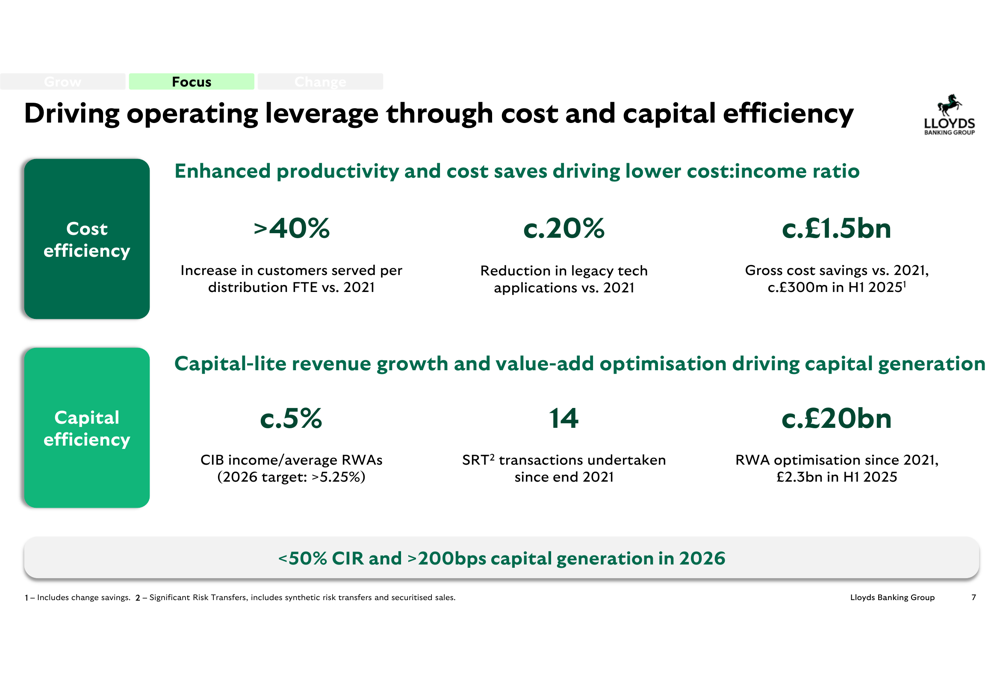

Lloyds is driving operating leverage through enhanced productivity and cost savings, as illustrated in this slide:

The bank reported a 40% increase in customers served per distribution full-time equivalent compared to 2021, along with approximately £1.5 billion in gross cost savings versus 2021, including about £300 million in H1 2025.

Forward-Looking Statements

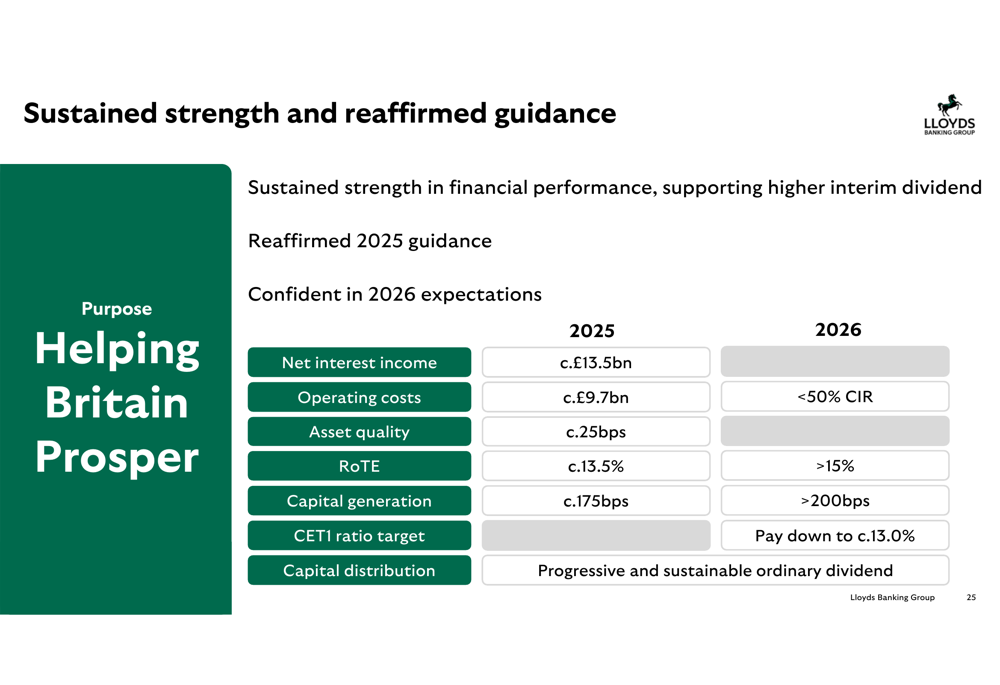

Lloyds Banking Group has reaffirmed its guidance for 2025 and expressed confidence in its outlook for 2026. For 2025, the bank expects net interest income of approximately £13.5 billion, operating costs of around £9.7 billion, and a return on tangible equity of approximately 13.5%.

The bank’s structural hedge is expected to provide a significant tailwind, with 2025 hedge income projected to be approximately £1.2 billion higher than 2024, and 2026 hedge income expected to be around £1.5 billion higher than 2025.

Looking further ahead to 2026, Lloyds aims to achieve a cost-to-income ratio below 50%, a return on tangible equity above 15%, and capital generation exceeding 200 basis points. The bank also targets a CET1 ratio of approximately 13.0%.

As shown in the following guidance summary:

The bank also highlighted its commitment to continued growth in capital distributions, with the interim dividend increased by 15% year-over-year to 1.22 pence per share. Since the end of 2021, Lloyds has announced £7.7 billion in share buybacks, reducing its share count by approximately 16%.

Lloyds Banking Group’s H1 2025 results demonstrate sustained financial strength and strategic progress, positioning the bank well to deliver on its medium-term targets despite the evolving economic environment. With its focus on digital transformation, targeted growth areas, and disciplined cost management, the bank appears well-positioned to continue delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.