TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Lloyds Banking Group (LSE:LLOY) presented its Q3 2025 Interim Management Statement on October 23, highlighting robust underlying performance despite a significant remediation charge for motor finance commissions. The bank continues to make strategic progress while maintaining strong capital generation and asset quality in a challenging economic environment.

Trading at 47.44p per share, Lloyds stock has shown impressive performance year-to-date with a 46.5% return according to recent market data, despite ongoing regulatory challenges in the motor finance sector.

Quarterly Performance Highlights

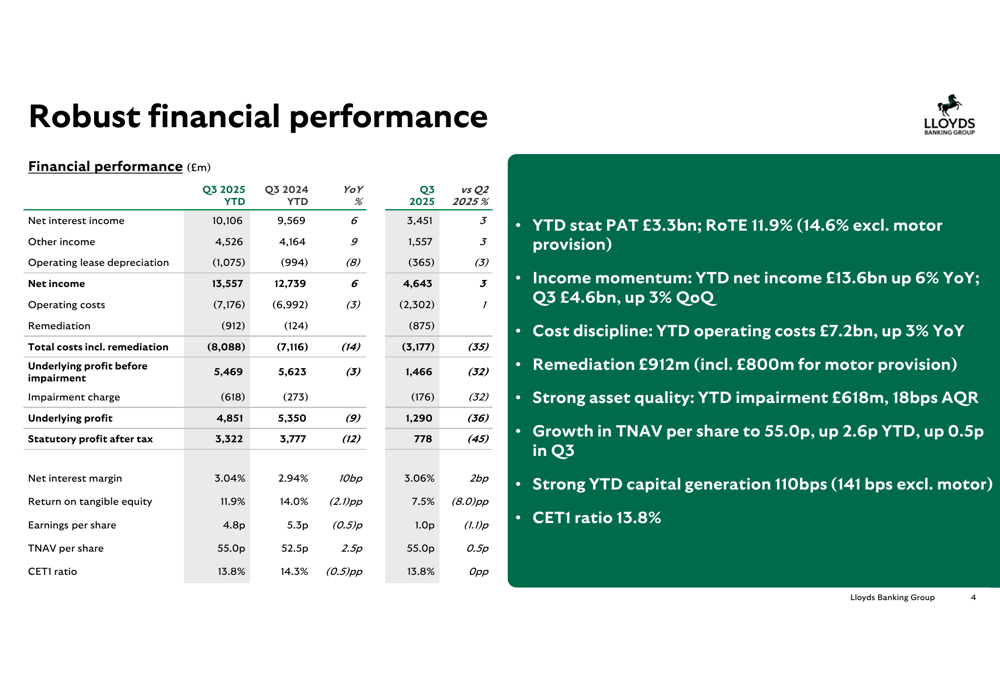

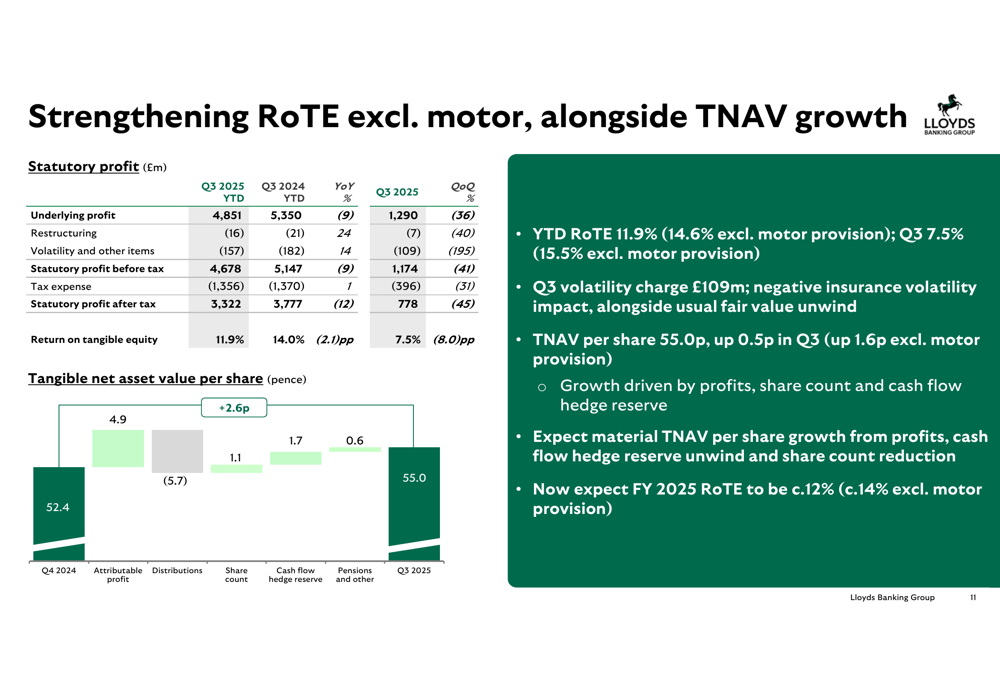

Lloyds reported Q3 2025 statutory profit after tax of £778 million, bringing the year-to-date total to £3.32 billion. The quarter’s results were significantly impacted by an £800 million provision for motor finance commissions, without which performance would have been considerably stronger.

Net income showed positive momentum, reaching £4.64 billion in Q3 (up 3% quarter-on-quarter), driven by growth in both net interest income and other income. The bank’s net interest margin improved to 3.06% in Q3 from 3.04% year-to-date.

As shown in the following financial performance summary:

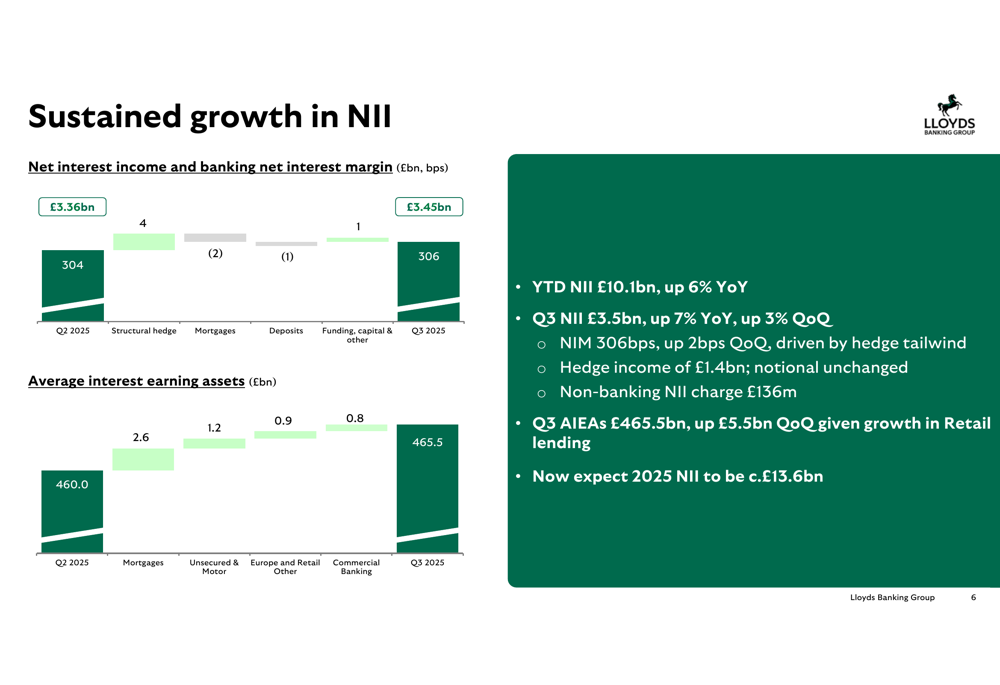

Net interest income continued its upward trajectory, reaching £3.45 billion in Q3 (up 3% quarter-on-quarter and 7% year-on-year). This growth was supported by increased average interest-earning assets, which rose to £465.5 billion in Q3 from £460.0 billion in Q2.

The sustained growth in net interest income is illustrated in this chart:

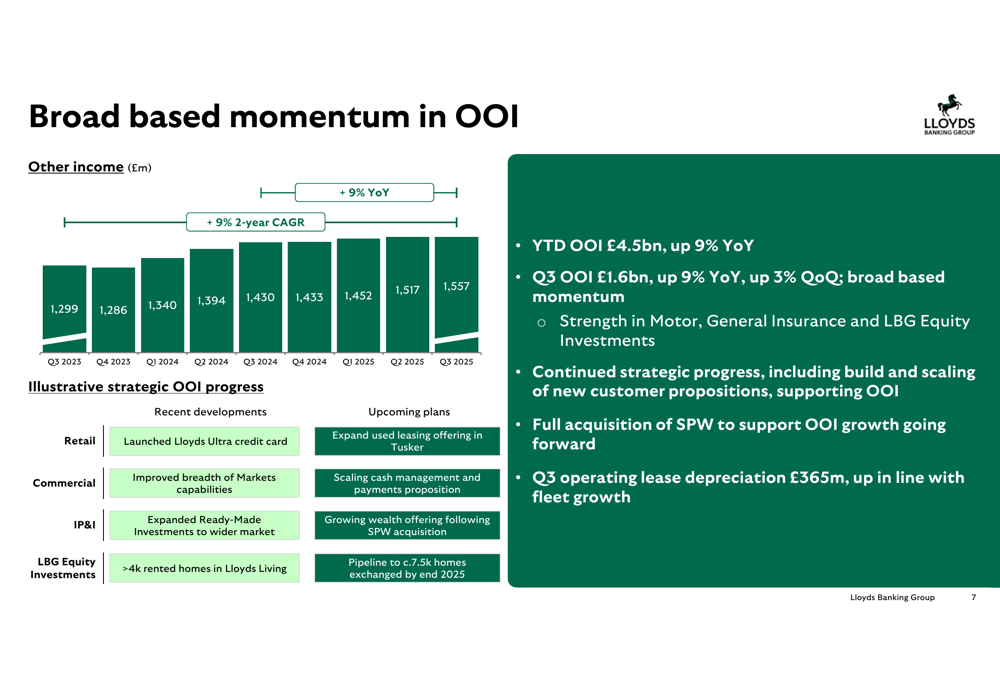

Other income also demonstrated broad-based momentum, growing to £1.56 billion in Q3 (up 3% quarter-on-quarter and 9% year-on-year). This growth was driven by strength in motor, general insurance, and LBG equity investments, as well as strategic initiatives including the launch of the Lloyds Ultra credit card and expanded ready-made investments.

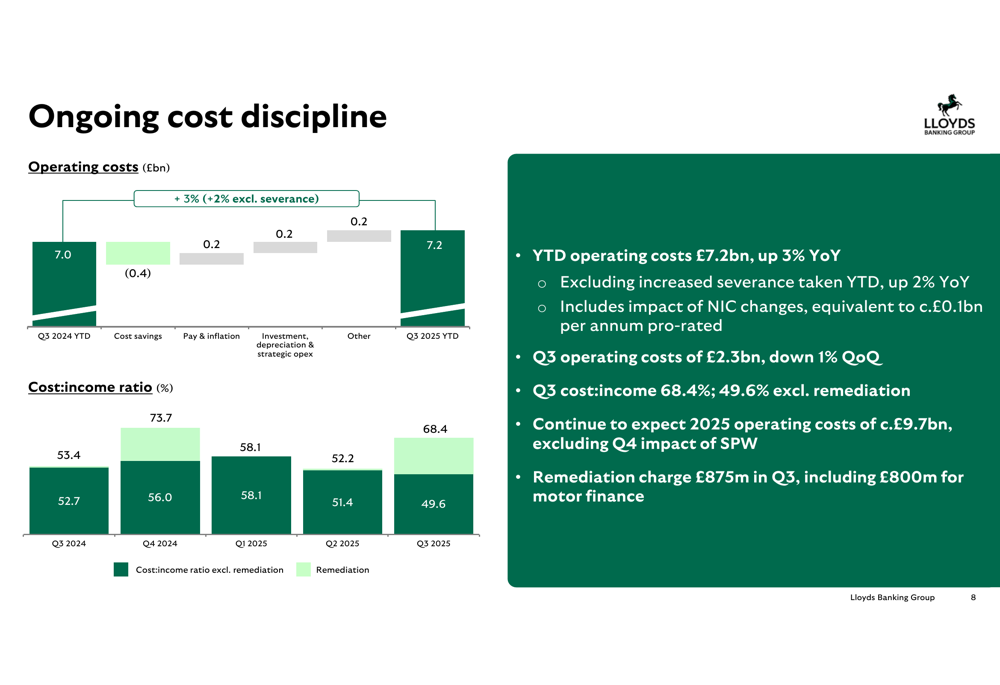

The bank maintained its focus on cost discipline, with operating costs of £2.3 billion in Q3 (down 1% quarter-on-quarter). The cost-to-income ratio stood at 68.4%, or 49.6% excluding remediation charges.

Strategic Initiatives

Lloyds highlighted several strategic developments in Q3, most notably the full acquisition of Schroders Personal Wealth with approximately £17 billion in assets under administration, over 300 advisors, and 60,000 clients. This acquisition aligns with the bank’s strategy to strengthen its wealth management offerings for mass affluent and workplace clients.

The bank also announced a partnership with Aberdeen that delivered an industry-first tokenized assets use case in July 2025, positioning Lloyds at the forefront of digital asset innovation in the banking sector.

These strategic initiatives are outlined in the following slide:

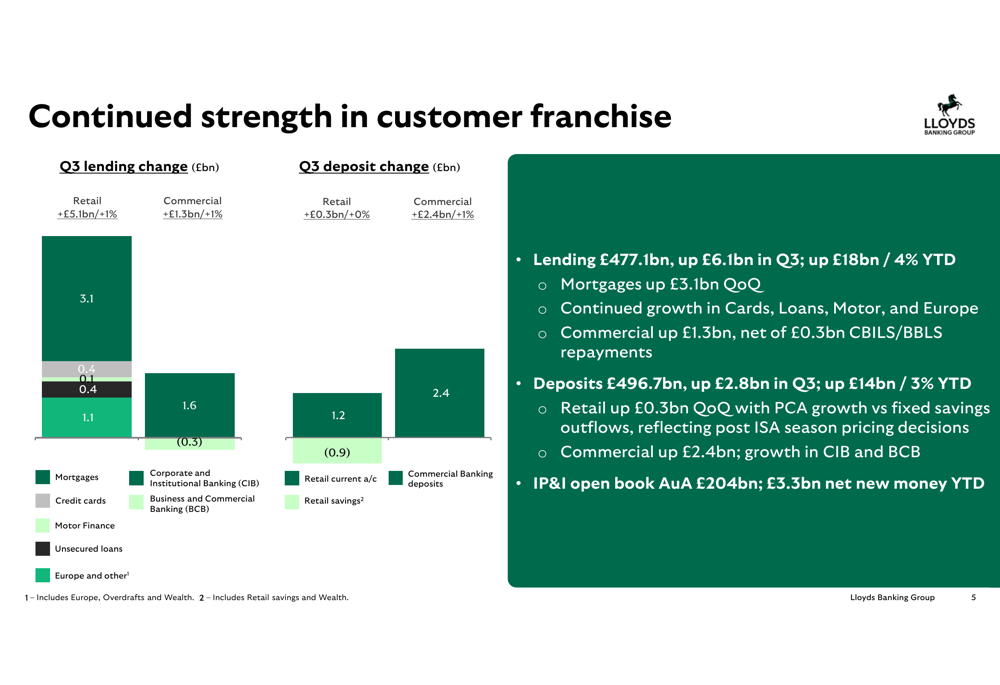

Lloyds continued to demonstrate strength in its customer franchise, with Q3 lending increasing by £6.1 billion (Retail +£5.1bn, Commercial +£1.3bn) and deposits growing by £2.8 billion (Retail +£0.3bn, Commercial +£2.4bn).

Motor Finance Provision Impact

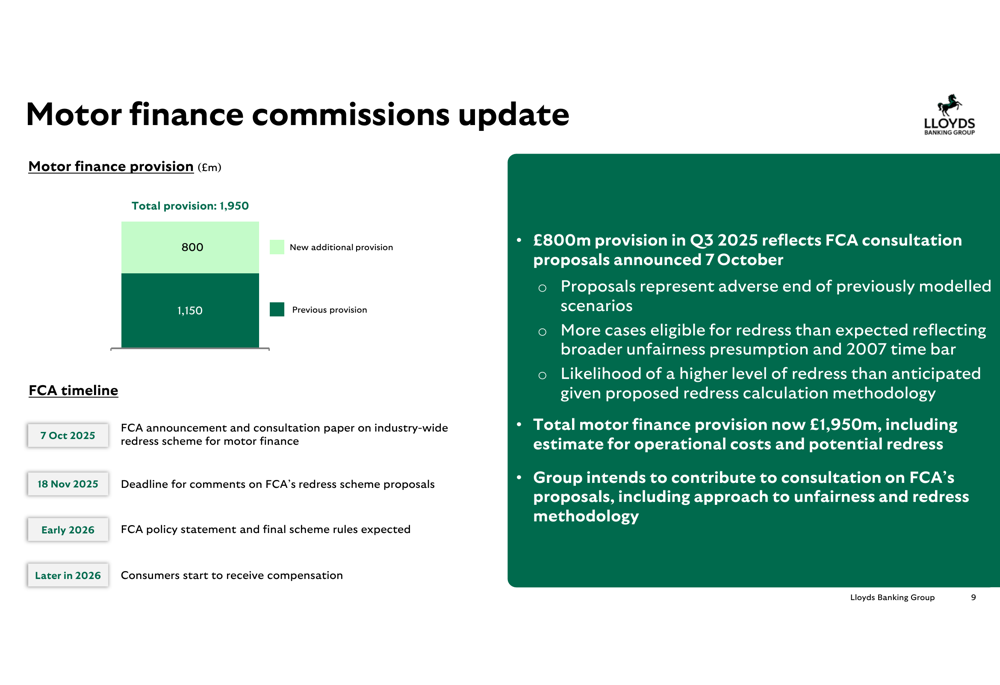

The most significant impact on Q3 results was an £800 million provision for motor finance commissions, bringing the total provision to £1.95 billion. This provision follows the Financial Conduct Authority’s consultation proposals announced on October 7, 2025, which represent the "adverse end of previously modeled scenarios" according to Lloyds.

The provision reflects a broader unfairness presumption, a 2007 time bar, and a higher level of redress than anticipated due to the proposed redress calculation methodology. Lloyds intends to contribute to the consultation on the FCA’s proposals.

The following slide details the motor finance commission update:

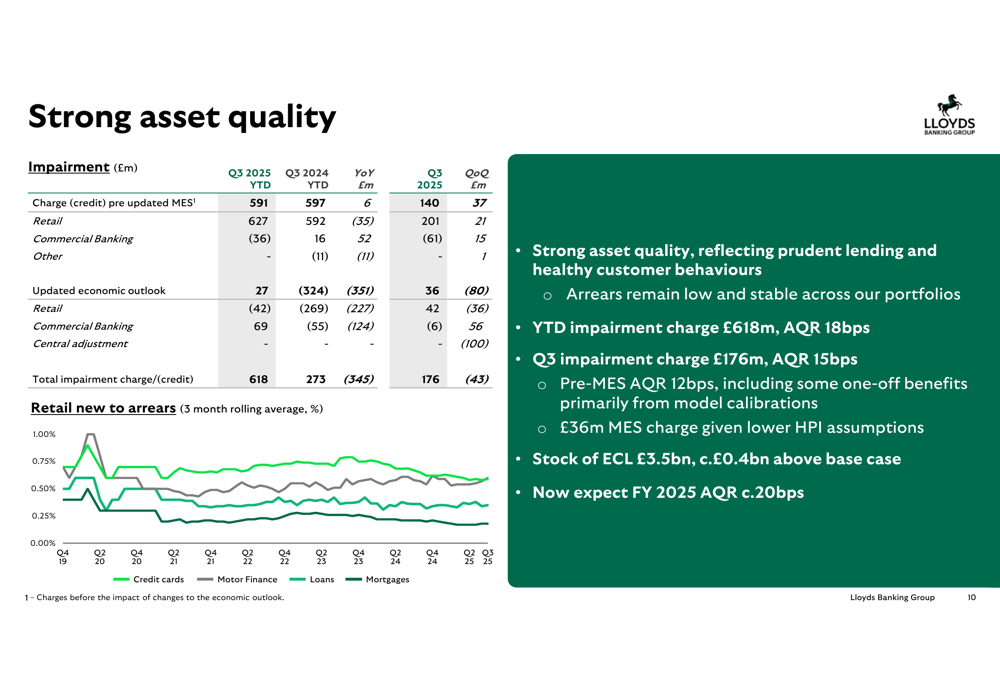

Despite this significant provision, Lloyds maintained strong asset quality across its portfolios, with a Q3 impairment charge of £176 million (asset quality ratio of 15bps). Arrears remained low and stable across the bank’s portfolios.

The motor finance provision significantly impacted the bank’s return on tangible equity (RoTE), which stood at 7.5% for Q3. However, excluding this provision, Q3 RoTE would have been 15.5%, demonstrating the underlying strength of the business.

Forward-Looking Statements

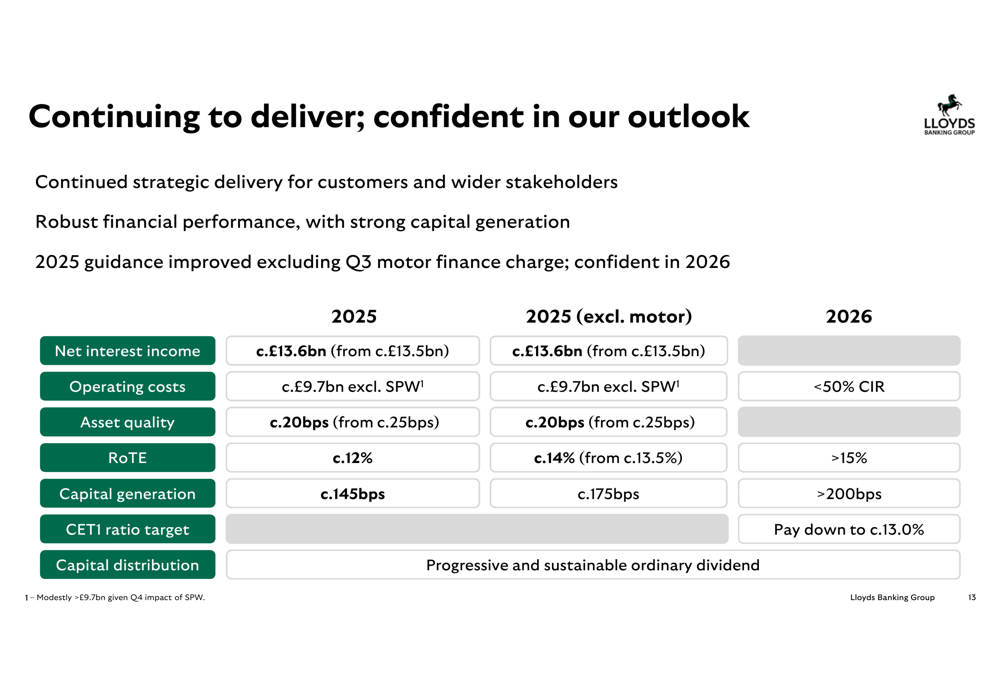

Lloyds improved its 2025 guidance for several key metrics, excluding the impact of the motor finance provision. The bank now expects:

- Net interest income of approximately £13.6 billion (up from previous guidance of £13.5 billion)

- Operating costs of approximately £9.7 billion (excluding Schroders Personal Wealth)

- Asset quality ratio of approximately 20bps (improved from previous guidance of 25bps)

- Return on tangible equity of approximately 12%, or 14% excluding the motor provision

- Capital generation of approximately 145bps, or 175bps excluding the motor provision

For 2026, Lloyds maintained its targets of a cost-to-income ratio below 50%, return on tangible equity above 15%, and capital generation exceeding 200bps.

The bank’s outlook is summarized in the following slide:

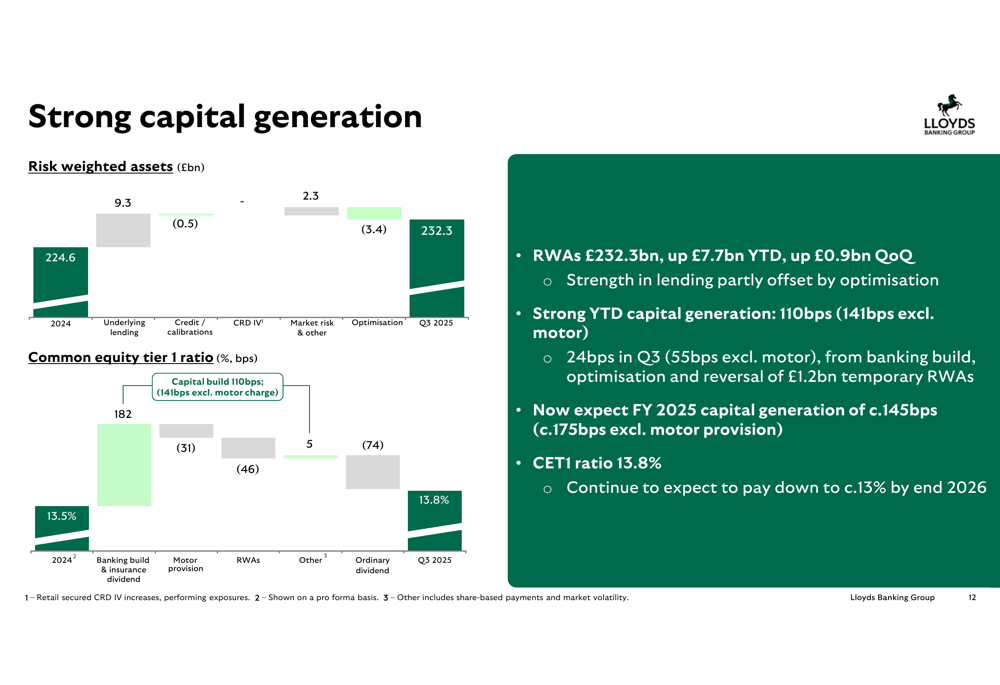

Lloyds continues to maintain a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 13.8%. The bank expects to pay down to approximately 13% by the end of 2026 while maintaining a progressive and sustainable ordinary dividend.

CEO Charlie Nunn had previously expressed confidence in the company’s strategic direction during the Q2 earnings call, stating that "Our strategy is providing our customers with leading propositions and supporting the real economy." The Q3 results, despite the remediation charge, appear to support this confidence in the underlying business performance.

With continued strategic execution and robust financial performance excluding one-off provisions, Lloyds Banking Group remains well-positioned to navigate the current economic environment and deliver on its medium-term targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.