5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Parsons Corporation (NYSE:PSN) presented its first quarter 2025 earnings results on April 30, 2025, showcasing record performance across key metrics despite facing challenges in its Federal Solutions segment. The results represent a significant recovery following the company’s disappointing fourth quarter 2024 performance, which had previously triggered a 12.71% stock drop.

Parsons shares closed at $68.66 prior to the earnings release, with premarket trading showing a modest 0.66% increase to $69.11. The stock remains well below its 52-week high of $114.68, suggesting potential upside if the company can maintain its positive momentum.

Quarterly Performance Highlights

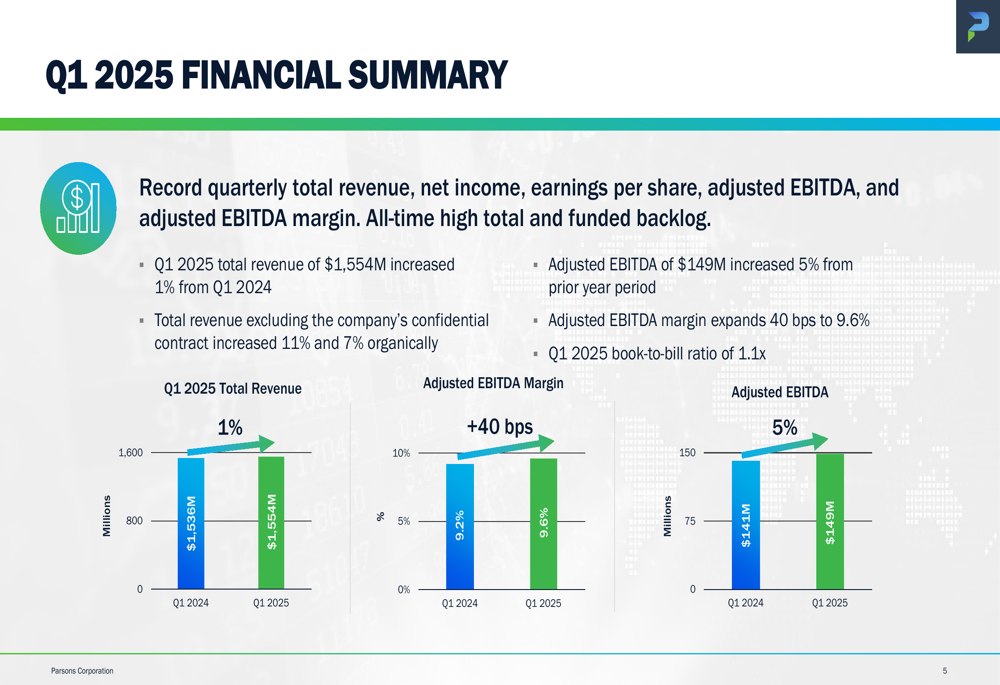

Parsons reported record first quarter results across multiple financial metrics. Total (EPA:TTEF) revenue reached $1.6 billion, while net income surged 67% to $66 million compared to the same period last year. Adjusted EBITDA grew 5% to $149 million, with margins expanding 40 basis points to 9.6%.

The company’s book-to-bill ratio stood at a healthy 1.1x, indicating strong future revenue potential, while contract win rates remained robust at 68%. Parsons also highlighted that excluding its confidential contract, the company achieved low double-digit total revenue growth and organic growth of 7%.

As shown in the following financial performance summary:

Parsons’ backlog increased to a record $9.1 billion, with 69% of that amount funded – also a company record. Additionally, the company reported approximately $12 billion worth of contract wins not yet booked into backlog and a substantial $55 billion pipeline that includes over 100 opportunities worth more than $100 million each.

Segment Analysis

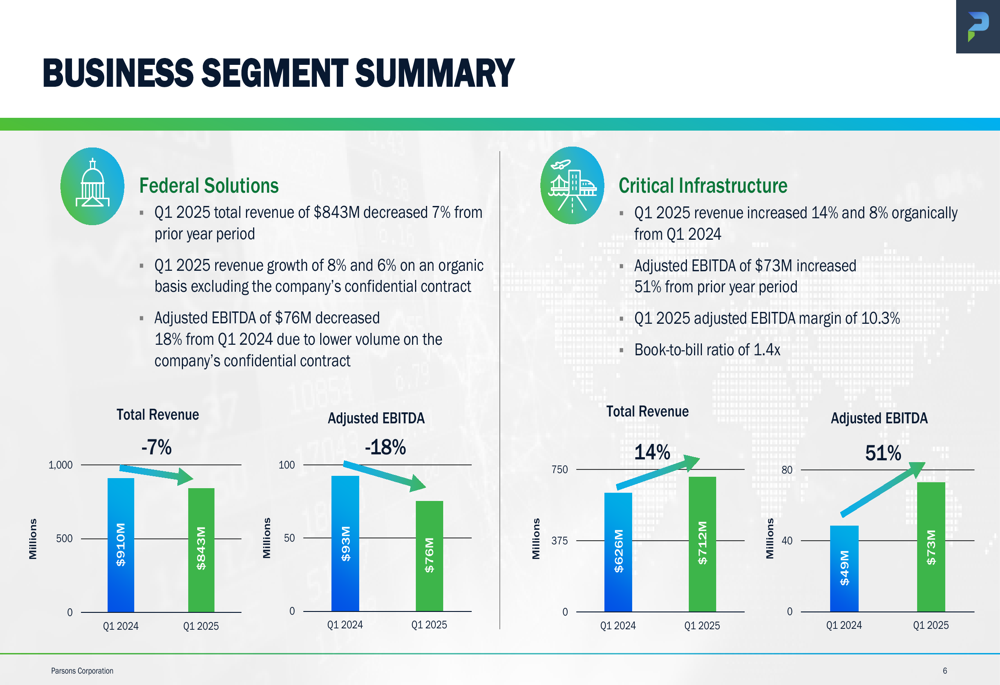

The quarter revealed a notable divergence in performance between Parsons’ two business segments. The Federal Solutions segment experienced a 7% year-over-year revenue decline to $843 million, with adjusted EBITDA decreasing 18% to $76 million. This contrasts sharply with the Critical Infrastructure segment, which saw revenue increase 14% to $712 million and adjusted EBITDA surge 51% to $73 million.

The following chart illustrates this segment performance divergence:

The Critical Infrastructure segment has now achieved a book-to-bill ratio above 1.0x for 18 consecutive quarters, demonstrating consistent demand for Parsons’ services in this area. This strong performance has helped offset the temporary weakness in the Federal Solutions segment.

Strategic Initiatives

Parsons secured several significant contract wins during the quarter, including five awards exceeding $100 million each. Notable wins included a $243 million GSA contract option year, $232 million in funding from a confidential customer, and a follow-on program and construction management contract in Dubai valued at over $200 million.

The company’s diverse contract wins across multiple sectors are highlighted below:

Parsons continues to expand its contract portfolio with additional significant awards:

The company is strategically positioned across six high-growth end markets, with market compound annual growth rates (CAGRs) ranging from 4-10%. This diversification helps insulate Parsons from fluctuations in any single market while allowing it to capitalize on multiple growth opportunities.

As illustrated in the following market overview:

On the acquisition front, Parsons announced and closed its purchase of TRS Group, an industry leader in PFAS, thermal, and holistic environmental remediation, for approximately $37 million. This strategic acquisition strengthens the company’s environmental remediation capabilities, particularly in the growing PFAS remediation market.

The company also maintained its ethical business practices, being named one of the World’s Most Ethical Companies for the 16th consecutive year by Ethisphere. Additionally, Parsons’ Board approved a $250 million share repurchase authorization, reflecting confidence in the company’s financial position and future prospects.

Forward-Looking Statements

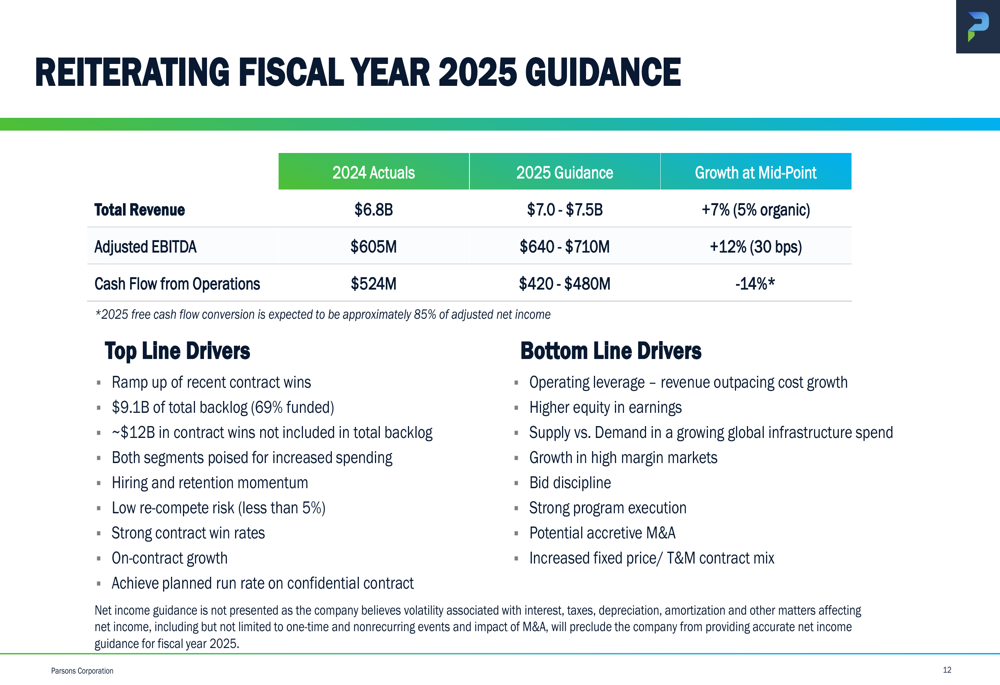

Parsons reiterated its fiscal year 2025 guidance, projecting total revenue between $7.0-$7.5 billion, representing 7% growth (5% organic) at the midpoint compared to 2024 actuals of $6.8 billion. The company expects adjusted EBITDA to reach $640-$710 million, a 12% increase at the midpoint, with 30 basis points of margin expansion.

The detailed guidance is presented in the following chart:

Management expects approximately 56% of total revenue to be generated from the Federal Solutions segment, with an adjusted EBITDA margin of approximately 9.3% at the midpoint of revenue guidance. The company anticipates net interest expense of around $40 million and a GAAP effective tax rate of approximately 22%.

Parsons’ strong balance sheet, with a net debt leverage ratio of 1.6x, positions the company to continue making strategic acquisitions while maintaining financial flexibility. The company’s trailing twelve-month free cash flow conversion rate stands at an impressive 125%, though cash flow used in operations was $12 million in Q1 2025.

These results and forward-looking projections suggest Parsons has rebounded from its disappointing Q4 2024 performance, with the company executing effectively on its strategic initiatives while navigating segment-specific challenges. Investors will likely focus on the continued recovery of the Federal Solutions segment and the sustainability of the strong growth in Critical Infrastructure as key indicators for future performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.