Street Calls of the Week

Introduction & Market Context

Procter & Gamble (NYSE:PG) released its first quarter fiscal 2026 earnings presentation on October 24, 2025, showing modest growth in what the company described as a "difficult geopolitical, competitive and consumer environment." The consumer goods giant reported core earnings per share of $1.99, up 3% versus the prior year, while organic sales grew 2%, driven by pricing and mix contributions.

Following the earnings announcement, P&G’s stock rose 2.09% in pre-market trading to $155.39, reflecting investor confidence in the company’s ability to navigate challenging market conditions.

Quarterly Performance Highlights

P&G’s Q1 FY 2026 results demonstrated the company’s resilience amid various headwinds. Organic sales growth of 2% was achieved through a combination of pricing (1%) and mix (1%), while organic volume remained flat. The company maintained a consistent growth pattern over recent quarters, as illustrated in its organic sales trend.

Core earnings per share reached $1.99, representing a 3% increase year-over-year, both on a reported and currency-neutral basis. This growth came despite core gross margin declining by 50 basis points, as the company’s productivity savings helped offset various challenges.

From a market share perspective, P&G faced some competitive pressures with global aggregate value share down 30 basis points. However, the company noted that 24 of its top 50 category/country combinations held or grew share during the quarter, and 8 of 10 product categories grew or held organic sales.

The company’s overall performance metrics for the quarter showed solid execution of its integrated strategy:

Segment Performance Analysis

P&G’s business segments delivered notably varied results in Q1 FY 2026, with Beauty and Grooming outperforming while other segments faced challenges:

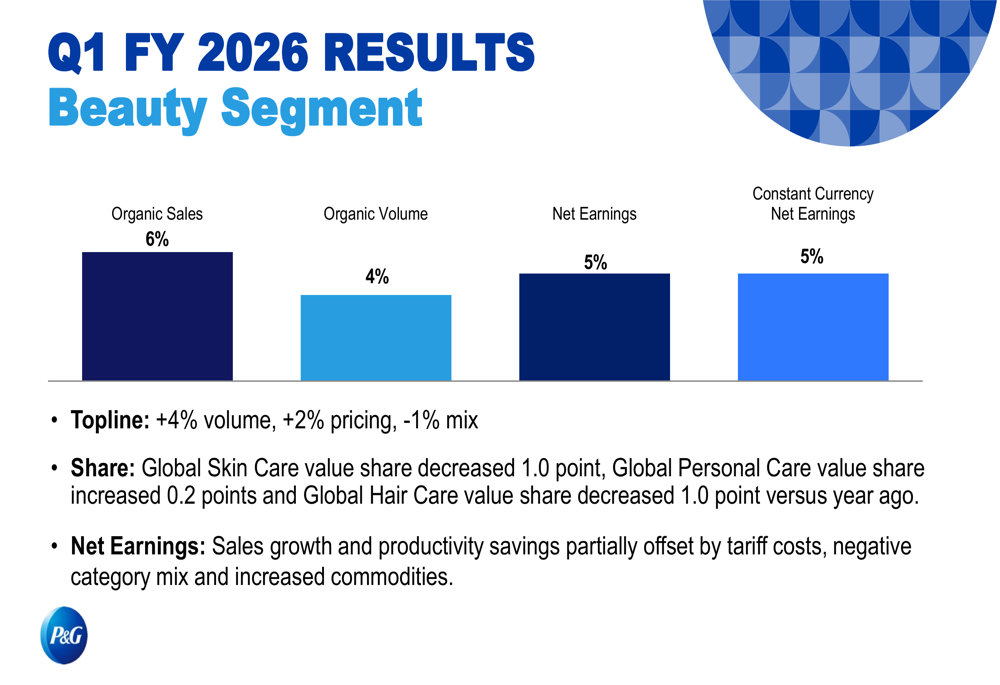

The Beauty segment was the standout performer, delivering 6% organic sales growth with a 4% increase in volume. Net earnings grew 5%, supported by sales growth and productivity savings, though partially offset by tariff costs and commodity pressures.

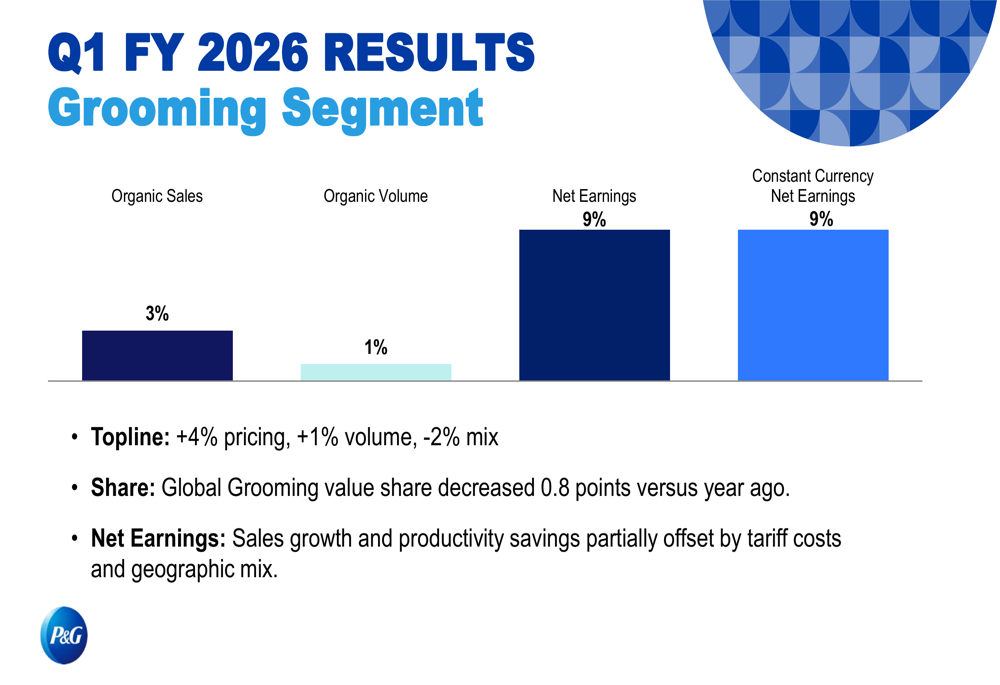

The Grooming segment also performed well, with 3% organic sales growth and impressive 9% net earnings growth. This segment benefited from 4% pricing and 1% volume growth, though it experienced a 0.8 point decrease in global value share.

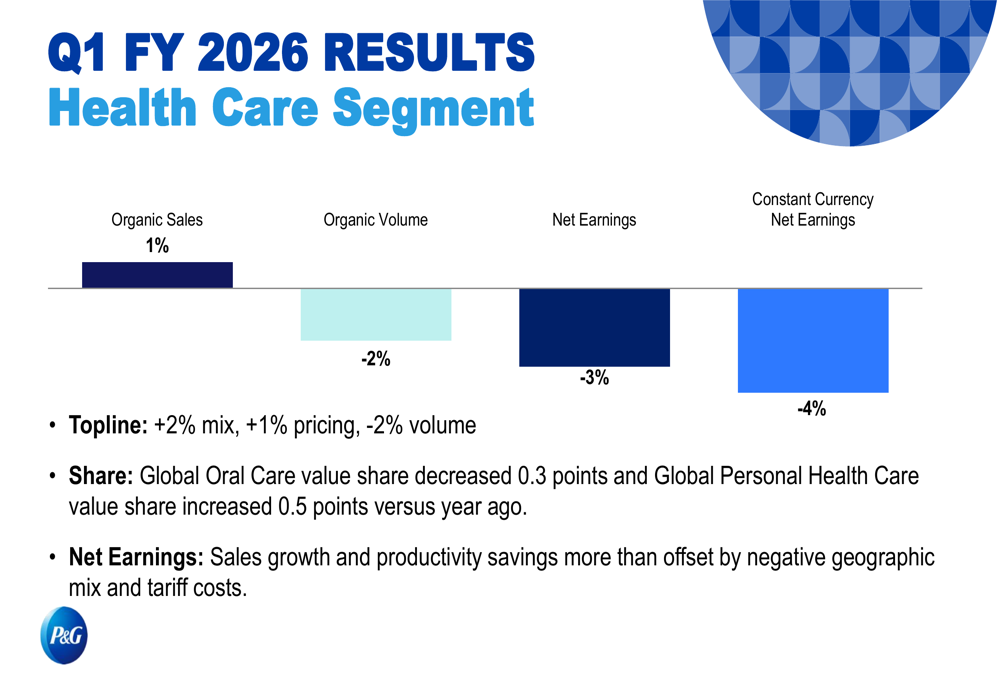

In contrast, the Health Care segment showed more modest growth with 1% organic sales growth but a 3% decline in net earnings. The segment faced a 2% volume decline, though this was offset by positive mix and pricing contributions.

The Fabric & Home Care and Baby, Feminine and Family Care segments both reported flat organic sales (0% growth). Fabric & Home Care experienced a 3% decline in net earnings, while Baby, Feminine and Family Care managed to grow net earnings by 4% despite flat sales, primarily through productivity savings and lower commodity costs.

Strategic Initiatives & Outlook

P&G’s presentation highlighted its integrated growth strategy centered around five key elements: portfolio optimization, organizational effectiveness, product superiority, constructive disruption, and productivity improvements. The company emphasized focus areas including supply chain enhancement, environmental sustainability, digital acumen, and employee value proposition.

For fiscal year 2026, P&G maintained its guidance across all key metrics. The company expects organic sales growth between 0% and 4%, with net sales growth slightly higher at 1% to 5%, benefiting from a 1% positive impact from foreign exchange and acquisitions/divestitures.

Core EPS growth is projected at 0% to 4%, with currency-neutral core EPS growth of -2% to +2%. The company outlined several headwinds impacting its outlook, including approximately $0.1 billion after-tax headwind from commodities and a more substantial $0.4 billion after-tax headwind from tariffs. These challenges are partially offset by a $0.3 billion after-tax tailwind from foreign exchange.

P&G also provided guidance on shareholder returns, projecting approximately $10 billion in dividends and $5 billion in direct share repurchases for fiscal 2026.

Forward-Looking Statements

While maintaining its full-year guidance, P&G identified several potential headwinds not included in its current outlook that could impact future performance. These include significant deceleration of market growth rates, substantial currency weakness, significant commodity cost increases, additional geopolitical disruptions, major supply chain disruptions, and significant tariff changes.

Notably, the earnings call transcript revealed that P&G has announced a significant restructuring plan targeting a reduction of up to 7,000 non-manufacturing roles, which wasn’t explicitly mentioned in the presentation slides. This initiative appears to align with the company’s productivity focus but represents a material development for investors to monitor.

Despite these challenges, P&G’s CFO Andre Schulten expressed confidence in the company’s strategy, stating, "We continue to believe the best path to sustainable balanced growth is to double down on the strategy." The company’s focus on understanding consumer behavior to drive sales and innovation remains central to its approach.

As P&G navigates a complex global environment, its ability to maintain growth while addressing competitive pressures and cost challenges will be crucial for meeting its fiscal 2026 targets and delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.