TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Q2 Holdings (NYSE:QTWO) presented its second quarter 2025 financial results on July 30, showcasing a significant turnaround in profitability alongside continued revenue growth. The digital banking solutions provider reported a 13% year-over-year revenue increase and a shift from net loss to net income, reflecting the company’s successful execution of its growth strategy.

The results come amid increasing demand for digital banking, risk management, and fraud prevention solutions among financial institutions. After reporting strong Q1 2025 results earlier this year with 15% revenue growth, Q2 Holdings has maintained positive momentum through the second quarter, though with a slightly moderated growth rate.

Quarterly Performance Highlights

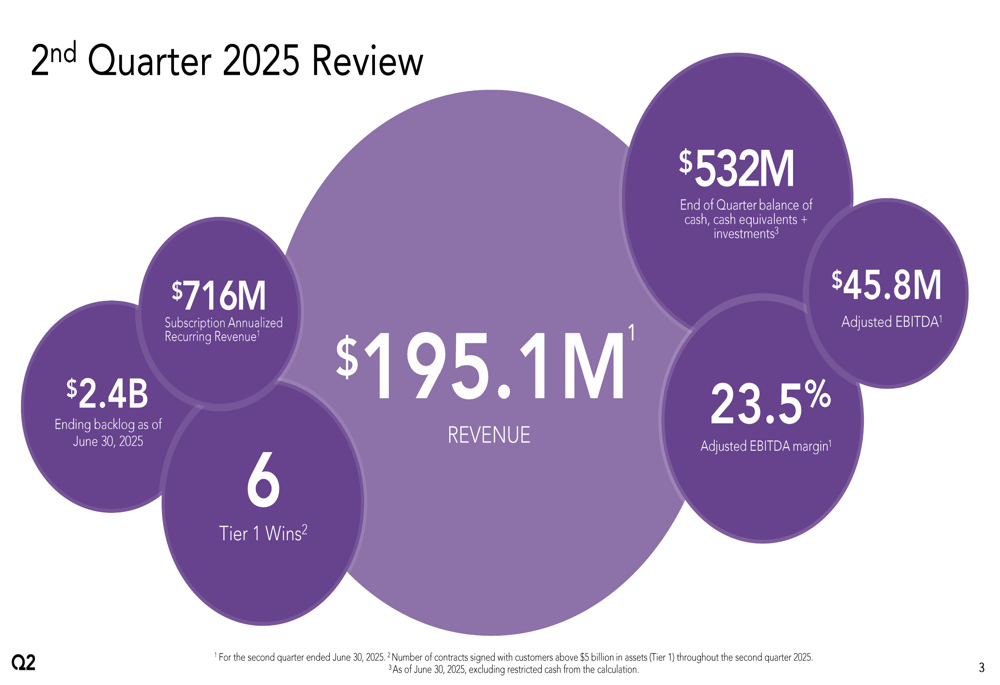

Q2 Holdings reported total revenue of $195.1 million for the second quarter, representing a 13% increase compared to the same period in 2024. More significantly, the company achieved net income of $11.8 million, a substantial improvement from the $13.1 million loss recorded in Q2 2024.

As shown in the following quarterly results summary:

Gross profit increased 20% year-over-year to $104.6 million, while non-GAAP gross profit rose 17% to $112.3 million. The company’s adjusted EBITDA saw remarkable growth of 53%, reaching $45.8 million with a margin of 23.5%, demonstrating significant operational efficiency improvements compared to the previous year.

The company’s key financial metrics for the quarter are highlighted in this comprehensive overview:

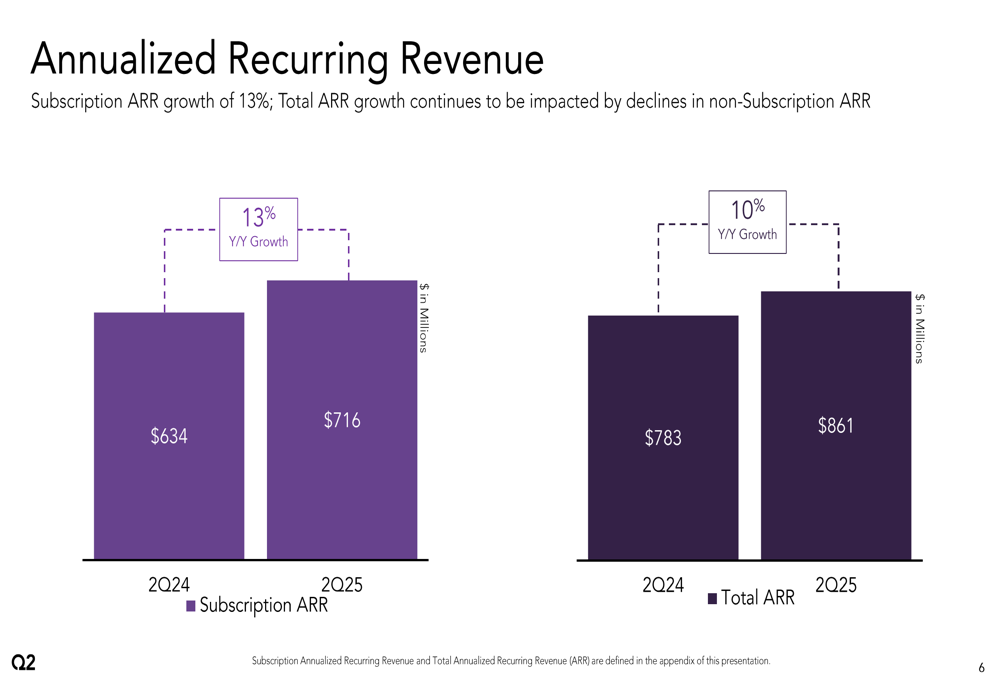

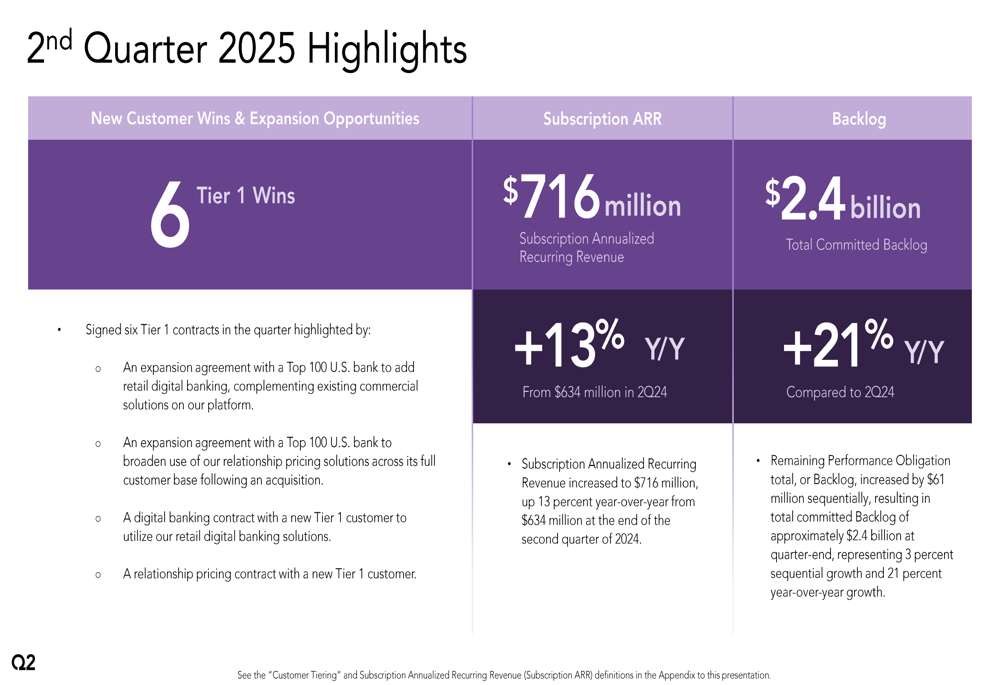

Subscription Annualized Recurring Revenue (ARR) grew to $716 million, representing a 13% year-over-year increase from $634 million in Q2 2024. Total (EPA:TTEF) ARR reached $861 million, up 10% from the previous year. The company ended the quarter with $532 million in cash, cash equivalents, and investments, providing substantial financial flexibility.

The following chart illustrates the company’s ARR growth trajectory:

Strategic Initiatives and Customer Wins

Q2 Holdings secured six tier 1 wins during the quarter, including an expansion agreement with a Top 100 U.S. bank to add retail digital banking capabilities and another expansion to broaden the use of relationship pricing solutions. The company also signed a new digital banking contract with a tier 1 customer, further strengthening its position in the enterprise market.

The company’s quarterly highlights demonstrate continued momentum in customer acquisition and expansion:

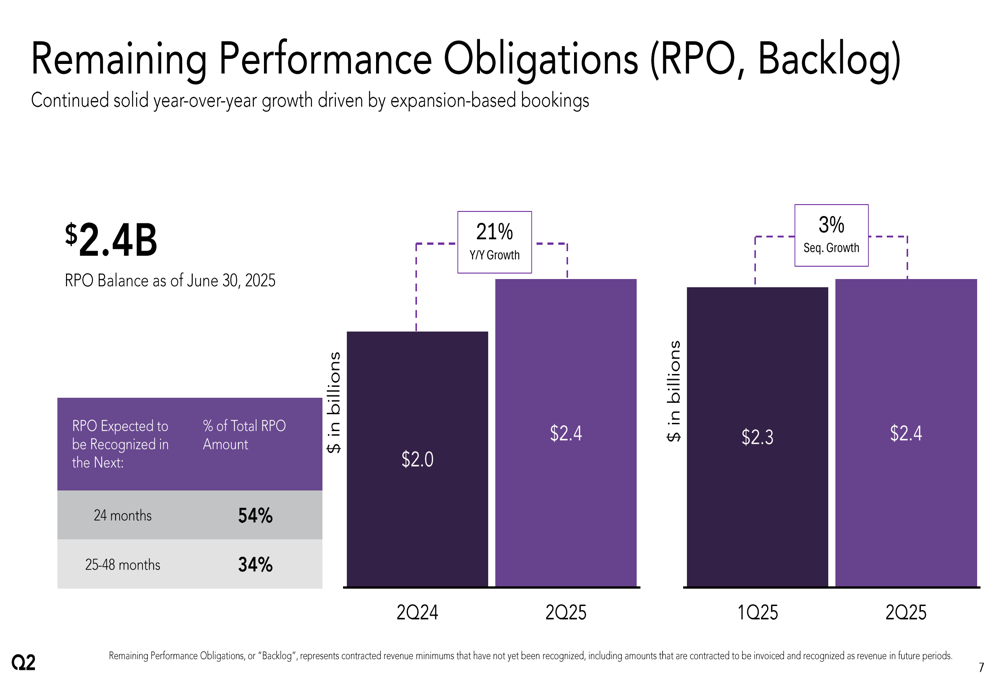

The company’s total committed backlog reached $2.4 billion, growing 21% year-over-year and 3% sequentially from the previous quarter. This substantial backlog provides strong visibility into future revenue streams and reflects the company’s success in securing long-term contracts.

The following chart shows the growth in Remaining Performance Obligations (RPO), also known as backlog:

Q2 Holdings maintains a diverse customer base across different financial institution segments, with tier 1 and tier 2 institutions representing the largest portions of revenue at 36% and 34% respectively. By customer type, banks account for 64% of revenue, credit unions 25%, and other customers 11%. Importantly, the company has limited customer concentration risk, with its largest customer representing only 2% of revenue.

Financial Outlook and Guidance

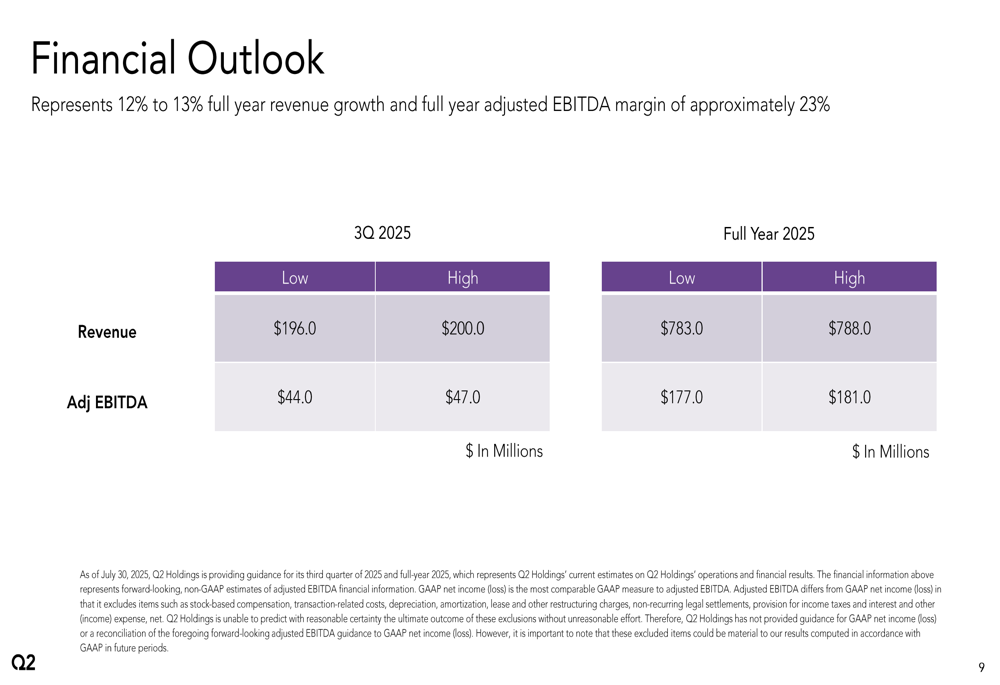

Based on its strong performance, Q2 Holdings has provided guidance for the third quarter and full year 2025. For Q3, the company expects revenue between $196.0 million and $200.0 million, with adjusted EBITDA between $44.0 million and $47.0 million.

The full-year 2025 outlook has been slightly raised from previous guidance, with revenue now projected between $783.0 million and $788.0 million, compared to the $776-783 million range provided after Q1 results. Adjusted EBITDA for the full year is expected to be between $177.0 million and $181.0 million.

The company’s detailed financial outlook is presented in the following table:

Forward-Looking Statements

Looking beyond 2025, Q2 Holdings has outlined ambitious financial targets for the 2024-2026 period. The company aims to achieve average annual subscription revenue growth of approximately 15%, driven by strong market demand for its solutions. Management also targets average annual adjusted EBITDA margin expansion of around 360 basis points, leveraging revenue mix improvements and cost scaling.

By the full year 2026, Q2 Holdings expects to achieve free cash flow conversion exceeding 90%, which would provide significant flexibility to service debt and reinvest in the business.

Matt Flake, Chairman and CEO of Q2 Holdings, expressed confidence in the company’s trajectory, stating: "We delivered solid sales execution in the second quarter, including six tier 1 wins. Renewals and expansions continue to be an important part of our business, and we’re seeing strong demand for our risk and fraud solutions. We remain confident in our ability to deliver on our profitable growth strategy."

The company’s strong customer base of over 1,300 clients, including 460 digital banking platform customers and more than 26 million registered end users, positions it well to capitalize on the estimated $20 billion total addressable market. With average contract lengths exceeding five years and a track record of 57% average customer contracted revenue growth at 48 months, Q2 Holdings has established a foundation for sustainable long-term growth.

Despite these positive developments, Q2 Holdings’ stock declined slightly in aftermarket trading following the earnings release, down 1.01% to $89.49, suggesting investors may have already priced in the strong performance or had even higher expectations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.