5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

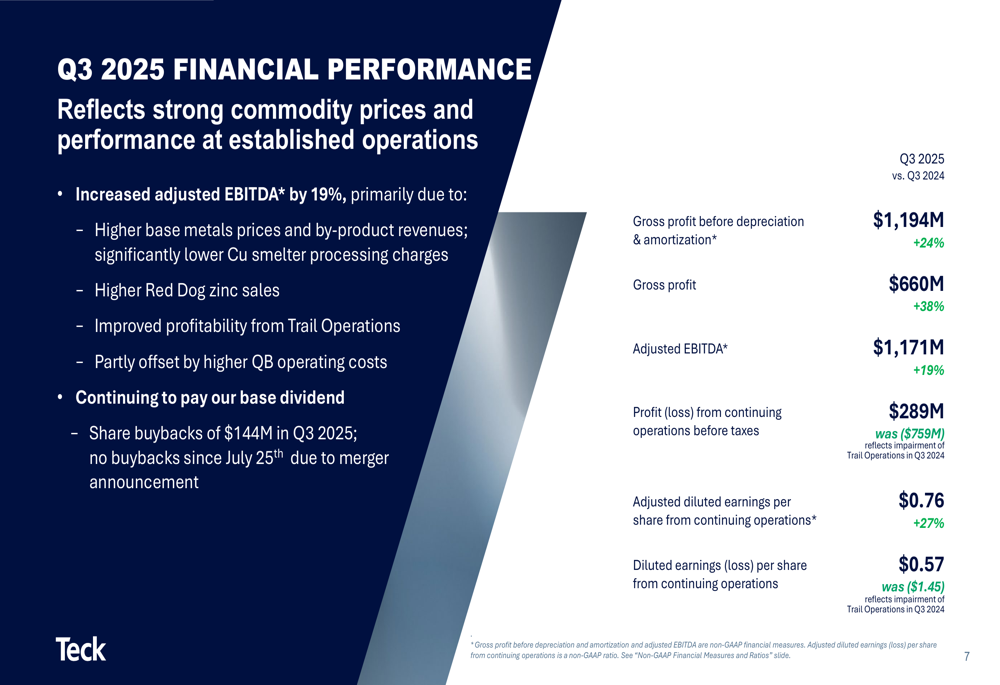

Teck Resources Ltd (NYSE:TECK) presented its third quarter 2025 results on October 22, highlighting a 19% year-over-year increase in adjusted EBITDA to $1.2 billion, driven by higher base metals prices and improved operational performance at established mines. The company’s shares initially rose 1.31% in pre-market trading following the earnings announcement but later declined by 2.01% to $42.84 during the regular session.

The Canadian mining company is advancing its proposed merger of equals with Anglo American, which aims to create a top five global copper producer. This strategic move comes as copper demand continues to grow, particularly from emerging Asian economies and China’s ongoing energy transition initiatives.

Quarterly Performance Highlights

Teck’s financial performance showed significant improvement across key metrics compared to the same period last year. The company reported gross profit before depreciation and amortization of $1.19 billion, up 24% year-over-year, while gross profit increased 38% to $660 million. Profit from continuing operations before taxes reached $289 million, compared to a loss of $759 million in Q3 2024 that reflected an impairment of Trail Operations.

As shown in the following financial performance summary, adjusted diluted earnings per share from continuing operations increased 27% to $0.76, significantly exceeding analyst expectations of $0.53:

The improved profitability was driven by several factors, with higher metal prices and increased sales volumes being the primary contributors. The following waterfall chart breaks down the specific drivers of the $185 million increase in adjusted EBITDA compared to Q3 2024:

Higher primary and by-product prices contributed $211 million, while increased volumes added $160 million. These gains were partially offset by higher operating costs (-$123 million) and increased royalties (-$88 million).

Segment Performance

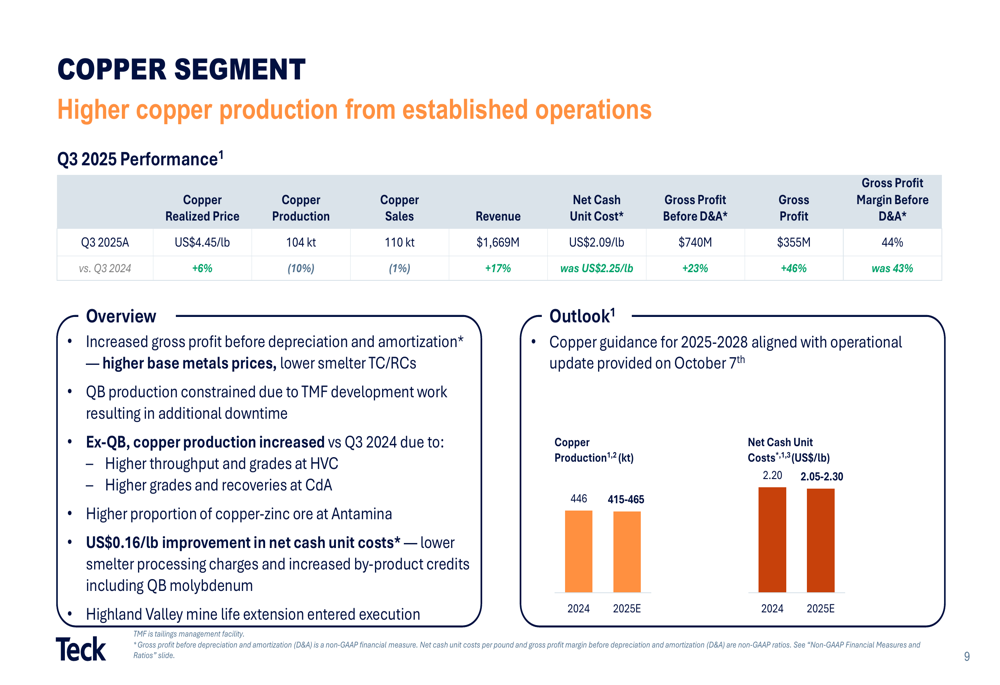

Teck’s copper segment benefited from higher realized prices, which increased 6% year-over-year to US$4.45 per pound. While copper production decreased 10% to 104,000 tonnes, net cash unit costs improved to US$2.09 per pound from US$2.25 in the prior year period. This resulted in a 23% increase in gross profit before depreciation and amortization to $740 million.

The copper segment’s detailed performance metrics are illustrated below:

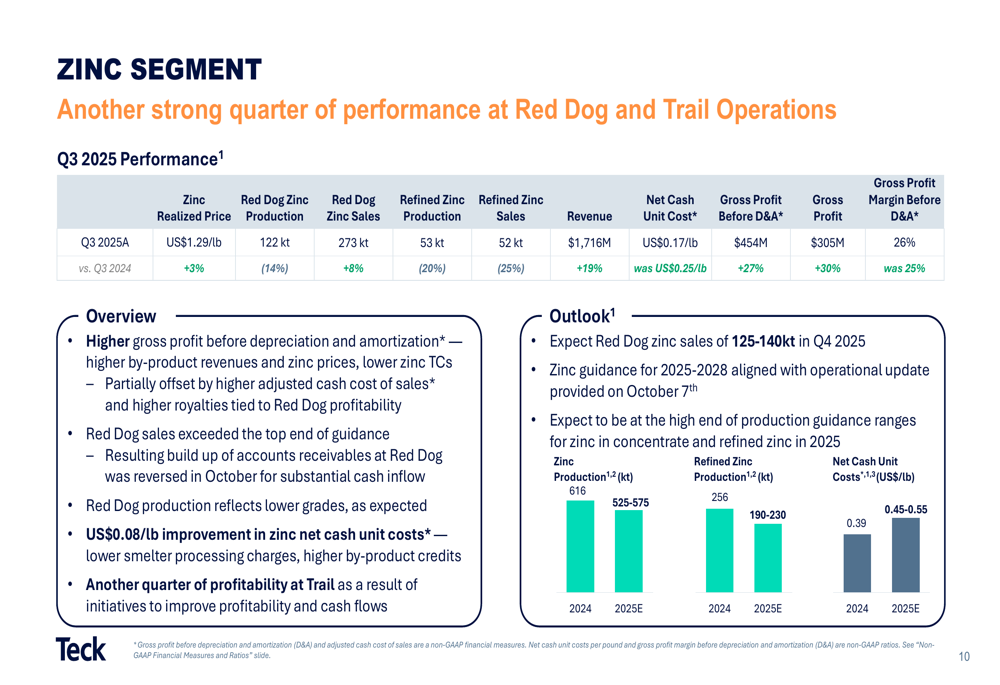

The zinc segment also delivered strong results, with Red Dog zinc sales increasing 8% year-over-year to 273,000 tonnes, despite a 14% decrease in production. Zinc realized prices rose 3% to US$1.29 per pound, while net cash unit costs improved to US$0.17 per pound from US$0.25 in Q3 2024. These factors contributed to a 27% increase in gross profit before depreciation and amortization to $454 million.

The zinc segment’s performance is summarized in the following chart:

Strategic Initiatives

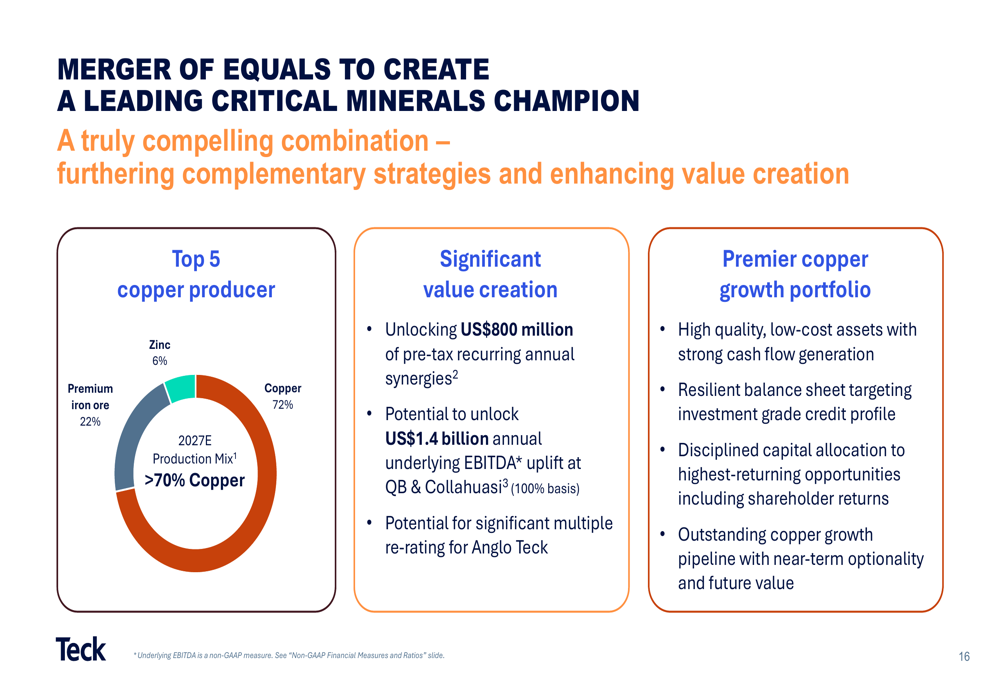

The most significant strategic development announced by Teck is the proposed merger with Anglo American, which was revealed in September 2025. The transaction is structured as a merger of equals and is expected to close within 12-18 months, subject to shareholder and regulatory approvals.

The merger aims to create a premier copper-focused mining company with over 70% of production coming from copper. Management highlighted the expected benefits, including approximately US$800 million in annual synergies and the potential to unlock US$1.4 billion in annual underlying EBITDA uplift from optimizing the Quebrada Blanca and Collahuasi operations.

The strategic rationale and benefits of the merger are illustrated in this slide:

Teck also announced the sanctioning of the Highland Valley Mine Life Extension project, which is expected to extend the life of this core copper asset. Early works on this project are already progressing.

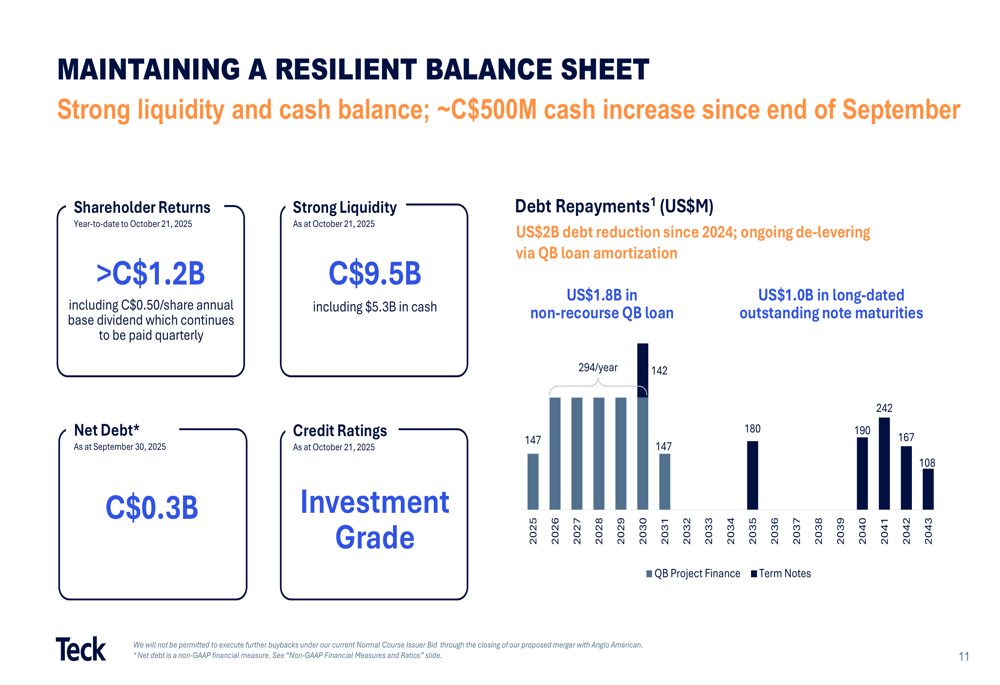

Balance Sheet Strength

Teck maintained a strong financial position with $9.5 billion in liquidity as of October 21, 2025, including $5.3 billion in cash. Net debt remained low at C$0.3 billion as of September 30, 2025, and the company has maintained its investment grade credit ratings.

The company continued to return capital to shareholders, with year-to-date returns exceeding C$1.2 billion, including the annual base dividend of C$0.50 per share and share buybacks of C$144 million in Q3 2025. However, buybacks have been suspended since July 25th due to the merger announcement.

The following chart illustrates Teck’s debt maturity profile and liquidity position:

Operational Challenges and Action Plan

While financial results were strong, Teck continues to face operational challenges at its Quebrada Blanca (QB) operation, where production has been constrained by the pace of Tailings Management Facility (TMF) development. The company is implementing an action plan to address these issues, with several near-term development objectives either completed or in progress.

Mill availability at QB reached 87% in Q3 2025, below the design availability of 92%, while actual utilization was only 70%. Copper recoveries have also fluctuated, reaching 81% in Q3 2025, down from 85% in Q4 2024.

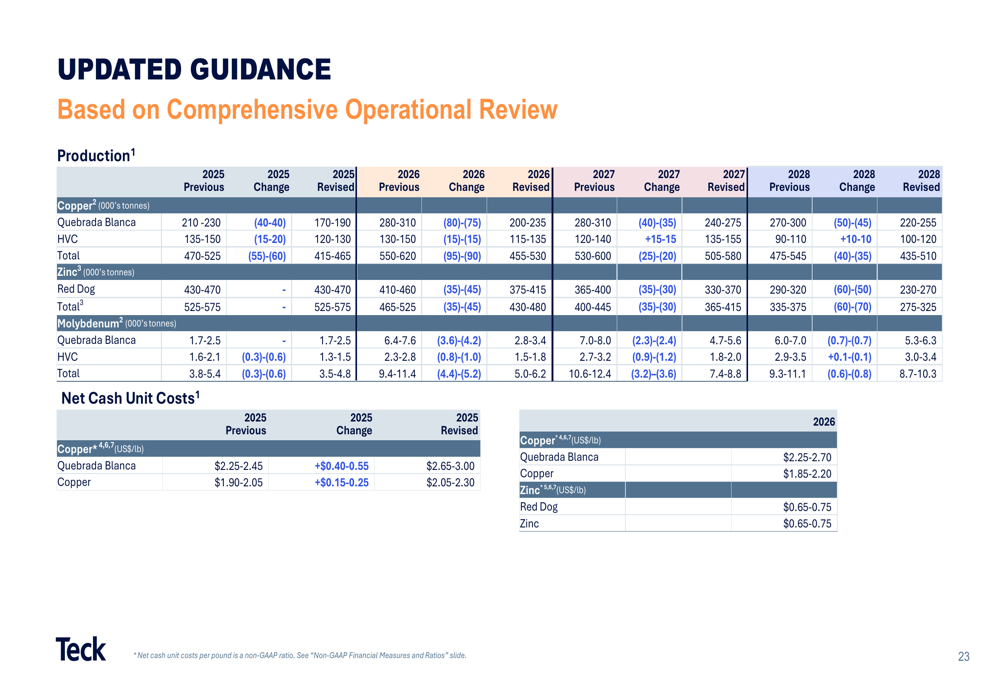

The company has updated its production guidance for QB, factoring in additional TMF development requirements and conservative recovery assumptions. For 2026, the low-end guidance assumes 80% mill availability with partially constrained throughput of 115,000 tonnes per day, while the high-end assumes 86% mill availability with throughput of 132,000 tonnes per day.

Updated Guidance

Teck provided comprehensive updated guidance for its operations through 2028. The revised estimates reflect the operational challenges at QB and adjustments to mine plans at other sites.

The following table presents the updated production and cost guidance:

For 2025, copper production is expected to be 415,000-465,000 tonnes, with net cash unit costs of US$2.05-2.30 per pound. Zinc production is projected at 525,000-575,000 tonnes, with net cash unit costs of US$0.15-0.25 per pound.

Market Outlook

Teck’s presentation highlighted favorable long-term fundamentals for copper, driven by global electrification trends and China’s continued leadership in the energy transition. The company noted that emerging Asian economies have significant growth potential for copper consumption, with per capita usage still well below developed market levels.

In the short term, copper treatment and refining charges remain exceptionally low amid supply disruptions, supporting Teck’s profitability in this segment. For zinc, spot treatment charges are rising but remain low relative to historical norms.

The company also highlighted China’s resilience despite some economic challenges, with electricity production, exports, and industrial production showing positive year-over-year growth in recent months.

Conclusion

Teck Resources delivered strong financial results in Q3 2025, with significant improvements in profitability driven by higher metal prices and operational efficiencies. The proposed merger with Anglo American represents a transformative opportunity to create a leading global copper producer, positioning the company to benefit from growing demand for copper in the energy transition.

While operational challenges persist at the Quebrada Blanca operation, management has implemented a comprehensive action plan and provided updated guidance that reflects a more conservative outlook. With a strong balance sheet and continued focus on shareholder returns, Teck appears well-positioned to navigate these challenges while pursuing its strategic growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.