5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Watsco, Inc. (NYSE:WSO) recently presented its second quarter 2025 investor presentation, highlighting its position as a market leader in the highly fragmented HVAC distribution industry. The presentation comes at a challenging time for the company, which reported Q2 earnings below analyst expectations, with EPS of $4.52 missing the forecasted $4.80 and revenue of $2.06 billion falling short of the expected $2.23 billion.

Following these results, Watsco’s stock has declined to $418.77, down from the $441.62 referenced in the presentation and approaching its 52-week low of $403.01. Despite these short-term challenges, the company emphasized its long-term value creation strategy and continued digital transformation efforts.

Quarterly Performance Highlights

While Watsco’s Q2 2025 results missed analyst forecasts, the company achieved record gross profit margins despite a 4% decline in sales. The earnings miss was largely attributed to the industry’s transition to A2L refrigerants, which affected 55% of Watsco’s historical product sales.

The company’s presentation highlighted its extensive geographic footprint, with 701 locations across North America and the Caribbean, providing strategic coverage in key markets. This network includes 641 locations in the United States, 34 in Canada, and 26 in Latin America and the Caribbean.

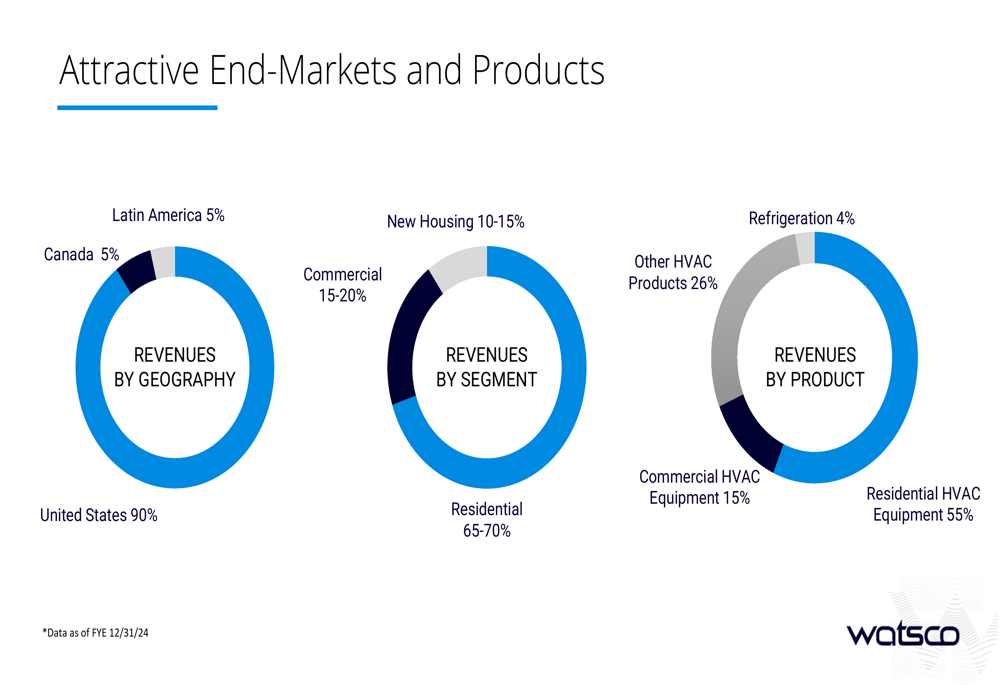

As shown in the following geographic and segment breakdown:

The company’s revenue remains heavily concentrated in the United States (90%), with Canada and Latin America each accounting for 5%. Residential HVAC equipment continues to be the dominant product category at 55% of sales, with the residential segment overall representing 65-70% of the business.

Strategic Initiatives

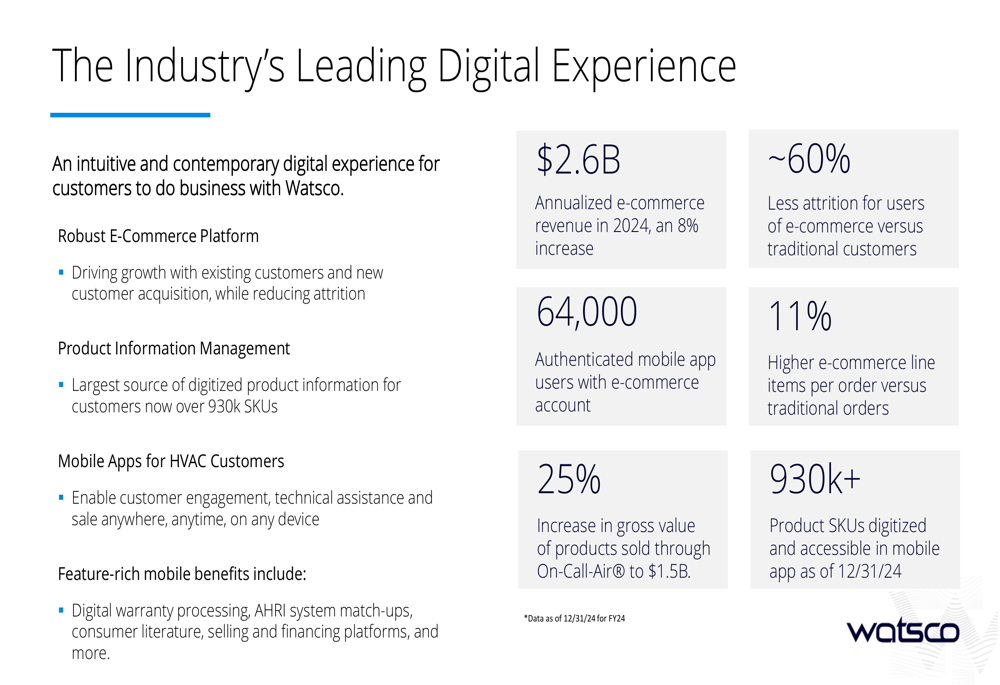

Watsco’s presentation emphasized its ongoing digital transformation as a key strategic initiative. The company has made significant investments in technology to enhance customer experience and operational efficiency.

As illustrated in the following metrics on digital adoption:

E-commerce revenue reached $2.6 billion in 2024, representing an 8% increase. This aligns with the earnings report, which noted e-commerce sales accounting for 34% of total sales. The company has grown its mobile app user base to 64,000 authenticated users with e-commerce accounts, and products sold through On-Call-Air® increased by 25% to $1.5 billion.

The company’s digital strategy is showing tangible benefits, with e-commerce users demonstrating 60% lower attrition rates and 11% higher line items per order compared to traditional customers.

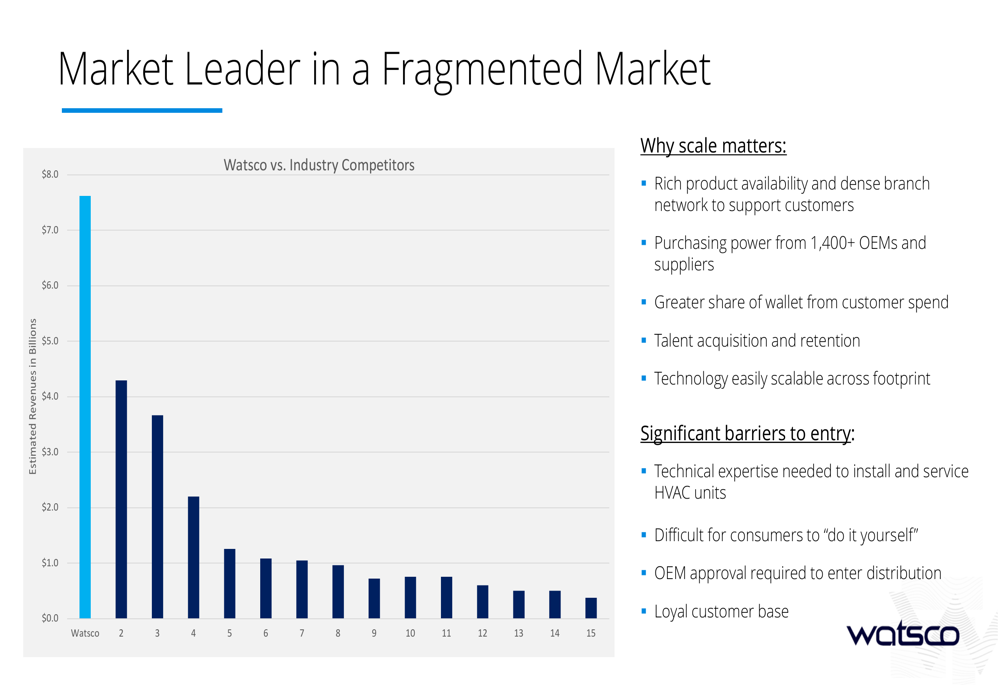

Watsco also highlighted its competitive position in a fragmented market, emphasizing the significant barriers to entry and the advantages of scale:

Despite facing near-term challenges, Watsco’s scale advantages include rich product availability, purchasing power, greater share of wallet, talent acquisition and retention, and technology scalability. These factors position the company to navigate the current market environment and potentially gain market share.

Financial Position and Outlook

Watsco maintains a strong financial position despite the recent earnings miss. The presentation highlighted the company’s robust capital structure and long-term performance metrics:

Since 1989, Watsco has grown revenues from $64 million to $7.5 billion (LTM 6/30/25), representing a 14% CAGR. EBIT has increased from $2 million to $770 million (17% CAGR), while the share price has grown from $2.70 to $441.62 (15% CAGR) over the same period.

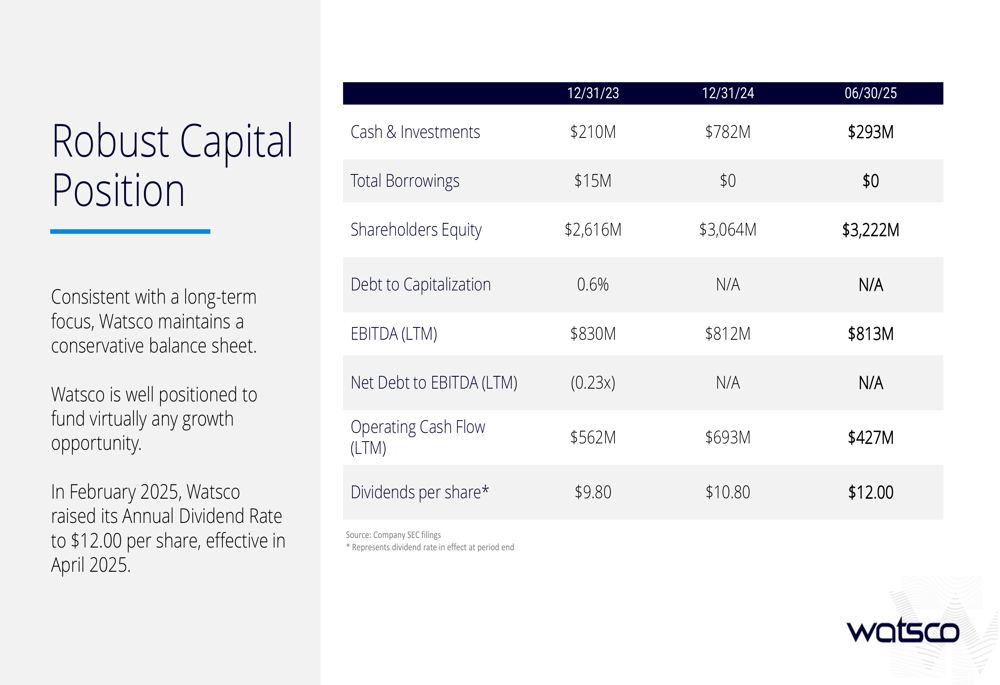

The company’s financial strength is further illustrated by its capital position:

As of June 30, 2025, Watsco reported $293 million in cash and investments, no borrowings, and shareholders’ equity of $3.22 billion. The company has consistently increased its dividend, which stood at $12.00 per share as of the presentation date, representing a 21% CAGR since 1989.

During the earnings call, executives outlined "Dream Plan Two," targeting $10 billion in revenue, a 30% gross profit margin, and five inventory turns. However, the company faces near-term challenges, including the A2L refrigerant transition, soft market conditions, and a 15-20% decline in residential new construction.

Forward-Looking Statements

Watsco’s presentation emphasized its ESG initiatives and long-term value creation strategy. The company highlighted its environmental impact, including 24.5 million metric tons of CO₂e averted from the sale of high-efficiency equipment from January 2020 to June 2025.

The company’s ownership culture was presented as a key differentiator, with 160+ restricted stock plan participants and operating leaders possessing over $415 million in restricted stock. This long-term incentive structure aligns with Watsco’s focus on sustainable growth and shareholder returns.

Watsco ranks #25 out of approximately 1,600 public companies for 30-year shareholder returns, with annualized total shareholder returns of 19% over 30 years. However, investors should note the current challenges facing the company, including the refrigerant transition and market softness that have impacted recent results.

CEO Albert Naumann described 2025 as "the noisiest year in HVAC ever" during the earnings call, but expressed confidence in the company’s ability to "win in any environment and emerge bigger and stronger." As Watsco navigates these challenges, its strong balance sheet and technology investments may provide competitive advantages in a fragmented industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.