Raymond James initiates QXO stock with Outperform rating on acquisition strategy

Introduction & Market Context

AAR Corp (NYSE:AIR) presented its fourth quarter and full fiscal year 2025 results on July 16, 2025, highlighting strong financial performance across most business segments. The company, which is celebrating its 70th anniversary this year, reported significant growth in revenue and profitability while continuing to optimize its portfolio through strategic acquisitions and divestitures.

The aviation services provider saw its stock rise 2.03% to $73.39 on the day of the earnings call, with an additional 0.83% gain in aftermarket trading, suggesting positive investor reception to the results. This follows a mixed market reaction to the company’s Q3 results earlier in the year, when AAR missed revenue expectations despite posting record sales.

As shown in the company’s presentation overview:

Quarterly Performance Highlights

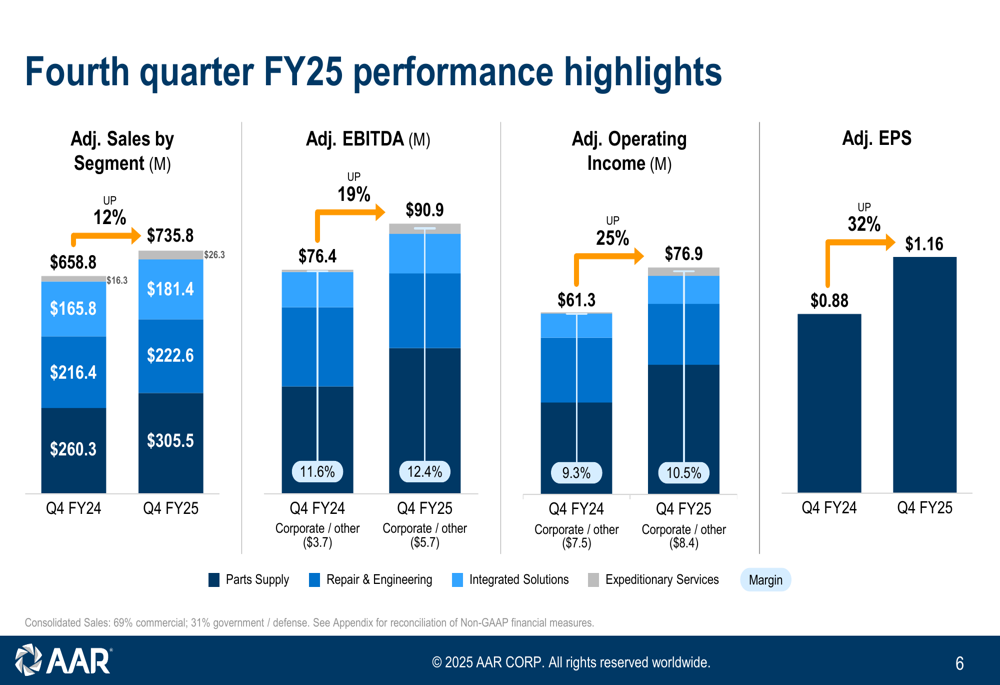

AAR delivered impressive fourth quarter results, with adjusted sales increasing 12% to $735.8 million compared to Q4 FY24. Adjusted EBITDA rose 19% to $90.9 million, while adjusted earnings per share jumped 32% to $1.16, significantly outpacing sales growth and indicating improved operational efficiency.

The quarterly performance breakdown reveals strong results across most business segments:

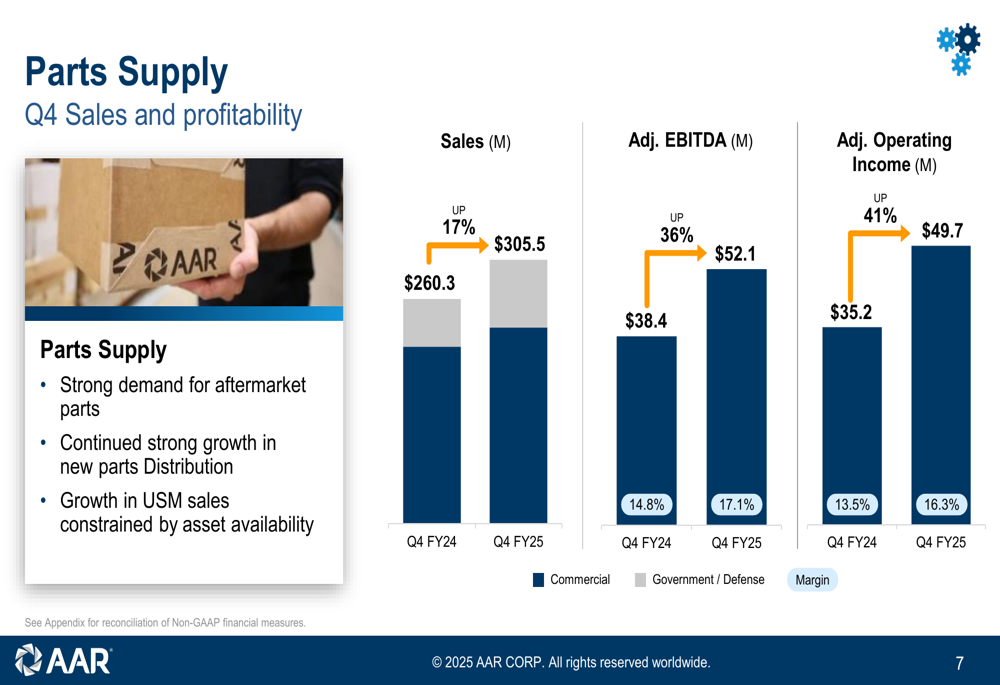

The Parts Supply segment was the standout performer, with sales increasing 17% to $305.5 million and adjusted EBITDA surging 36% to $52.1 million. This segment benefited from strong demand for aftermarket parts and continued growth in new parts distribution, though the company noted that growth in USM (used serviceable material) sales was constrained by asset availability.

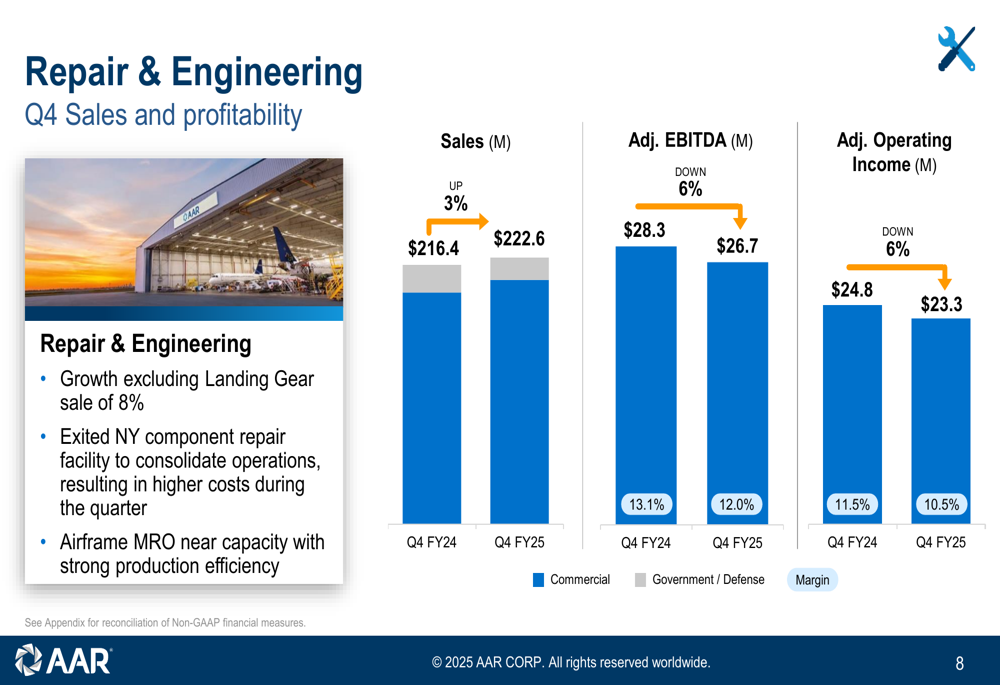

The Repair & Engineering segment showed more modest growth, with sales increasing 3% to $222.6 million. However, adjusted EBITDA and operating income both decreased by 6%. The company attributed this mixed performance to the divestiture of its Landing Gear business, noting that growth excluding this sale would have been 8%. AAR also mentioned the exit from its New York component repair facility as part of its operational consolidation efforts.

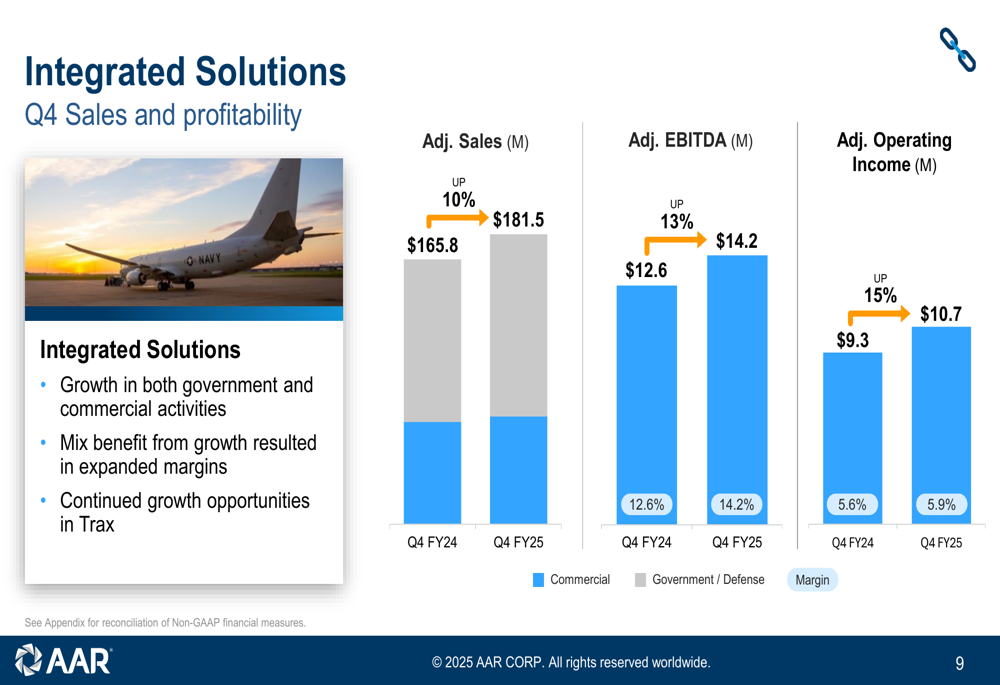

The Integrated Solutions segment delivered solid results, with adjusted sales increasing 10% to $181.5 million and adjusted EBITDA rising 13% to $14.2 million. This segment saw growth in both government and commercial activities, with expanded margins due to favorable mix benefits.

Detailed Financial Analysis

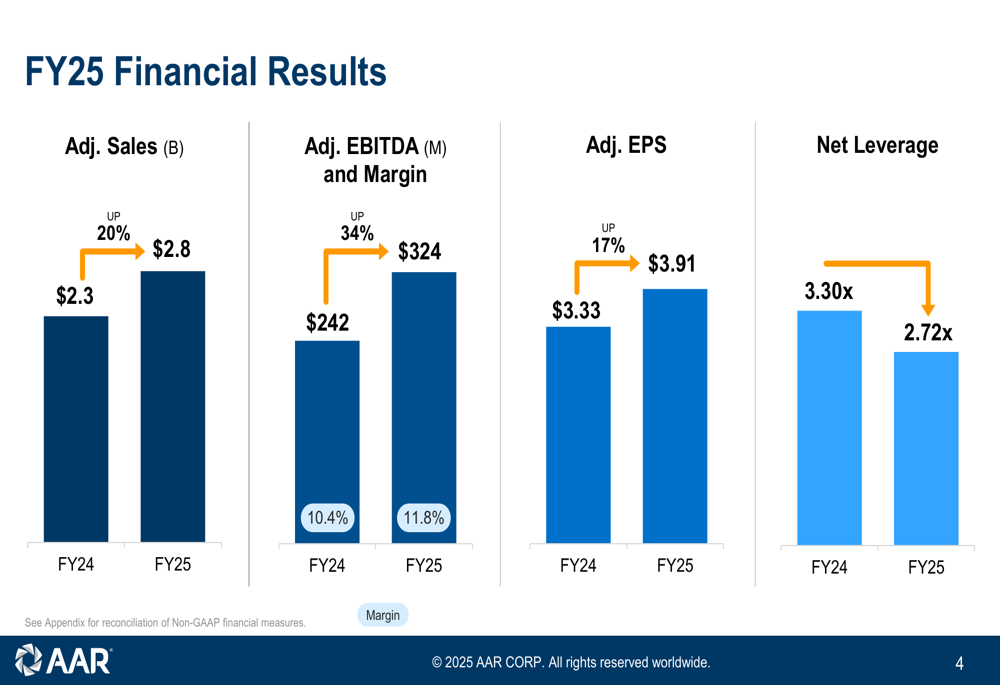

For the full fiscal year 2025, AAR reported impressive financial results across all key metrics. Adjusted sales increased 20% to $2.8 billion from $2.3 billion in FY24, while adjusted EBITDA rose 34% to $324 million, with margin improvements from 10.4% to 11.8%. Adjusted earnings per share grew 17% from $3.33 to $3.91.

The full-year performance demonstrates AAR’s successful execution of its growth strategy and operational improvements:

These results align with the trajectory seen in the company’s Q3 FY2025 report, which showed a 20% year-over-year increase in sales and a 39% rise in adjusted EBITDA. The consistent performance throughout the fiscal year reflects AAR’s ability to capitalize on strong demand in both commercial and government sectors.

Strategic Initiatives and Portfolio Optimization

AAR has been actively refining and optimizing its portfolio, with several key achievements highlighted in the presentation. The company has substantially completed the integration of Triumph Product Support, which it acquired earlier, and has finalized the divestiture of its Landing Gear business.

The company also detailed progress on various strategic initiatives, including extending its agreement with FTAI, signing a Supply Chain Alliance charter with the DLA, continuing hangar expansions, and establishing a joint venture with KIRA. Additionally, AAR’s Trax software solution has gained significant traction, securing new business with major airlines including Delta TechOps.

Looking ahead to FY26, AAR outlined several strategic objectives, including winning market share through new business in parts distribution, completing its Oklahoma City hangar expansion, driving component services volume through cross-selling, and fully completing the Product Support integration to realize $10 million in cost synergies.

Balance Sheet Improvements

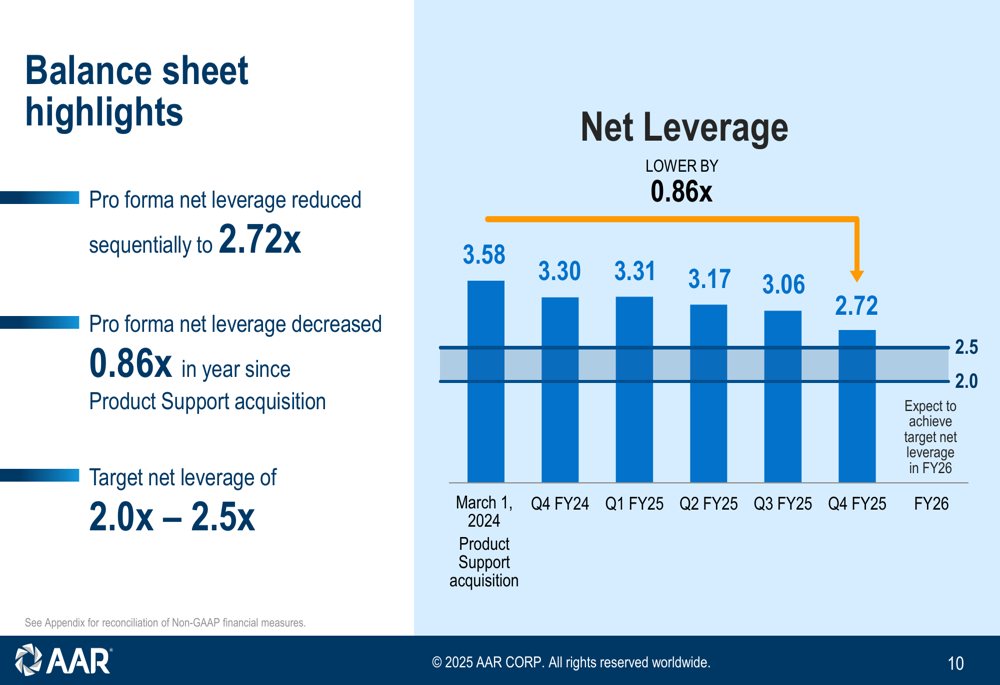

A key focus for AAR has been strengthening its balance sheet by reducing leverage. The company has made significant progress in this area, with pro forma net leverage decreasing to 2.72x at the end of Q4 FY25, down from 3.58x in Q3 FY24. This represents a reduction of 0.86x in the year since the Product Support acquisition.

The company expects to achieve its target net leverage range of 2.0x to 2.5x in FY26, as illustrated in the following chart:

This continued deleveraging provides AAR with increased financial flexibility for future growth initiatives and potential acquisitions. The improvement from the 3.06x leverage reported in Q3 FY25 to 2.72x in Q4 demonstrates the company’s commitment to strengthening its financial position.

Forward-Looking Statements for FY26

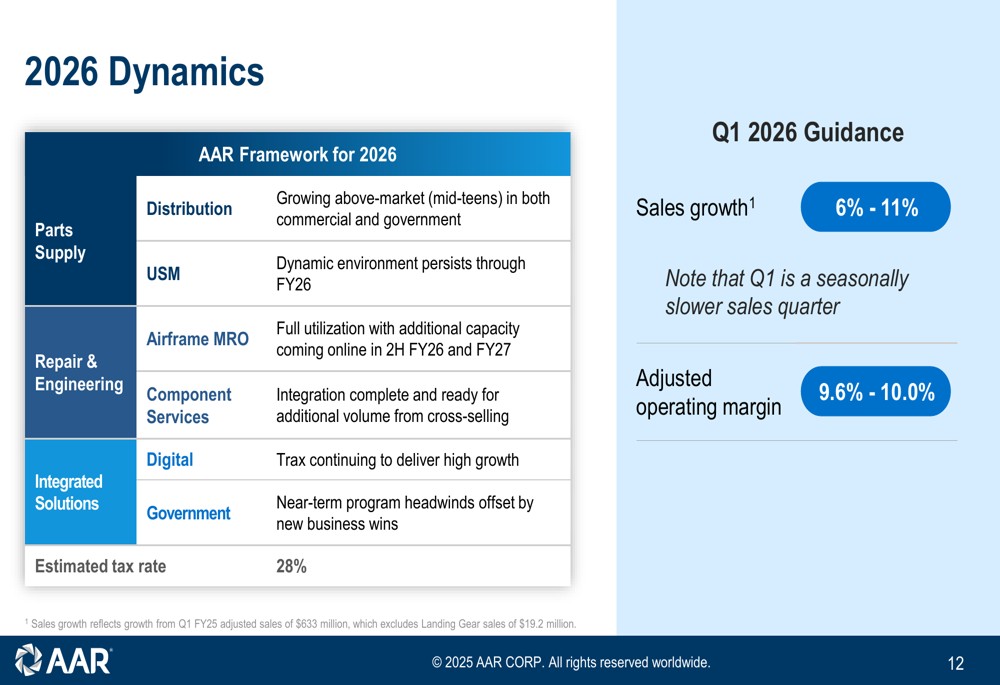

For fiscal year 2026, AAR provided a framework highlighting expected dynamics across its business segments. In Parts Supply, the company anticipates above-market growth (mid-teens) in Distribution for both commercial and government sectors, while noting that the dynamic environment for USM will persist through FY26.

In Repair & Engineering, AAR expects full utilization of its Airframe MRO capacity, with additional capacity coming online in the second half of FY26 and into FY27. For Integrated Solutions, the company projects continued high growth for its Trax digital business, while acknowledging near-term program headwinds in its Government business that should be offset by new business wins.

For Q1 FY26, which the company noted is typically a seasonally slower quarter, AAR projects sales growth of 6-11% and adjusted operating margin of 9.6-10.0%. This guidance suggests continued momentum, albeit at a more moderate pace than the 12% sales growth achieved in Q4 FY25.

Overall, AAR’s Q4 and full-year FY25 results demonstrate strong performance across most business segments, successful portfolio optimization, and continued balance sheet improvement. The company appears well-positioned to maintain its growth trajectory in FY26, supported by strategic initiatives and expanding capabilities in high-growth areas like digital solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.