After-hours movers: AMD, Pinterest, CAVA Group, Toast, and more

Introduction & Market Context

Acadian Asset Management Inc. presented its third-quarter 2025 earnings results on October 30, showcasing strong growth in assets under management and client inflows despite a challenging market environment. The systematic investment manager, with a nearly 40-year operating history, reported significant increases in economic net income and management fees, though performance fees declined substantially year-over-year.

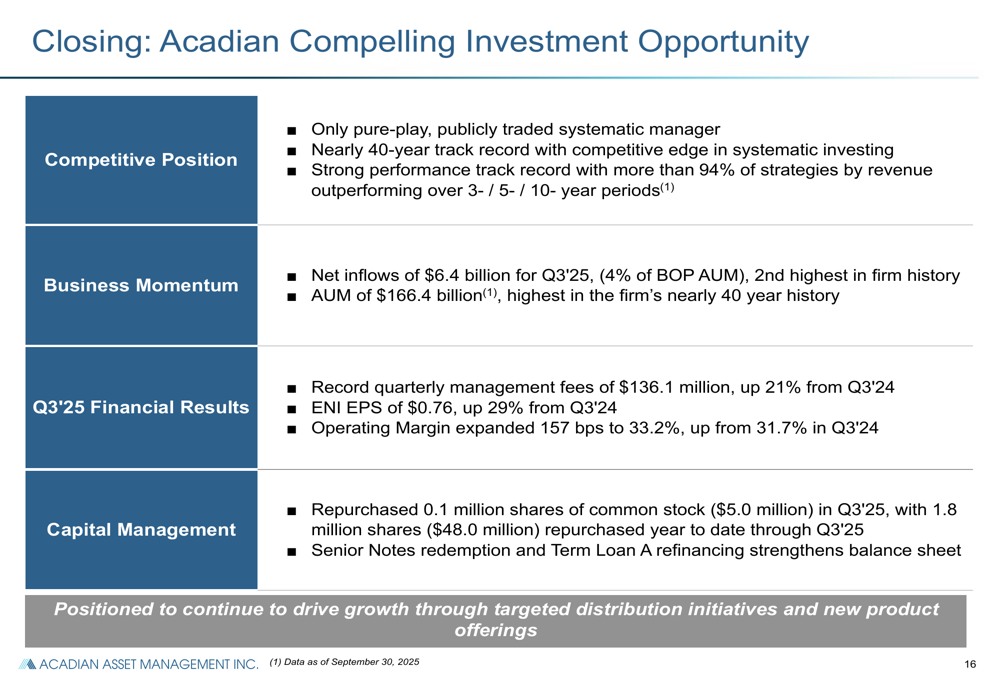

The company emphasized its position as the only pure-play publicly traded systematic manager, highlighting its long-term investment outperformance and global distribution capabilities as key competitive advantages. With $166.4 billion in assets under management, Acadian has leveraged its quantitative approach across multiple strategy groups including global equity, emerging markets, and enhanced equity products.

Quarterly Performance Highlights

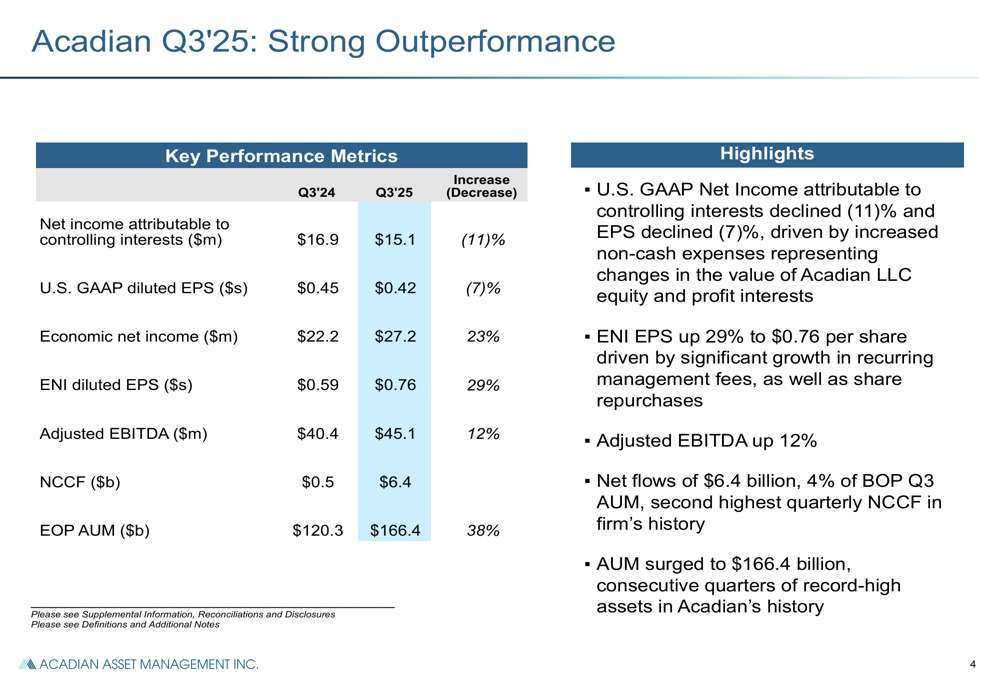

Acadian reported mixed GAAP results for Q3 2025, with net income attributable to controlling interests decreasing 11% year-over-year to $15.1 million and diluted EPS falling 7% to $0.42. However, the company’s preferred profitability metrics showed substantial improvement, with economic net income (ENI) increasing 23% to $27.2 million and ENI diluted EPS rising 29% to $0.76.

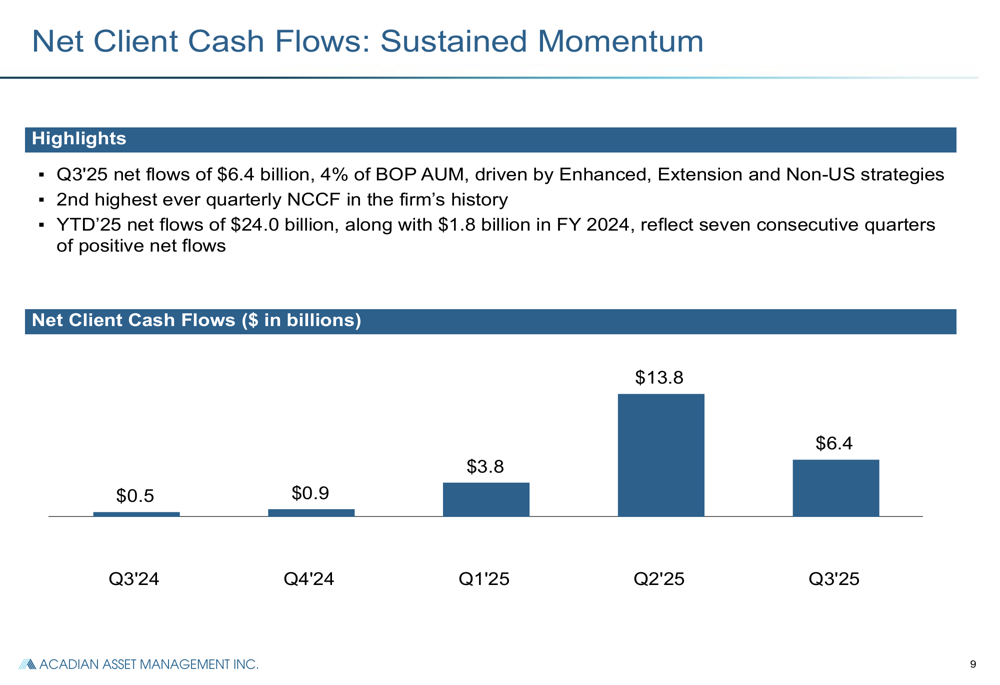

The quarter’s standout metric was the significant growth in assets under management, which surged 38% year-over-year to $166.4 billion, supported by $6.4 billion in net client cash flows – the second highest quarterly inflow in the firm’s history. These strong flows were primarily driven by enhanced, extension, and non-US strategies.

As shown in the following performance metrics overview:

The company’s adjusted EBITDA increased 12% year-over-year to $45.1 million, reflecting the firm’s improved operational efficiency and scale. Management emphasized that these results demonstrate Acadian’s ability to generate sustainable growth through both market appreciation and new client mandates.

Detailed Financial Analysis

Acadian’s ENI revenue reached $136.3 million in Q3 2025, representing a 12% increase from the prior year. This growth was driven entirely by management fees, which rose 21% to $136.1 million, reflecting a 34% increase in average AUM. However, performance fees declined significantly to just $0.2 million from $10.1 million in Q3 2024.

The following chart illustrates the shift in revenue composition:

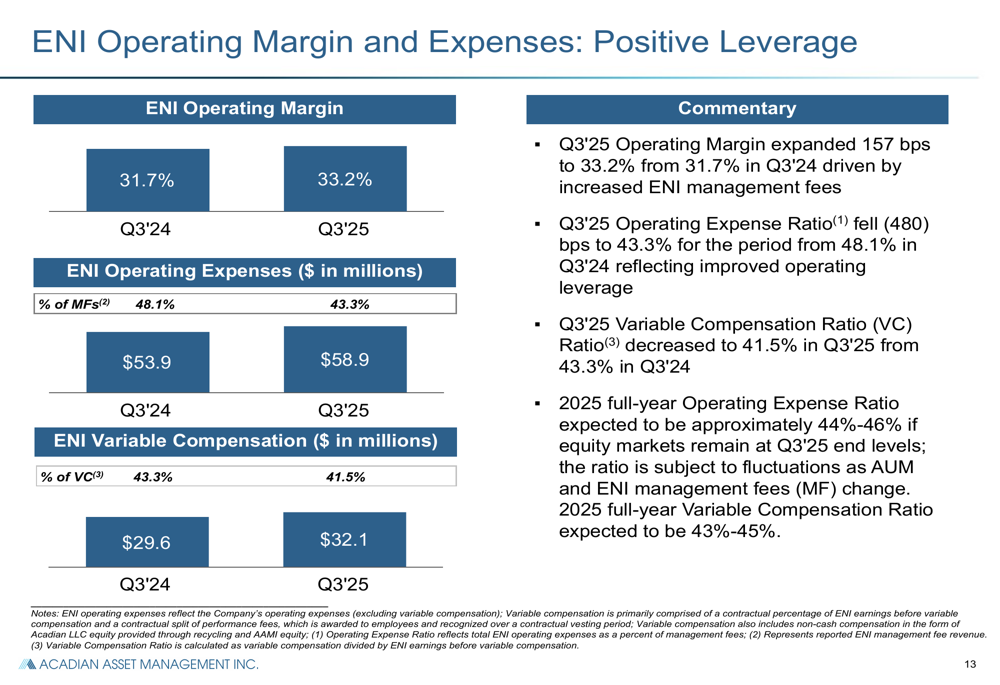

The company’s operating margin expanded to 33.2% in Q3 2025 from 31.7% in the prior year, demonstrating improved operating leverage as the business scaled. Operating expenses as a percentage of management fees decreased to 43.3% from 48.1% in Q3 2024, while the variable compensation ratio declined to 41.5% from 43.3%.

This margin expansion is visualized in the following slide:

Acadian’s balance sheet remains strong, with $117.3 million in cash and cash equivalents. The company announced plans to redeem its 4.80% Senior Notes using a new $200 million committed bank term loan and balance sheet cash, with the transaction expected to close on December 1, 2025.

The company has maintained its capital return program, repurchasing 0.1 million shares for $5.0 million during the quarter at an average price of $48.58. Since Q4 2019, Acadian has reduced its share count by 58%, from 86.0 million to 35.8 million shares outstanding, returning $1.4 billion to shareholders through buybacks and dividends.

Strategic Initiatives & Competitive Positioning

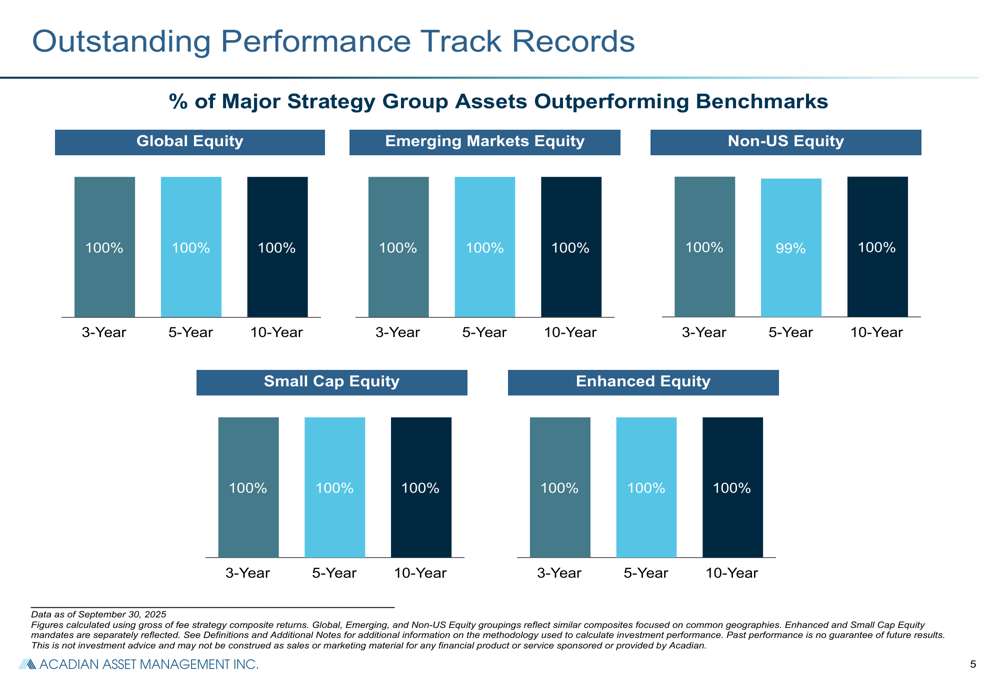

Acadian highlighted its investment performance as a key competitive advantage, with 95% of strategies by revenue outperforming their benchmarks over a 5-year period. The company’s revenue-weighted 5-year annualized excess return stands at an impressive 4.5%.

The following chart demonstrates this consistent outperformance across major strategy groups:

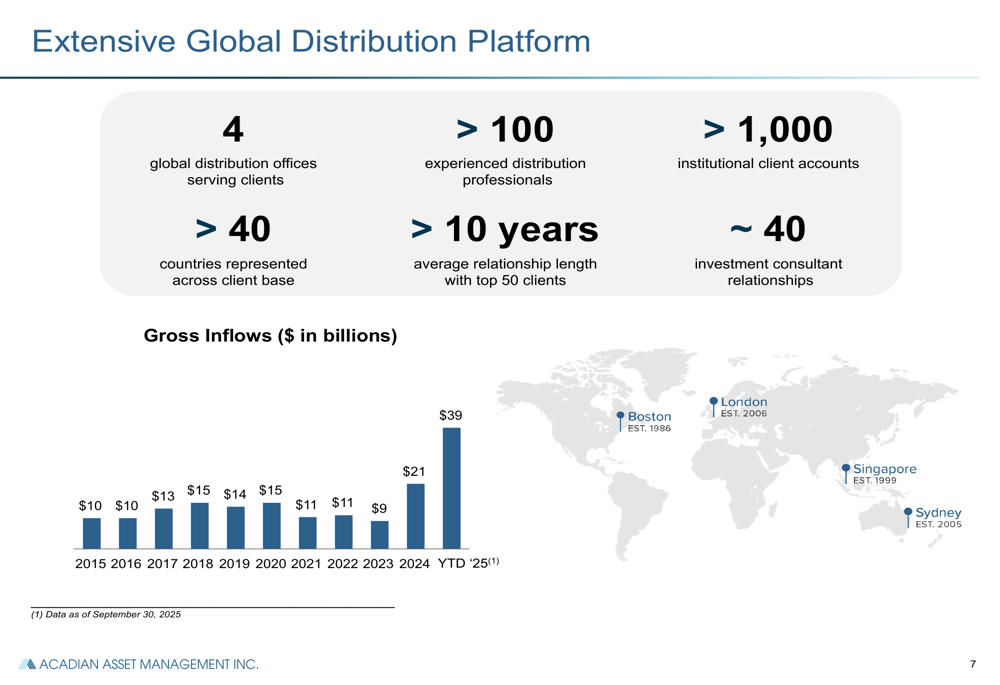

The company’s global distribution platform has been instrumental in driving growth, with offices in Boston, London, Singapore, and Sydney serving clients across more than 40 countries. Acadian’s institutional client base includes 5 of the top 20 global asset owners and 24 of the top 50 U.S. retirement plans.

This extensive distribution network has supported strong gross inflows, as illustrated below:

The company’s net client cash flows have shown sustained momentum over recent quarters, with Q3 2025 representing the second-highest quarterly inflow in Acadian’s history:

Forward-Looking Statements

Looking ahead, Acadian expects its full-year 2025 operating expense ratio to be approximately 44-46% and its variable compensation ratio to be 43-45%. Management expressed confidence in the firm’s ability to continue driving growth through targeted distribution initiatives and new product offerings.

The company summarized its investment thesis with the following key points:

Acadian’s management emphasized its commitment to maintaining strong investment performance while expanding its product offerings and global reach. The company’s systematic approach to investing, combined with its data-driven culture and experienced team of over 120 investment professionals, positions it well to capitalize on continued growth opportunities in the asset management industry.

While the decline in performance fees presents a potential headwind, the strong growth in management fees and AUM suggests that Acadian’s core business remains robust. The company’s focus on operating efficiency and margin expansion further supports its ability to generate sustainable earnings growth despite the competitive market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.