Palantir shares slip by 7% despite posting record revenue in third quarter

Introduction & Market Context

Spanish multinational Acciona SA (BME:ANA) presented its H1 2025 results on July 29, highlighting substantial financial growth and strategic progress across its business segments. The company reported significant EBITDA and profit increases, driven by both operational improvements and its asset rotation strategy, despite challenges in certain markets.

The presentation revealed a company actively reshaping its portfolio, with a particular focus on deleveraging and maintaining investment grade ratings while continuing strategic growth in renewable energy and infrastructure.

Financial Performance Highlights

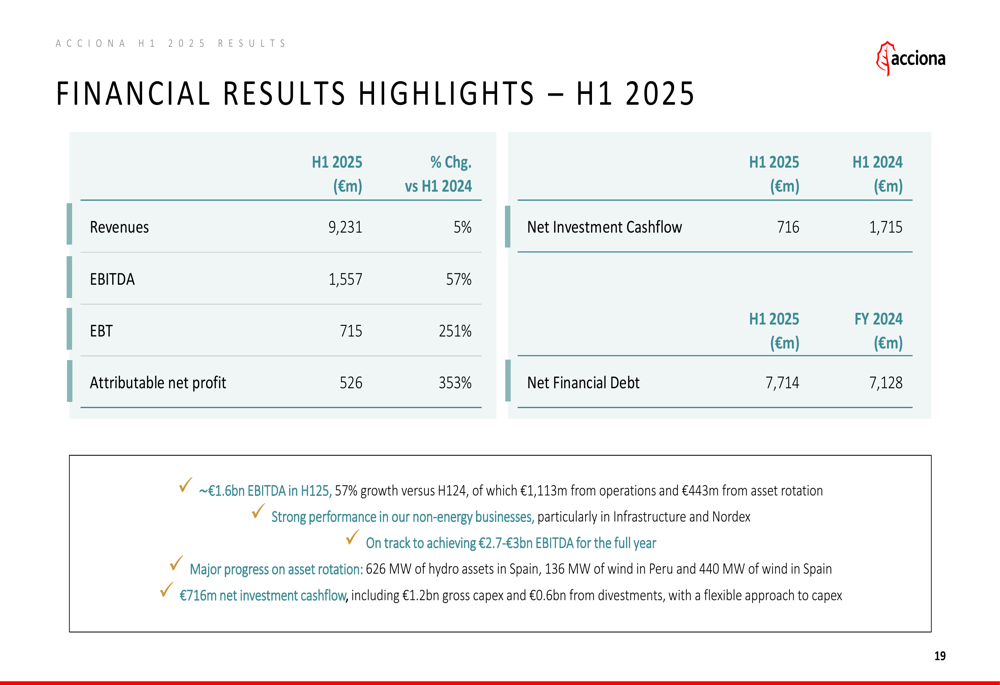

Acciona delivered robust financial results in the first half of 2025, with revenue increasing 5% year-over-year to €9.23 billion. More impressively, EBITDA surged 57% to €1.56 billion, while attributable net profit soared 353% to €526 million.

As shown in the following financial highlights chart:

The company’s EBITDA growth was driven by both operational performance (€1.11 billion) and asset rotation (€443 million). The presentation indicated Acciona is on track to achieve €2.7-3 billion in EBITDA for the full year, though this appears to differ from the €2.2-2.25 billion guidance mentioned in recent earnings calls.

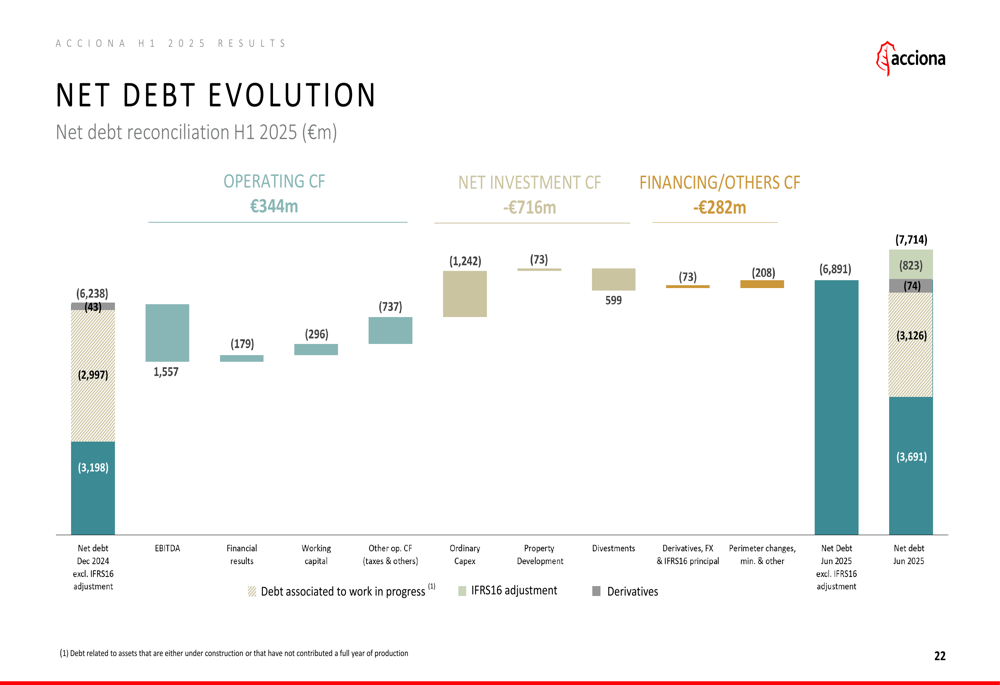

Net financial debt increased to €7.71 billion as of June 2025, up from €7.13 billion at the end of 2024. This debt evolution is illustrated in the following chart:

Strategic Initiatives

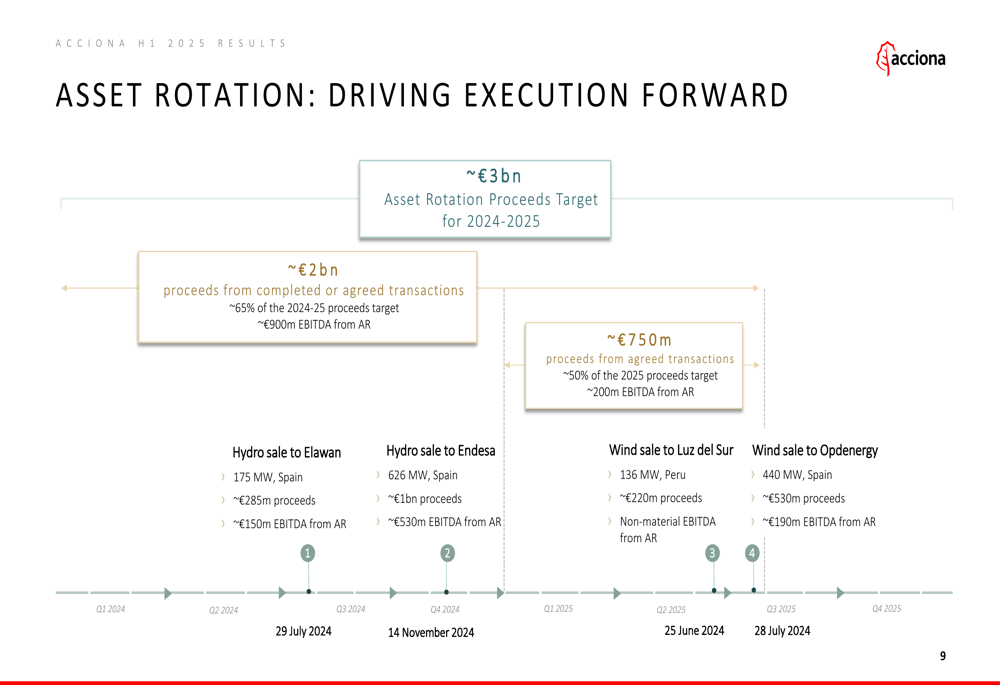

A central theme of Acciona’s presentation was its asset rotation strategy, which is progressing well with approximately €2 billion in proceeds secured from completed or agreed transactions. This represents about 65% of the company’s 2024-2025 target.

The asset rotation strategy is illustrated in the following chart:

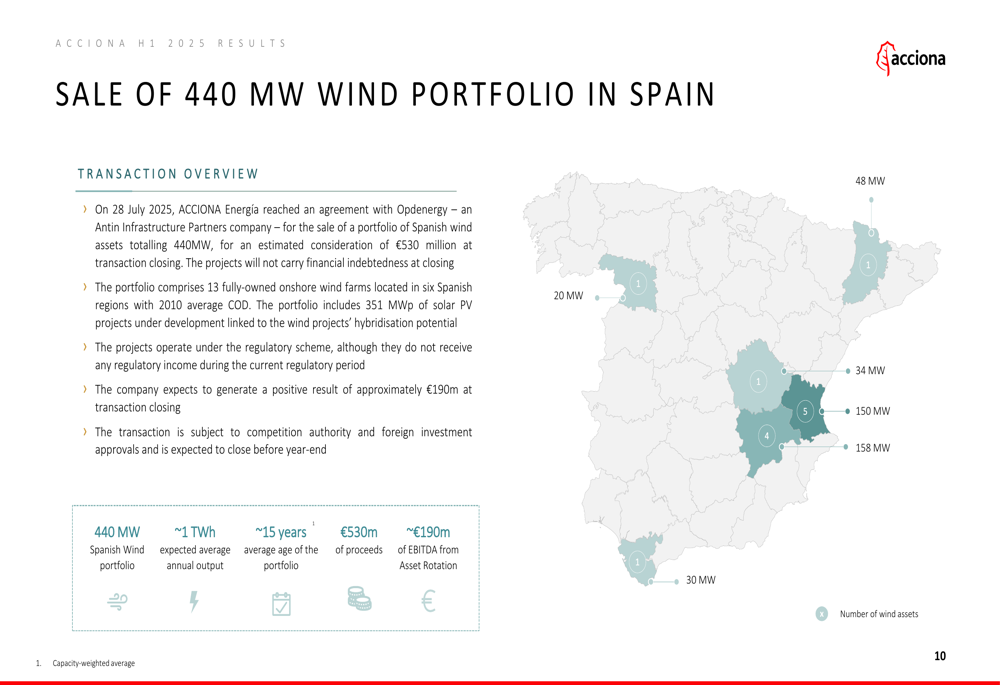

One of the most significant recent transactions was the sale of a 440 MW wind portfolio in Spain to Opdenergy for €530 million, announced on July 28, 2025. This portfolio consists of 13 fully-owned onshore wind farms across six Spanish regions, with an average commissioning date of 2010, and is expected to generate approximately €190 million in EBITDA from asset rotation.

The details of this transaction are shown in the following slide:

Operational Progress

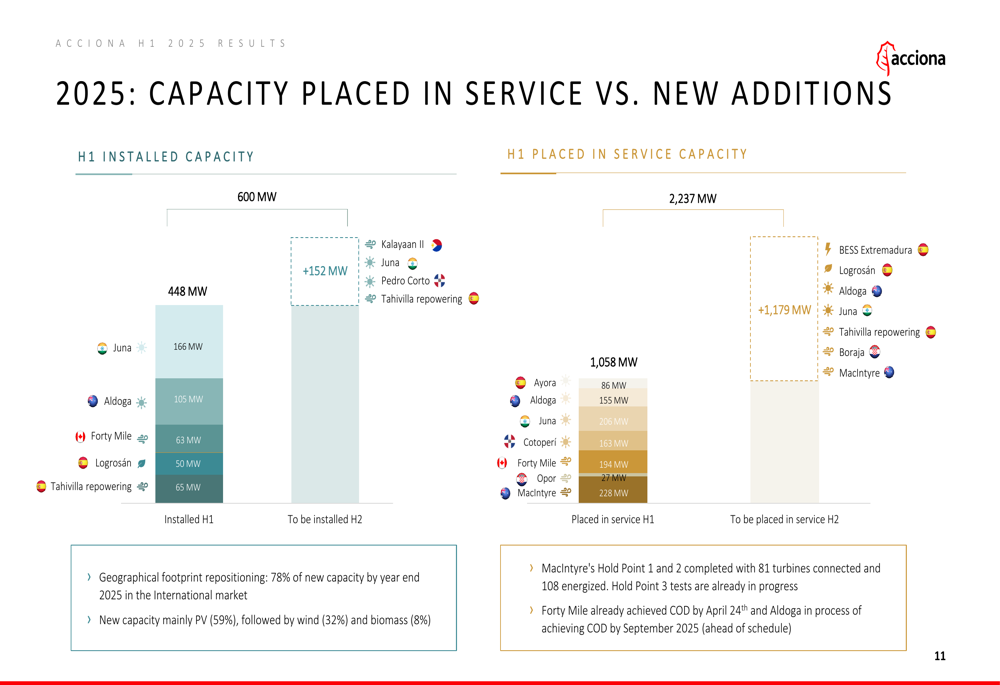

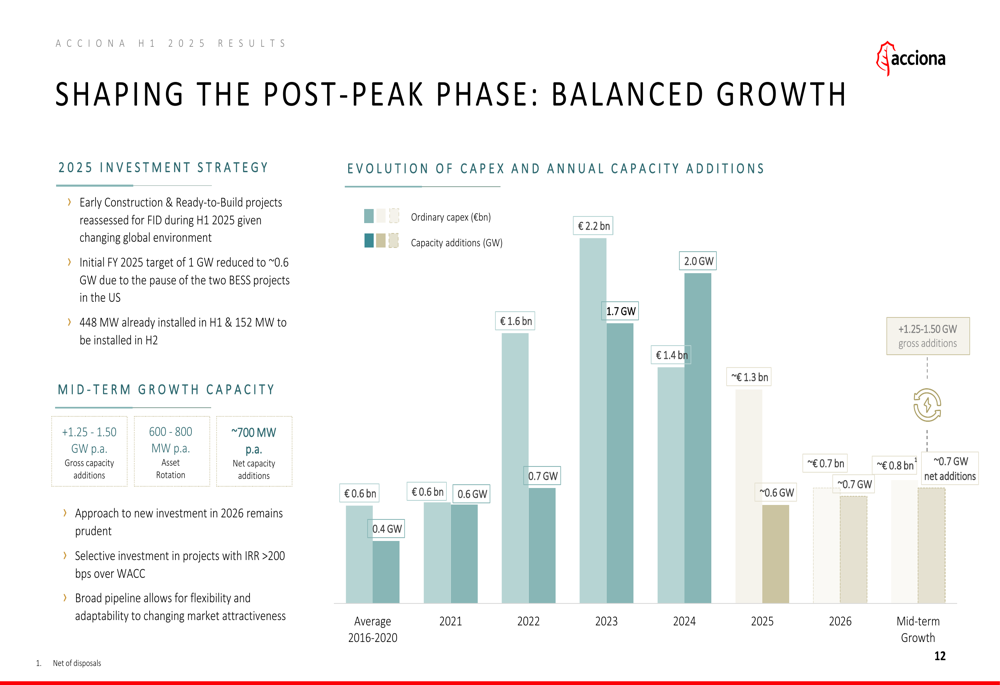

Acciona reported substantial progress in its renewable energy capacity expansion, with 448 MW installed in H1 2025 and 1,058 MW placed in service during the same period. The company has adjusted its 2025 investment strategy, reducing its initial full-year target from 1 GW to approximately 0.6 GW of new capacity.

The following chart details the capacity placed in service versus new additions:

The company is also reshaping its post-peak growth phase, taking a more balanced approach to investments with projected capex of approximately €1.3 billion in 2025, declining to around €0.7 billion in 2026:

Business Segment Performance

Acciona’s presentation highlighted strong performance across its three main business segments:

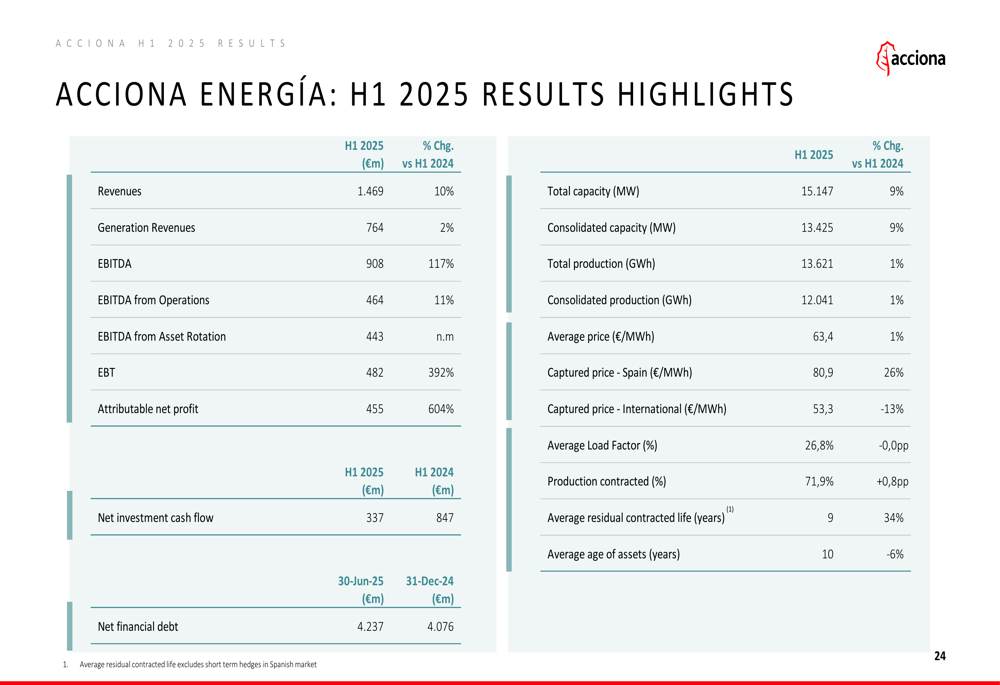

1. ACCIONA Energía: Delivered exceptional results with EBITDA of €908 million, up 117% year-over-year. The energy division’s total capacity reached 15,147 MW (up 9%), with consolidated production increasing by 1% to 12,041 GWh. The average price was €63.4/MWh (up 1%), with 71.9% of production contracted.

2. Infrastructure: Continued to secure long-term growth with a record backlog of €58 billion (up 7% vs December 2024). The division reported EBITDA of €352 million, a 6% increase year-over-year, with growth anchored in concessions.

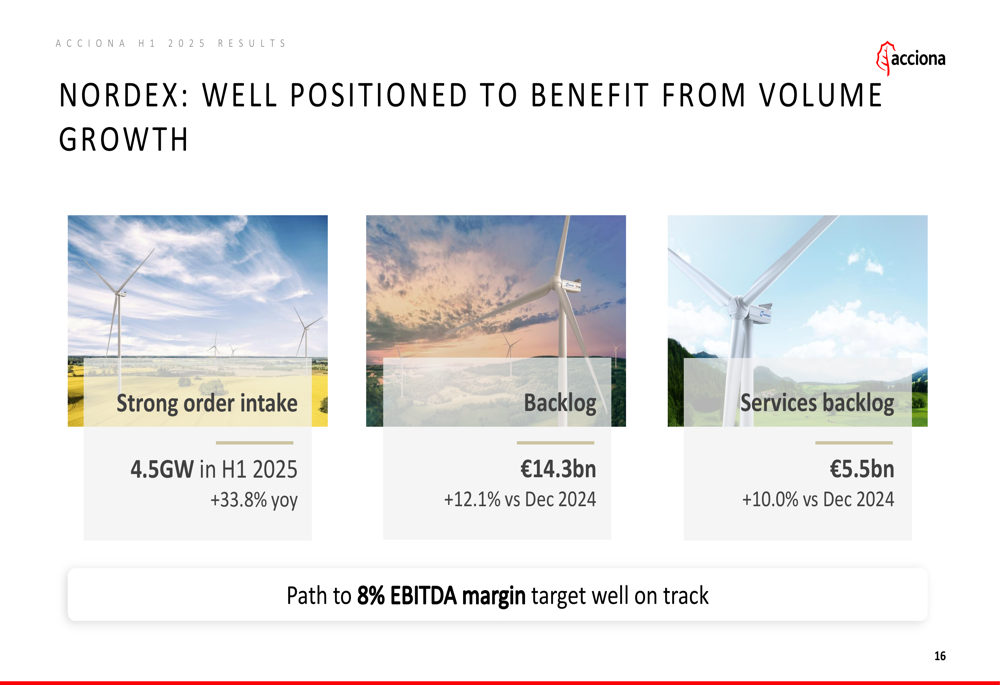

3. Nordex: Demonstrated strong momentum with order intake of 4.5 GW in H1 2025 (up 33.8% year-over-year) and a backlog of €14.3 billion (up 12.1% vs December 2024). The company reported EBITDA of €273 million (up 24% year-over-year) and confirmed its guidance for the full year 2025.

Forward-Looking Statements

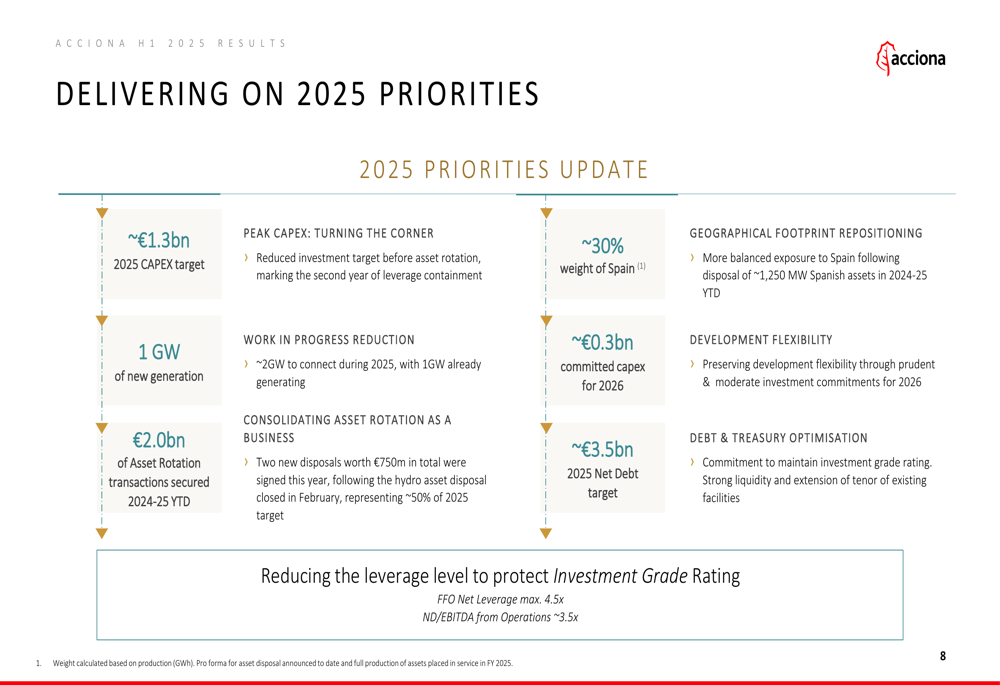

Acciona outlined several key priorities for the remainder of 2025, focusing on deleveraging to protect its investment grade rating. The company is targeting a net debt to EBITDA ratio from operations of approximately 3.5x and is committed to maintaining financial flexibility.

The company is also addressing challenges in the US renewable energy market, where tariffs and new FEOC (Foreign Entity of Concern) provisions are limiting access to IRA tax credits. In response, Acciona has paused 0.4 GW of battery energy storage system (BESS) projects in the US while maintaining 1.4 GW of projects with safe harbor provisions.

Despite these challenges, Acciona remains focused on its 2025 priorities, including reducing its capex to €1.3 billion, placing 2 GW of new generation into service during the year, and continuing its asset rotation strategy to achieve approximately €3 billion in proceeds for 2024-2025.

As the company’s presentation demonstrates, Acciona is delivering on its strategic priorities while adapting to changing market conditions:

With its diversified business model, strong project pipeline, and strategic focus on deleveraging and portfolio optimization, Acciona appears well-positioned to navigate market challenges while continuing to deliver strong financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.