TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

ACS Group presented its H1 2025 financial results on July 30, showing robust growth across most business segments, with particularly strong performance from its Turner division. The construction and infrastructure giant reported significant increases in sales, profits, and order backlog, reinforcing its strategic focus on digital infrastructure and data centers.

The company’s performance comes amid strong demand in the construction sector, particularly in digital infrastructure, where ACS has positioned itself as a key player in the rapidly expanding data center market.

Quarterly Performance Highlights

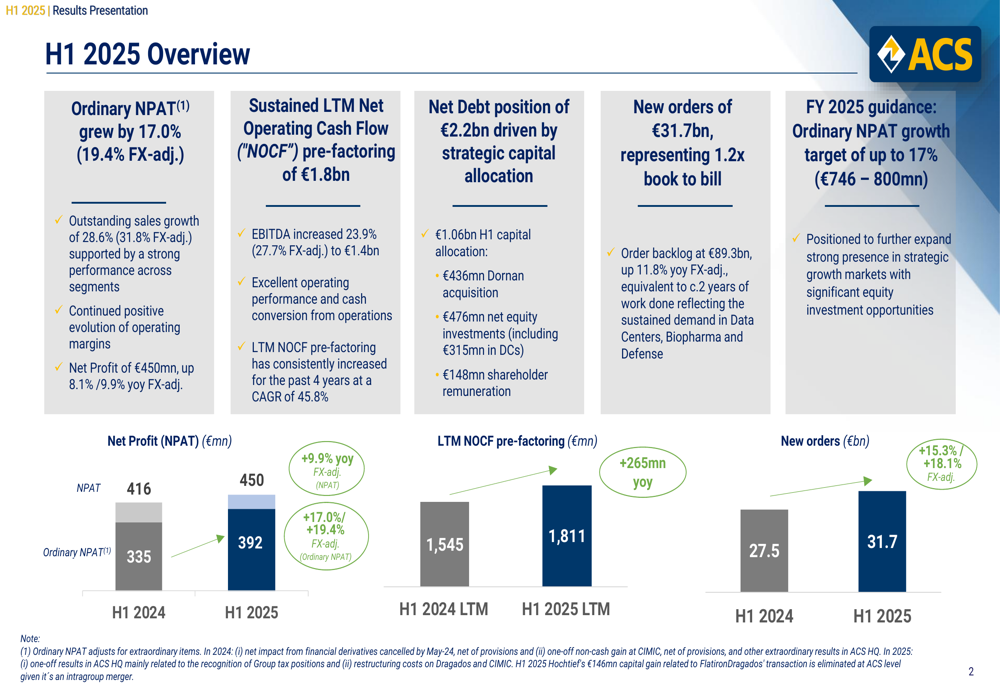

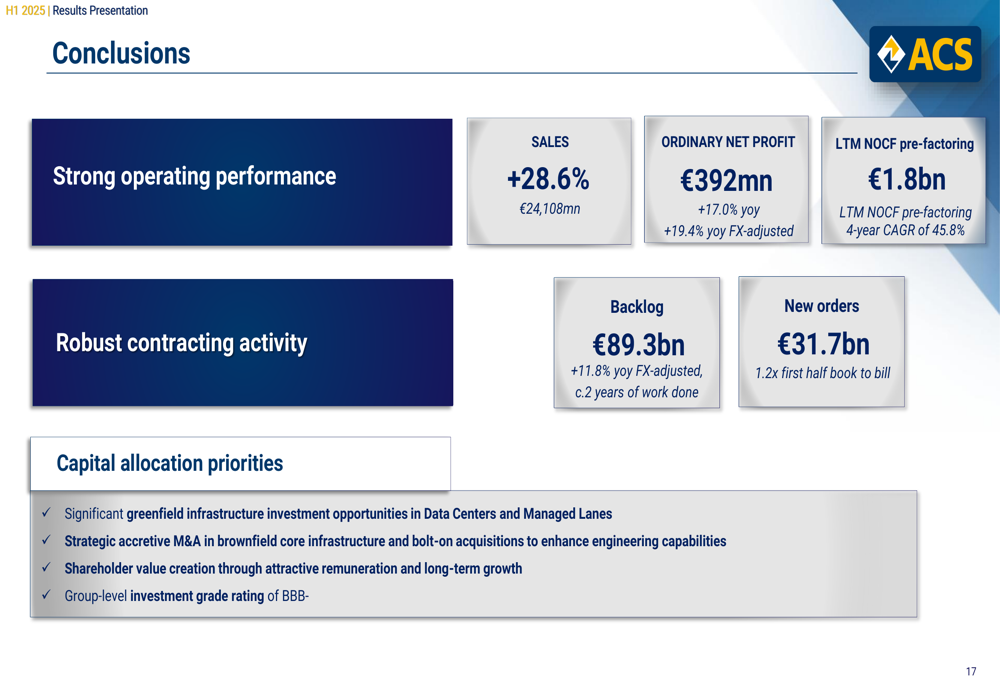

ACS reported sales of €24.1 billion for H1 2025, representing a substantial 28.6% increase (31.8% FX-adjusted) compared to the same period last year. Ordinary net profit grew by 17.0% (19.4% FX-adjusted) to €392 million, while net profit reached €450 million, up 8.1% year-over-year.

The company’s EBITDA increased by 23.9% to €1.4 billion, reflecting improved operational efficiency across most business segments. Cash generation remained strong, with last twelve months (LTM) net operating cash flow pre-factoring reaching €1.8 billion.

As shown in the following overview of key financial metrics:

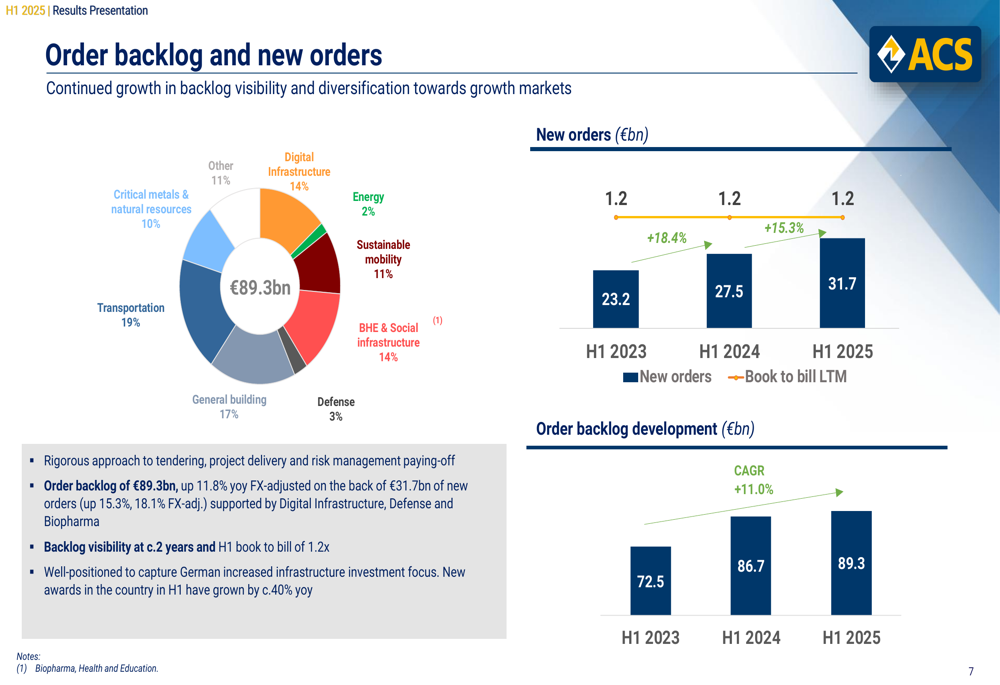

New orders for the period totaled €31.7 billion, representing a book-to-bill ratio of 1.2x, indicating strong future revenue potential. The order backlog reached €89.3 billion, an 11.8% increase on an FX-adjusted basis, equivalent to approximately two years of work.

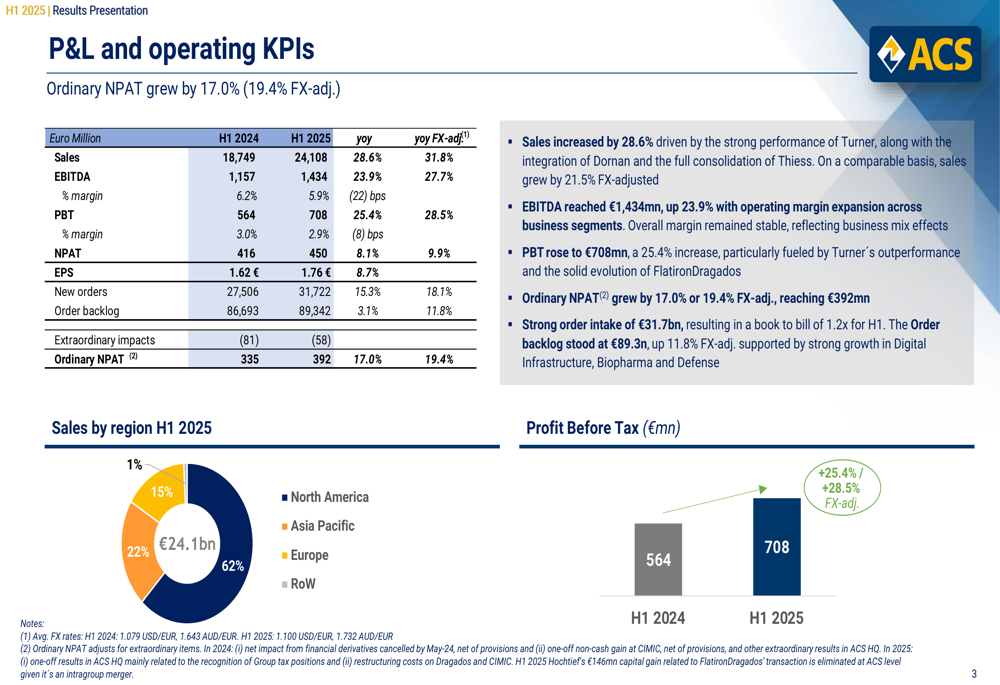

The detailed P&L statement highlights the company’s strong performance across key financial metrics:

Segment Analysis

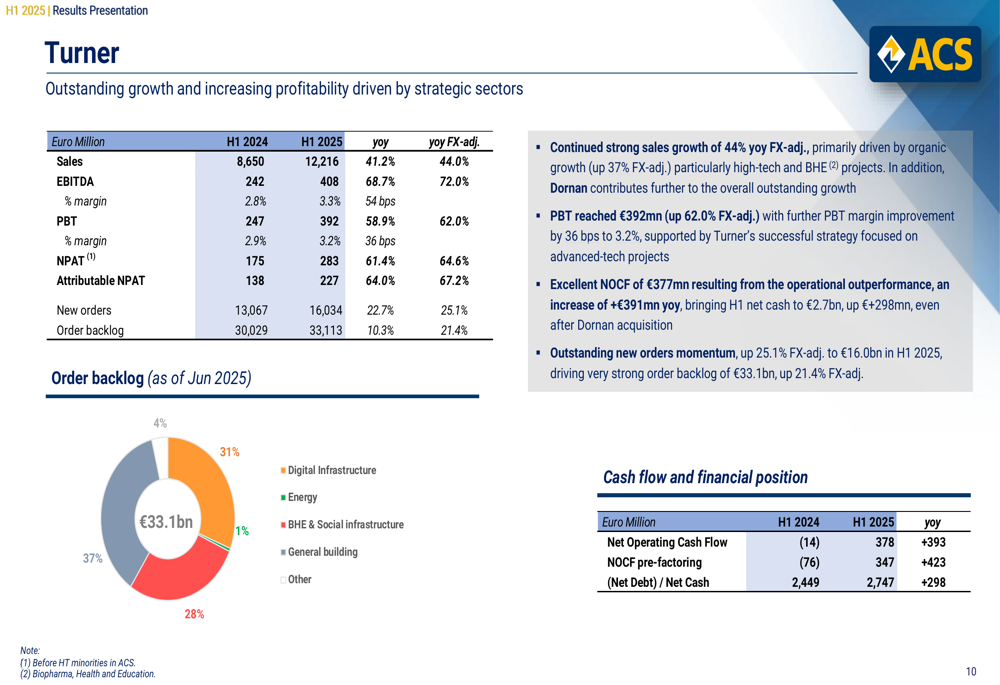

Turner emerged as the standout performer within ACS Group, with attributable net profit surging 64.0% (67.2% FX-adjusted) to €227 million. Sales increased by an impressive 41.2% to €12.2 billion, driven by significant growth in digital infrastructure projects, particularly data centers.

The following breakdown shows Turner’s exceptional performance metrics:

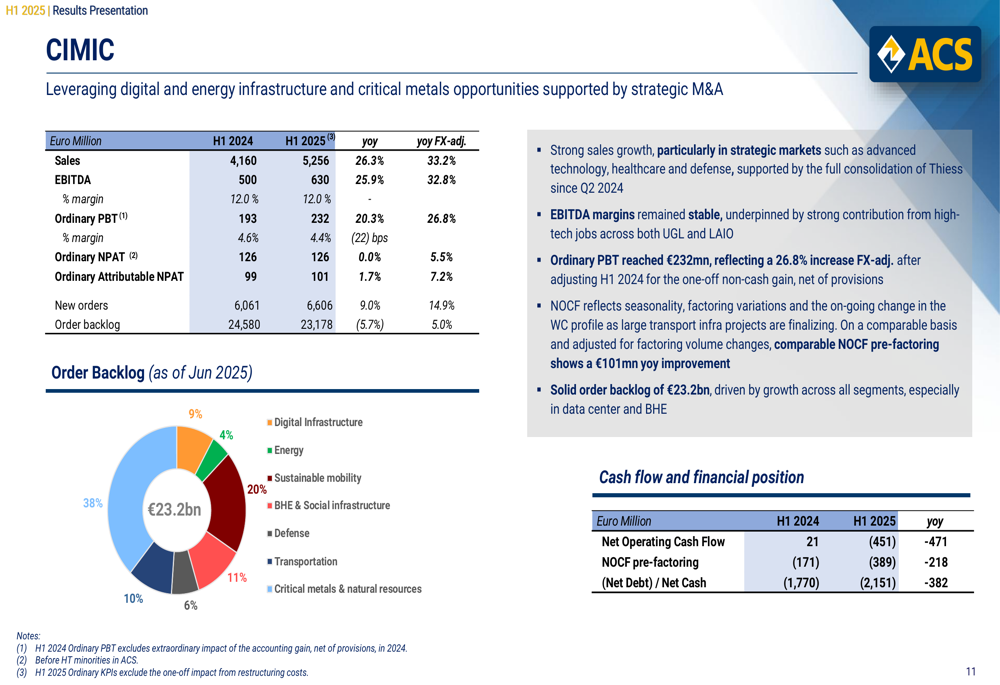

CIMIC, the group’s Australian subsidiary, delivered more modest growth with attributable net profit increasing by 1.7% (7.2% FX-adjusted) to €101 million. Sales grew by 26.3% to €5.3 billion, with a diverse order backlog across multiple sectors.

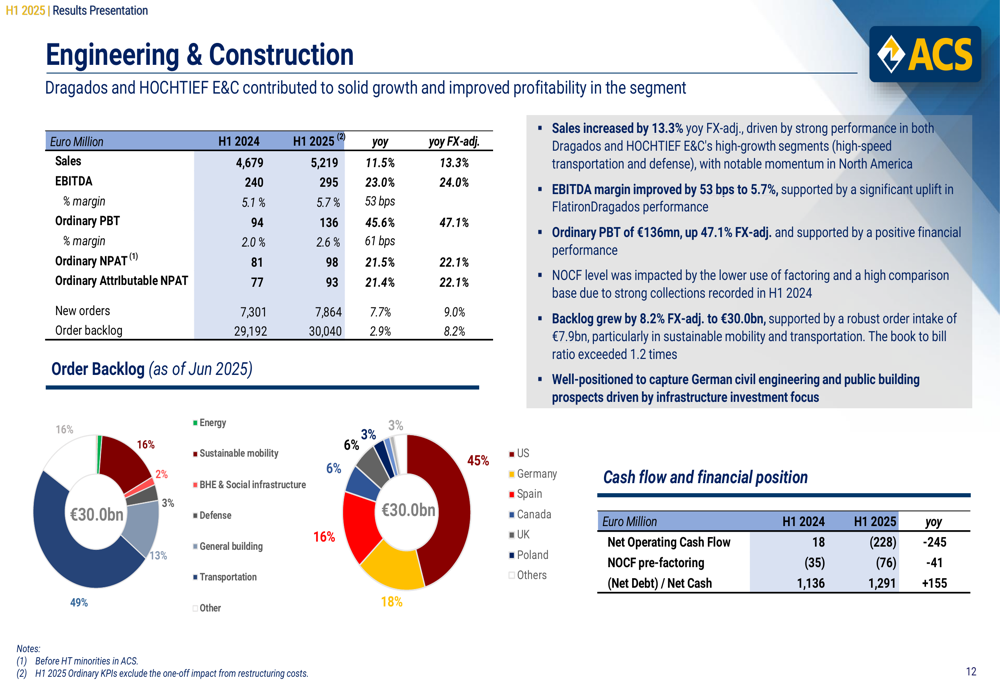

The Engineering & Construction segment also performed well, with attributable net profit rising 21.4% (22.1% FX-adjusted) to €93 million. Sales increased by 11.5% to €5.2 billion, with transportation projects accounting for nearly half of the segment’s order backlog.

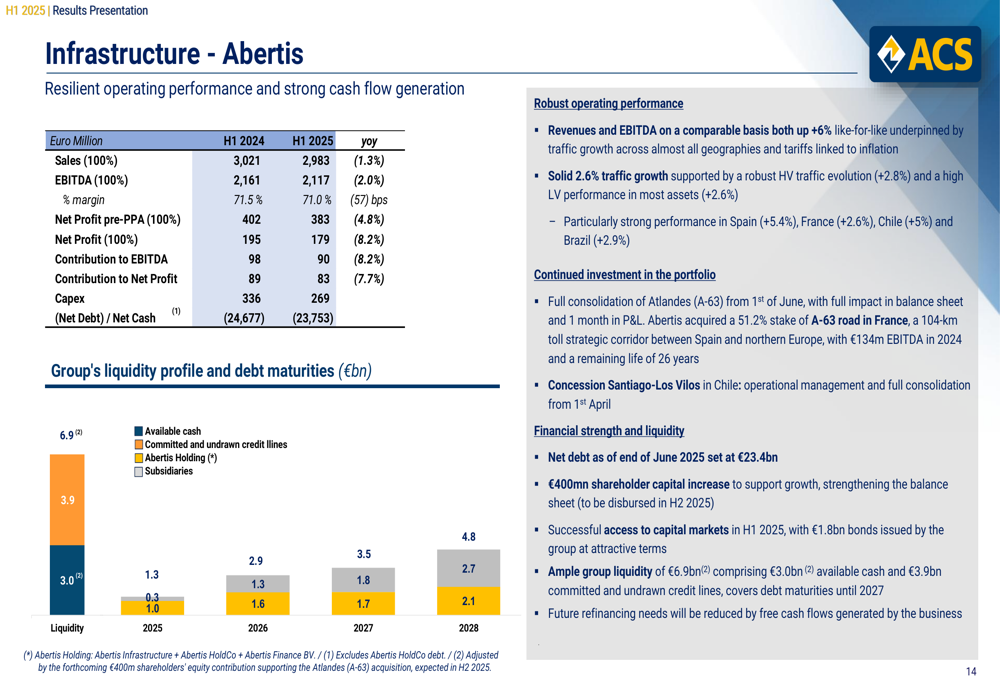

In contrast, the Infrastructure segment, which includes ACS’s stake in toll road operator Abertis, experienced a decline, with net profit decreasing by 7.1% (6.7% FX-adjusted). Abertis specifically saw an 8.2% decrease in sales and a 7.7% drop in net profit contribution, reflecting challenges in the toll road business.

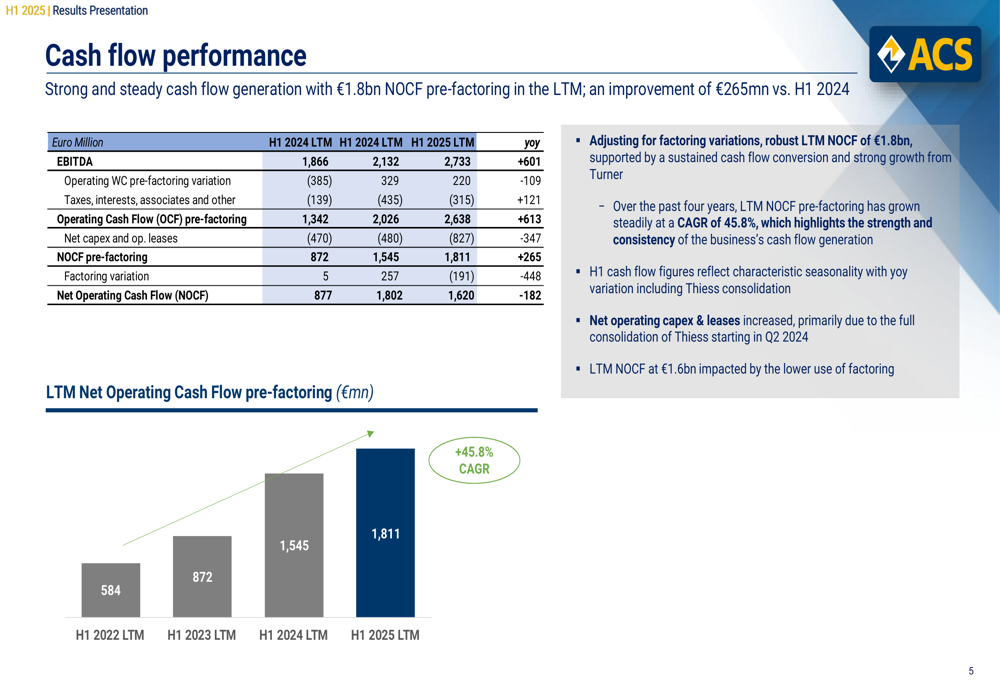

Cash Flow and Financial Position

ACS Group maintained strong cash flow generation, with LTM net operating cash flow pre-factoring increasing to €1.8 billion. The company has consistently improved its cash conversion, with a four-year CAGR of 45.8% in this metric.

The following chart illustrates the company’s cash flow performance:

The group ended H1 2025 with a net debt position of €2.2 billion, an increase of €0.6 billion year-over-year. This increase was primarily due to strategic capital allocation initiatives, including the €436 million acquisition of Dornan, €476 million in net equity investments (including €315 million in data centers), and €148 million in shareholder remuneration.

Strategic Initiatives

ACS Group’s order backlog reflects its strategic focus on diversification across sectors, with significant exposure to transportation (19%), general building (17%), digital infrastructure (14%), and social infrastructure (14%).

The composition of the order backlog demonstrates the company’s balanced approach to different market segments:

Digital infrastructure has emerged as a key growth driver for ACS, particularly through its Turner segment. The company has secured several significant new orders in this sector, including the CoreWeave Lancaster Data Center project worth $6 billion in Pennsylvania, USA.

ACS’s capital allocation priorities include significant greenfield infrastructure investment opportunities in data centers and managed lanes, strategic M&A in brownfield core infrastructure, and bolt-on acquisitions to enhance engineering capabilities. The company also remains committed to shareholder value creation through attractive remuneration while maintaining its BBB- investment grade rating.

Forward-Looking Statements

ACS Group has provided guidance for FY 2025, targeting ordinary net profit growth of up to 17%, which would result in a range of €746-800 million. This guidance is supported by the strong order backlog and continued focus on high-growth sectors.

The company’s strategic priorities and outlook are summarized in the following slide:

During the earnings call, CEO Juan Santamaría emphasized the company’s commitment to building a diversified business model and global footprint. He highlighted the "astronomical demand" in the digital infrastructure sector and identified semiconductors and batteries as key growth areas for the future.

Despite the positive outlook, ACS faces potential challenges including supply chain disruptions, market saturation in certain regions, macroeconomic pressures such as inflation and interest rate hikes, regulatory changes, and intense competition in the digital infrastructure and construction sectors.

Overall, ACS Group’s H1 2025 results demonstrate strong performance across most business segments, with its strategic focus on digital infrastructure and data centers driving significant growth, particularly in the Turner segment. The company’s robust order backlog and book-to-bill ratio provide a solid foundation for continued growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.