Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Adaptive Biotechnologies Corp (NASDAQ:ADPT) reported strong first-quarter 2025 results on May 1, showcasing significant revenue growth while substantially reducing operating expenses. The company’s shares responded positively in after-hours trading, climbing 7.34% to $7.90 following the earnings announcement.

The biotechnology firm, which specializes in immune-driven clinical diagnostics and drug discovery, demonstrated continued momentum in its Minimal Residual Disease (MRD) business segment while making progress toward operational efficiency and eventual profitability.

Quarterly Performance Highlights

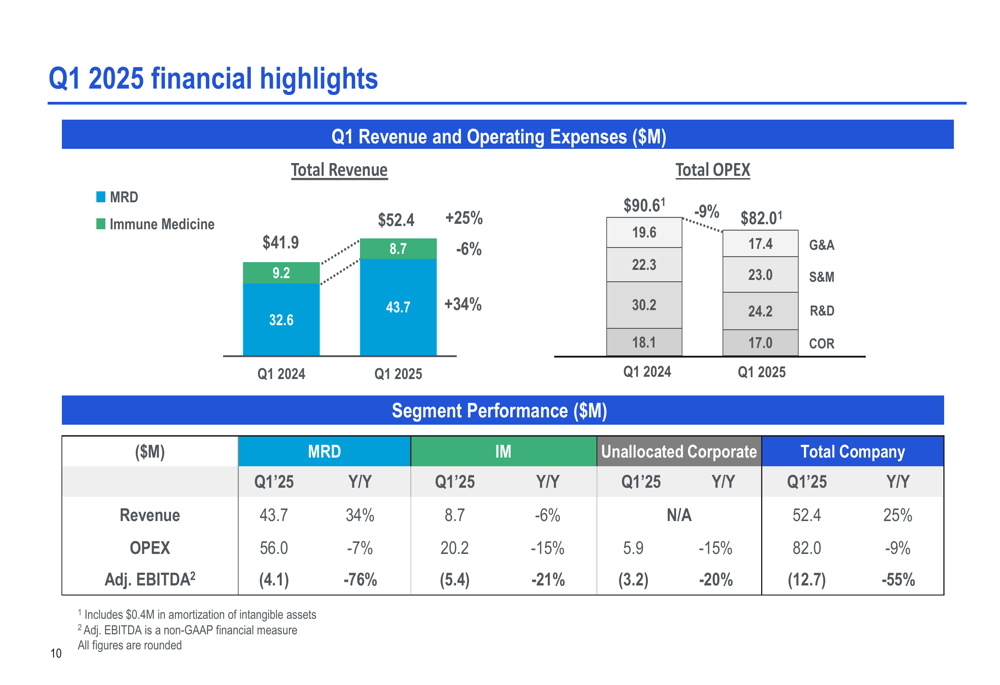

Adaptive reported total revenue of $52.4 million for Q1 2025, representing a 25% increase year-over-year. This growth was primarily driven by the company’s MRD segment, which generated $43.7 million in revenue, up 34% compared to the same period last year.

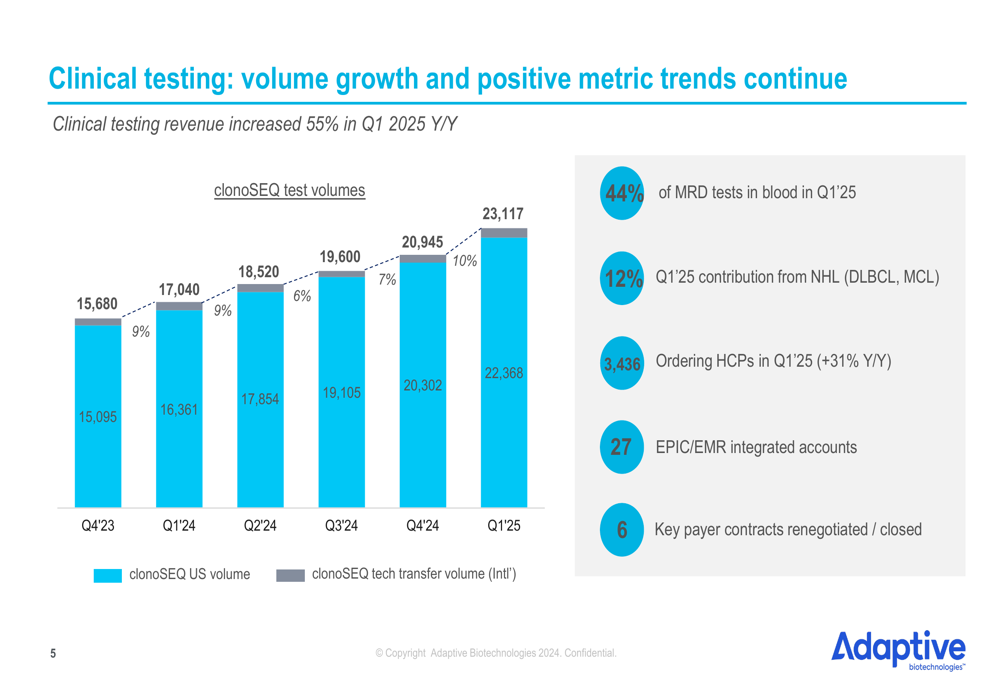

The company’s clinical testing volumes showed impressive growth, with 23,117 clonoSEQ tests performed in Q1 2025, compared to 17,040 tests in Q1 2024. This represents a substantial increase in adoption of the company’s MRD testing technology.

As shown in the following chart of quarterly testing volumes:

Clinical testing revenue increased 55% year-over-year, with several notable metrics highlighting the expanding reach of Adaptive’s testing platform:

- 44% of MRD tests were conducted using blood samples in Q1 2025

- 12% of Q1 2025 contribution came from non-Hodgkin lymphoma (NHL) indications

- The company expanded its healthcare provider network to 3,436 ordering HCPs, a 31% increase from the previous year

- 27 accounts now have EPIC/EMR integration, streamlining the ordering process

Detailed Financial Analysis

Adaptive made significant progress in improving its financial efficiency during the quarter. Total (EPA:TTEF) operating expenses decreased by 9% year-over-year to $82.0 million, demonstrating the company’s commitment to disciplined spending while maintaining growth.

The company’s gross margin improved to 68%, with sequencing gross margin reaching 62%, representing a substantial 17 percentage point improvement compared to the same period last year. This margin expansion reflects increasing operational efficiency and scale benefits.

The following financial highlights chart illustrates the company’s revenue growth and expense reduction:

Adaptive’s cash position remained strong at approximately $233 million as of March 31, 2025. The company significantly reduced its cash burn to approximately $23 million in Q1 2025, a 38% reduction compared to Q1 2024. This improvement in cash efficiency positions the company well for sustainable growth.

The company’s adjusted EBITDA loss narrowed to $12.7 million, a 55% improvement from the $28.2 million loss reported in Q1 2024. This trend indicates Adaptive is making substantial progress toward profitability, with management confirming they are on track to reach positive adjusted EBITDA in the second half of 2025.

Strategic Initiatives

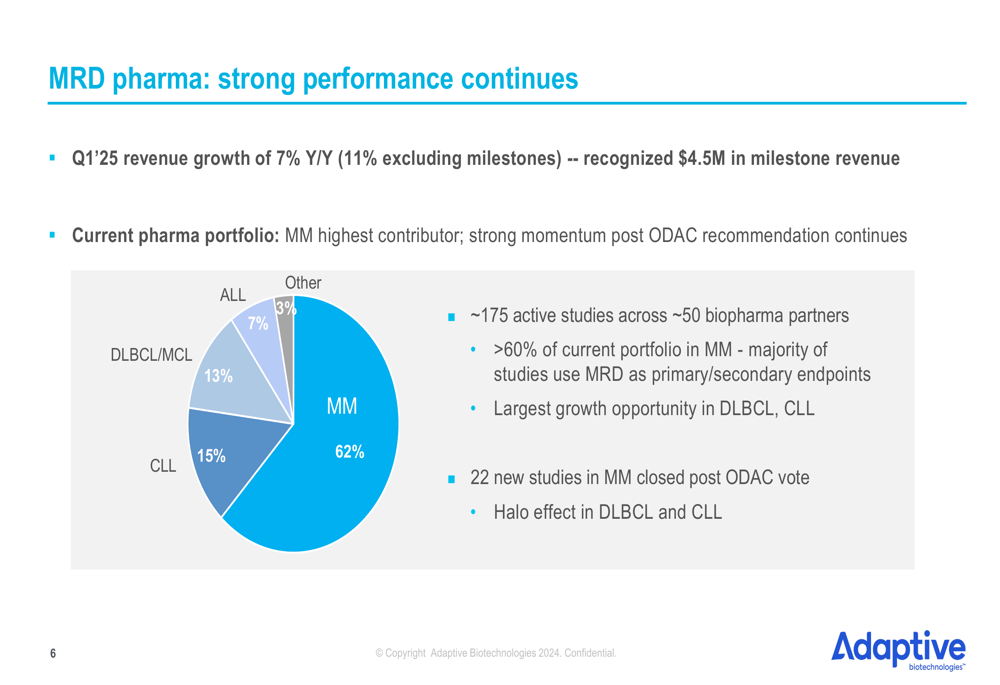

Adaptive’s MRD pharmaceutical business continues to be a significant growth driver, with revenue increasing 7% year-over-year (11% excluding milestones). The company recognized $4.5 million in milestone revenue during the quarter.

The company’s pharmaceutical portfolio is heavily weighted toward multiple myeloma (MM), which represents 62% of current studies. This strategic focus appears to be paying dividends, particularly following a positive ODAC recommendation that has accelerated study adoption.

The following chart shows the breakdown of Adaptive’s pharmaceutical portfolio:

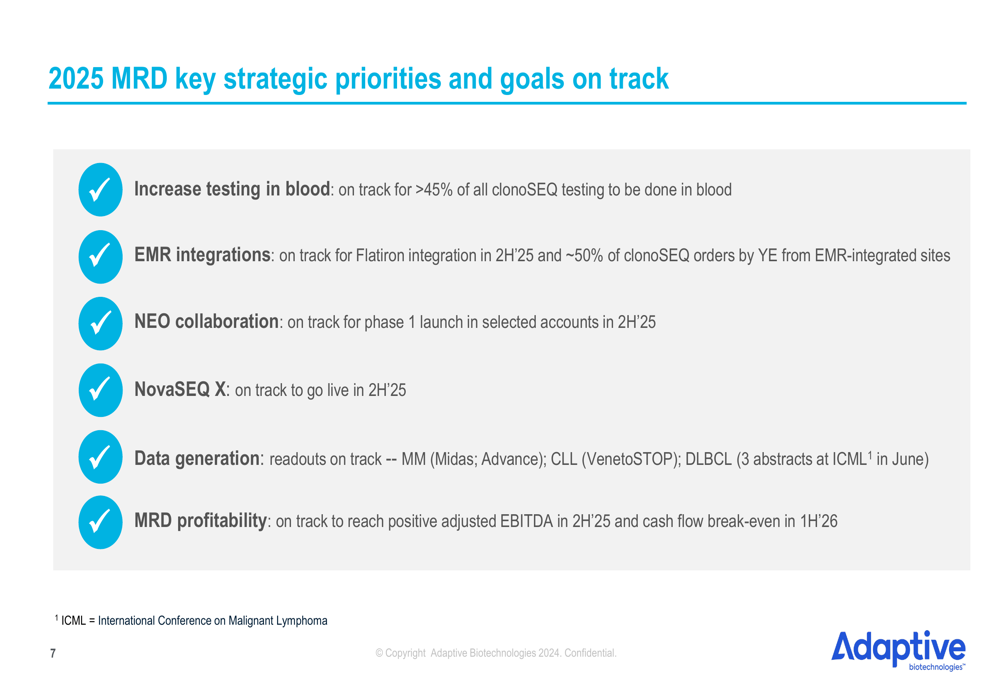

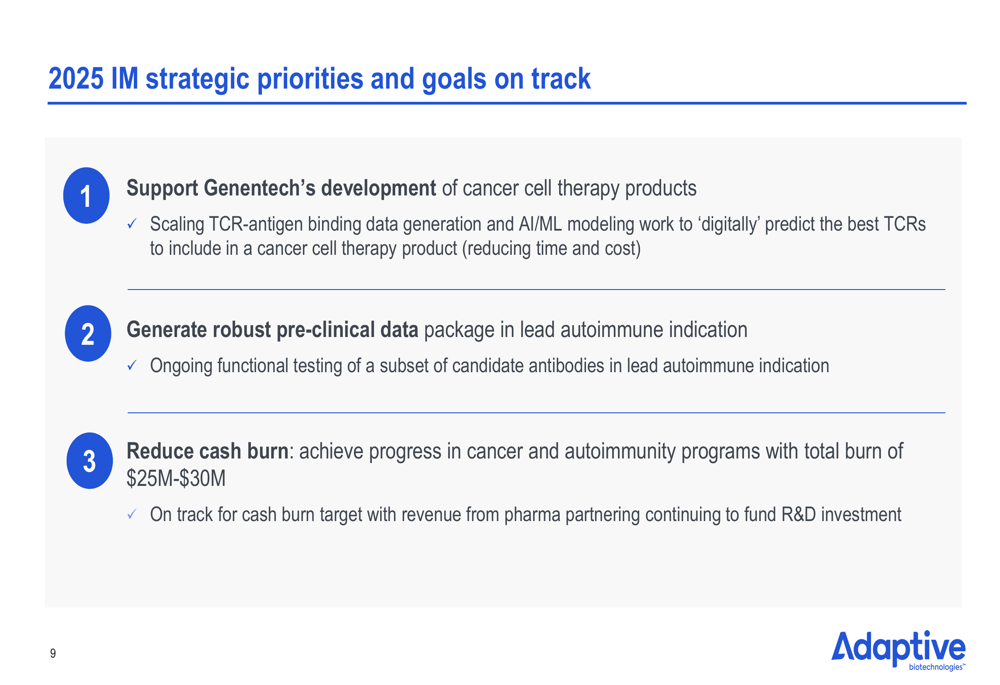

Adaptive outlined several key strategic priorities for 2025, all of which the company reports are on track:

In the Immune Medicine segment, Adaptive is advancing several initiatives while maintaining financial discipline:

Forward-Looking Statements

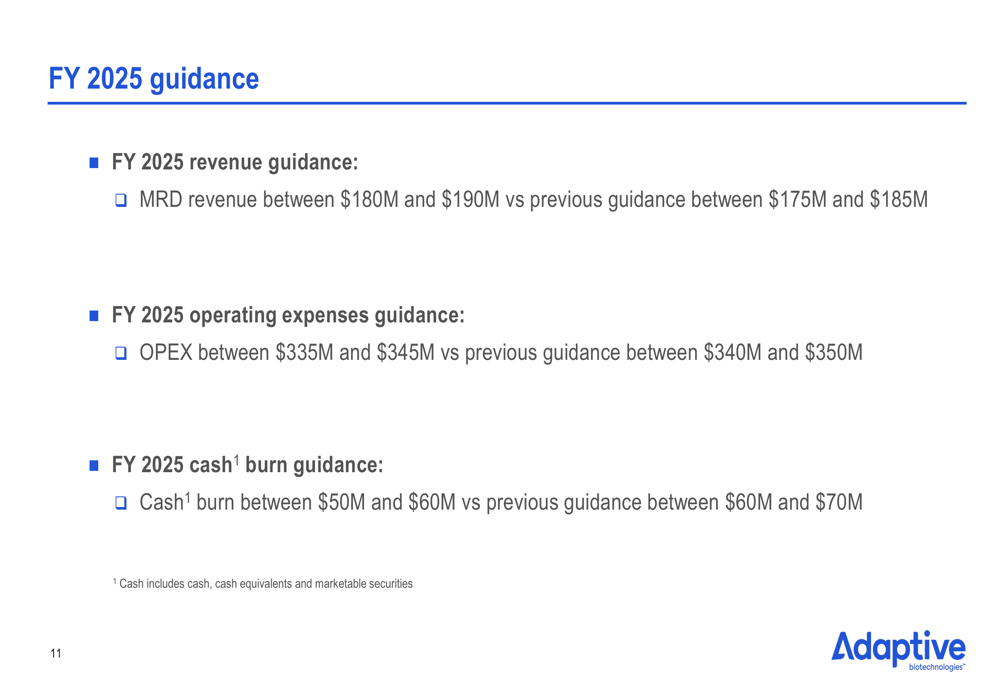

Based on strong Q1 performance, Adaptive raised its full-year 2025 guidance for MRD revenue to between $180 million and $190 million, up from the previous range of $175 million to $185 million. The company also lowered its operating expense guidance to between $335 million and $345 million, down from $340 million to $350 million previously.

Additionally, Adaptive reduced its expected cash burn for the full year to between $50 million and $60 million, compared to the previous guidance of $60 million to $70 million. This improved outlook reflects the company’s confidence in continued revenue growth and operational efficiency.

The updated guidance is summarized in the following slide:

Adaptive remains focused on achieving positive adjusted EBITDA in the second half of 2025 and reaching cash flow break-even in the first half of 2026. These milestones would represent significant achievements in the company’s path to sustainable profitability.

The company’s strategic investments in blood-based testing, EMR integrations, and technology upgrades position Adaptive for continued growth in both clinical and pharmaceutical markets. With expanded coverage for mantle cell lymphoma recurrence monitoring and ongoing development of its autoimmune program, Adaptive is diversifying its revenue streams while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.