Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Advanced Drainage Systems (NYSE:WMS) presented its first quarter fiscal 2026 financial results on August 7, 2025, revealing mixed performance across its business segments. The water management solutions provider reported modest overall growth while navigating challenging conditions in some markets. The company’s stock closed at $113.91 on August 6, down 2.72% ahead of the earnings presentation, and has declined significantly from its 52-week high of $166.03.

The presentation comes after ADS missed expectations in its Q4 2025 results, which had triggered a 6.35% stock price drop. Against this backdrop, the company’s Q1 performance demonstrates resilience in certain segments while continuing to face headwinds in others.

Quarterly Performance Highlights

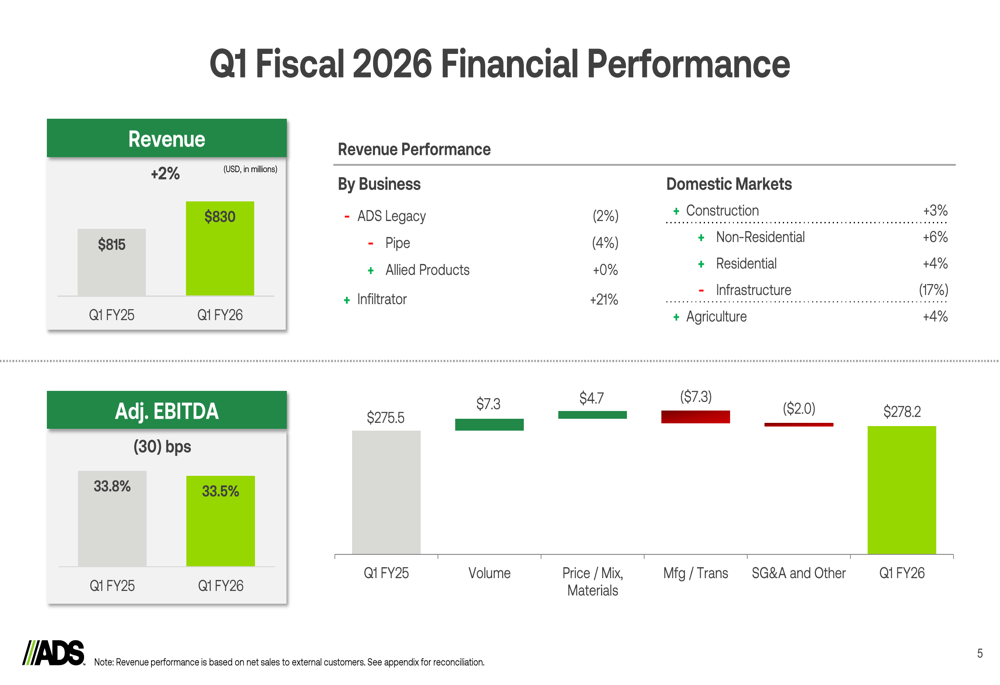

ADS reported Q1 fiscal 2026 revenue of $830 million, representing a 1.8% increase from $815 million in the same period last year. This growth was driven primarily by the company’s Infiltrator segment, which saw an impressive 21% year-over-year increase. However, this strength was partially offset by declines in other areas, with the ADS Legacy business decreasing by 2% and Pipe products falling by 4%.

As shown in the following chart of Q1 financial performance:

Performance across domestic markets varied significantly. Non-residential construction showed solid growth at 6%, while residential construction increased by 4% and agriculture grew by 4%. The infrastructure segment, however, experienced a substantial 17% decline, highlighting the uneven nature of the recovery across ADS’s various end markets.

The company’s adjusted EBITDA margin was 33.5% in Q1 FY26, slightly down from 33.8% in Q1 FY25. Management noted that favorable volume, price/cost dynamics, and transportation costs were offset by unfavorable manufacturing costs during the quarter.

Detailed Financial Analysis

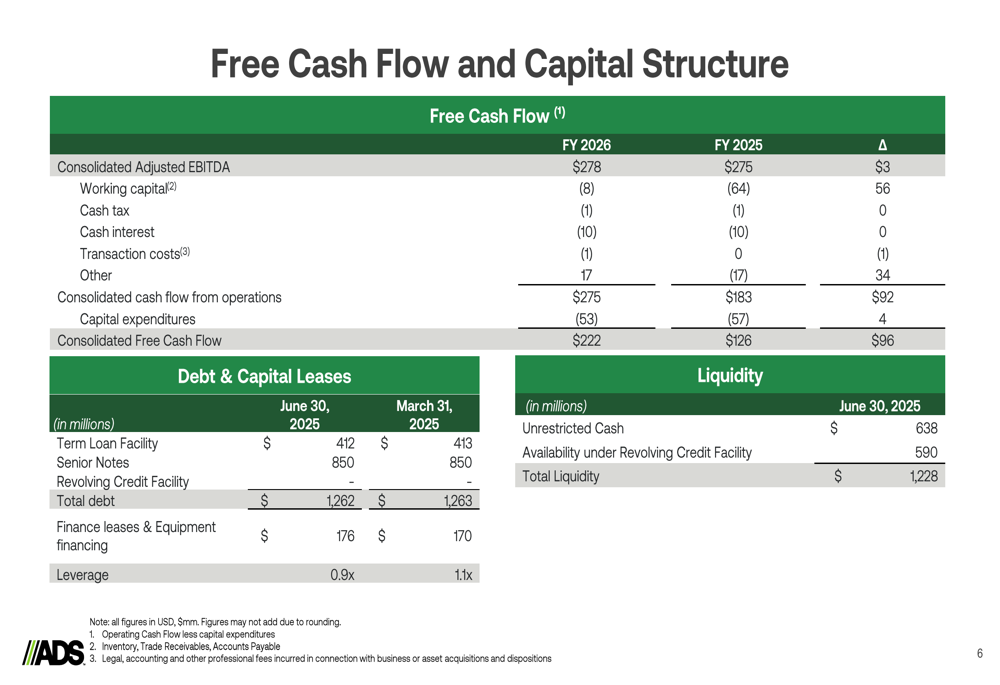

ADS maintained a strong financial position in Q1, reporting free cash flow of $278 million compared to $275 million in the prior year period. The company’s balance sheet remains robust with total liquidity of $1,228 million and a leverage ratio of just 0.9x, providing significant financial flexibility for future investments and capital allocation.

The following slide illustrates the company’s free cash flow and capital structure:

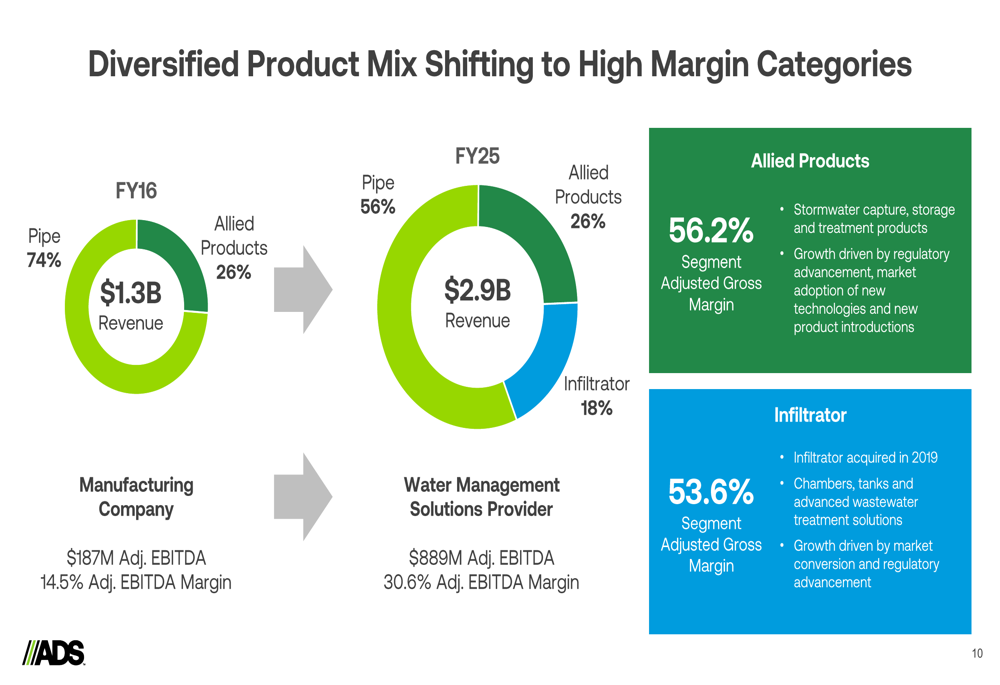

The company’s evolving product mix continues to support its margin profile. Over the past decade, ADS has successfully diversified its revenue streams, reducing its reliance on pipe products from 74% of revenue in FY16 to 56% in FY25. Meanwhile, higher-margin segments now represent a larger portion of the business, with Allied Products (56.2% gross margin) accounting for 26% of revenue and Infiltrator (53.6% gross margin) comprising 18%.

This strategic shift in product mix is clearly illustrated in the following slide:

Strategic Initiatives

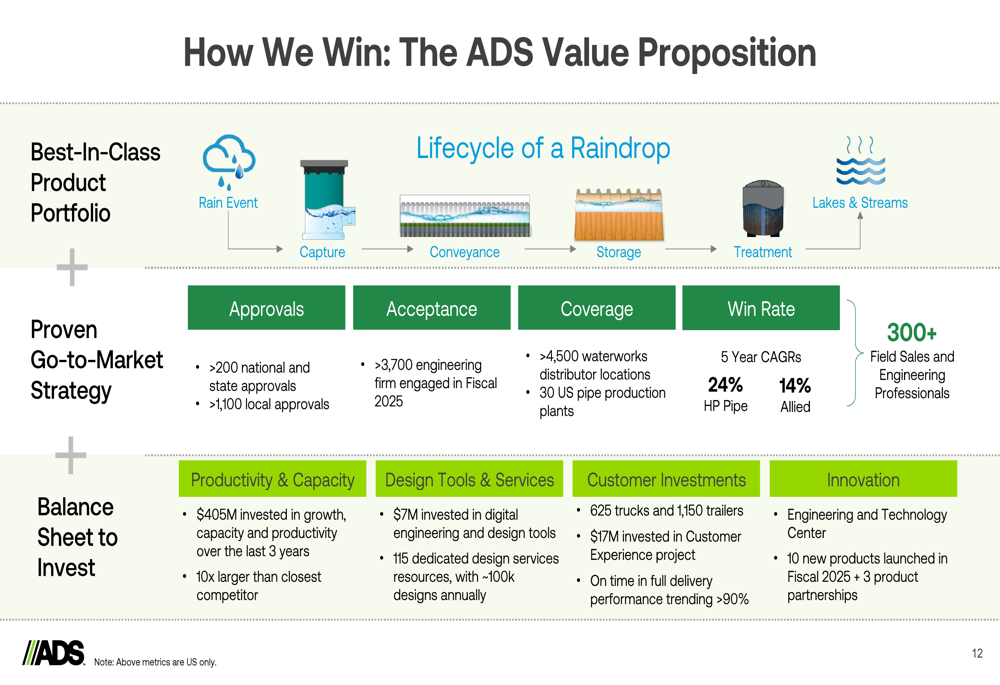

ADS continues to position itself as a comprehensive water management solutions provider rather than simply a pipe manufacturer. The company highlighted its best-in-class product portfolio, proven go-to-market strategy, and strong balance sheet as key competitive advantages.

The company’s value proposition is built on several pillars, including more than 200 national and state approvals, relationships with over 3,700 engineering firms, and distribution through more than 4,500 waterworks locations. ADS has invested $405 million in growth, capacity, and productivity initiatives, along with $7 million in digital engineering and design tools.

The following slide details the company’s value proposition:

During the quarter, ADS completed the acquisition of River Valley Pipe, further strengthening its market position. The company also introduced the Arcadia Hydrodynamic Separator, expanding its product portfolio in the stormwater management space.

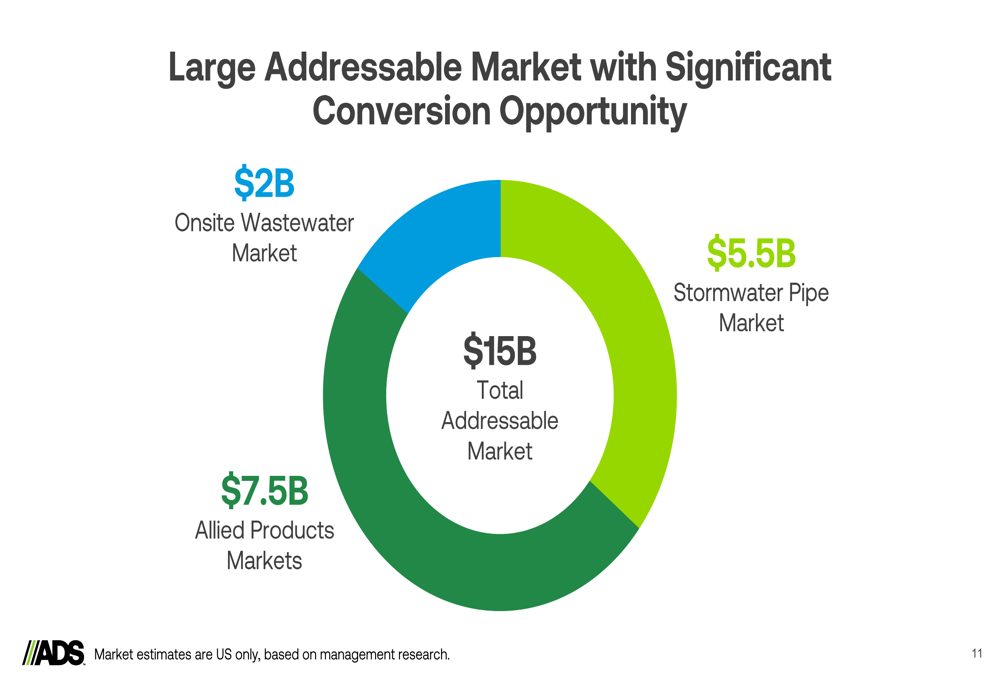

ADS operates in a large addressable market totaling approximately $15 billion, broken down into Onsite Wastewater ($2 billion), Stormwater Pipe ($5.5 billion), and Allied Products ($7.5 billion). This substantial market opportunity provides significant runway for continued growth.

As shown in the following market size breakdown:

Forward-Looking Statements

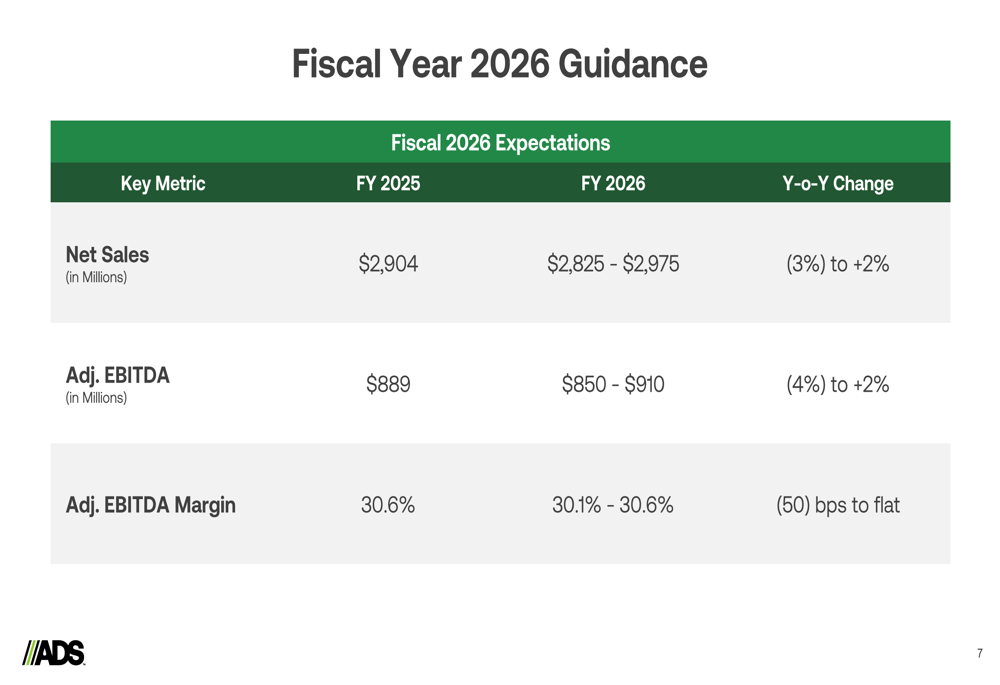

For fiscal year 2026, ADS provided guidance that reflects cautious optimism amid economic uncertainty. The company expects net sales between $2,825 million and $2,975 million, representing a range from a 3% decrease to a 2% increase compared to FY25. Adjusted EBITDA is projected to be between $850 million and $910 million, with adjusted EBITDA margin between 30.1% and 30.6%.

The following slide details the company’s fiscal 2026 guidance:

This guidance aligns with management’s previous commentary from the Q4 earnings call, where they noted expectations for volume growth in the low single digits offset by slight pricing declines. The company anticipates challenges in non-residential and residential markets, with international markets expected to decline in double digits.

Despite these headwinds, ADS’s diversified product mix, strong balance sheet, and strategic investments position the company to navigate the current economic environment while continuing to execute on its long-term strategy of expanding beyond traditional pipe manufacturing into comprehensive water management solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.