BofA update shows where active managers are putting money

Introduction & Market Context

Advantage Solutions Inc (NASDAQ:ADV) reported a challenging first quarter of 2025, with both revenue and adjusted EBITDA declining year-over-year amid macroeconomic pressures and ongoing transformation investments. The company’s stock, which has faced significant pressure over the past six months, was trading at $1.47 as of the May 12, 2025 earnings announcement, representing a substantial decline from earlier in the year.

The consumer products and retail services provider faced a combination of tariff concerns, labor market challenges, and retail inventory destocking that collectively weighed on performance across its business segments. Despite these headwinds, management emphasized the company’s continued progress on transformation initiatives designed to drive long-term growth.

Quarterly Performance Highlights

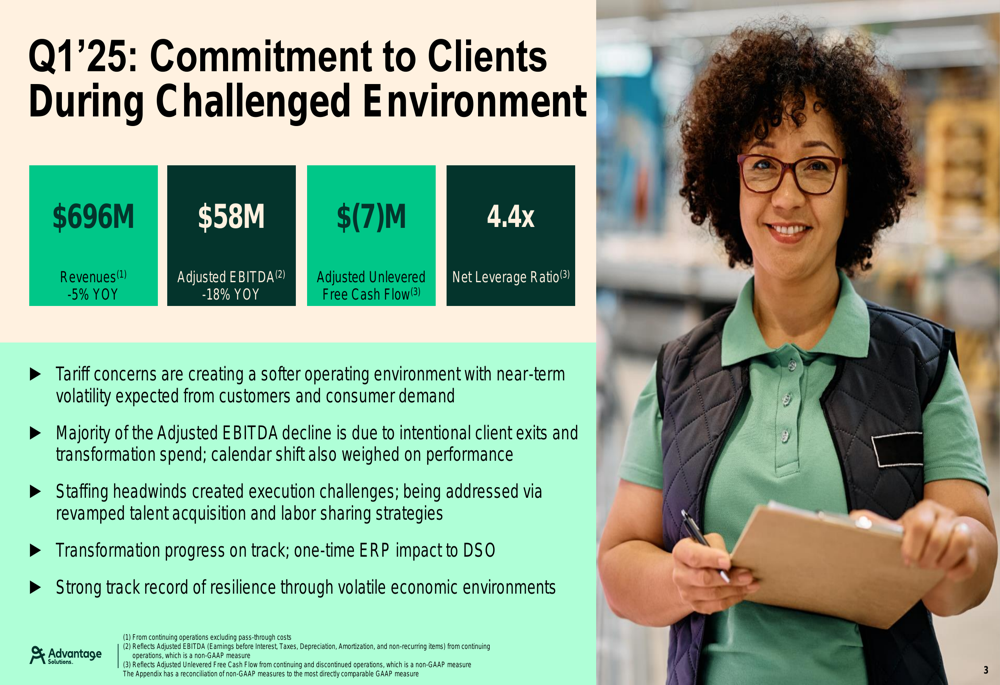

Advantage Solutions reported Q1’25 revenues of $696 million, representing a 5% year-over-year decline, while adjusted EBITDA fell 18% to $58 million. The company also reported negative adjusted unlevered free cash flow of $7 million, though management expects cash flow to improve as the year progresses.

As shown in the following comprehensive performance overview:

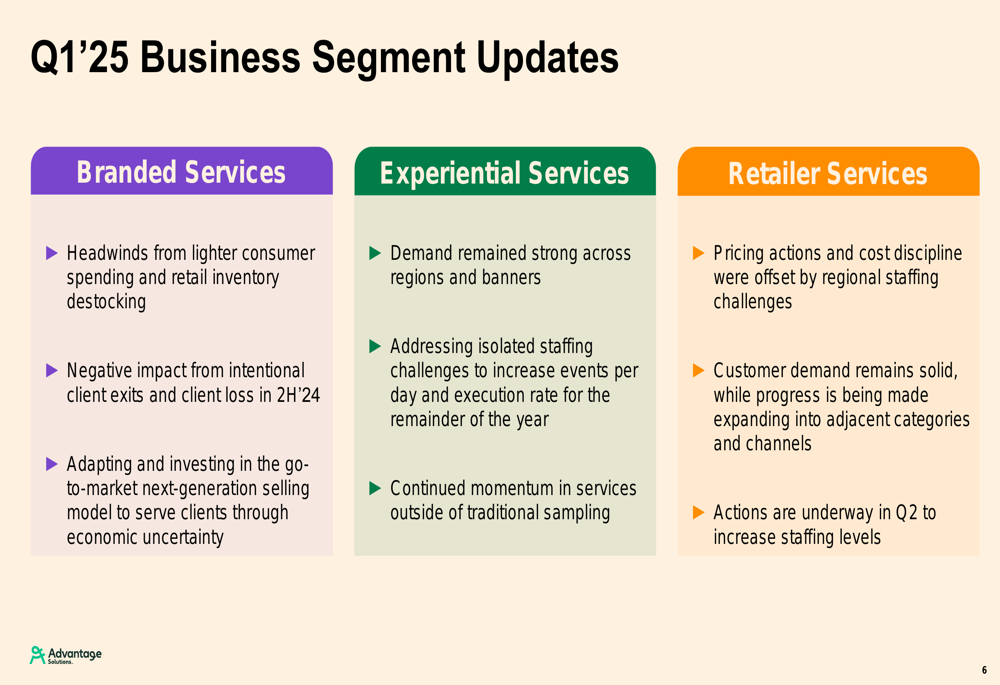

Breaking down performance by segment, all three of the company’s business units faced challenges during the quarter:

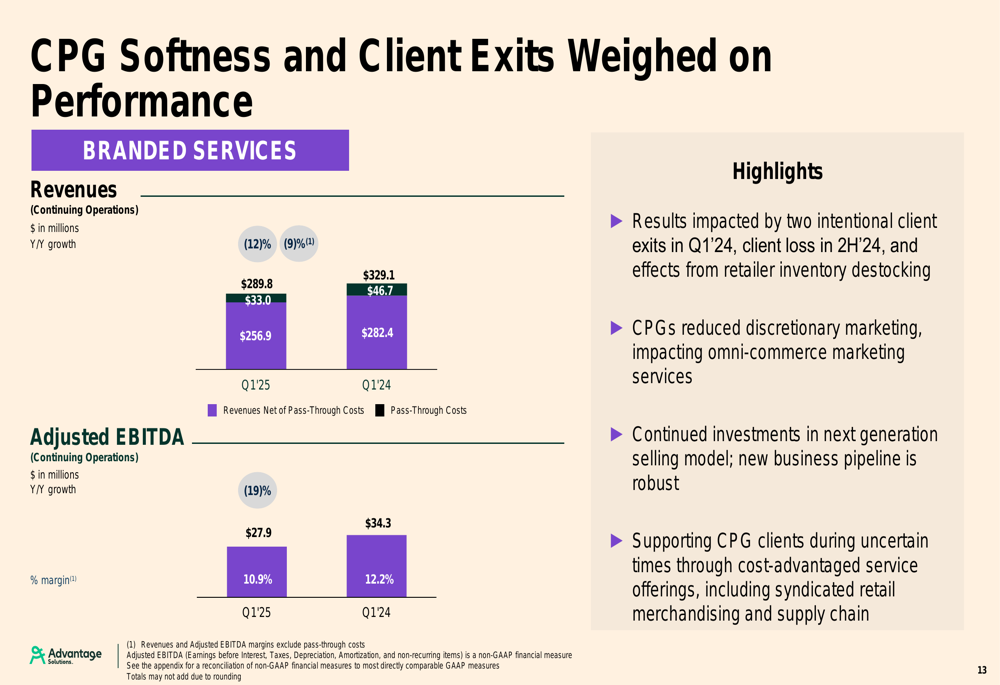

Branded Services

The Branded Services segment, which includes the company’s sales and marketing services for consumer packaged goods manufacturers, was particularly hard hit with a 12% revenue decline to $256.9 million and a 19% drop in adjusted EBITDA to $27.9 million. Management attributed this performance to intentional client exits, a client loss in the second half of 2024, and the effects of retailer inventory destocking.

The following chart illustrates the segment’s performance:

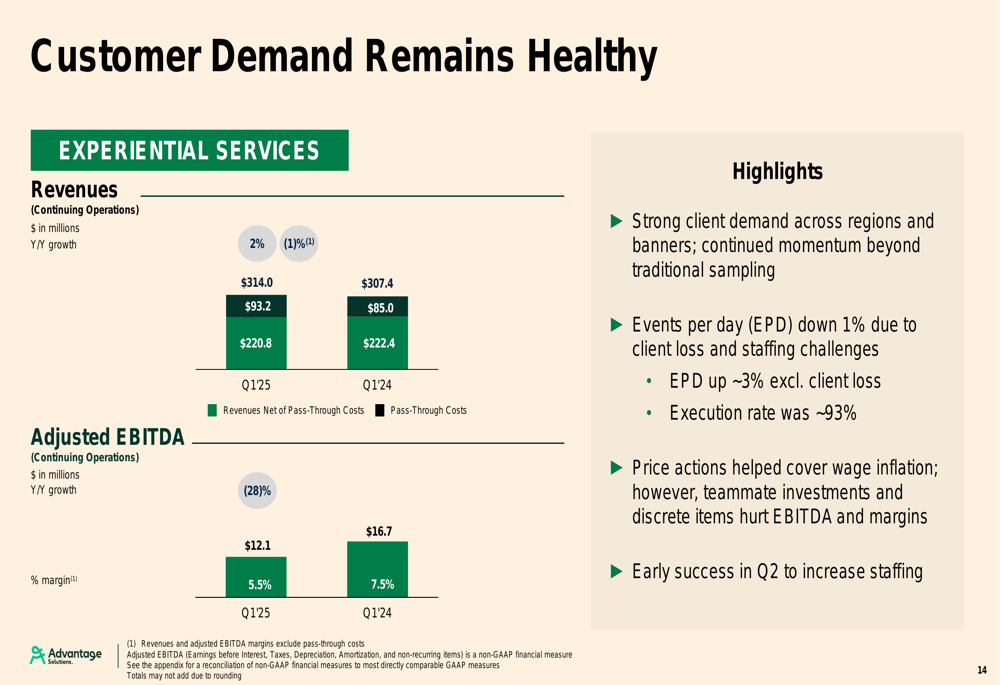

Experiential Services

The Experiential Services segment showed mixed results, with revenue growing 2% year-over-year to $220.8 million, but adjusted EBITDA declining significantly by 28% to $12.1 million. While customer demand remained strong across regions and banners, staffing challenges impacted events per day and execution rates, which fell to approximately 93%. The company noted early success in Q2 to increase staffing levels.

The segment’s performance is detailed in the following chart:

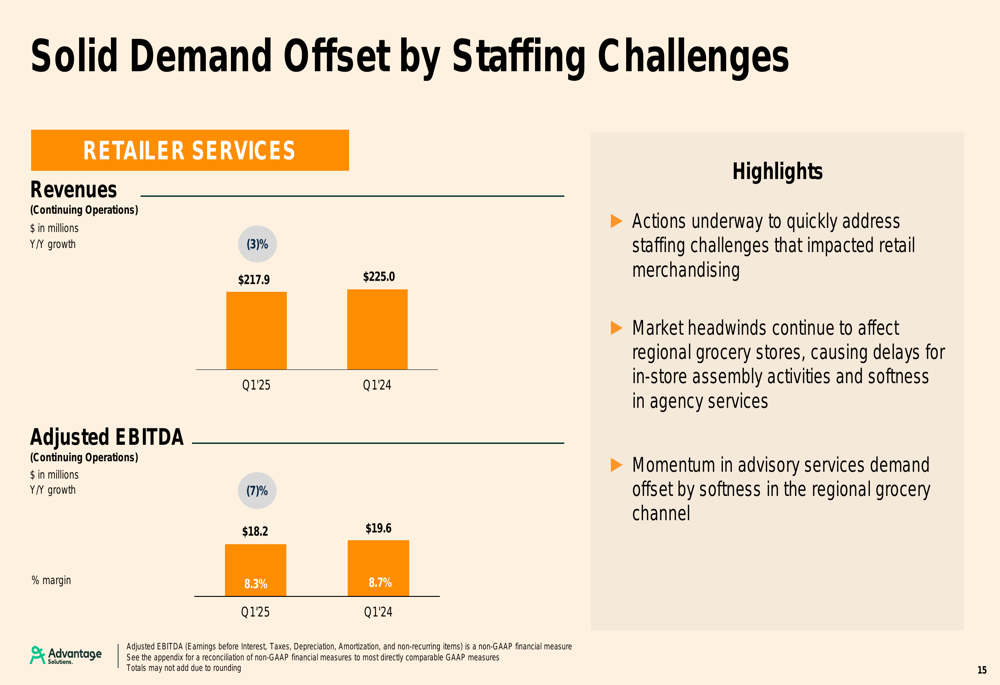

Retailer Services

The Retailer Services segment, which provides merchandising and other in-store services, saw revenue decline 3% to $217.9 million and adjusted EBITDA fall 7% to $18.2 million. The company cited staffing challenges that impacted retail merchandising execution, along with market headwinds affecting regional grocery stores.

The segment’s results are illustrated below:

Market Challenges

Advantage Solutions highlighted several external factors impacting its business environment. Tariff concerns are creating uncertainty in the consumer products industry, though the company noted it is largely a domestic services business without direct manufacturing exposure. Management indicated they are proactively implementing cost reduction programs to mitigate potential impacts.

Labor market challenges represented another significant headwind, with tight labor markets creating staffing difficulties across the business. The company specifically mentioned intentional turnover and attrition in its talent acquisition team, with remedies initiated in Q2.

The company’s business segment updates provided additional context on these challenges:

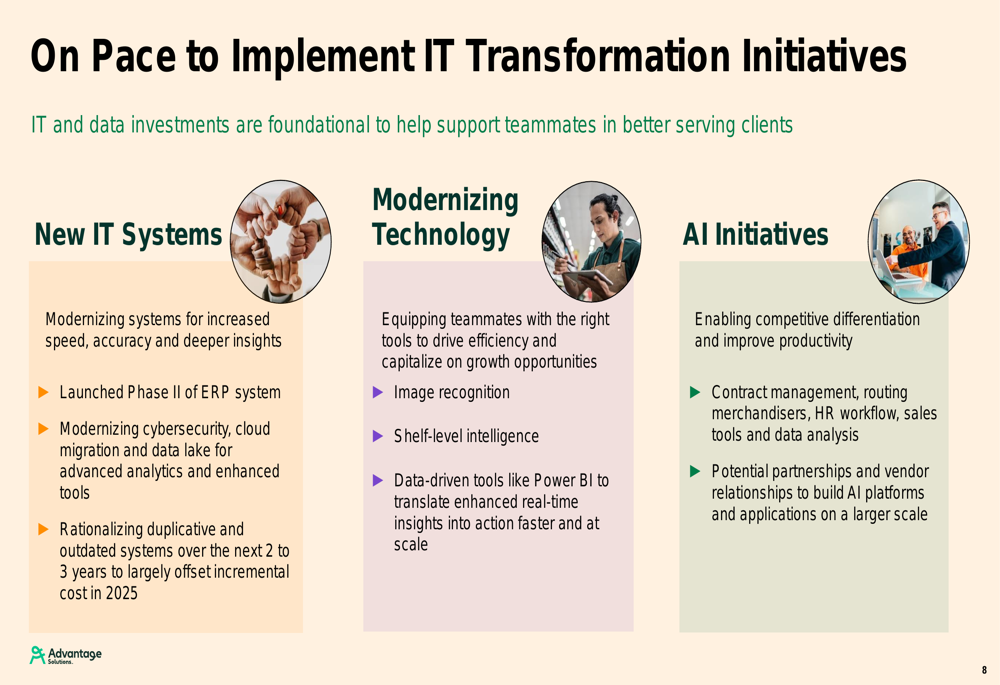

Transformation Initiatives

Despite the challenging environment, Advantage Solutions continues to advance its transformation strategy centered around three core principles: Simplify, Transform, and Accelerate. A key component of this strategy is the company’s IT transformation initiative, which involves modernizing systems, equipping teammates with better tools, and implementing AI initiatives to drive efficiency.

The following slide outlines the company’s IT transformation plans:

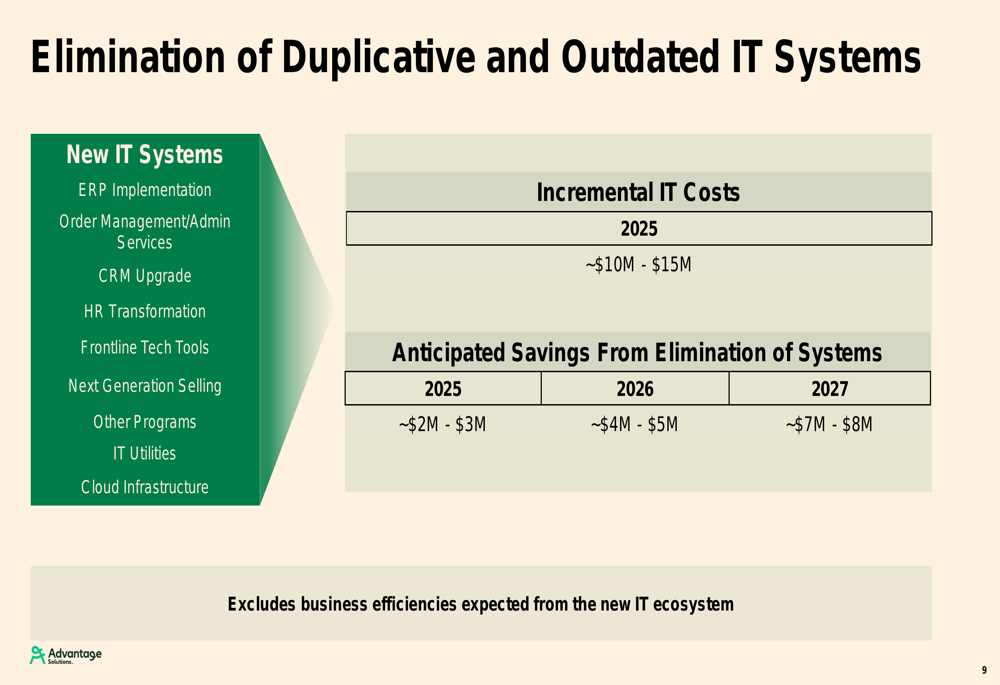

The company provided specific financial projections related to its IT transformation, noting incremental IT costs of approximately $10-15 million in 2025, with anticipated savings growing from $2-3 million in 2025 to $7-8 million by 2027. These figures exclude additional business efficiencies expected from the new IT ecosystem.

Advantage is also advancing workforce optimization strategies aimed at enhancing how it assigns and deploys talent across more than 85,000 retail stores. The company expressed confidence in achieving a 30%+ uplift in availability of hours for relevant teammates through these initiatives.

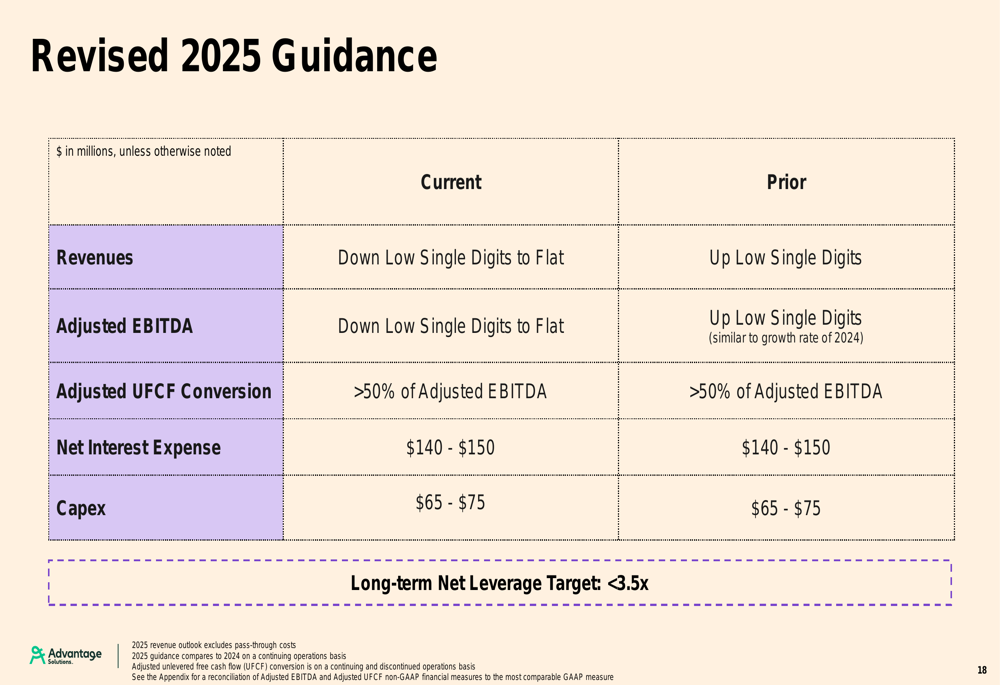

Revised Outlook

In response to the challenging operating environment, Advantage Solutions has revised its 2025 guidance downward. The company now expects both revenues and adjusted EBITDA to range from down low single digits to flat compared to the prior year, a significant reduction from previous guidance of low single-digit growth.

The revised guidance is detailed in the following comparison:

This downward revision represents a notable shift from the company’s outlook following Q4 2024 results, when it had targeted low single-digit growth in both revenue and adjusted EBITDA for 2025. Management cited the softer environment in the broader consumer market as the primary driver for the revised outlook, while emphasizing confidence in the company’s people and investments to enhance capabilities for high-quality client service.

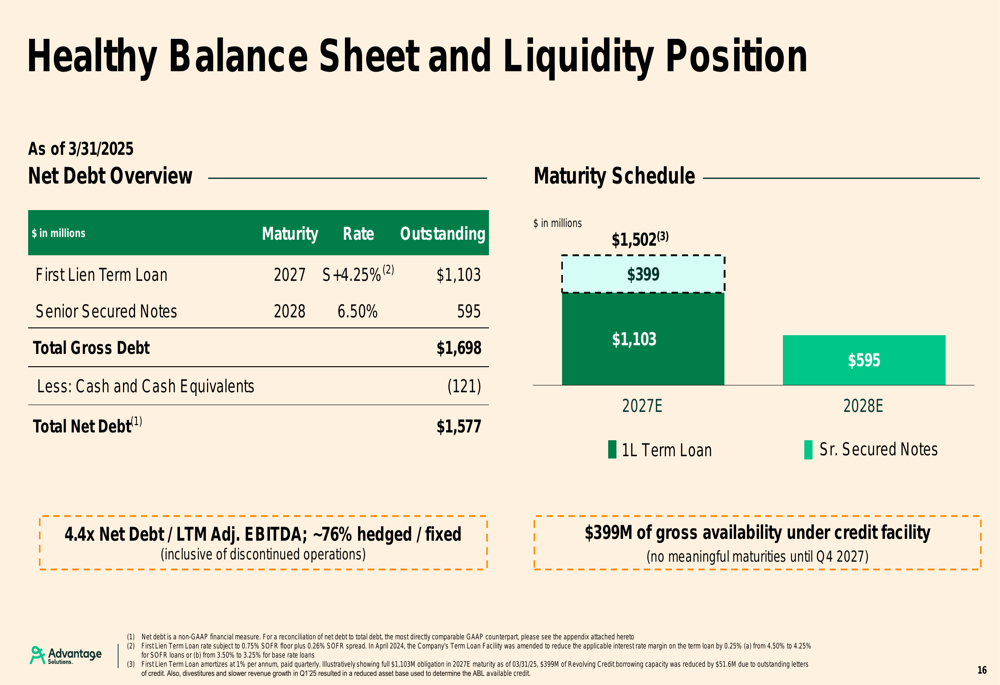

Financial Position

As of March 31, 2025, Advantage Solutions maintained a net debt position of $1.577 billion, with a net leverage ratio of 4.4x LTM adjusted EBITDA. The company reported $121 million in cash and cash equivalents and $399 million of gross availability under its credit facility.

The company’s debt maturity schedule and key balance sheet metrics are illustrated below:

During the quarter, the company allocated capital to debt reduction and share repurchases, including approximately $20 million in voluntary debt repurchases, $3 million in mandatory debt amortization, and $1 million spent on discretionary share buybacks (approximately 0.5 million shares). Management noted that current debt and equity trading levels present attractive value creation opportunities for excess cash.

Forward-Looking Statements

Looking ahead, Advantage Solutions expects cash flow to improve as the year progresses, with potential upside in delivering more than 50% of adjusted EBITDA as free cash flow due to improved working capital management. The company maintains its long-term net leverage target of less than 3.5x.

Management emphasized that the current transformation initiatives are positioning Advantage for long-term earnings power and cash generation, despite the near-term challenges. The company’s focus on modernizing technology, optimizing workforce deployment, and enhancing operational efficiency is expected to yield benefits as these initiatives mature over the coming years.

While the revised outlook reflects caution regarding the current market environment, the company’s continued investment in transformation initiatives signals confidence in its long-term strategic direction and ability to navigate through the current headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.