SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Advantage Solutions Inc (NASDAQ:ADV) presented its second quarter 2025 earnings results on August 7, showing signs of recovery from staffing challenges that plagued its first quarter while navigating a persistently soft consumer environment. The company reported modest revenue declines but highlighted sequential improvement and segment-specific growth.

The marketing services provider, which closed at $1.34 on August 6, continues to face headwinds in its Branded Services segment while seeing positive momentum in its Experiential and Retailer Services divisions. This mixed performance comes as the company implements transformation initiatives aimed at improving long-term earnings power and cash generation.

Quarterly Performance Highlights

Advantage Solutions reported Q2 2025 revenues of $736.2 million, representing a 2% year-over-year decline, while Adjusted EBITDA fell 4% to $86.4 million. Despite these declines, the results showed improvement compared to Q1 2025, when revenues dropped 5% and Adjusted EBITDA fell 18%.

The company generated $57 million in Adjusted Unlevered Free Cash Flow during the quarter, achieving a 66% cash conversion rate. Management highlighted the substantial progress made in resolving the staffing shortfall that impacted first quarter results.

As shown in the following performance summary:

Segment Performance Analysis

Advantage Solutions’ performance varied significantly across its three business segments, with Branded Services continuing to struggle while Experiential and Retailer Services showed improvement.

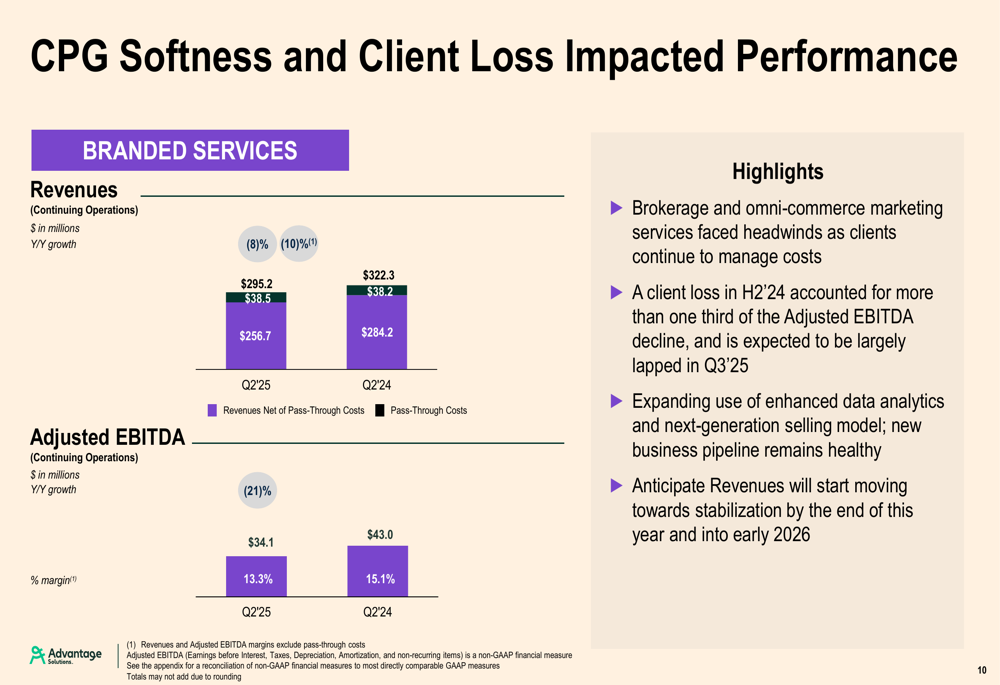

The Branded Services segment, which includes brokerage and omni-commerce marketing services, was most severely impacted by market headwinds and reduced client investments. Revenues declined 8% year-over-year to $256.7 million, while Adjusted EBITDA fell 21% to $34.1 million. Management noted that a client loss accounted for more than one-third of the Adjusted EBITDA decline but expects this impact to be largely lapped in Q3 2025.

As illustrated in the Branded Services performance chart:

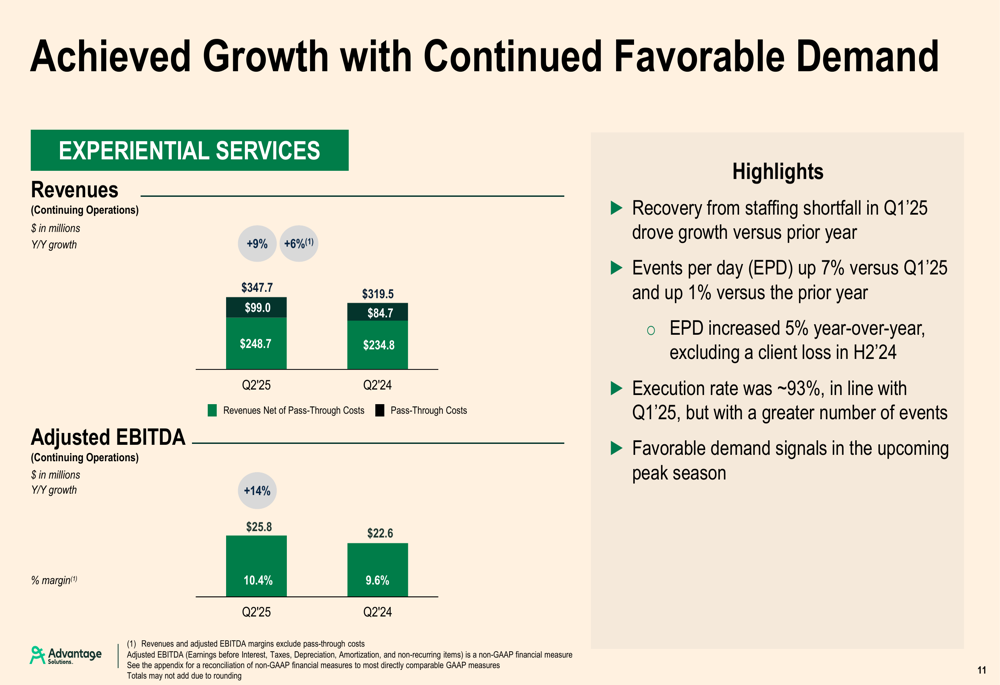

In contrast, the Experiential Services segment delivered strong results, with revenues increasing 6% year-over-year to $248.7 million and Adjusted EBITDA growing 14% to $25.8 million. This improvement was attributed to the recovery from staffing shortfalls experienced in Q1, with events per day growing 1% overall and 5% excluding a client loss. The segment achieved an execution rate of approximately 93%.

The Experiential Services segment performance is shown here:

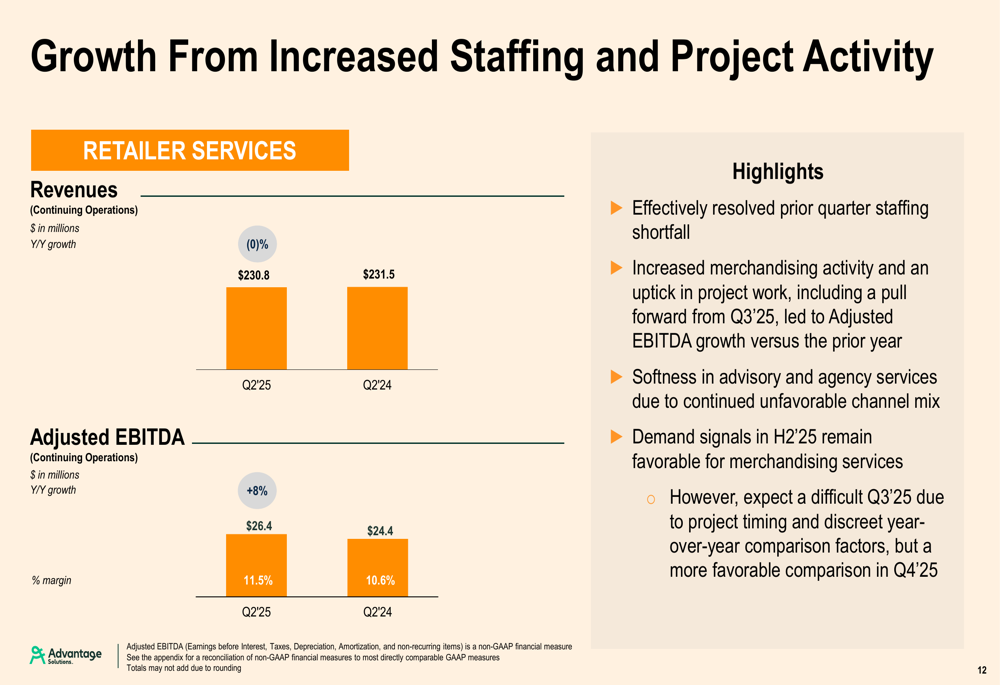

The Retailer Services segment also showed resilience, with revenues essentially flat year-over-year at $230.8 million but Adjusted EBITDA increasing 8% to $26.4 million. Similar to Experiential Services, this segment benefited from improved staffing levels compared to the previous quarter.

The following chart details the Retailer Services segment performance:

Balance Sheet and Cash Flow

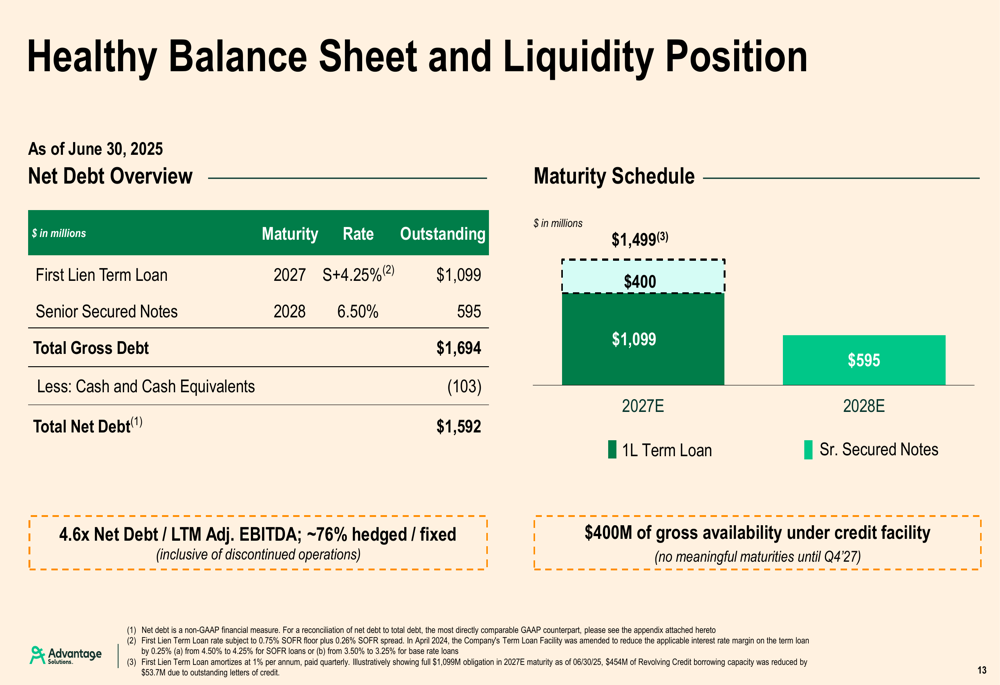

Advantage Solutions maintained a stable balance sheet with $103 million in cash as of June 30, 2025. The company’s net leverage ratio stood at 4.6x, slightly higher than the 4.4x reported at the end of Q1. Management reaffirmed its long-term net leverage target of less than 3.5x.

Total (EPA:TTEF) gross debt amounted to $1.69 billion, consisting of a $1.1 billion First Lien Term Loan due in 2027 and $595 million in Senior Secured Notes due in 2028. The company has approximately $400 million of gross availability under its credit facility.

The balance sheet structure is illustrated in the following slide:

Capital expenditures from continuing operations totaled approximately $2 million in Q2, significantly lower than the previous guidance range. The company has revised its full-year capex guidance downward to $50-60 million from the prior range of $65-75 million.

Management expects cash generation to improve in the second half of 2025, with Adjusted Free Cash Flow conversion projected to exceed 50% of Adjusted EBITDA. The company also noted that it received $22.5 million in proceeds on July 31 related to the first of two deferred purchase price installments for Jun Group.

Strategic Initiatives and Outlook

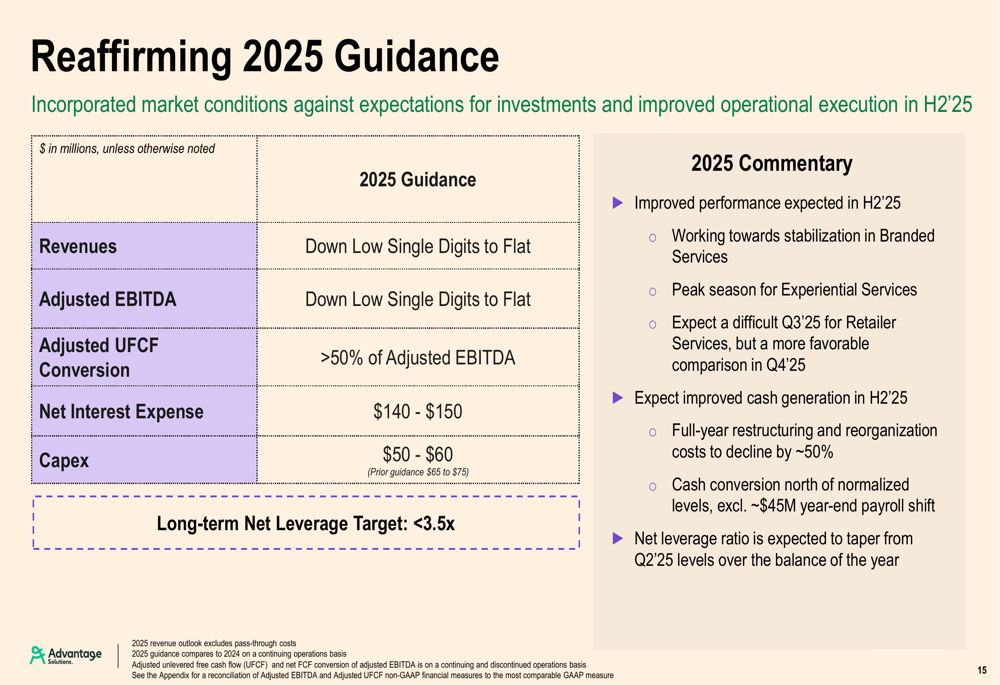

Advantage Solutions reaffirmed its 2025 guidance, projecting revenues and Adjusted EBITDA to be down low single digits to flat compared to the prior year. The company expects improved performance and cash generation in the second half of 2025.

The guidance details are shown in the following slide:

The company is advancing several strategic initiatives to drive long-term growth and operational efficiency. These include:

1. Establishing foundational IT systems by 2026, with a focus on modernizing technology and implementing AI initiatives for contract management, HR workflow, sales tools, and data analysis.

2. Optimizing workforce management across 85,000+ retail stores, with the goal of achieving a 30%+ uplift in the availability of hours for teammates.

3. Enhancing service offerings in areas such as branded and retailer merchandising, supply chain logistics, product sampling, and private brand development.

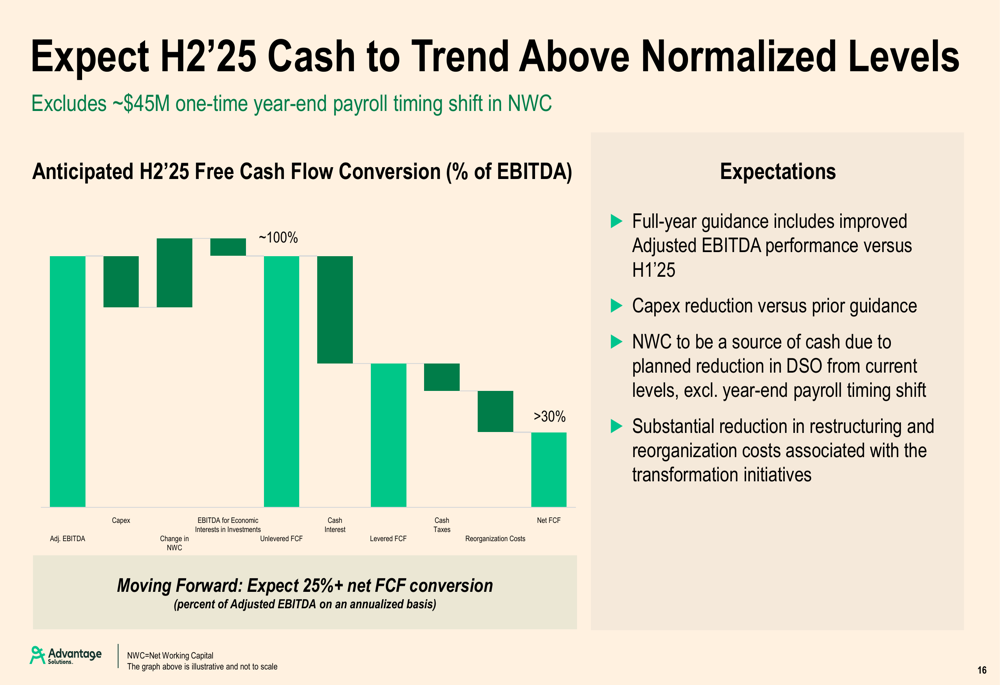

Management emphasized that these transformation initiatives are positioning the company well for long-term earnings power and cash generation, despite the current soft operating environment. The company expects cash flow conversion to normalize at 25%+ of Adjusted EBITDA going forward.

As illustrated in the expected cash flow conversion:

Advantage Solutions continues to navigate a challenging consumer market while implementing operational improvements that are beginning to show results in specific segments. While the Branded Services segment remains under pressure, the recovery in Experiential and Retailer Services provides some optimism for the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.