e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

AECOM Technology Corporation (NYSE:ACM) released its third quarter fiscal 2025 results on August 5, showcasing strong performance across all key financial metrics. The infrastructure consulting firm’s stock rose 1.1% in aftermarket trading to $112.30, building on its 0.88% gain during regular trading hours.

The company’s presentation highlighted accelerating growth in a favorable infrastructure spending environment, with significant government funding still in early deployment stages. AECOM continues to benefit from secular trends in infrastructure investment, sustainability initiatives, and increasing energy demand across its key markets.

As shown in the following overview of AECOM’s position in the market:

Quarterly Performance Highlights

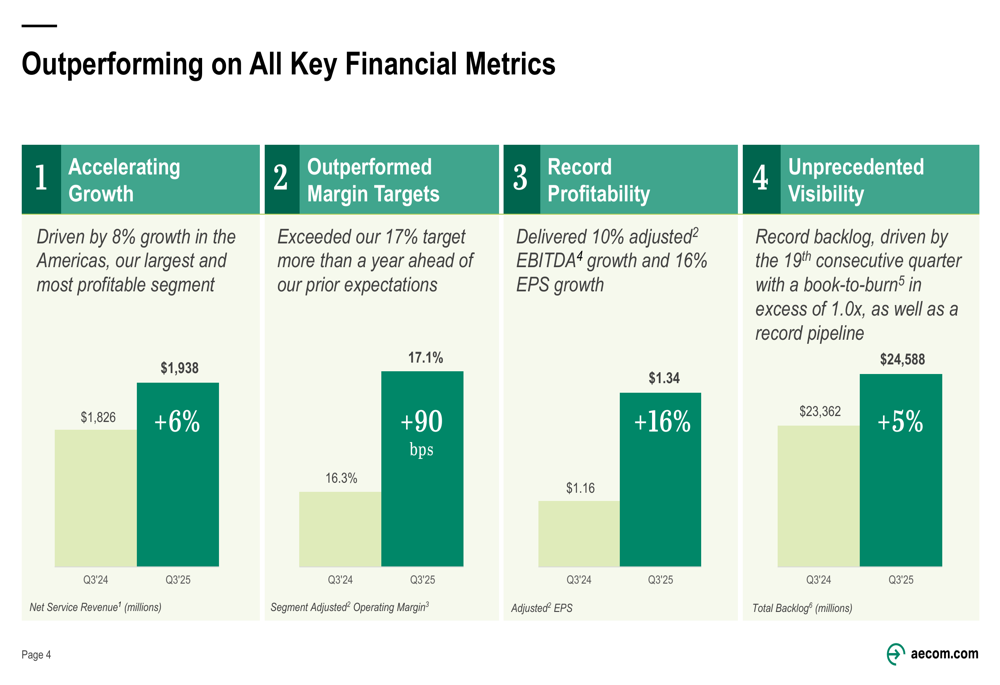

AECOM delivered robust financial results in Q3 2025, outperforming on all key metrics and exceeding its margin targets ahead of schedule. The company reported net service revenue of $1,938 million, representing 6% year-over-year growth, while achieving a segment adjusted operating margin of 17.1%, an improvement of 90 basis points from the prior year.

Adjusted earnings per share reached $1.34, increasing 16% compared to Q3 2024, reflecting the company’s continued focus on high-margin business and operational efficiency. Total (EPA:TTEF) backlog grew to $24,588 million, up 5% year-over-year, providing unprecedented visibility into future revenue streams.

The following chart illustrates AECOM’s strong performance across these key metrics:

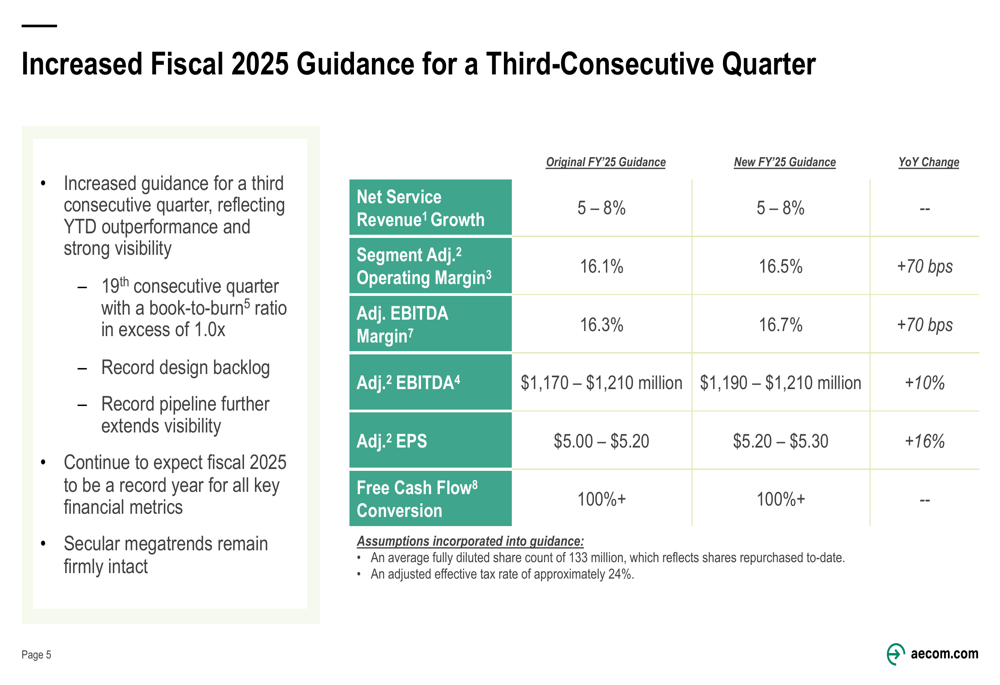

Based on this strong performance, AECOM raised its fiscal 2025 guidance, increasing its segment adjusted operating margin target to 16.5% (up from 16.1%) and narrowing its adjusted EBITDA range to $1,190-$1,210 million. The company also raised its adjusted EPS guidance to $5.20-$5.30, representing a 16% year-over-year increase at the midpoint.

The updated guidance reflects management’s confidence in continued strong execution and favorable market conditions, as shown in the following table:

Detailed Financial Analysis

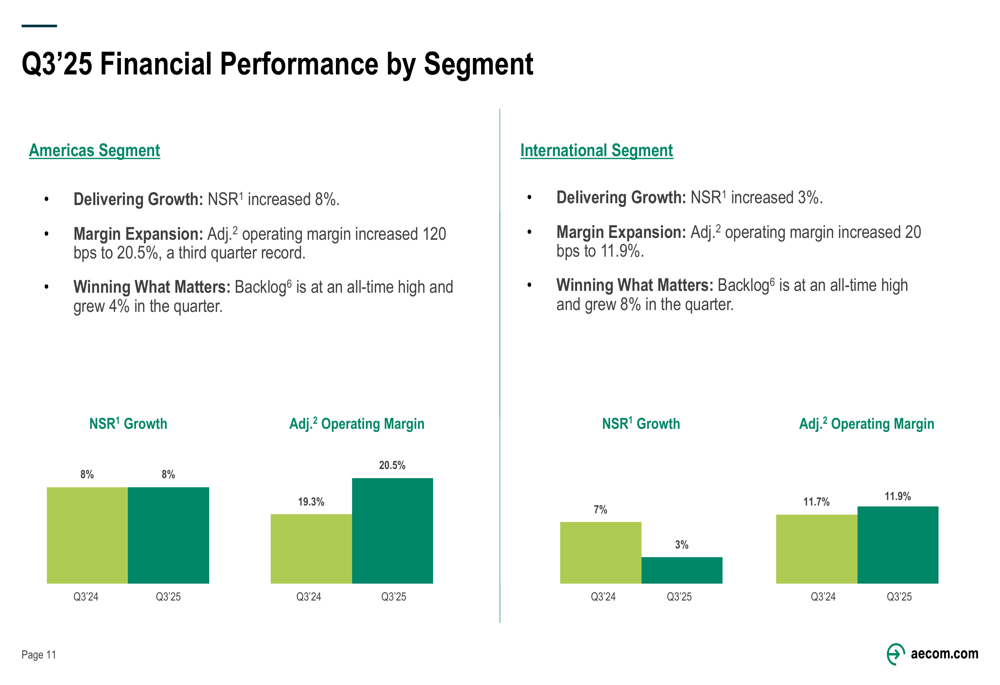

AECOM’s financial performance showed strength across both its Americas and International segments. The Americas segment, which represents the larger portion of the business, delivered 8% NSR growth and expanded its adjusted operating margin by 120 basis points to an impressive 20.5%. The International segment achieved 3% NSR growth with a 20 basis point improvement in adjusted operating margin to 11.9%.

The following breakdown illustrates the performance of both segments:

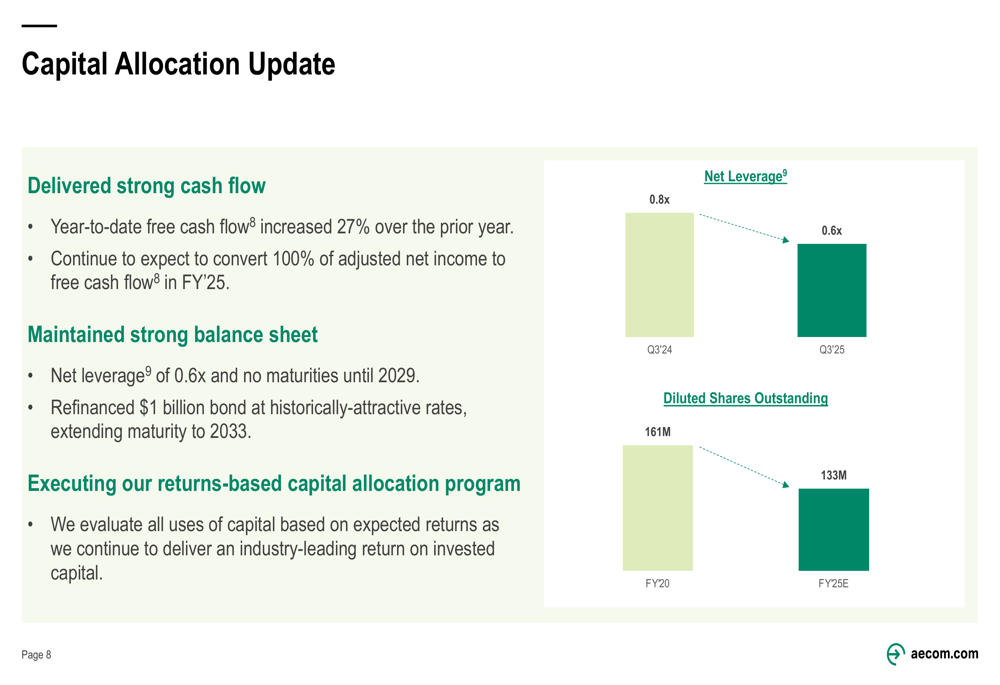

The company’s capital allocation strategy remains focused on delivering strong shareholder returns while maintaining a solid balance sheet. Year-to-date free cash flow increased 27% year-over-year, with the company continuing to expect free cash flow conversion of over 100% of adjusted net income for fiscal 2025. Net leverage improved to 0.6x from 0.8x in the prior year, and AECOM successfully refinanced $1 billion in bonds, extending maturity to 2033.

As shown in the capital allocation update below, AECOM has returned nearly $240 million to shareholders in fiscal 2025 to date and approximately $2.7 billion since initiating share repurchases in September 2020:

Strategic Initiatives & Outlook

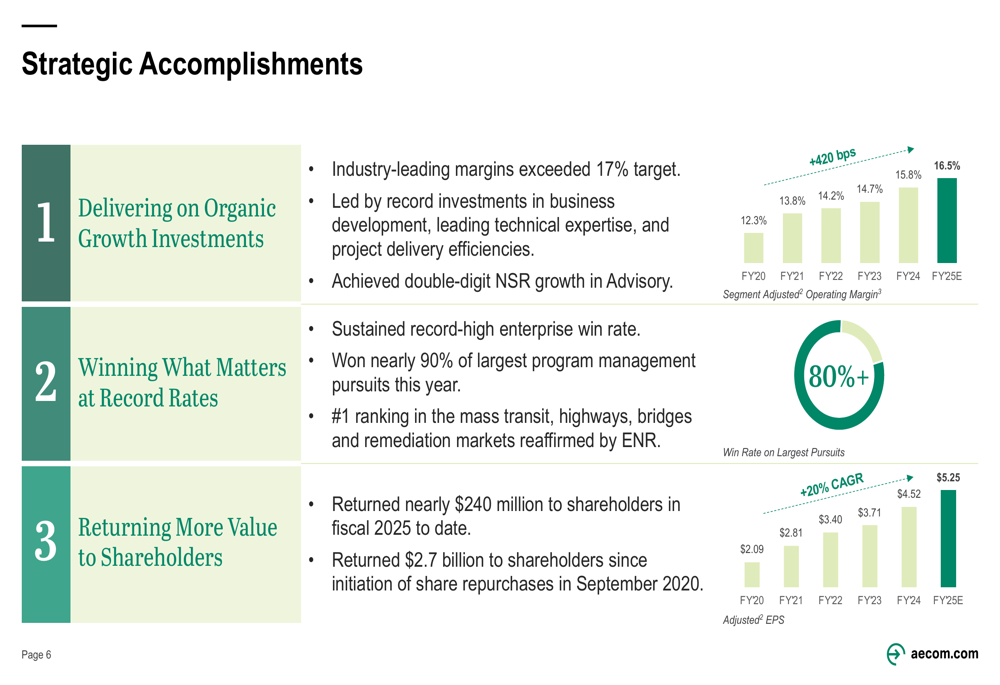

AECOM’s strategic accomplishments in Q3 2025 centered around three key areas: delivering on organic growth investments, winning high-value projects, and returning value to shareholders. The company has successfully expanded its segment adjusted operating margin from 12.3% in FY2020 to a projected 16.5% in FY2025, while growing adjusted EPS from $2.09 to a projected $5.25 over the same period.

The company highlighted its success in winning nearly 90% of its largest program management pursuits this year and maintaining its #1 ranking in mass transit, highways, bridges, and remediation markets according to Engineering News-Record (ENR).

As illustrated in the following strategic accomplishments slide:

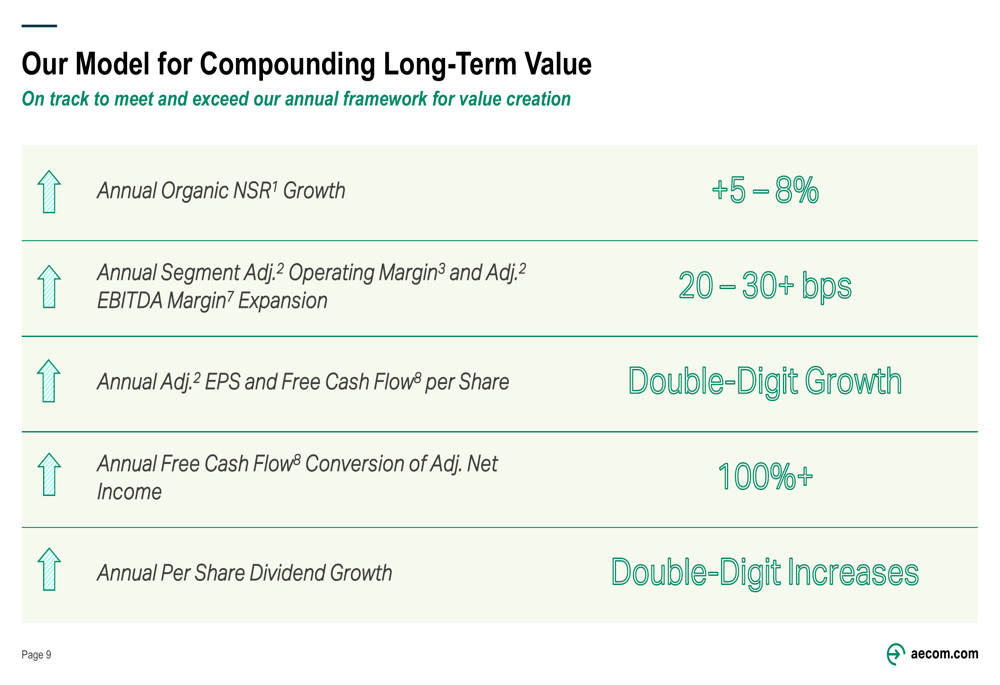

Looking ahead, AECOM outlined its long-term value creation model, targeting 5-8% annual organic net service revenue growth, 20-30+ basis points of annual margin expansion, and double-digit growth in adjusted EPS and free cash flow per share. The company also aims to deliver double-digit annual dividend growth while maintaining free cash flow conversion of over 100% of adjusted net income.

The long-term value creation targets are shown in the following slide:

Competitive Industry Position

AECOM emphasized its industry-leading profitability compared to peers, with segment adjusted operating margins reaching 16.3% on a trailing twelve-month basis through Q3 2025. Despite this superior performance, the company noted a substantial valuation gap, with AECOM trading at 12.5x enterprise value to adjusted EBITDA based on FY2026 estimates, compared to 15.8x for peers.

The company’s diverse exposure across markets, geographies, funding sources, and technical expertise positions it well to capitalize on long-term infrastructure trends. AECOM highlighted its balanced revenue distribution, with approximately 90% of profit coming from four key geographies: the United States, Europe, Middle East & India, and Asia Pacific.

As shown in the following slide, AECOM’s diversified business model provides resilience and multiple growth avenues:

The company’s secular demand drivers remain strong across its key markets. In the U.S. and Canada, only 36% of Infrastructure Investment and Jobs Act (IIJA) funding in AECOM’s primary end markets has been spent, providing substantial visibility for future work. In the UK and Ireland, a new 10-year infrastructure strategy commits £725 billion across water, transportation, and energy sectors. The Middle East continues to show strong infrastructure investment, particularly in the UAE, while Australia and New Zealand maintain long-term demand strength, especially in water programs.

These favorable market conditions, combined with AECOM’s strategic positioning and execution, support management’s confidence in achieving its raised guidance for fiscal 2025 and long-term growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.