United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

The AES Corporation (NYSE:AES) presented its first quarter 2025 financial results on May 2, revealing a decline in quarterly earnings while highlighting strong momentum in its renewable energy business and strategic positioning with technology customers. Despite reporting lower year-over-year results, the company maintained its full-year guidance and emphasized its growing project backlog.

AES shares closed at $9.95 on May 1, 2025, near its 52-week low of $9.57, suggesting investors remain cautious about the company’s near-term performance despite its strategic initiatives in renewable energy and data center markets.

Quarterly Performance Highlights

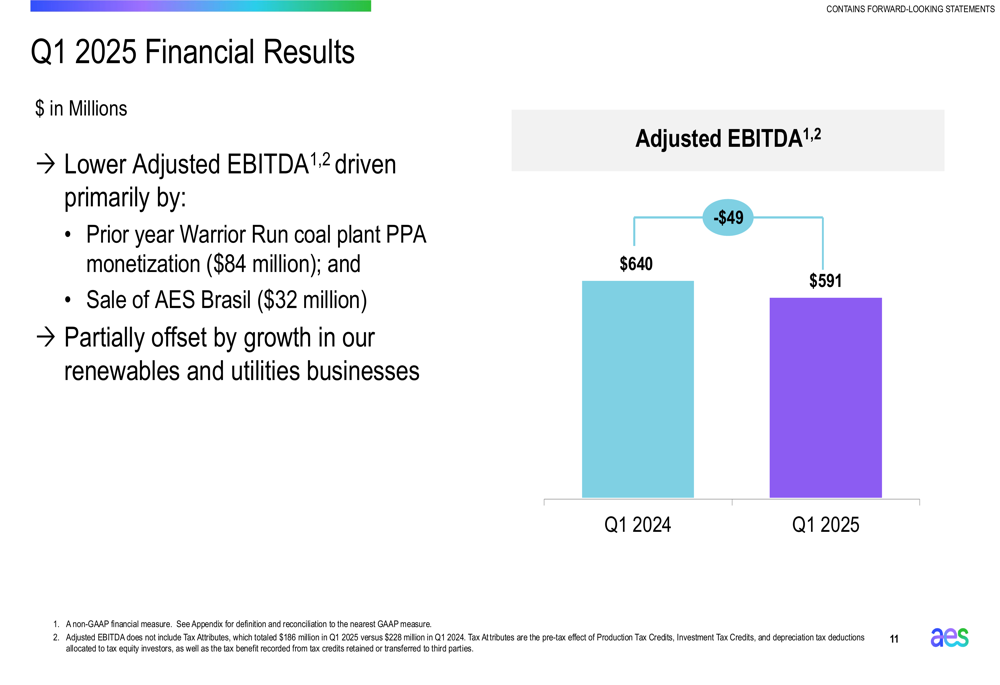

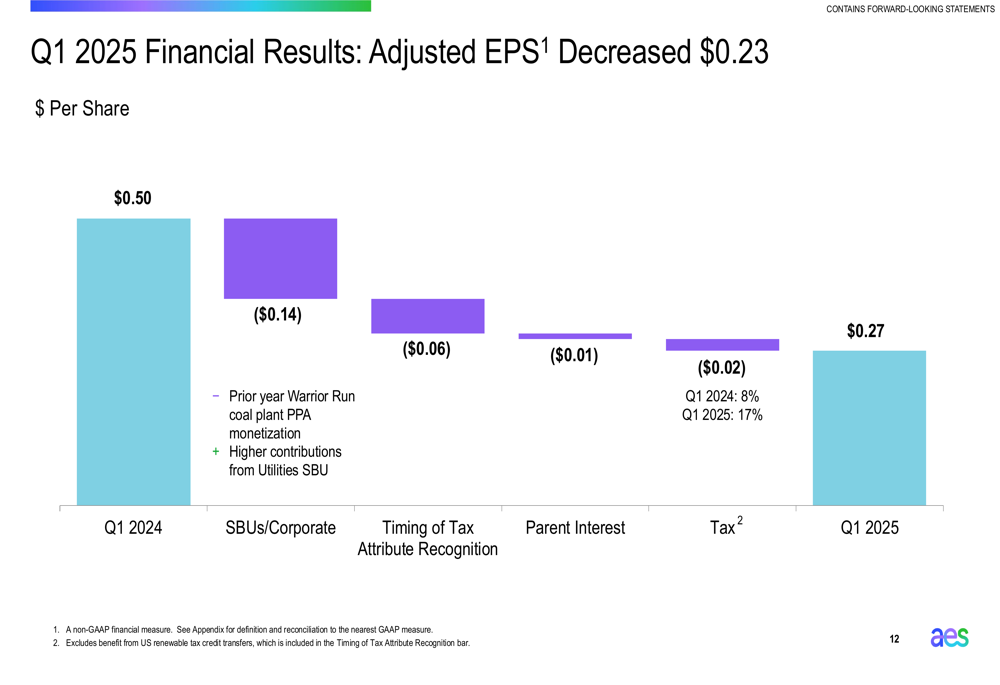

AES reported Q1 2025 Adjusted EBITDA of $591 million, down from $640 million in the same period last year. Adjusted EPS came in at $0.27, a significant decrease from $0.50 in Q1 2024. The company attributed the decline primarily to the prior year’s Warrior Run coal plant PPA monetization ($84 million impact) and the sale of AES Brasil ($32 million impact).

As shown in the following chart comparing quarterly Adjusted EBITDA:

The decline in Adjusted EPS was broken down in detail, with the largest negative factors being SBUs/Corporate (-$0.14), timing of tax attribute recognition (-$0.06), and tax impacts (-$0.02):

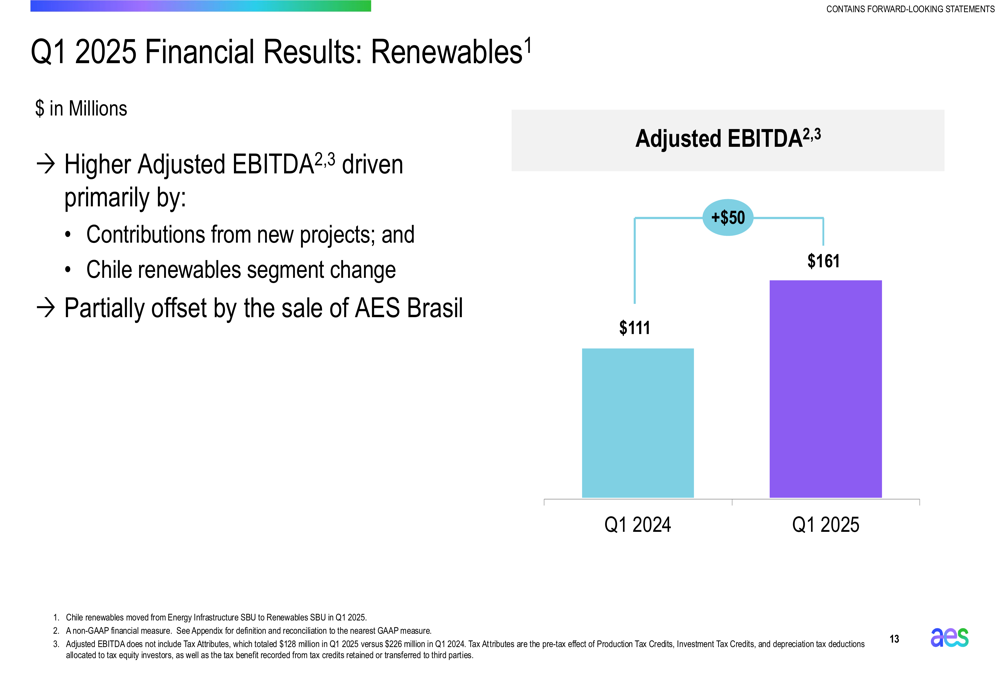

Despite the overall decline, AES’s renewable energy segment showed strong performance, with Adjusted EBITDA increasing from $111 million in Q1 2024 to $161 million in Q1 2025, driven by contributions from new projects and the Chile renewables segment change:

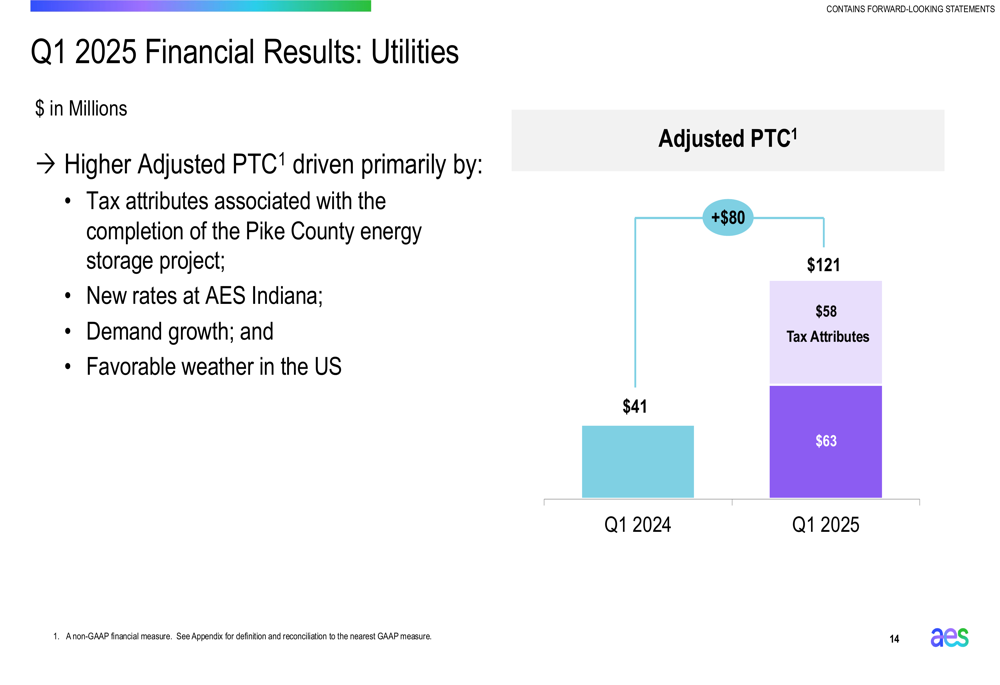

The utilities segment also demonstrated significant growth, with Adjusted PTC (NASDAQ:PTC) rising from $41 million to $121 million, boosted by tax attributes associated with the completion of the Pike County energy storage project, new rates at AES Indiana, demand growth, and favorable weather in the US:

Strategic Initiatives

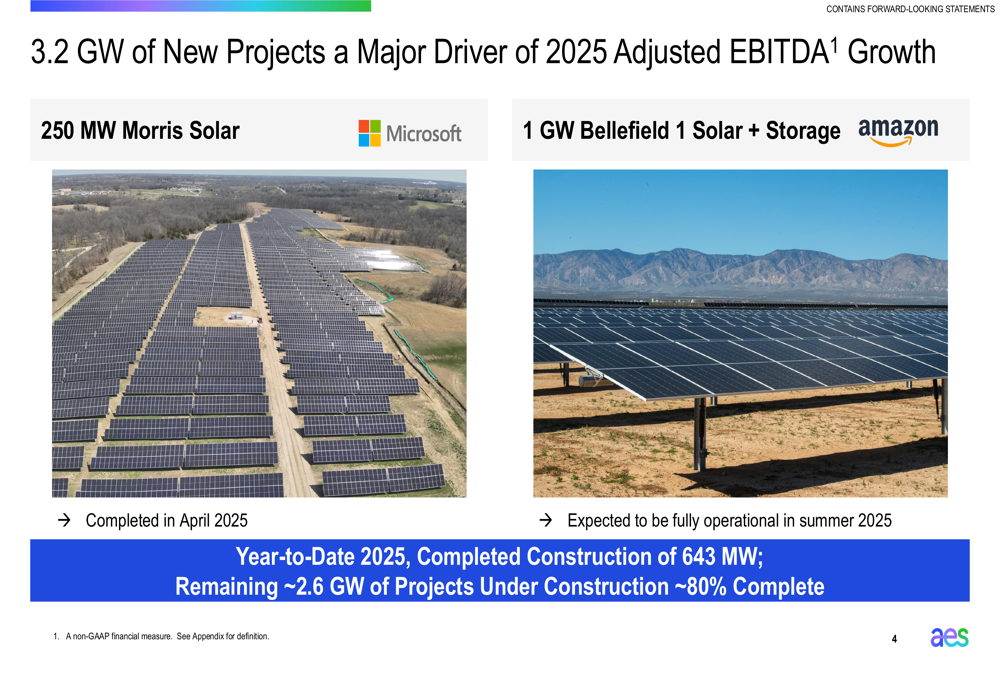

AES highlighted several strategic achievements during the quarter, including signing or being awarded 443 MW of new PPAs for renewables, bringing its backlog to 11.7 GW. The company also completed construction of 643 MW of renewables, with the remaining 2.6 GW of projects under construction for 2025 now approximately 80% complete.

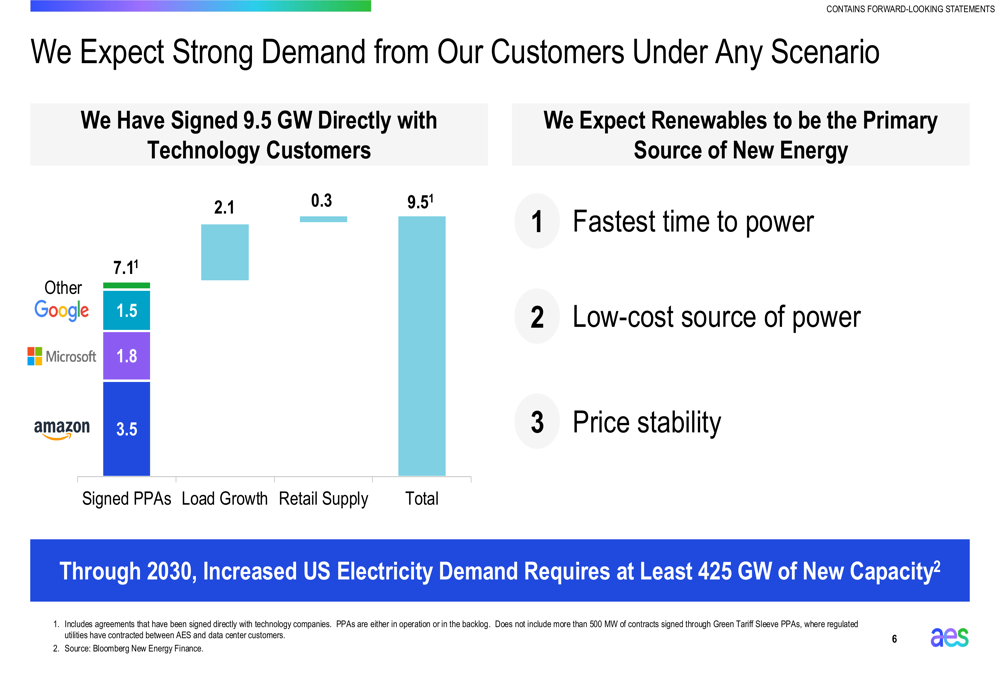

The company’s strategic focus on key technology customers continues to drive growth, with 9.5 GW of renewable capacity signed directly with major tech companies. As illustrated in the following chart, Amazon (NASDAQ:AMZN) leads with 3.5 GW, followed by Microsoft (NASDAQ:MSFT) with 1.8 GW and Google (NASDAQ:GOOGL) with 1.5 GW:

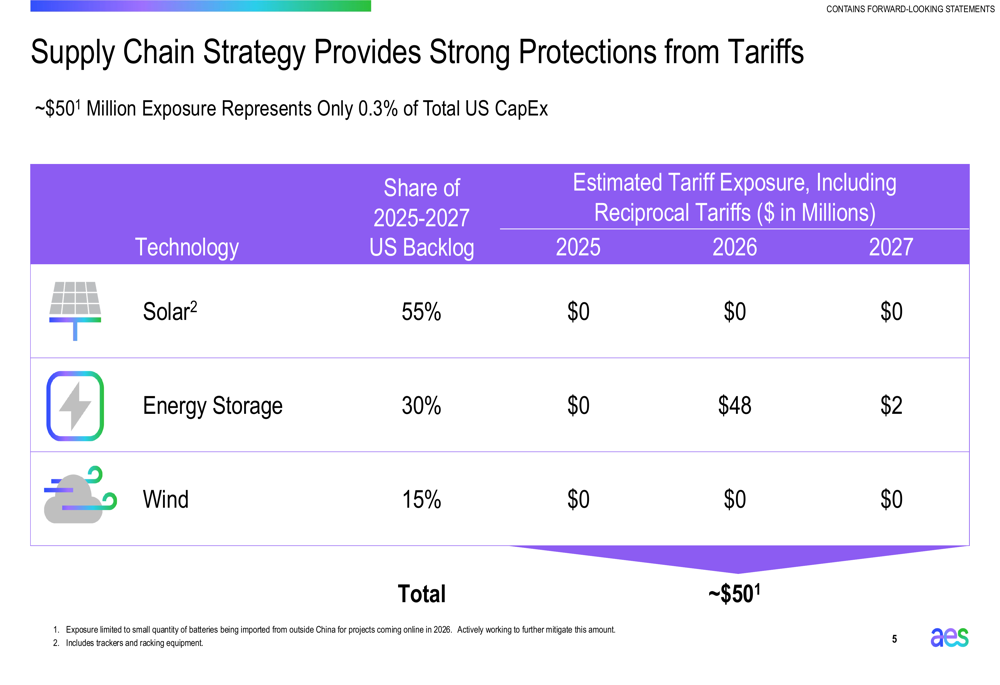

AES emphasized its supply chain strategy, which provides strong protection against potential tariff impacts. The company reported minimal exposure to tariffs, with only about $50 million exposure representing just 0.3% of total US CapEx:

The company also highlighted two major projects driving 2025 Adjusted EBITDA growth: the 250 MW Morris Solar project with Microsoft (completed in April 2025) and the 1 GW Bellefield 1 Solar + Storage project with Amazon (expected to be fully operational in summer 2025):

Forward-Looking Statements

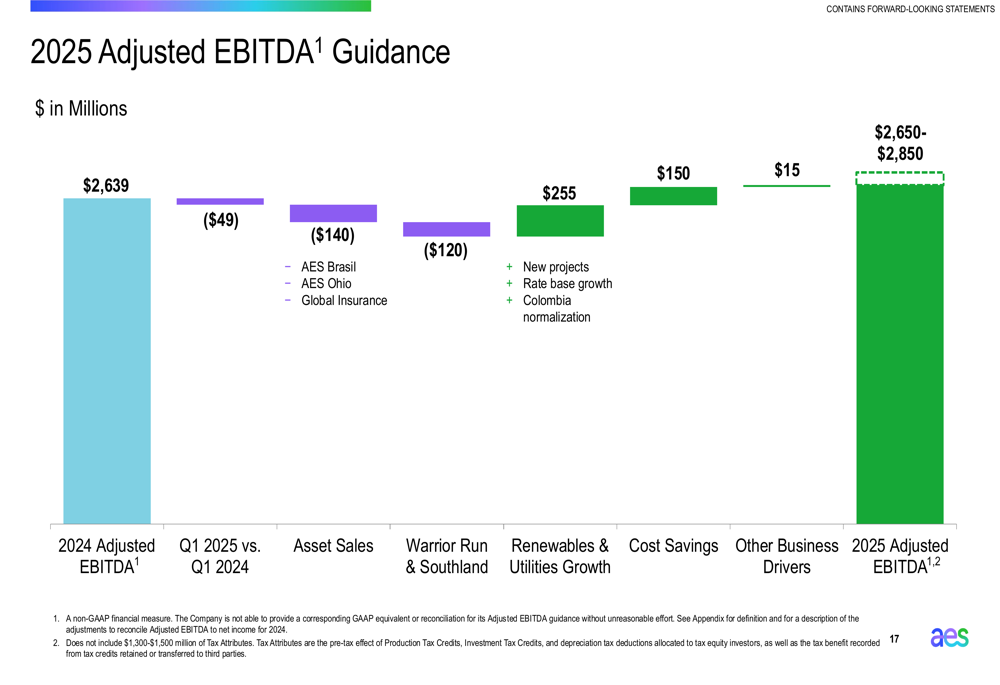

Despite the quarterly earnings decline, AES reaffirmed its 2025 guidance, projecting Adjusted EBITDA between $2,650 million and $2,850 million. The company provided a detailed breakdown of the factors contributing to this guidance:

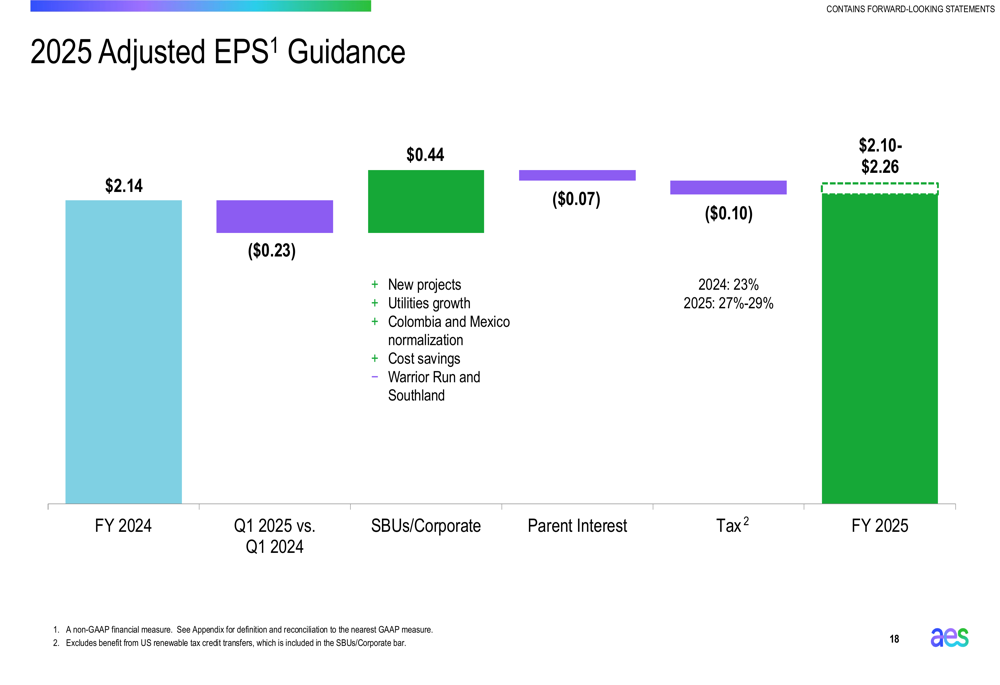

For Adjusted EPS, AES maintained its guidance range of $2.10 to $2.26 for 2025, with a waterfall chart showing the key drivers of change from 2024:

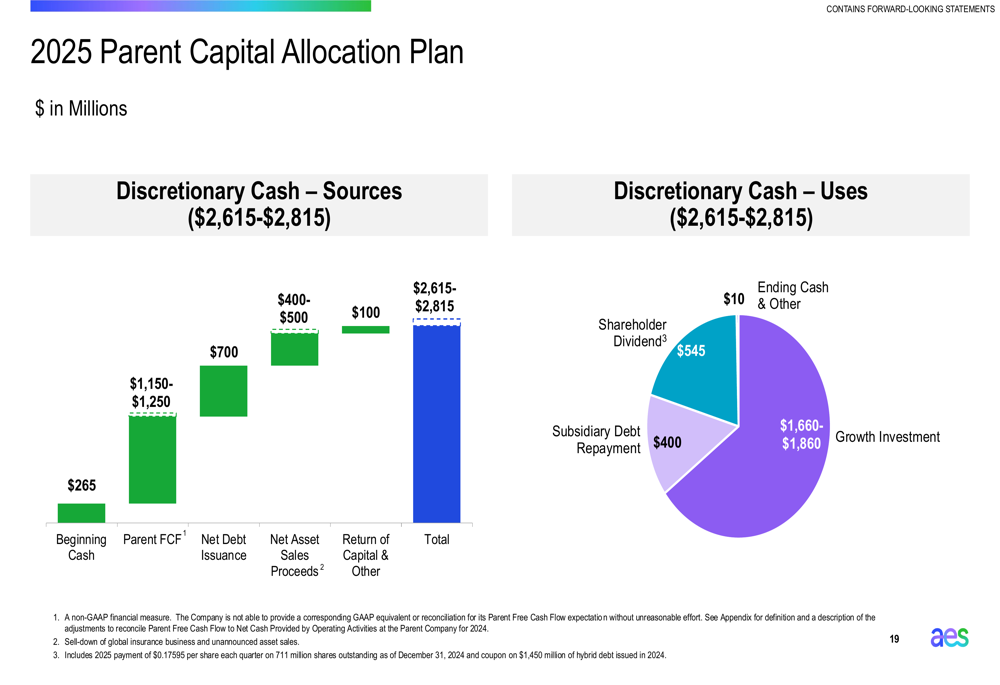

The company also outlined its 2025 Parent Capital Allocation Plan, with discretionary cash sources and uses forecasted between $6,065 million and $6,365 million:

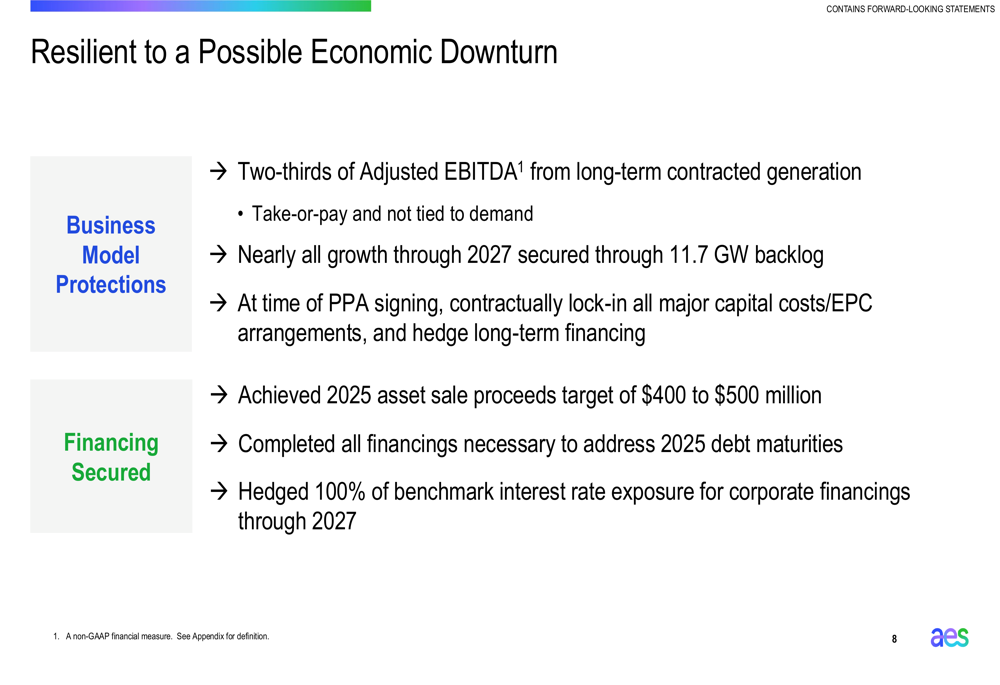

AES highlighted its resilience to potential economic downturns, noting that two-thirds of its Adjusted EBITDA comes from long-term contracted generation, nearly all growth through 2027 is secured through its 11.7 GW backlog, and it has contractually locked in major capital costs and hedged long-term financing:

Detailed Financial Analysis

AES achieved its 2025 asset sale proceeds target with the sale of a minority stake in AES Global Insurance Company for $450 million. The company also completed all financings necessary to address 2025 debt maturities and hedged 100% of benchmark interest rate exposure for corporate financings through 2027.

The company’s utilities segment is experiencing robust growth, with AES Ohio having 2.1 GW of new data centers in its service territory and expecting to break ground this summer on a $500 million transmission investment needed to serve a new Amazon data center. AES Indiana completed the 200 MW Pike County energy storage project, the largest operational battery storage project in MISO, and continues to make progress on the 295 MW Petersburg Energy Center solar-plus-storage project expected to be operational by year-end.

The company’s tax rate is expected to rise from 23% in 2024 to between 27-29% in 2025, which will impact earnings. However, tax attributes are expected to add $1,300-$1,500 million to 2025 results, providing a significant boost to the company’s financial performance.

AES’s Q1 2025 results reflect a company in transition, with short-term earnings pressure from asset sales and prior-year comparisons, but with strong momentum in its renewable energy business and strategic positioning with technology customers. The company’s focus on long-term contracted business models and its growing backlog of renewable projects suggest potential for improved performance in the coming quarters, though investors appear to be taking a wait-and-see approach given the current stock price.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.