Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

AEye Inc (NASDAQ:LIDR) presented its second quarter 2025 earnings on July 31, showcasing a mix of strategic achievements and ongoing financial challenges. The LiDAR technology company’s stock experienced significant volatility following the announcement, surging 8.87% in aftermarket trading on the earnings day before plunging 11.63% in the following day’s premarket session.

The presentation comes amid AEye’s efforts to position itself as a capital-efficient player in the competitive LiDAR space, where the company has seen its stock gain an impressive 291% over the past six months despite ongoing profitability challenges.

Strategic Initiatives & Partnerships

AEye highlighted several key strategic developments in its presentation, with particular emphasis on partnerships with major technology and automotive companies.

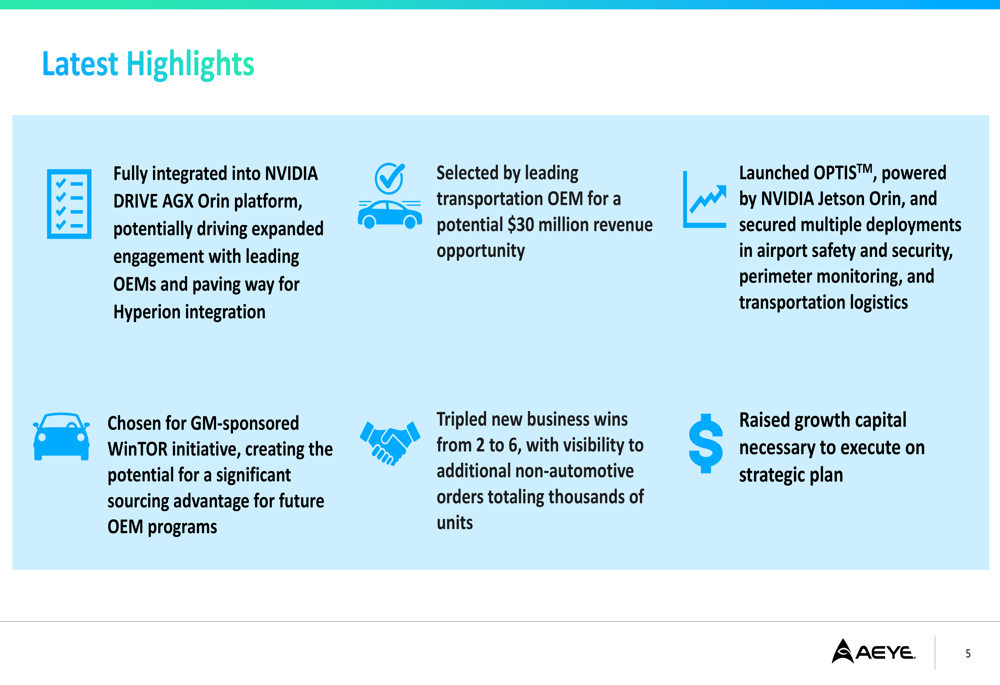

As shown in the following highlights slide, the company has fully integrated into NVIDIA (NASDAQ:NVDA)’s DRIVE AGX Orin platform, potentially opening doors to expanded engagement with leading OEMs:

The NVIDIA partnership represents a cornerstone of AEye’s strategy, with the company launching its OPTIST™ platform powered by NVIDIA Jetson Orin. This product has already secured multiple deployments across various sectors including airport safety, perimeter monitoring, and transportation logistics.

Another significant win highlighted in the presentation is AEye’s selection for the GM-sponsored WinTOR initiative, which the company believes could create a substantial sourcing advantage for future OEM programs. The company also secured a contract with a leading transportation OEM, representing a potential $30 million revenue opportunity to be realized over the next 2-3 years.

Quarterly Performance Highlights

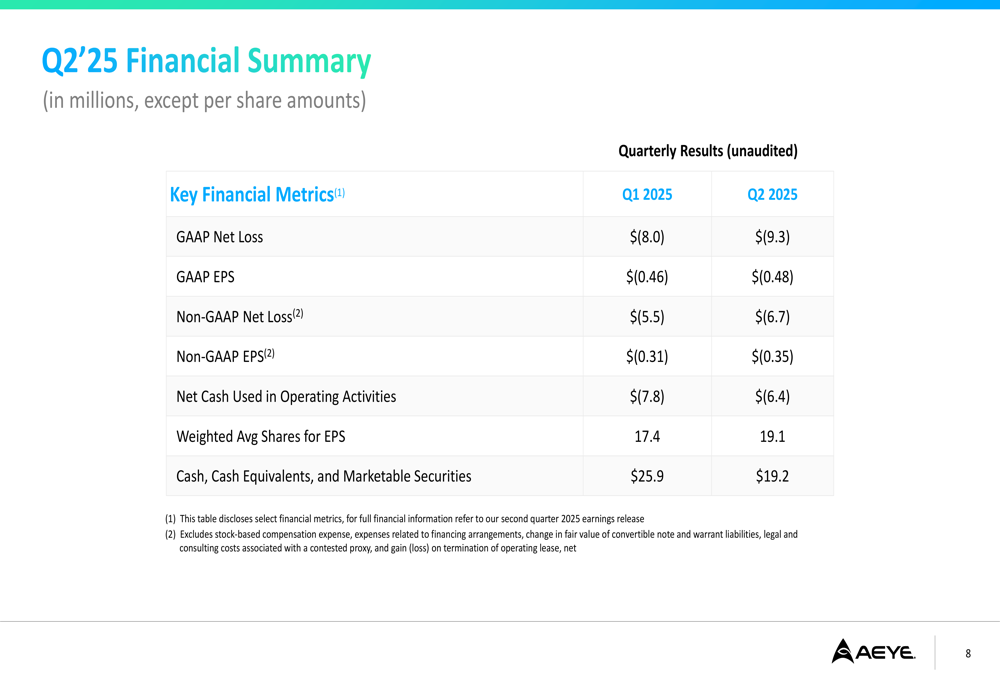

Despite the strategic wins, AEye’s financial performance for Q2 2025 showed increasing losses compared to the previous quarter. The company’s detailed financial summary reveals the extent of these challenges:

AEye reported a GAAP net loss of $9.3 million for Q2 2025, deteriorating from the $8.0 million loss in Q1. On a per-share basis, this translated to a loss of $0.48, compared to $0.46 in the previous quarter. Non-GAAP figures showed a similar trend, with net loss increasing to $6.7 million ($0.35 per share) from $5.5 million ($0.31 per share) in Q1.

The company’s cash position declined to $19.2 million at the end of Q2, down from $25.9 million at the end of Q1, though the company noted an improvement in cash used for operations, which decreased from $7.8 million to $6.4 million quarter-over-quarter.

Competitive Industry Position

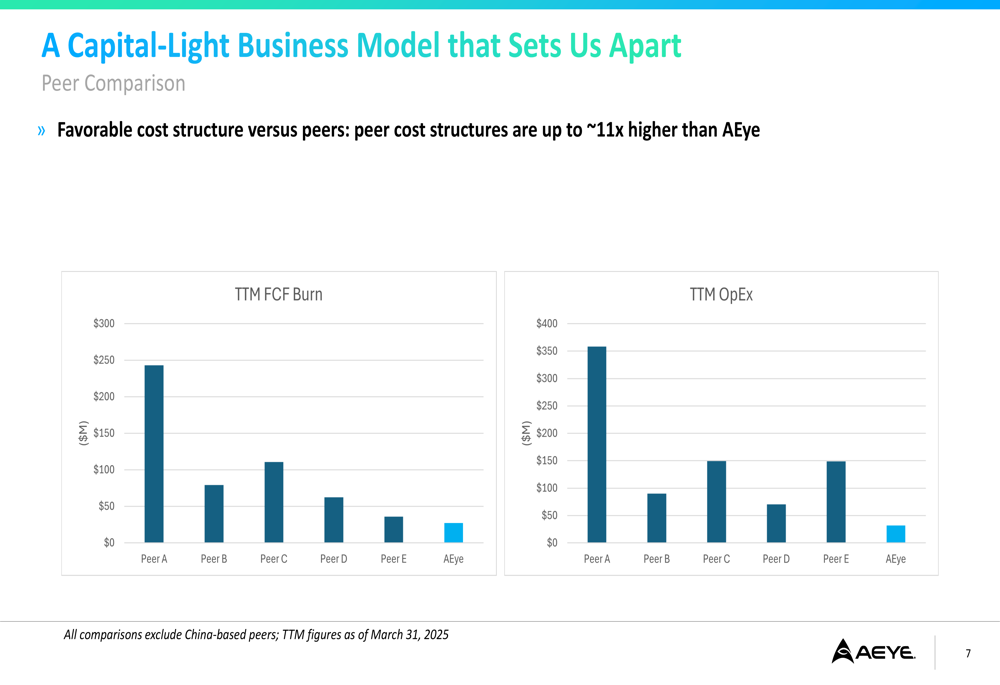

A central theme of AEye’s presentation was its capital-light business model, which the company positions as a significant competitive advantage in the LiDAR industry. The following slide illustrates how AEye’s cost structure compares favorably to industry peers:

According to the company’s analysis, AEye’s trailing twelve-month free cash flow burn of $10 million is substantially lower than competitors, which range from $20 million to $260 million. Similarly, its operating expenses of $40 million compare favorably to peers ranging from $60 million to $450 million.

This capital efficiency approach appears to be central to AEye’s strategy as it navigates a path toward profitability in a sector where many companies are burning through significant cash reserves while pursuing technological advancement and market share.

Forward-Looking Statements

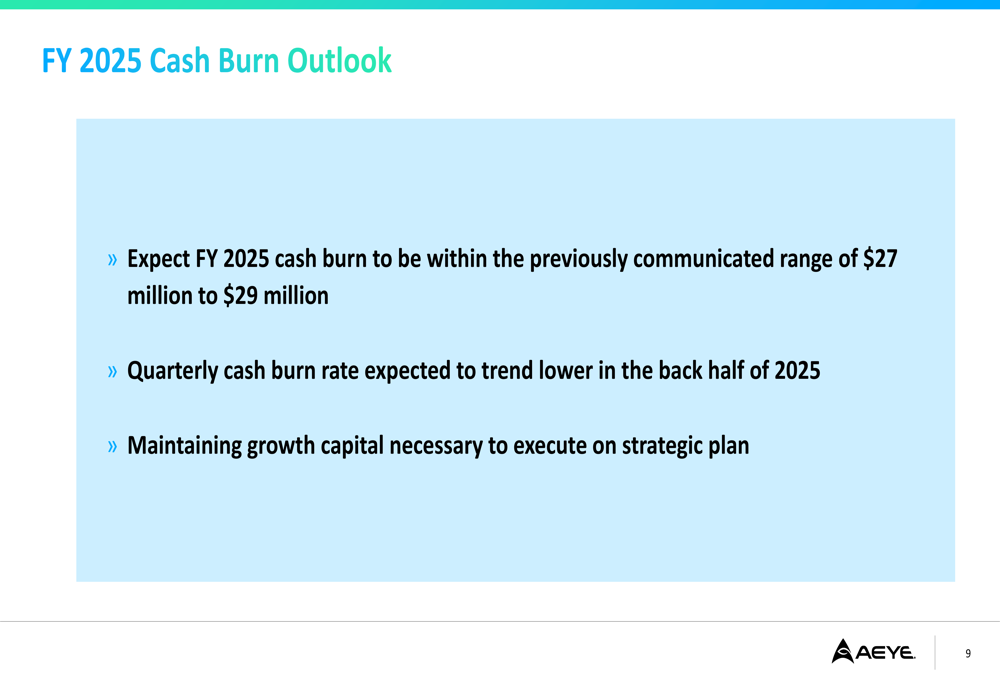

Looking ahead, AEye provided guidance on its expected cash burn for the remainder of 2025:

The company expects its full-year 2025 cash burn to remain within the previously communicated range of $27 million to $29 million, with quarterly burn rates projected to trend lower in the second half of the year. This guidance suggests management is focused on improving capital efficiency while maintaining sufficient resources to execute its strategic plan.

Detailed Financial Analysis

The contrast between AEye’s strategic achievements and financial performance raises questions about the company’s path to profitability. While the company has tripled its new business wins and secured potentially lucrative contracts, its immediate financial metrics continue to deteriorate.

The increase in weighted average shares from 17.4 million in Q1 to 19.1 million in Q2 indicates dilution for existing shareholders, likely resulting from the capital raise mentioned in the presentation. This additional capital appears necessary to fund operations as the company works toward monetizing its strategic partnerships and contract wins.

The market’s mixed reaction—initial enthusiasm followed by a significant pullback—suggests investors are weighing AEye’s long-term potential against its near-term financial challenges. As the company continues to execute its capital-light strategy and pursue integration with major technology platforms like NVIDIA’s, investors will be closely monitoring whether these strategic initiatives translate into improved financial performance in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.