Street Calls of the Week

Introduction & Market Context

agilon health (NYSE:AGL) presented its Q2 2025 earnings on August 4, 2025, revealing substantial financial challenges and a major leadership overhaul. The company’s stock closed at $1.70, up 6.76% on the day, with modest aftermarket gains of 2.35%. Despite this positive trading session, the stock remains significantly below its 52-week high of $6.63, reflecting ongoing investor concerns about the company’s performance trajectory.

Executive Summary

The Q2 2025 presentation revealed a stark contrast to the company’s Q1 results, with agilon reporting a net loss of $104 million and negative medical margin of $53 million. This represents a dramatic deterioration from Q1 2025, when the company reported positive earnings per share of $0.03 and a medical margin of $128 million. The disappointing performance has triggered significant organizational changes, including the departure of CEO Steven Sell and the establishment of an Office of the Chairman to accelerate performance improvements.

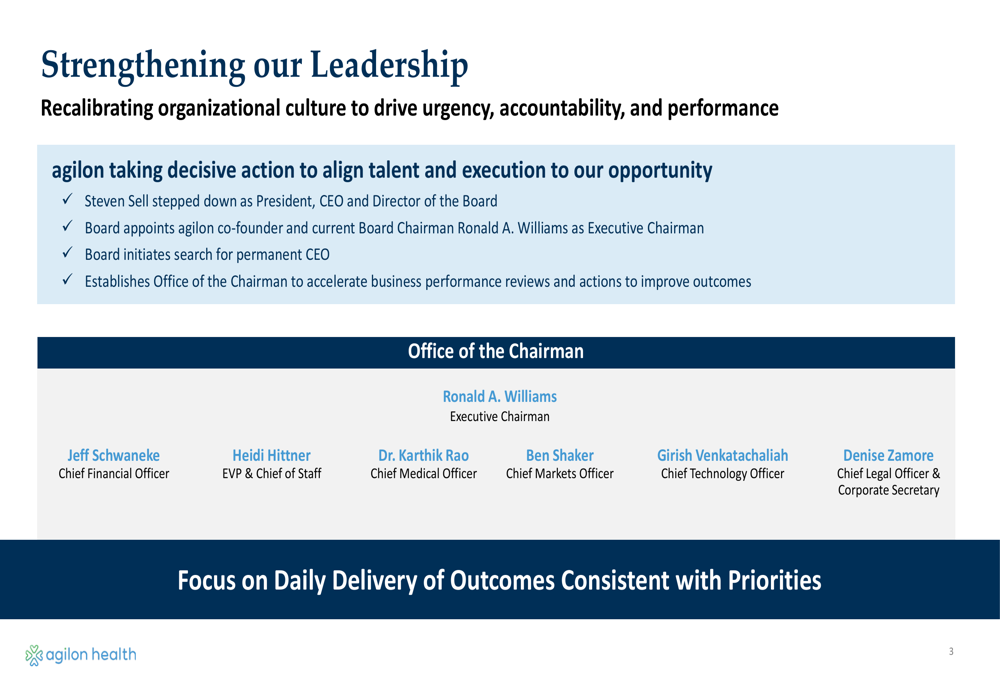

As shown in the following leadership restructuring slide:

The company has appointed co-founder and Board Chairman Ronald A. Williams as Executive Chairman, while initiating a search for a permanent CEO. The newly established Office of the Chairman includes key executives across finance, medical, technology, legal, and market operations functions, reflecting a comprehensive approach to addressing the company’s challenges.

Financial Performance Analysis

agilon’s Q2 2025 financial results fell significantly short of expectations, primarily due to revised risk adjustment factors for both 2024 and 2025. The company reported total revenues of $1.395 billion, down from $1.53 billion in Q1 2025, with a net loss of $104 million and negative Adjusted EBITDA of $83 million.

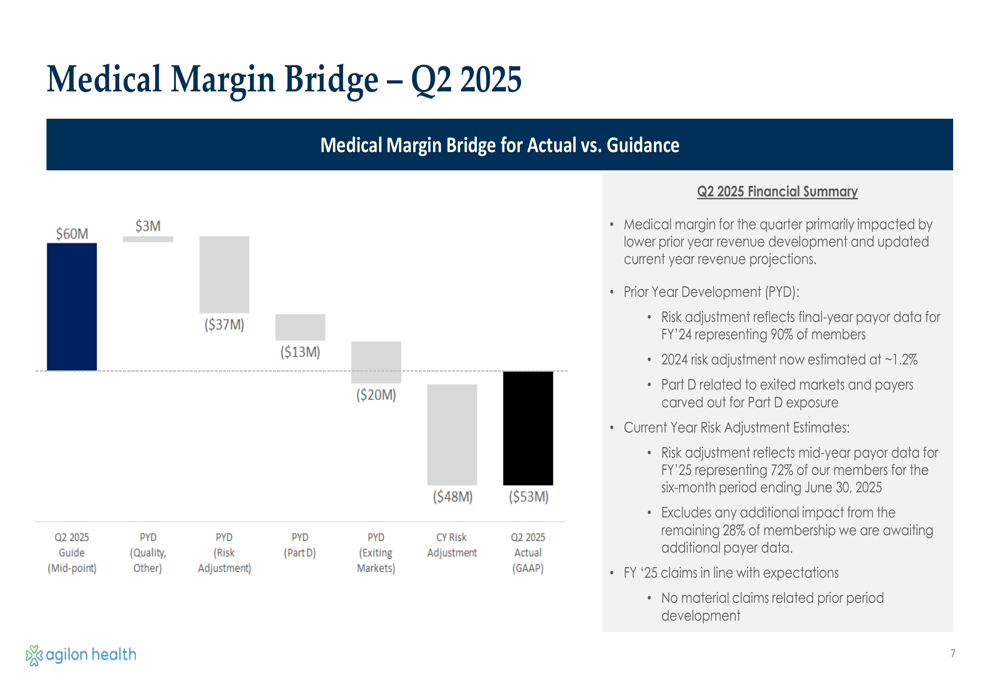

The following medical margin bridge illustrates the dramatic impact of risk adjustment revisions:

Starting with original guidance of $60 million in medical margin, the company experienced a series of negative adjustments: $37 million for prior year risk adjustment, $13 million for Part D, $20 million for exiting markets, and $48 million for current year risk adjustment. These factors collectively drove the medical margin to negative $53 million, representing a $113 million swing from guidance.

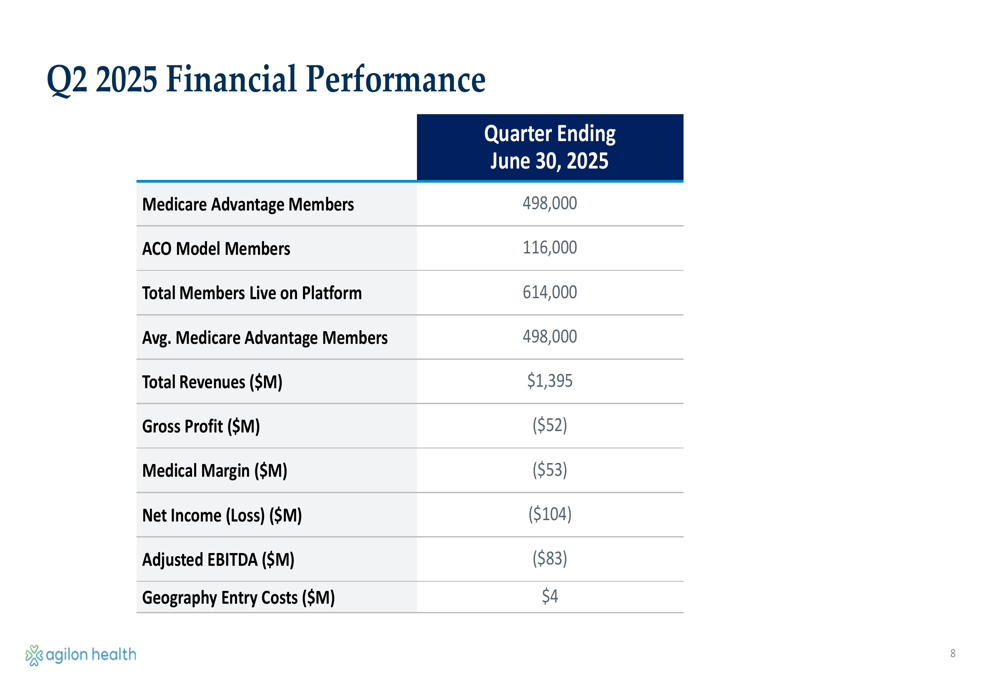

The comprehensive financial performance summary shows the scale of the challenge:

Despite these challenges, agilon maintains a relatively strong balance sheet with approximately $327 million in cash and short-term investments (excluding $176 million in ACO REACH Cash). The company serves 498,000 Medicare Advantage members and 116,000 ACO model members, for a total of 614,000 members on its platform.

Strategic Initiatives

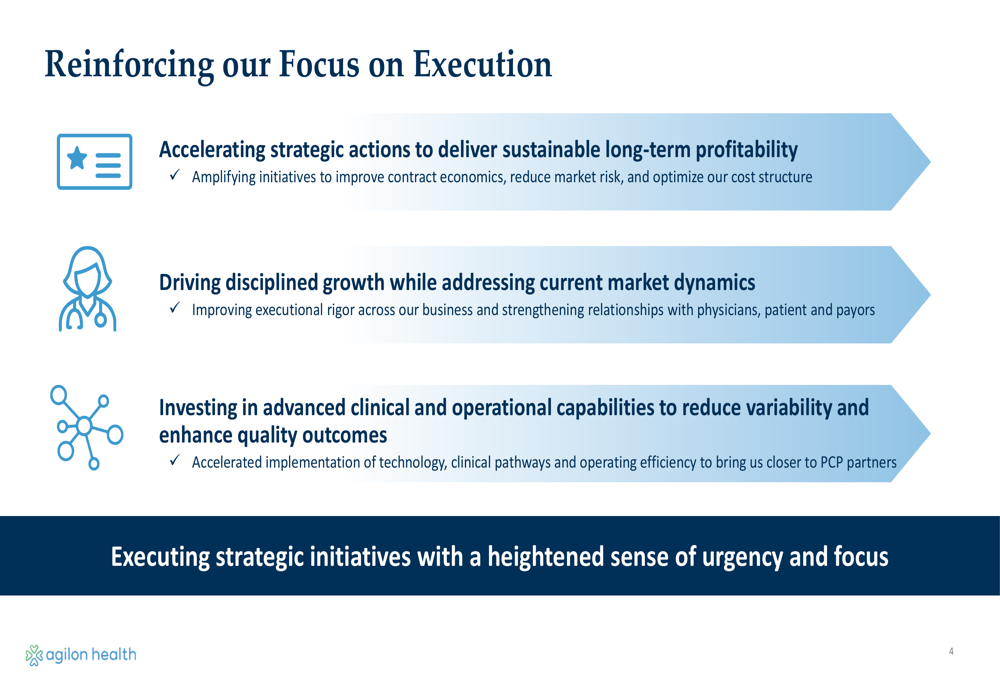

In response to these challenges, agilon has outlined a renewed strategic focus on execution and operational discipline. The company is implementing a three-pronged approach to address current market dynamics:

The strategy emphasizes accelerating actions to deliver sustainable long-term profitability, driving disciplined growth while addressing current market challenges, and investing in advanced clinical and operational capabilities. This represents a significant pivot from the company’s previous approach, with a heightened emphasis on "urgency, accountability, and performance."

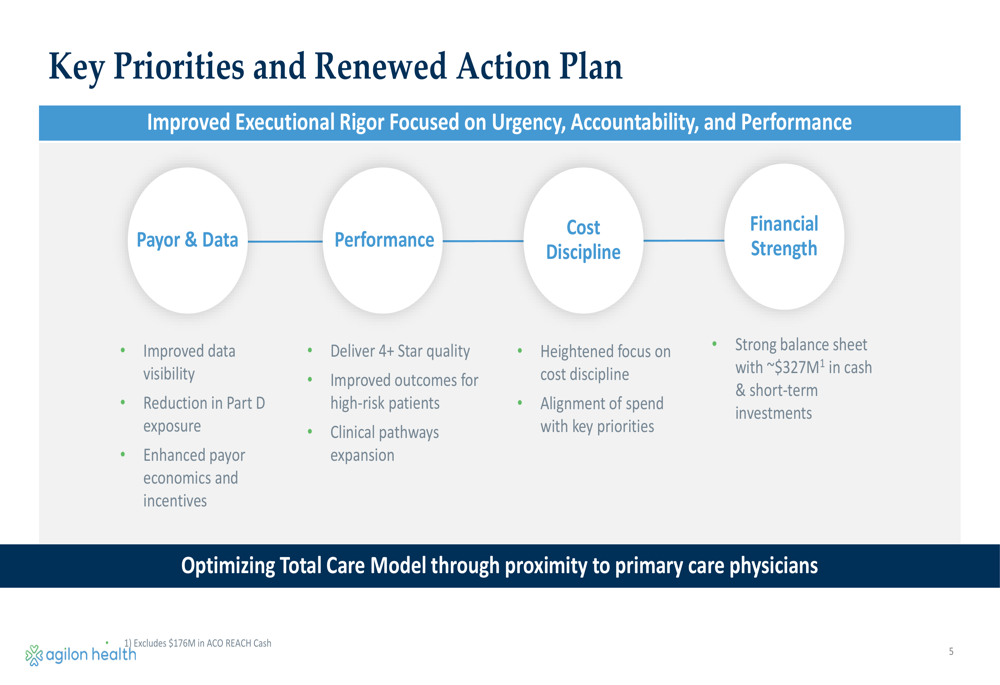

The company has also detailed specific priorities across four key areas:

These priorities include improved data visibility, reduction in Part D exposure, enhanced payor economics, delivering 4+ Star quality, improved outcomes for high-risk patients, heightened cost discipline, and maintaining financial strength. The company specifically notes that it has carved out Part D for 2025, addressing one of the factors that negatively impacted Q2 2025 results.

Forward-Looking Statements

agilon’s presentation suggests that while 2025 remains challenging, the company is implementing structural changes to improve future performance. Key to this effort is enhancing data infrastructure to provide better visibility into risk adjustment factors and cost trends for 2026.

The company notes that "Data infrastructure enhancements already providing additional visibility to insights supporting forecasting accuracy for RAF and cost trends for 2026," indicating that management believes the risk adjustment surprises experienced in Q2 2025 can be mitigated going forward.

This represents a significant shift from Q1 2025, when then-CEO Steve Sell characterized 2025 as "both a transition year financially and an inflection year in terms of quality and clinical programs." The leadership change and strategic reset suggest the transition has proven more challenging than initially anticipated.

While agilon faces significant headwinds, its strong cash position provides some runway to implement its strategic initiatives. Investors will be closely watching whether the new leadership structure can successfully execute on the company’s renewed focus on operational discipline and improved contract economics in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.