ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

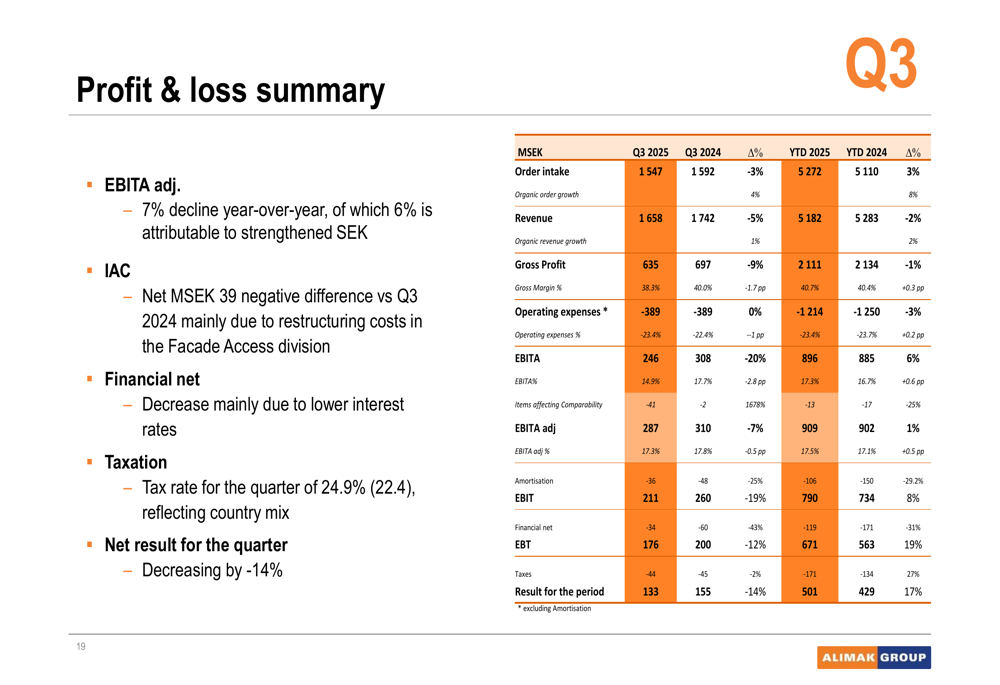

Alimak Group (STO:ALIG) shares fell 8.11% following the company’s Q3 2025 earnings presentation on October 23, as investors reacted to declining margins and challenges in key markets despite modest organic growth. The vertical access solutions provider reported earnings per share of SEK 1.25, down 14% year-over-year, while maintaining its strategic focus on service business growth and targeted acquisitions.

The company’s stock closed at SEK 138.2, moving closer to its 52-week low of SEK 107.8 as the market digested both the financial results and ongoing headwinds in the construction sector, particularly in Europe and North America.

Quarterly Performance Highlights

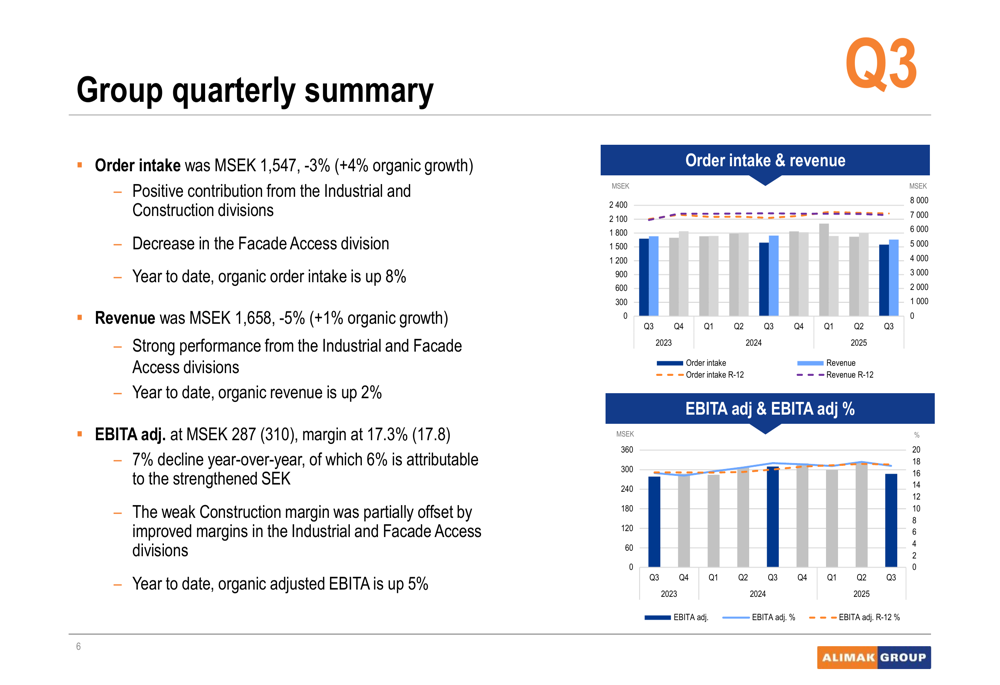

Alimak reported Q3 2025 order intake of MSEK 1,547, representing a 3% decline on a reported basis but 4% organic growth when adjusted for currency effects. Revenue reached MSEK 1,658, down 5% as reported but up 1% organically compared to the same period last year.

As shown in the following chart of quarterly financial performance:

Adjusted EBITA came in at MSEK 287, with a margin of 17.3%, down from 17.8% in the comparable quarter. The company noted that approximately 6% of the 7% year-over-year EBITA decline was attributable to the strengthened Swedish krona, while weak performance in the Construction division also weighed on results.

The detailed profit and loss summary reveals the full financial picture:

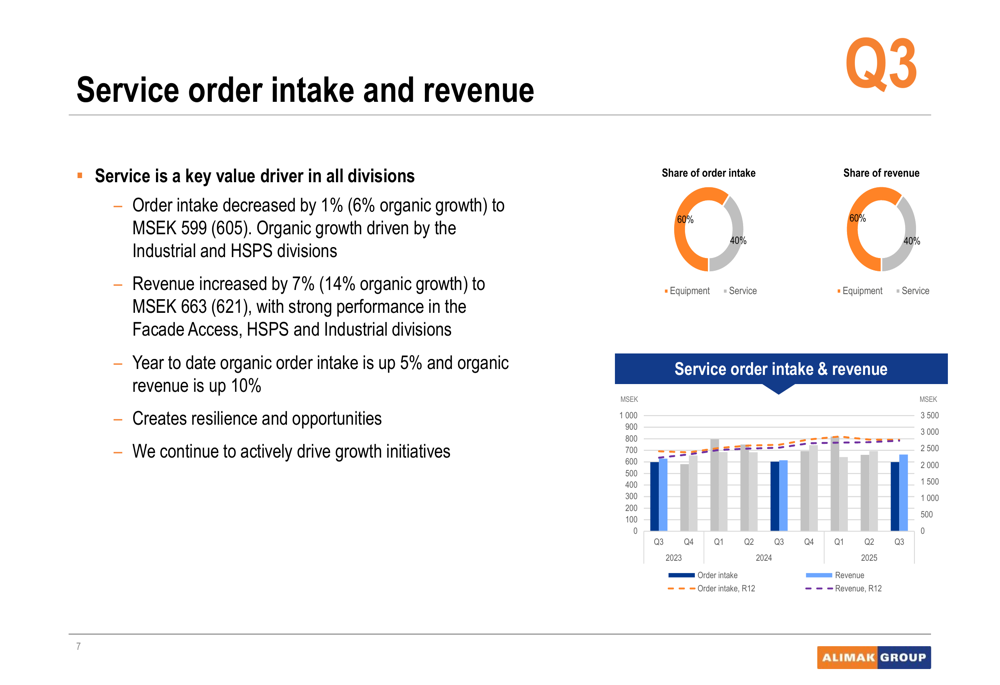

Service business continued to be a bright spot for Alimak, with service order intake growing 6% organically to MSEK 599 and service revenue increasing by an impressive 14% organically to MSEK 663. The company highlighted strong performance in the Facade Access, HSPS (Height Safety & Productivity Solutions), and Industrial divisions.

The service business performance is illustrated in this chart:

Divisional performance varied significantly across the company’s five business segments:

- Facade Access: Revenue up 11% at constant currency with margin improvement to 13.0% from 11.5%

- Construction: Revenue down 16% at constant currency with margin declining to 13.3% from 17.4%

- HSPS: Revenue down 2% at constant currency with margin slightly down to 18.5% from 19.2%

- Industrial: Revenue up 9% organically with margin improving to 24.5% from 23.0%

- Wind: Revenue down 6% at constant currency with margin declining to 18.6% from 19.4%

Strategic Initiatives

Alimak continues to execute its "New Heights 2.0" program focused on profitable growth, with several strategic initiatives highlighted in the presentation:

1. Acquisition strategy: The company signed an agreement on October 21 to acquire Swedish company Interlift, with approximately MSEK 50 in annual revenue. The acquisition is expected to close by the end of November 2025 and will strengthen Alimak’s position in the Nordic market.

2. Integration of Century Elevators: The company reported that the integration of recently acquired Century Elevators is proceeding as planned, with a growing opportunity pipeline and efforts to target the installed base to drive aftermarket sales.

3. European restructuring: Alimak is implementing capacity reductions in Spain and Luxembourg, with two-thirds of the announced MSEK 60 restructuring cost incurred in Q3. The company expects MSEK 30 in recurring cost savings from the beginning of 2026.

4. Product development: The company launched the new Alimak Levato 450, designed specifically for emerging markets and manufactured in China for cost efficiency and proximity to these markets.

The company’s financial and sustainability targets remain ambitious despite current challenges:

Forward-Looking Statements

Alimak maintained a cautiously optimistic outlook while acknowledging ongoing market challenges. The company highlighted signs of improvement in certain regions and segments, including early indications of a trend reversal in the US wind market and improving offshore wind market conditions in Northern Europe.

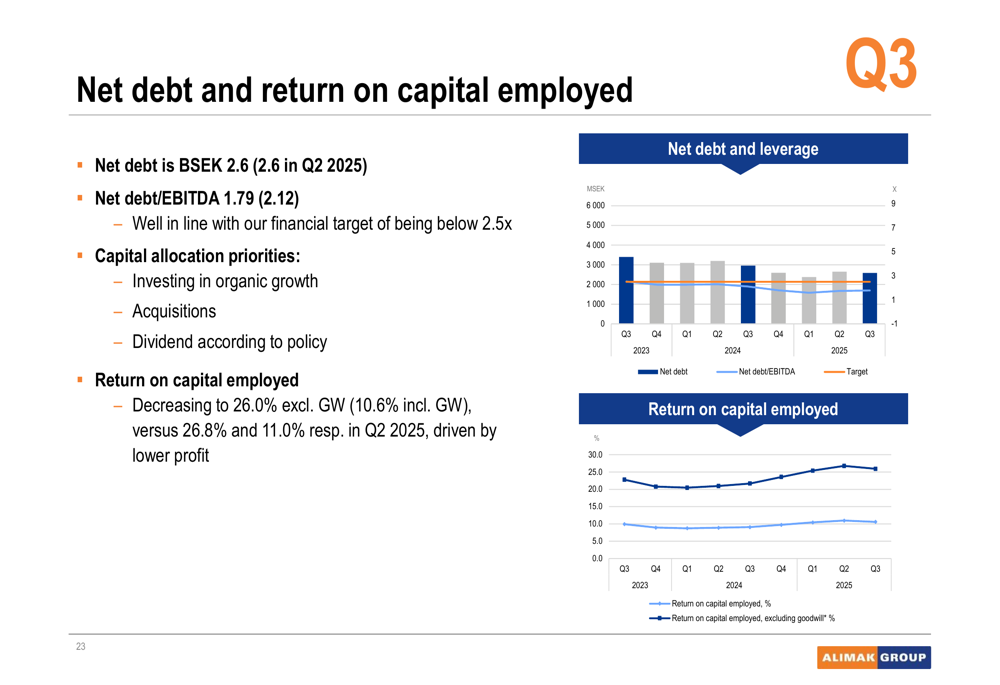

The company’s financial position remains solid with a leverage ratio (Net debt/EBITDA) of 1.79, well below its target ceiling of 2.5x. Cash flow from operations was MSEK 196 in the quarter, supporting the company’s capital allocation priorities.

As illustrated in this chart of the company’s debt position and returns:

CEO Ole Kristian Jødahl emphasized the company’s continued delivery on its strategic program despite market headwinds, stating, "We continue to deliver on the New Heights programme with 4% organic growth." The company also announced an upcoming Capital Markets Day on November 25, where investors can expect further details on strategic initiatives and market outlook.

While Alimak’s presentation emphasized resilience and strategic progress, the market reaction suggests investors remain concerned about margin pressure and the ongoing challenges in key construction markets. The company’s ability to execute on cost-saving initiatives and leverage its service business will be crucial factors in navigating the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.