US stock futures flat after Wall St drops on Trump tariffs, soft jobs data

Introduction & Market Context

Alimentation Couche-Tard (TSX:ATD), the parent company of Circle K, presented its Q4-FY25 investor presentation highlighting mixed quarterly results alongside an ambitious strategic roadmap. The company reported a slight decline in net earnings for the quarter but maintained strong full-year performance with approximately $2.6 billion in net earnings for fiscal 2025.

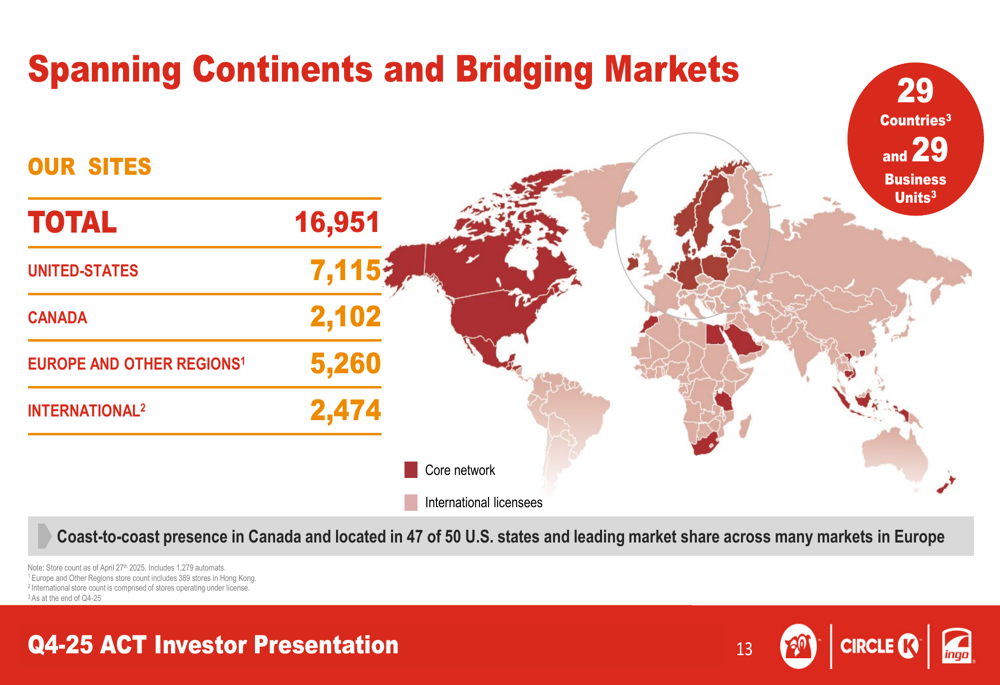

Operating in a convenience retail industry projected to grow at 2.6% CAGR in the US through 2027, Couche-Tard continues to leverage its global scale with 16,951 locations across North America, Europe, and other international markets. The company’s presentation emphasized its resilience in various economic conditions and outlined strategic initiatives aimed at expanding its food, beverage, and fuel offerings.

As shown in the following global presence map, Couche-Tard maintains a strong international footprint with operations concentrated in North America and Europe:

Quarterly Performance Highlights

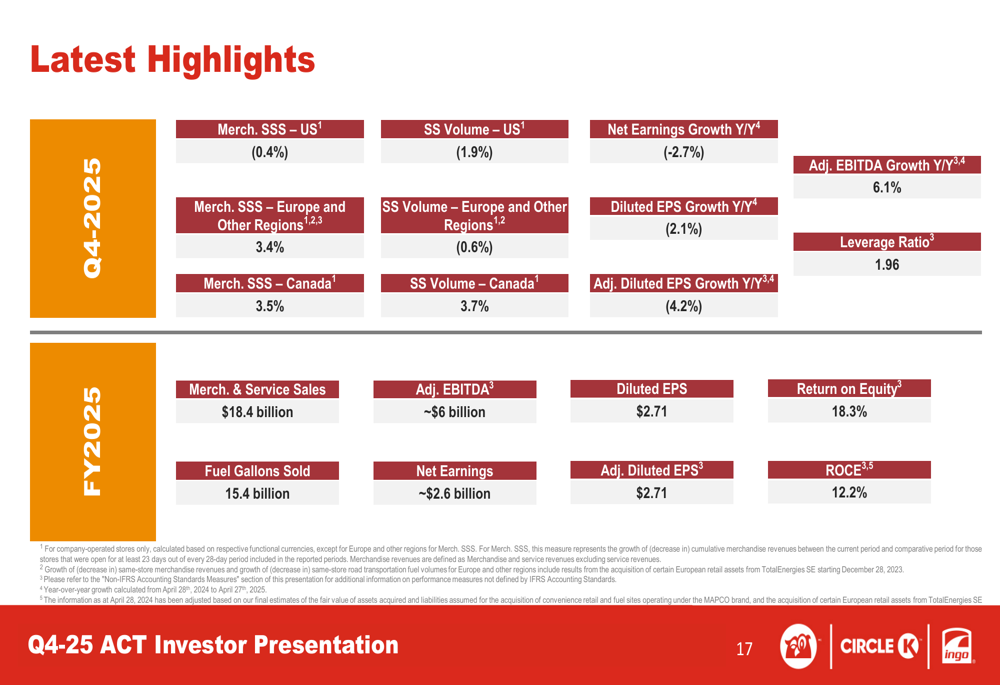

Couche-Tard’s Q4-FY25 results showed mixed performance across regions and categories. The company reported a 2.7% year-over-year decline in net earnings and a 2.1% decrease in diluted EPS for the quarter. However, adjusted EBITDA grew by 6.1% compared to the same period last year, indicating underlying operational improvements.

Same-store merchandise sales varied by region, with Canada showing the strongest growth at 3.5%, followed by Europe and other regions at 3.4%, while the US experienced a slight decline of 0.4%. Fuel volumes followed a similar pattern with Canada leading at 3.7% growth, while both the US and Europe saw declines of 1.9% and 0.6% respectively.

For the full fiscal year 2025, Couche-Tard reported:

- Merchandise & Service Sales: $18.4 billion

- Fuel Gallons Sold: 15.4 billion

- Adjusted EBITDA: ~$6 billion

- Net Earnings: ~$2.6 billion

- Diluted EPS: $2.71

- Return on Equity: 18.3%

- Return on Capital Employed: 12.2%

The following slide summarizes the company’s latest financial highlights:

Strategic Initiatives

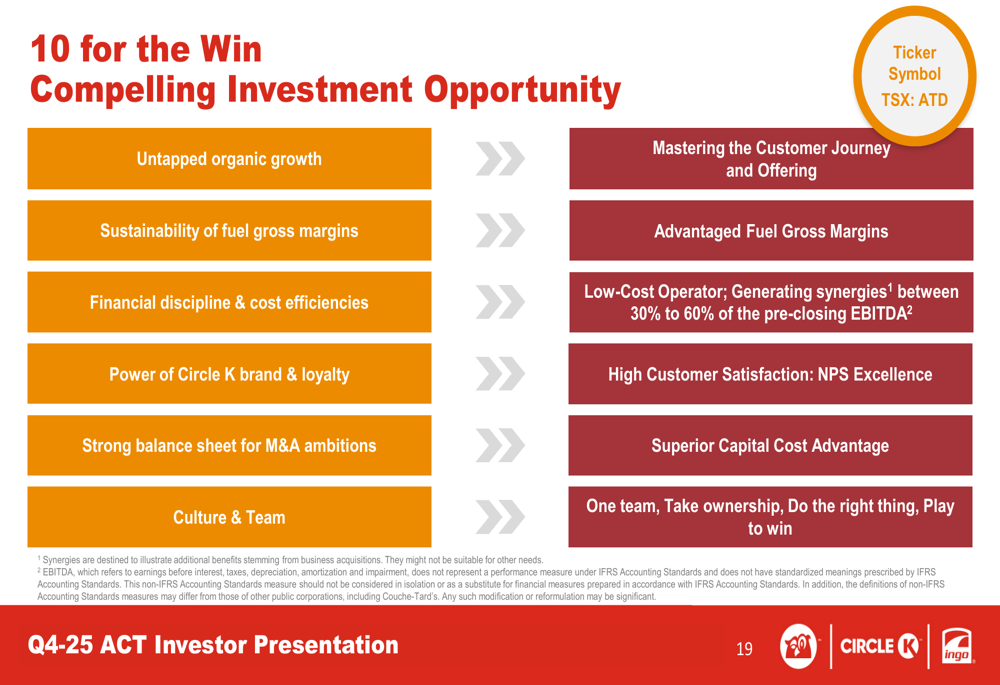

Couche-Tard’s presentation emphasized its "10 for the Win" strategic framework, which outlines the company’s approach to growth and value creation. The framework focuses on organic growth opportunities, fuel margin sustainability, financial discipline, brand power, and M&A capabilities.

As illustrated in this comprehensive strategic overview:

The company’s strategy is organized around four key pillars: Winning Offer, Winning Fuel, Winning the Customer, and Winning Growth. Each pillar contains specific initiatives designed to drive revenue and profit growth.

In the "Winning Offer" category, Couche-Tard is focusing heavily on food service expansion. The company has implemented its "Fresh Food, Fast" concept in approximately 6,000 sites globally and aims to generate an additional $150-200 million in EBITDA from food initiatives by FY2028.

The following slide details the company’s food strategy:

Similarly, the company’s "Own Thirst" initiative targets beverage sales growth through expanded cooler capacity and assortment optimization. Couche-Tard has already installed new cooler solutions in over 4,000 locations and projects this initiative will contribute approximately $250 million in EBITDA by FY2028.

As shown in this strategic overview of the beverage category:

Competitive Industry Position

Couche-Tard operates in a highly fragmented convenience store market, particularly in the United States where approximately 60% of stores are operated by single-store owners. This fragmentation presents significant consolidation opportunities for large players like Couche-Tard.

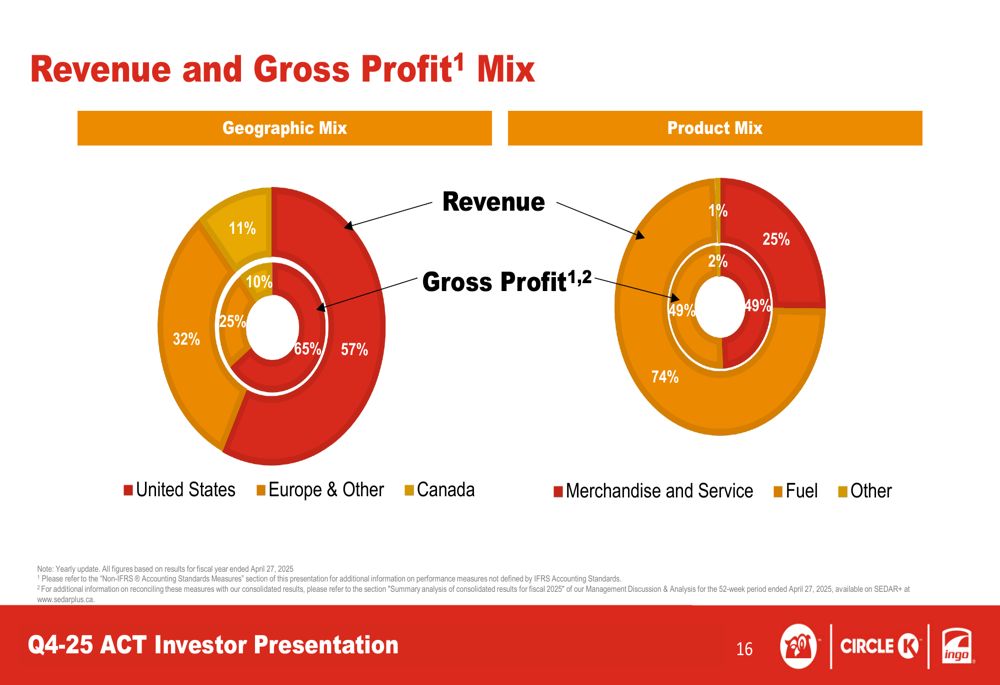

The company’s revenue and gross profit are diversified across geographic regions and product categories. The United States represents the largest portion of both revenue (65%) and gross profit (57%), followed by Europe and other regions, and Canada. From a product perspective, fuel generates 74% of revenue but only 25% of gross profit, highlighting the importance of merchandise and service offerings to the company’s profitability.

This breakdown of revenue and gross profit mix illustrates the company’s diversification:

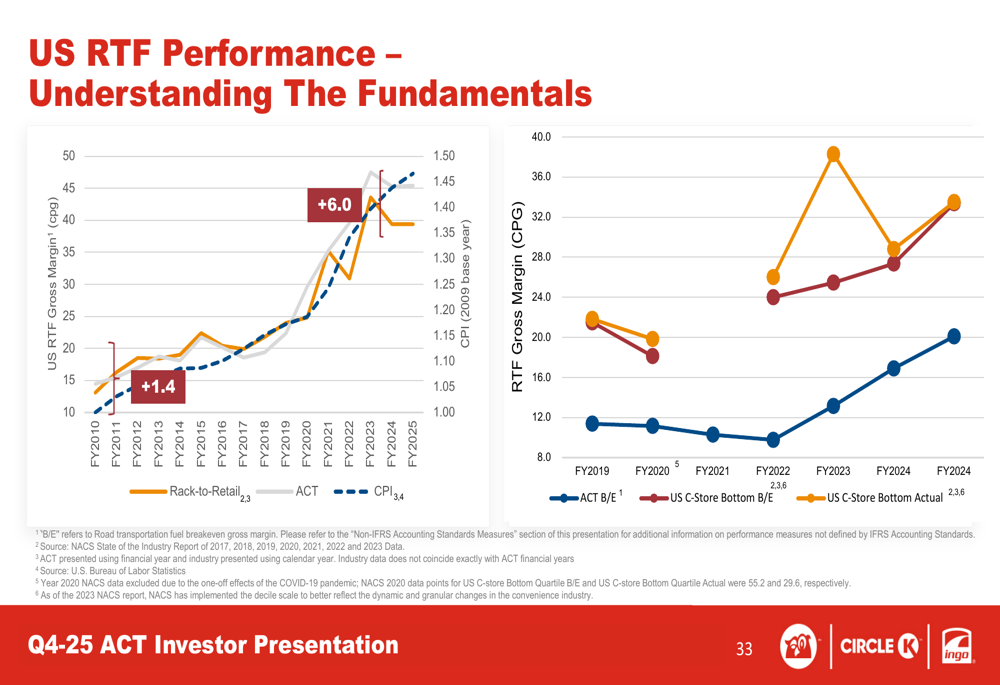

In the fuel segment, Couche-Tard has demonstrated resilience through economic cycles. The company’s presentation highlighted the correlation between fuel gross margins and operating expenses, suggesting that margin expansion has helped offset rising costs over time.

The following chart illustrates US road transportation fuel performance trends:

Forward-Looking Statements

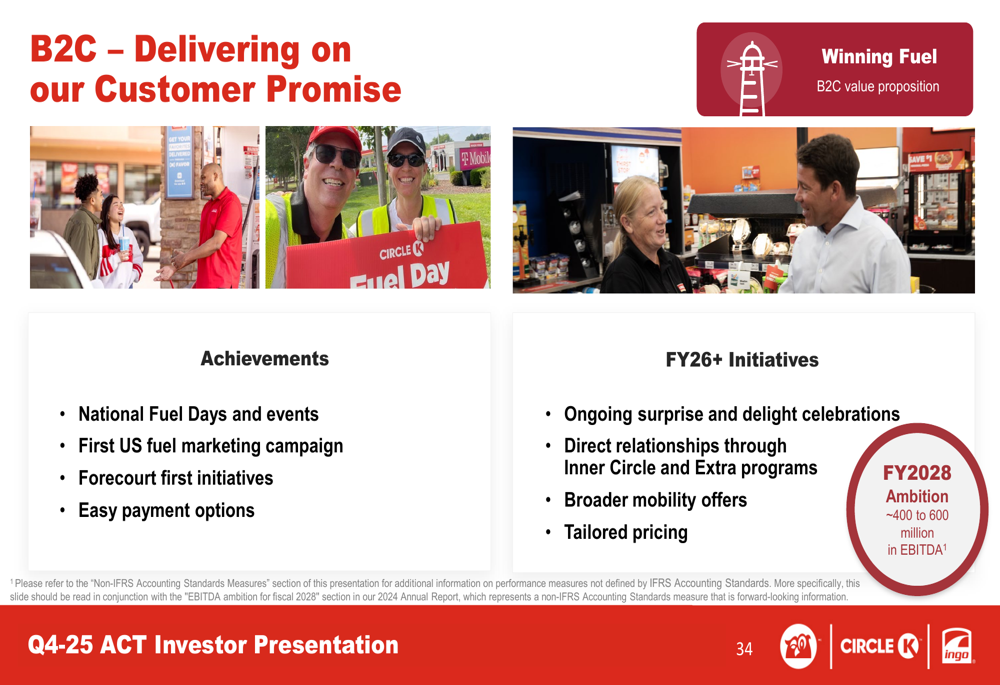

Couche-Tard outlined several customer-focused initiatives planned for FY26 and beyond, including national fuel promotion days, enhanced loyalty programs, forecourt improvements, and expanded mobility offerings. The company projects these initiatives could contribute $400-600 million in additional EBITDA.

As shown in this overview of customer-focused initiatives:

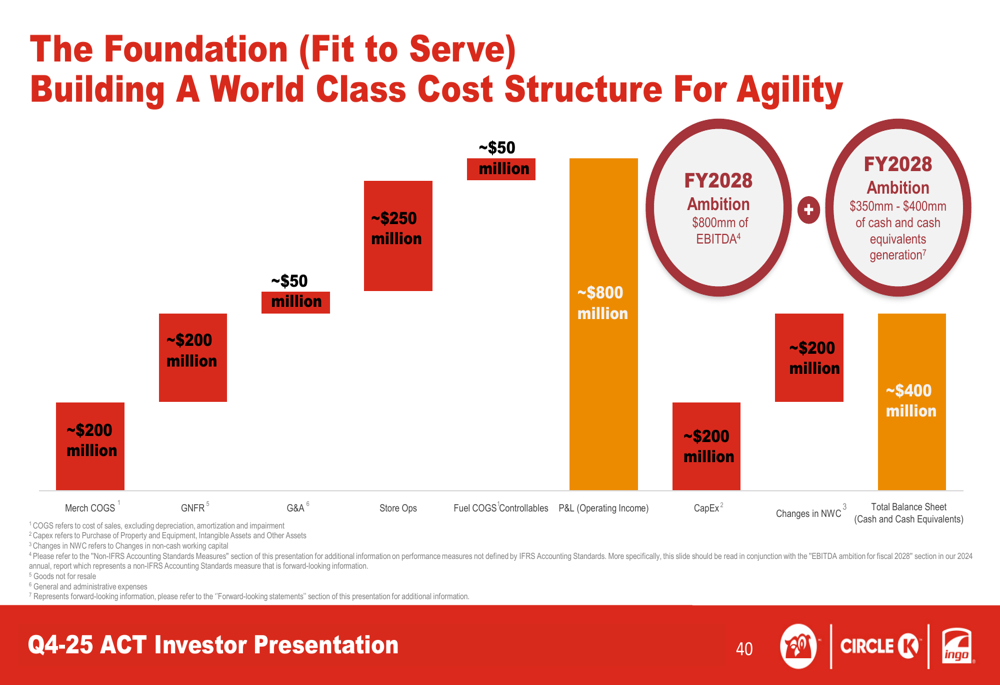

The company is also focusing on cost optimization through its "Fit to Serve" program, which targets improvements across merchandise cost of goods sold, non-merchandise procurement, general and administrative expenses, store operations, and fuel cost of goods sold. These efforts aim to build a "world class cost structure" to increase free cash flow.

The following slide outlines the company’s approach to cost optimization:

Couche-Tard continues to pursue growth through both organic expansion and acquisitions. The company noted that approximately 1,000 new store projects are in its pipeline, primarily new-to-industry locations. The presentation also highlighted recent acquisitions including TotalEnergies (EPA:TTEF) and MAPCO, reinforcing the company’s M&A strategy.

Analyst Perspectives

While the Q4-FY25 presentation showed some quarterly challenges with declining net earnings, the company’s full-year performance remained solid. The slight decline in US same-store merchandise sales (-0.4%) and fuel volumes (-1.9%) may indicate ongoing consumer spending pressures in the company’s largest market.

It’s worth noting that the Q4-FY25 results contrast with the Q3-FY25 performance reported earlier, where net earnings increased by 4.6% year-over-year to $641 million. This suggests a potential slowdown in the final quarter of the fiscal year.

Despite these quarterly fluctuations, Couche-Tard’s strategic initiatives demonstrate a clear focus on long-term growth through food service expansion, beverage optimization, fuel network enhancement, and digital customer engagement. The company’s healthy leverage ratio of 1.96 and strong return metrics (ROE of 18.3% and ROCE of 12.2%) provide financial flexibility to pursue both organic growth and acquisition opportunities in a fragmented market.

With the stock trading near $68.81 as of June 25, 2025, down 2.84% from its previous close, investors appear to be weighing the company’s long-term growth potential against near-term challenges in consumer spending and fuel volumes.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.