Bitcoin price today: slides below $100k, enters bear market amid valuation jitters

Introduction & Market Context

Alpek SAB De CV (BMV:ALPEKA) presented its third-quarter 2025 results on October 22, showing sequential improvement despite persistent industry headwinds. The Mexican petrochemical company reported a 10% quarter-over-quarter increase in comparable EBITDA to $137 million, though this figure remains 37% below the same period last year.

The company’s stock rose 2.96% following the presentation, suggesting investors responded positively to Alpek’s ability to navigate challenging market conditions. With a market capitalization of $1.09 billion, Alpek continues to face global oversupply pressures while making progress on operational efficiency and cash flow generation.

Quarterly Performance Highlights

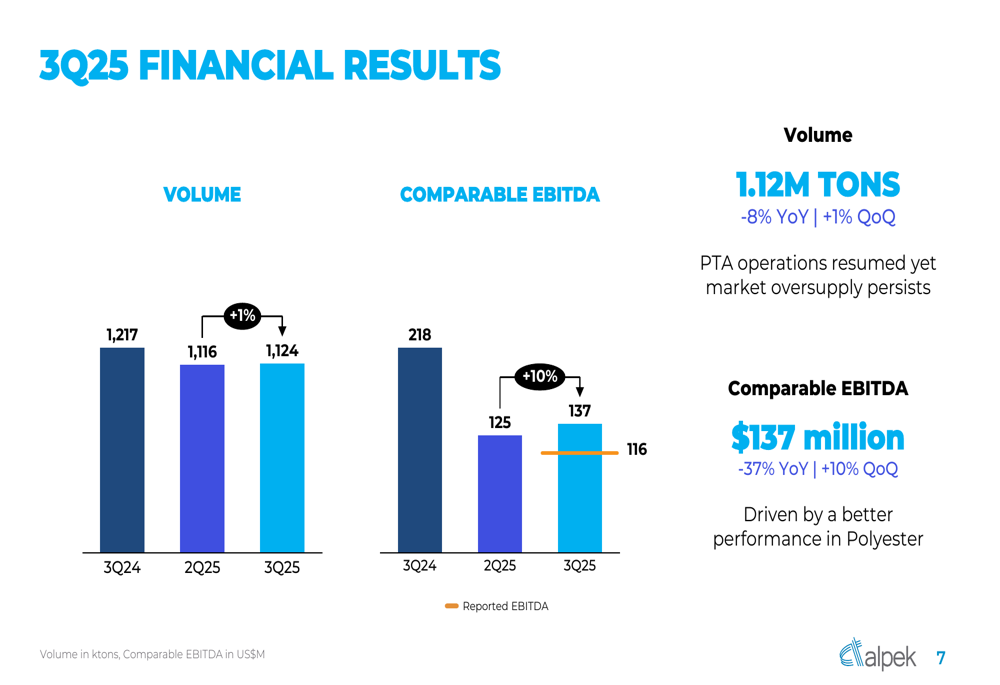

Alpek reported total volume of 1.12 million tons in Q3 2025, representing a 1% increase from the previous quarter but an 8% decline year-over-year. The company noted that while PTA operations have resumed, market oversupply continues to weigh on performance.

As shown in the following chart of quarterly financial results:

Comparable EBITDA reached $137 million, showing a 10% improvement quarter-over-quarter despite being down 37% compared to Q3 2024. This sequential growth was primarily driven by better performance in the Polyester segment, which benefited from improved product mix and operational cost efficiencies.

Segment Analysis

Polyester Segment

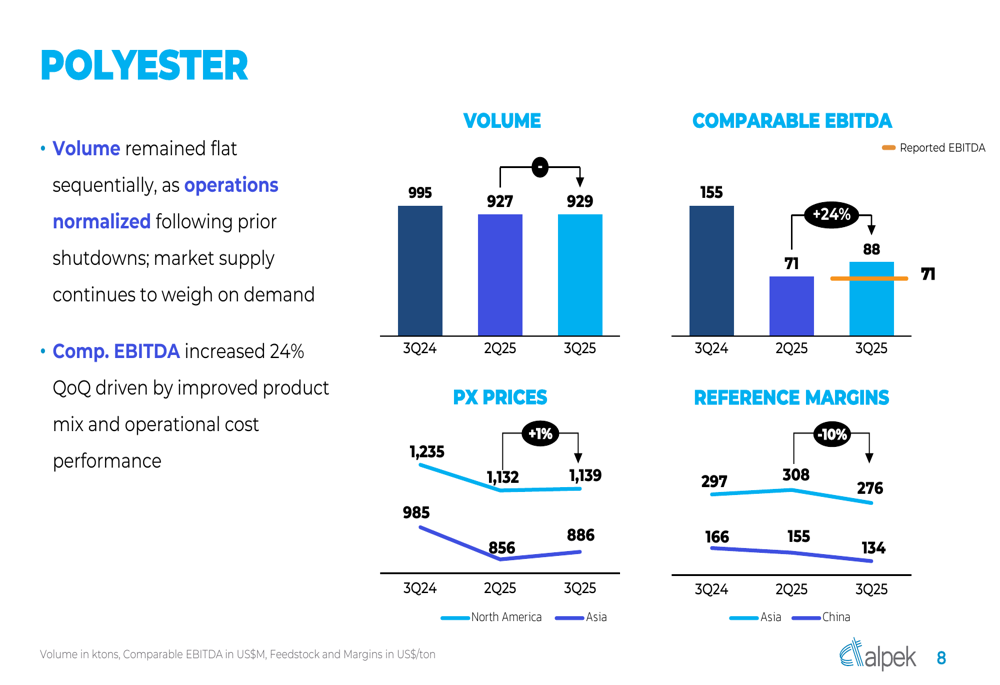

Alpek’s Polyester segment, which accounts for approximately 83% of total volume, showed signs of stabilization in Q3. Volume remained flat sequentially at 929,000 tons as operations normalized, though market supply continues to pressure demand.

The segment’s comparable EBITDA increased 24% quarter-over-quarter to $88 million, driven by improved product mix and operational cost performance. However, reference margins continued their downward trend, falling to $134 from $155 in the previous quarter.

The following chart illustrates the Polyester segment’s performance metrics:

Plastics & Chemicals Segment

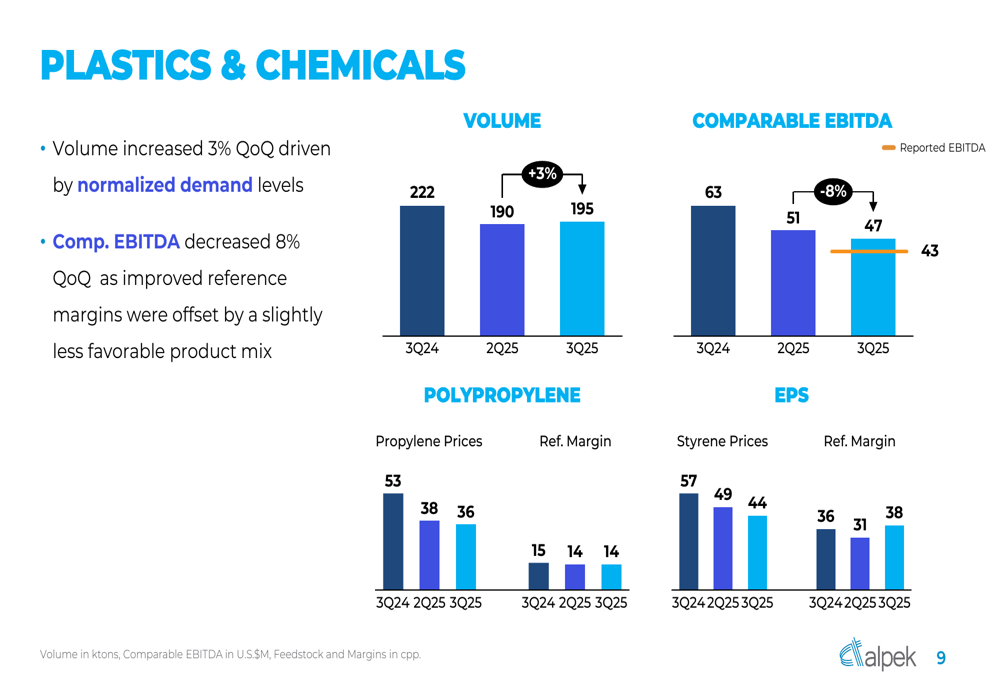

The Plastics & Chemicals segment showed mixed results in the third quarter. Volume increased 3% quarter-over-quarter to 195,000 tons, driven by normalized demand. However, comparable EBITDA decreased 8% to $47 million as improved reference margins were offset by a slightly less favorable product mix.

The following visualization details the performance of the Plastics & Chemicals segment:

The segment continues to face challenges from fluctuating raw material prices, with styrene prices declining to $44 in Q3 from $49 in Q2, while reference margins improved slightly from $31 to $38.

Financial Position and Cash Flow

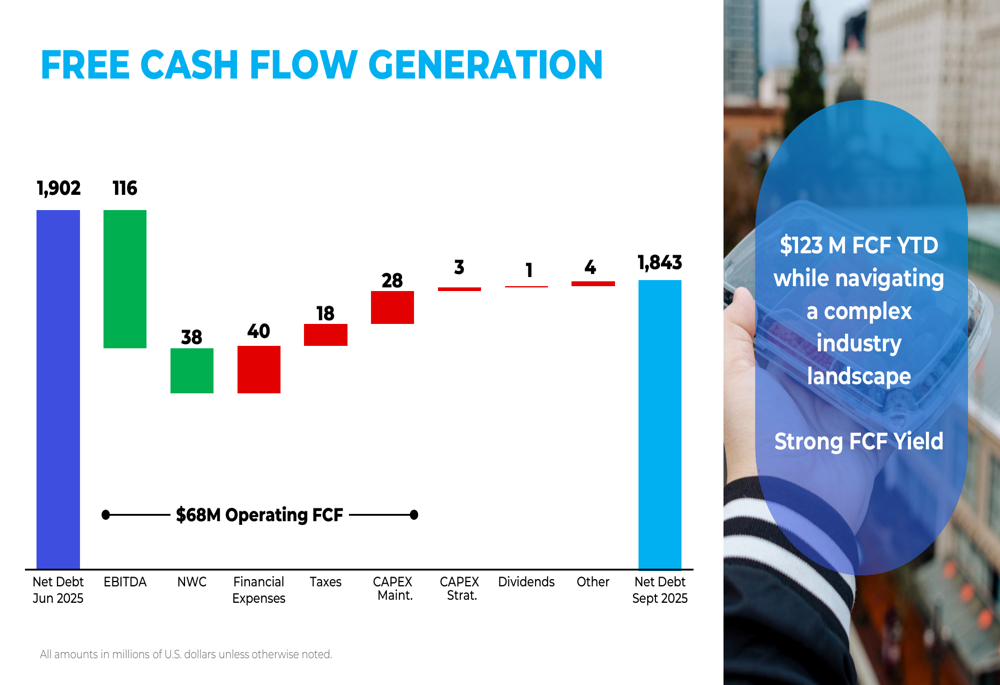

Alpek demonstrated strong cash generation capabilities during the quarter, reporting $68 million in operating free cash flow, a 41% improvement from the previous quarter. Year-to-date free cash flow reached $123 million, which the company characterized as strong performance while navigating a complex industry landscape.

The following waterfall chart details Alpek’s cash flow generation:

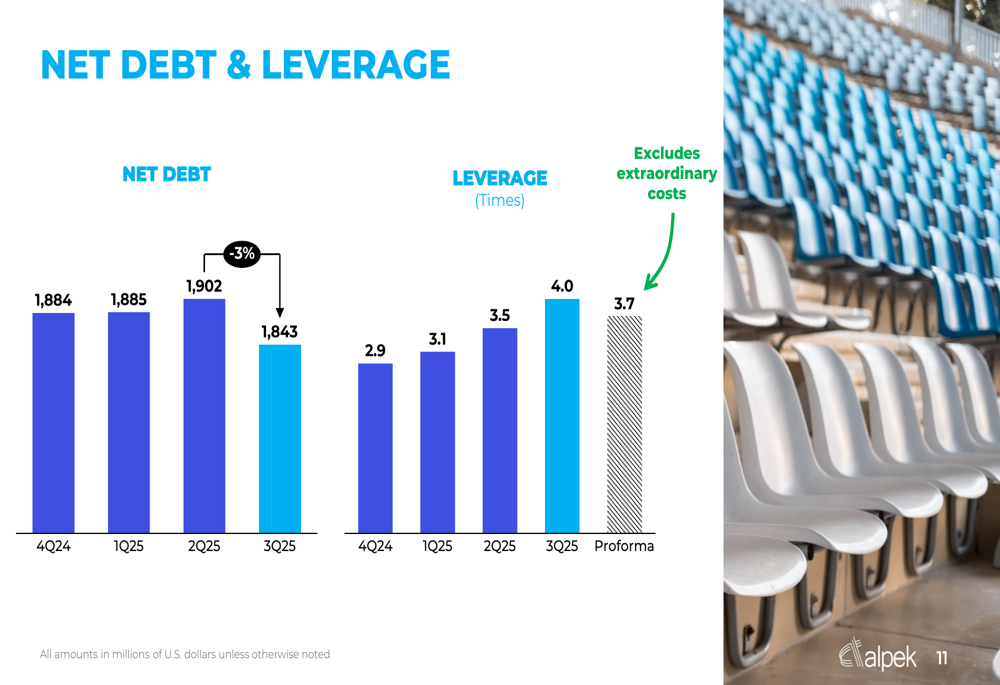

The company continued its deleveraging efforts, reducing net debt from $1,902 million in June 2025 to $1,843 million by the end of September. Despite this progress, Alpek’s leverage ratio increased to 4.0x in Q3, up from 3.5x in the previous quarter, though the proforma leverage excluding extraordinary costs stands at 3.7x.

The following chart shows Alpek’s net debt and leverage trends:

Forward-Looking Statements

During the earnings call, CEO Jorge Young emphasized the company’s strategic focus, stating, "We are bracing for a tough cycle and for actions on having the right footprint." This suggests Alpek is preparing for continued industry challenges while optimizing its operational structure.

CFO José Carlos Pons highlighted financial priorities, noting, "We expect to continue deleveraging throughout 2026." The company has revised its full-year comparable EBITDA guidance to $500 million, reflecting cautious optimism amid market challenges.

Alpek anticipates potential benefits from U.S. PET import tariffs in 2026-2027, which could provide some relief from the current market oversupply situation. However, the company expects lower demand in Q4 due to seasonal factors, which may temporarily impact performance before these potential regulatory benefits materialize.

With an attractive free cash flow yield of 20% and a dividend yield of 11.51%, Alpek maintains strong cash generation capabilities despite the challenging market environment, positioning the company to weather the current industry downturn while preparing for eventual market recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.