Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Alpha Teknova Inc. (NASDAQ:TKNO) presented its first quarter 2025 financial results on May 8, 2025, showing improved profitability metrics despite mixed revenue performance. The company’s stock, which closed at $5.99, gained 2.98% in after-hours trading to reach $6.56, suggesting investor optimism about the company’s financial trajectory.

Quarterly Performance Highlights

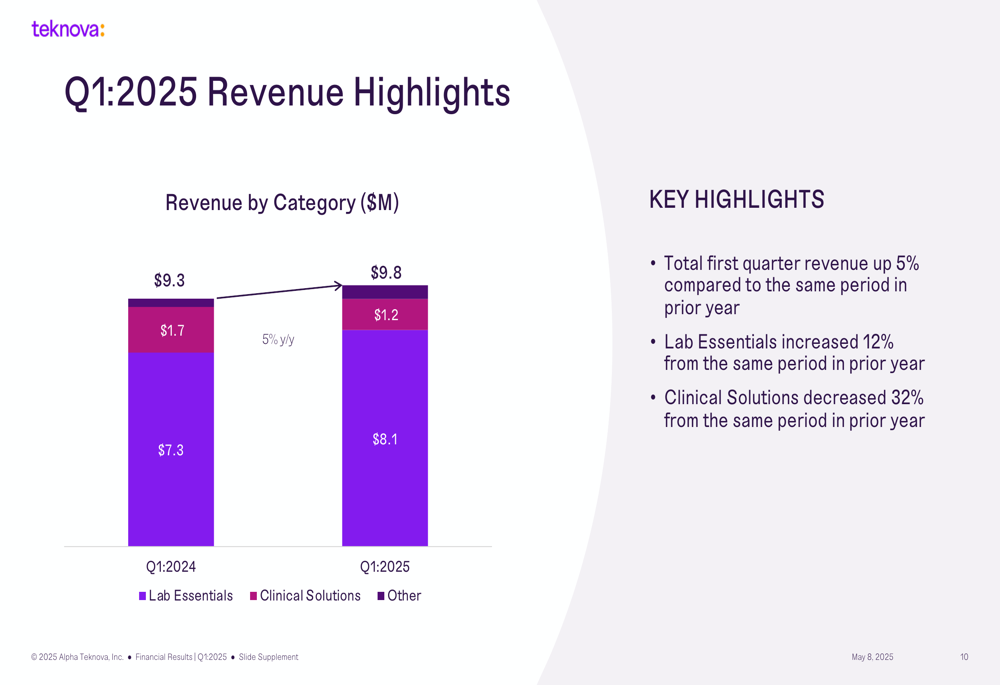

Teknova reported total revenue of $9.8 million for Q1 2025, representing a 5% increase compared to the same period last year. This growth was driven primarily by the Lab Essentials segment, which grew 12% year-over-year to $8.1 million. However, the Clinical Solutions segment experienced a 32% decline to $1.2 million compared to Q1 2024.

As shown in the following revenue breakdown chart:

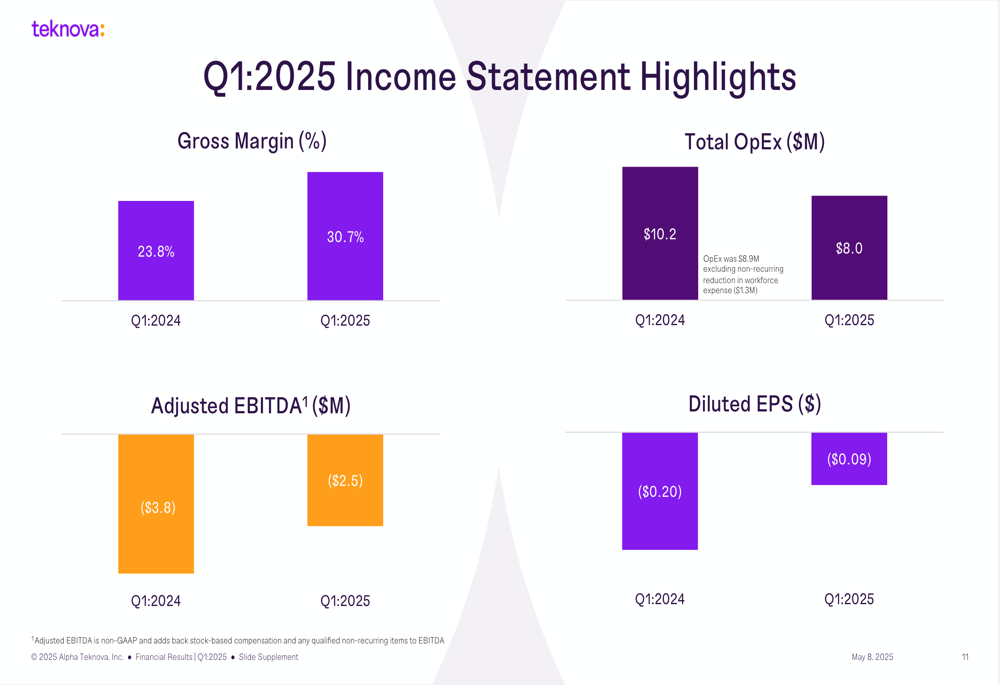

Despite the mixed revenue performance, Teknova demonstrated significant improvement in profitability metrics. Gross margin expanded substantially from 23.8% in Q1 2024 to 30.7% in Q1 2025, reflecting the company’s focus on operational efficiency and higher-margin products.

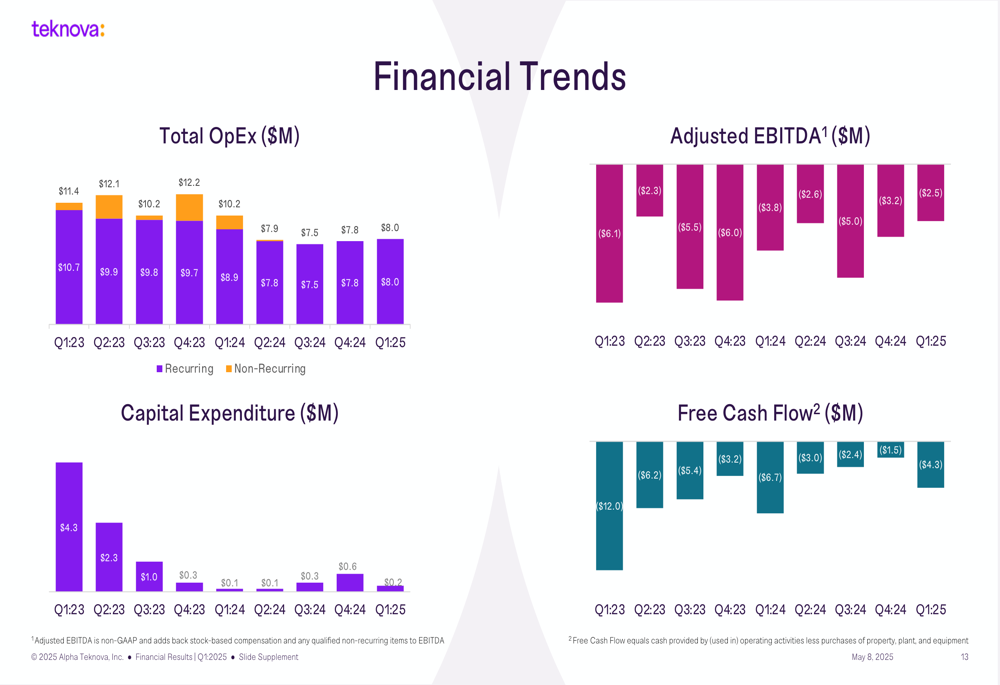

The company also made progress in controlling expenses, with total operating expenses decreasing from $10.2 million in Q1 2024 to $8.0 million in Q1 2025. This reduction excludes a $1.3 million non-recurring workforce reduction expense incurred in Q1 2024.

These improvements translated to better bottom-line performance, with adjusted EBITDA improving from -$3.8 million to -$2.5 million and diluted EPS improving from -$0.20 to -$0.09 year-over-year, as illustrated in the following chart:

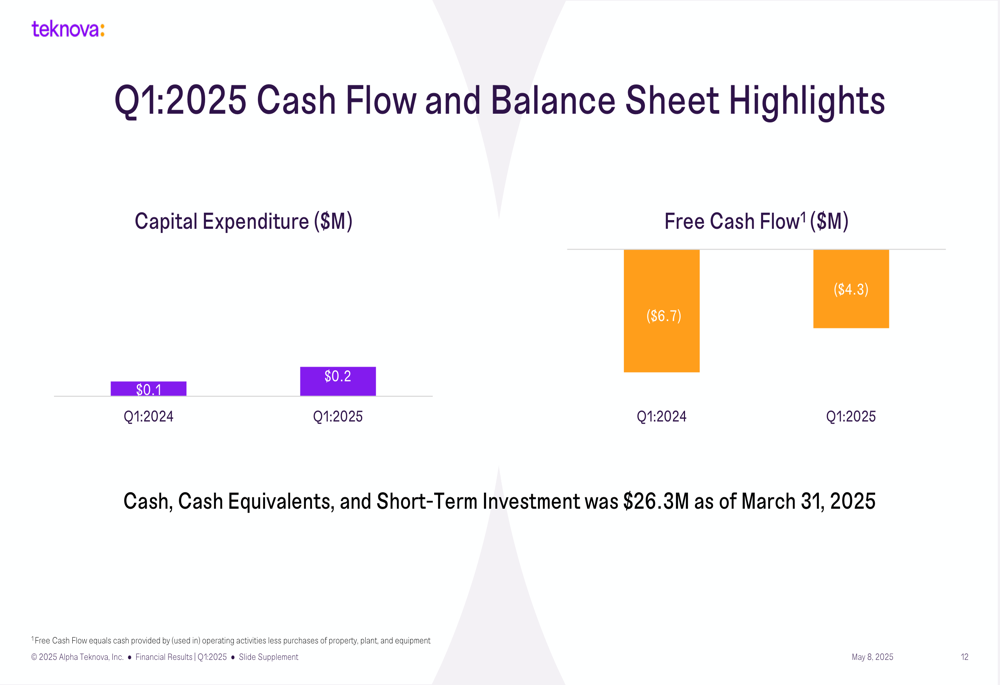

Cash management also showed improvement, with free cash flow of -$4.3 million in Q1 2025 compared to -$6.7 million in Q1 2024. The company reported $26.3 million in cash, cash equivalents, and short-term investments as of March 31, 2025.

Strategic Initiatives

Teknova’s presentation highlighted its strategic evolution, which is now entering what the company calls its "Scale" phase after periods of establishment (1996-2016) and investment (2017-2023). The company aims to achieve sustainable above-market revenue growth and become a partner of choice for emerging therapies like cell and gene therapy.

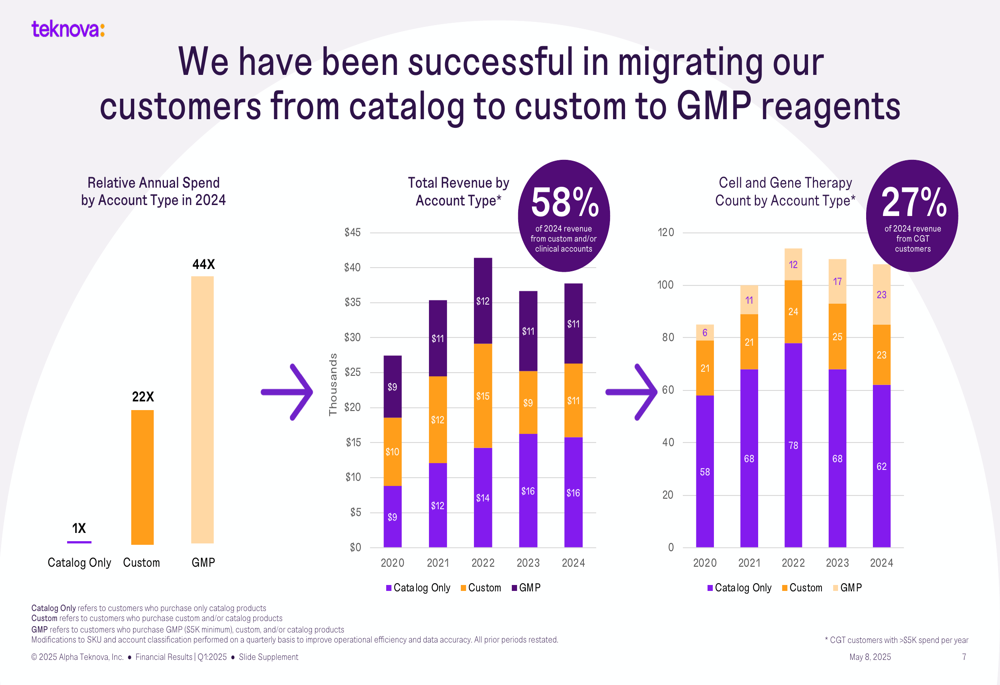

A key element of Teknova’s strategy is migrating customers from catalog-only purchases to higher-value custom and GMP reagents. Data presented shows that GMP customers spend 44 times more than catalog-only customers, while custom customers spend 22 times more. The company reported that 58% of its 2024 revenue came from custom and/or clinical accounts, with 27% specifically from cell and gene therapy customers.

As illustrated in the customer migration chart:

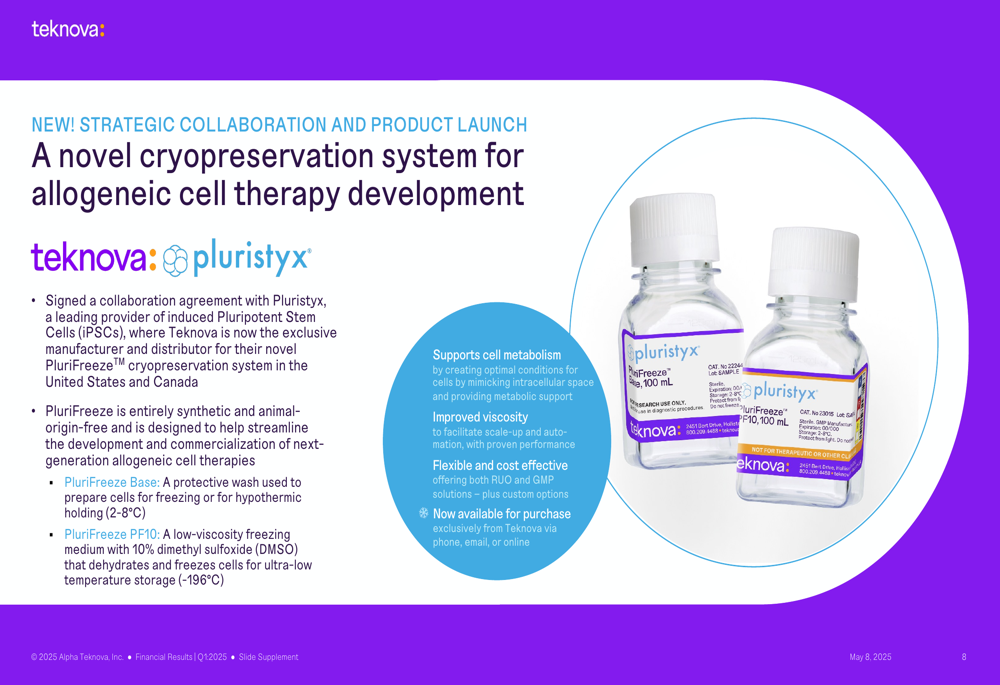

Teknova also announced a strategic collaboration with Pluristyx, becoming the exclusive manufacturer and distributor for the PluriFreeze cryopreservation system in the United States and Canada. This system is designed for allogeneic cell therapy development and features synthetic, animal-origin-free formulations that come in two forms: PluriFreeze Base (a protective wash) and PluriFreeze PF10 (a low-viscosity freezing medium).

Forward-Looking Statements

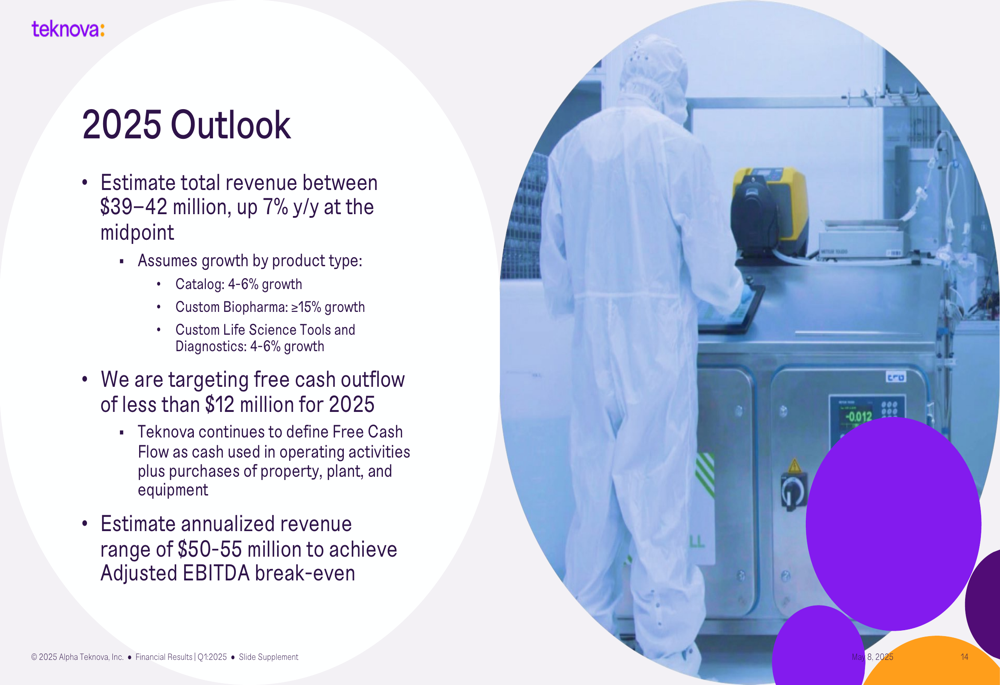

For full-year 2025, Teknova projects total revenue between $39-42 million, representing a 7% year-over-year increase at the midpoint. This outlook assumes different growth rates across product categories: 4-6% growth for catalog products, at least 15% growth for custom biopharma products, and 4-6% growth for custom life science tools and diagnostics.

The company is targeting free cash outflow of less than $12 million for 2025, continuing its trend of reducing cash burn. Teknova estimates it will achieve adjusted EBITDA break-even at an annualized revenue range of $50-55 million, suggesting the company is still a few quarters away from profitability at current growth rates.

Financial trends over the past two years show consistent improvement in operating expenses and adjusted EBITDA, along with reduced capital expenditures as the company completes its investment phase and focuses on scaling operations.

Competitive Industry Position

Teknova’s strategic positioning focuses on serving high-growth areas in the life sciences, particularly cell and gene therapy. The company’s 2024 revenue breakdown shows that approximately 60% came from catalog products, 35% from custom products (with biopharma representing 70% of custom revenue), and 5% from other sources including services and shipping.

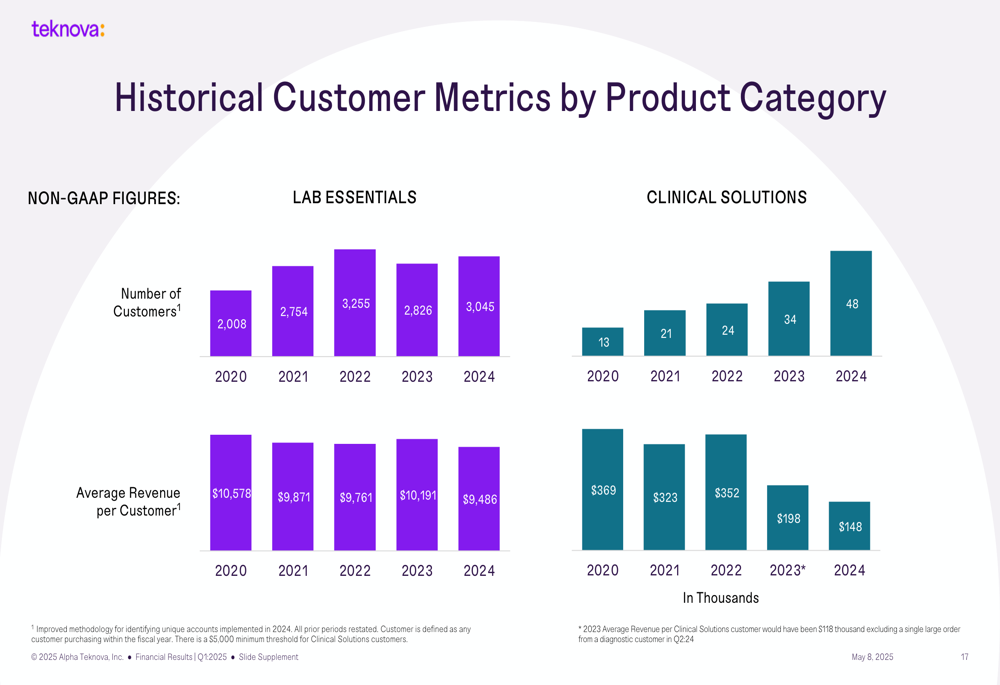

The company’s historical customer metrics reveal growth in both Lab Essentials and Clinical Solutions customer bases, with Lab Essentials customers increasing from 2,008 in 2020 to 3,045 in 2024. However, average revenue per customer in Clinical Solutions has declined from $359,000 in 2020 to $168,000 in 2024, suggesting a broadening of the customer base but potentially smaller initial orders.

Alpha Teknova’s Q1 2025 results demonstrate progress in its financial transformation, with improved profitability metrics despite mixed revenue performance. The company’s strategic focus on higher-value custom and GMP customers appears to be yielding results, though the path to profitability still requires continued revenue growth and operational efficiency. Investors will be watching to see if Teknova can maintain its margin improvements while accelerating growth in its strategic focus areas.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.