Microvast Holdings announces departure of chief financial officer

Alphabet Inc. (NASDAQ:GOOGL) presented its second quarter 2025 earnings results on July 23, showcasing robust financial performance that exceeded analyst expectations. The technology giant reported a 14% year-over-year revenue increase to $96.43 billion and a 22% rise in earnings per share to $2.31, surpassing the forecasted $2.17. Following the announcement, Alphabet’s stock saw a modest increase of 0.57% in after-hours trading, closing at $193.20.

Quarterly Performance Highlights

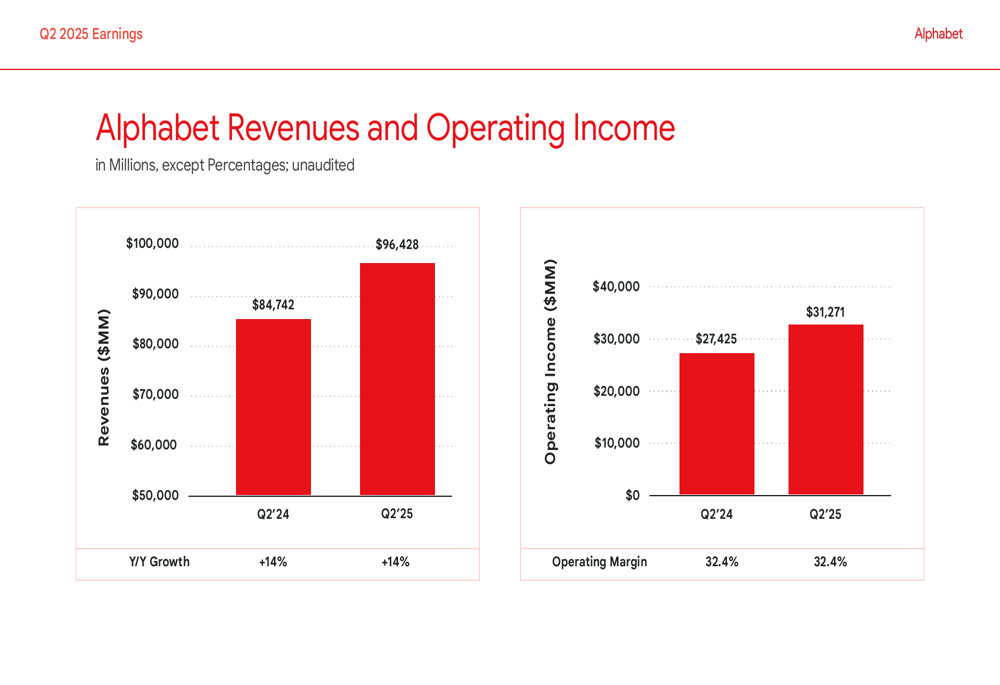

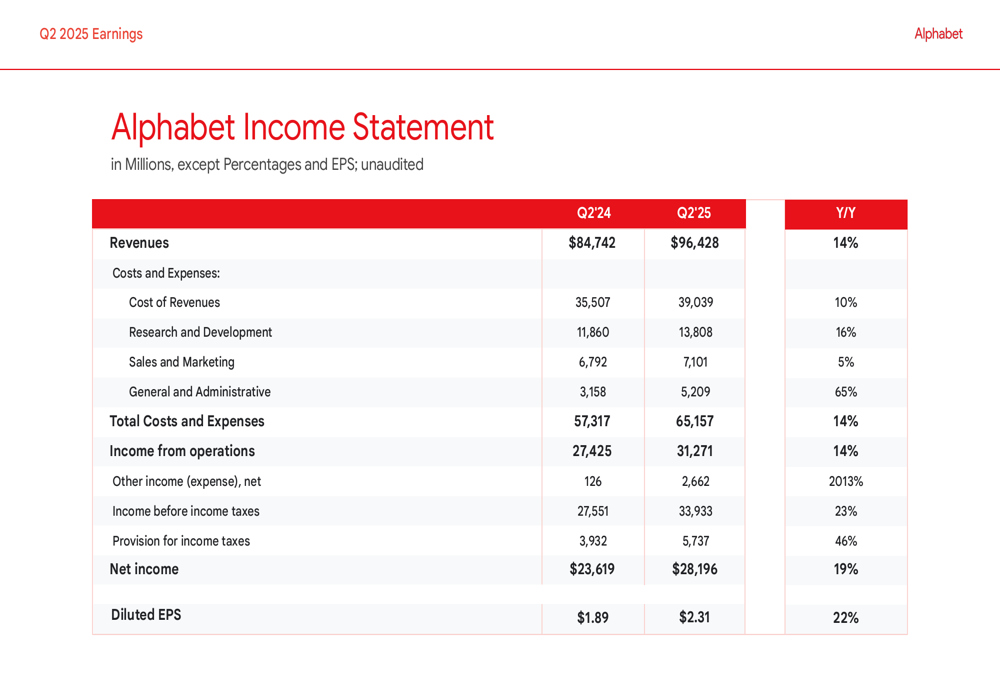

Alphabet delivered strong financial results across most business segments in Q2 2025. The company’s consolidated revenue reached $96.43 billion, representing a 14% increase compared to the same period last year. Net income grew by 19% year-over-year to $28.2 billion, while diluted earnings per share jumped 22% to $2.31.

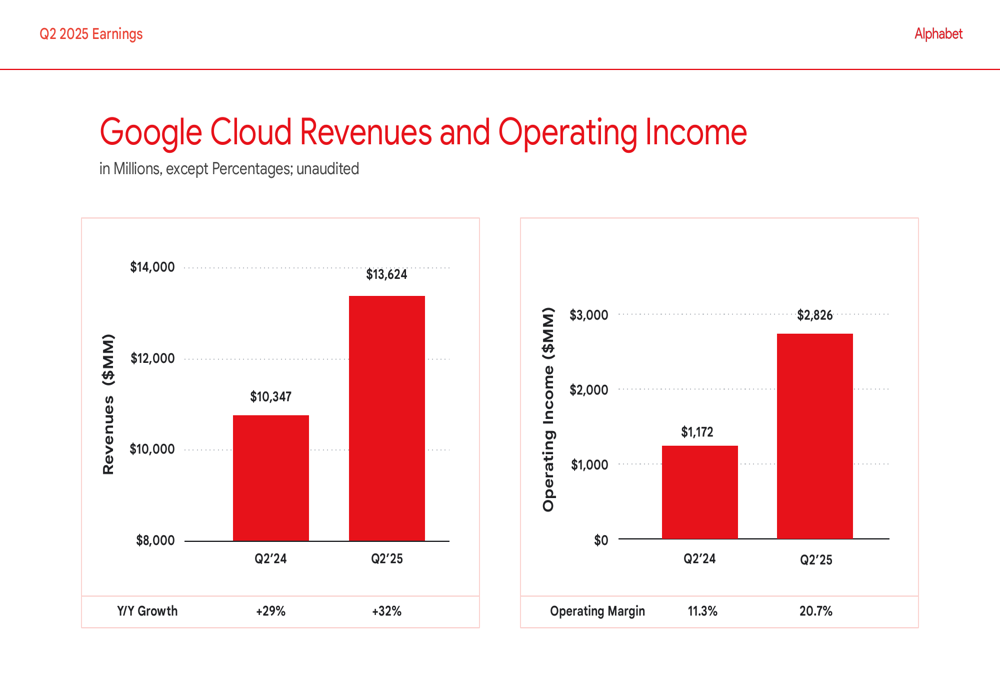

As shown in the following chart comparing revenues and operating income between Q2 2024 and Q2 2025:

Operating income increased by 14% year-over-year to $31.27 billion, maintaining a consistent operating margin of 32.4%. This stability in margin is particularly notable given the company’s significant investments in various growth initiatives, especially in artificial intelligence infrastructure.

Detailed Financial Analysis

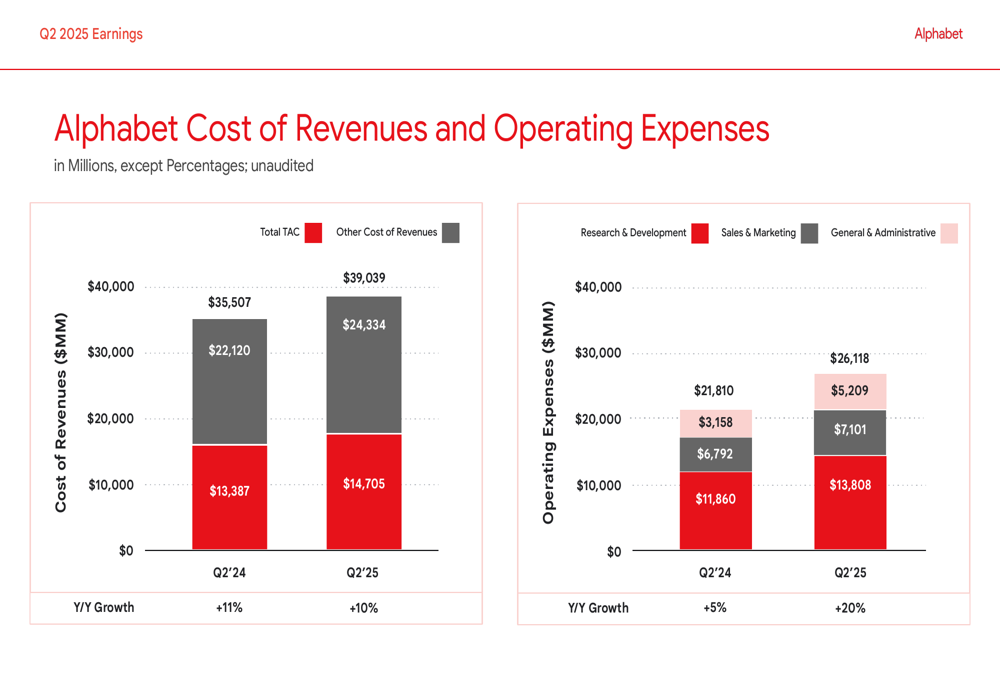

Alphabet’s income statement reveals strong performance across key metrics, with revenue growth outpacing the increase in costs and expenses. The company’s cost of revenues grew by 10% year-over-year, while total costs and expenses increased by 14%, in line with revenue growth.

The breakdown of operating expenses shows varying growth rates across different categories. Research and development expenses increased by 16% year-over-year to $13.81 billion, reflecting continued investment in innovation. Sales and marketing expenses grew modestly by 5% to $7.10 billion. The most significant increase was in general and administrative expenses, which surged by 65% to $5.21 billion.

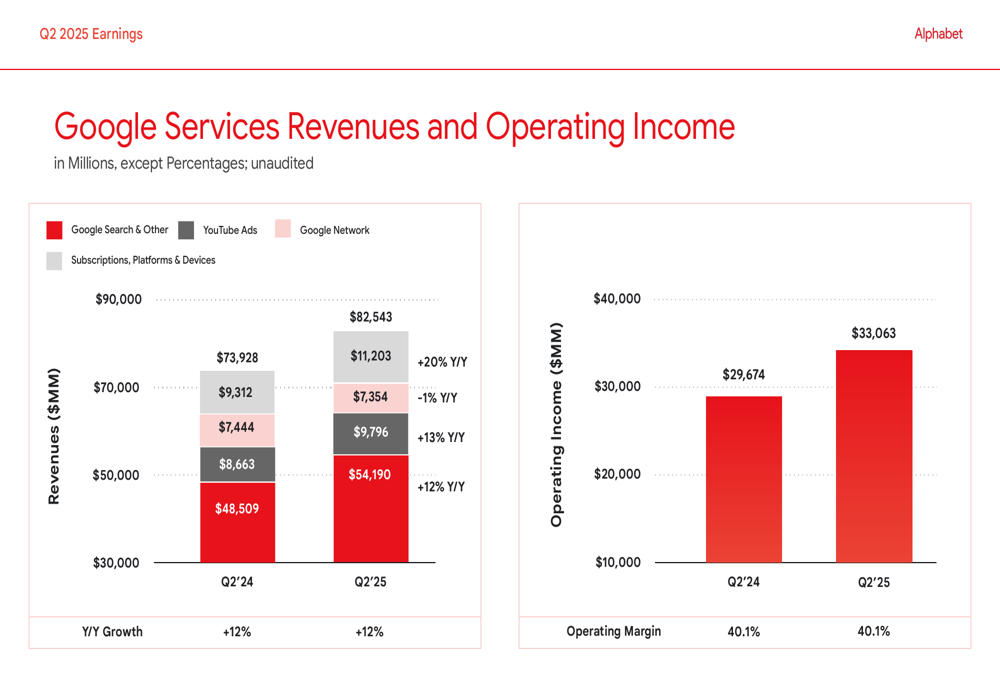

Google Services, which includes Search, YouTube, and other advertising businesses, continues to be Alphabet’s primary revenue driver. This segment generated $82.54 billion in revenue, up 11% year-over-year, and maintained a robust operating margin of 40.1%.

Google Cloud’s Standout Performance

Google Cloud emerged as a standout performer in Q2 2025, with revenue surging 32% year-over-year to $13.62 billion. More impressively, Cloud’s operating income more than doubled to $2.83 billion, with operating margin expanding significantly from 11.3% to 20.7% year-over-year.

This remarkable improvement in Cloud profitability demonstrates Alphabet’s successful execution in scaling its cloud business and competing effectively against industry leaders Amazon (NASDAQ:AMZN) Web Services and Microsoft (NASDAQ:MSFT) Azure. The strong performance aligns with CEO Sundar Pichai’s statement from the earnings call that "AI is positively impacting every part of the business, driving strong momentum."

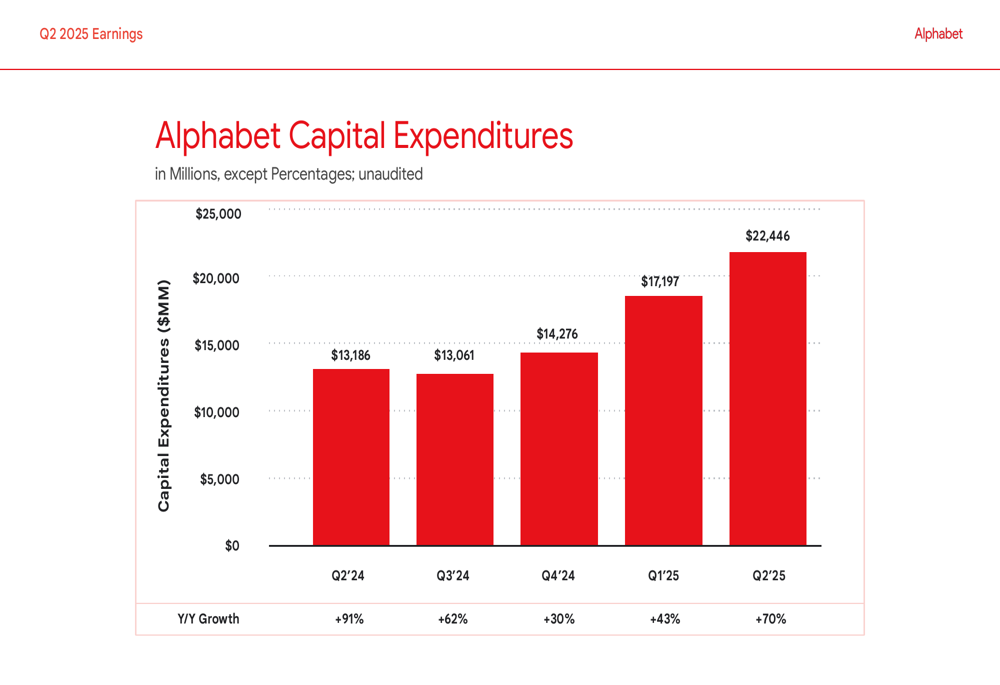

Capital Expenditure Strategy

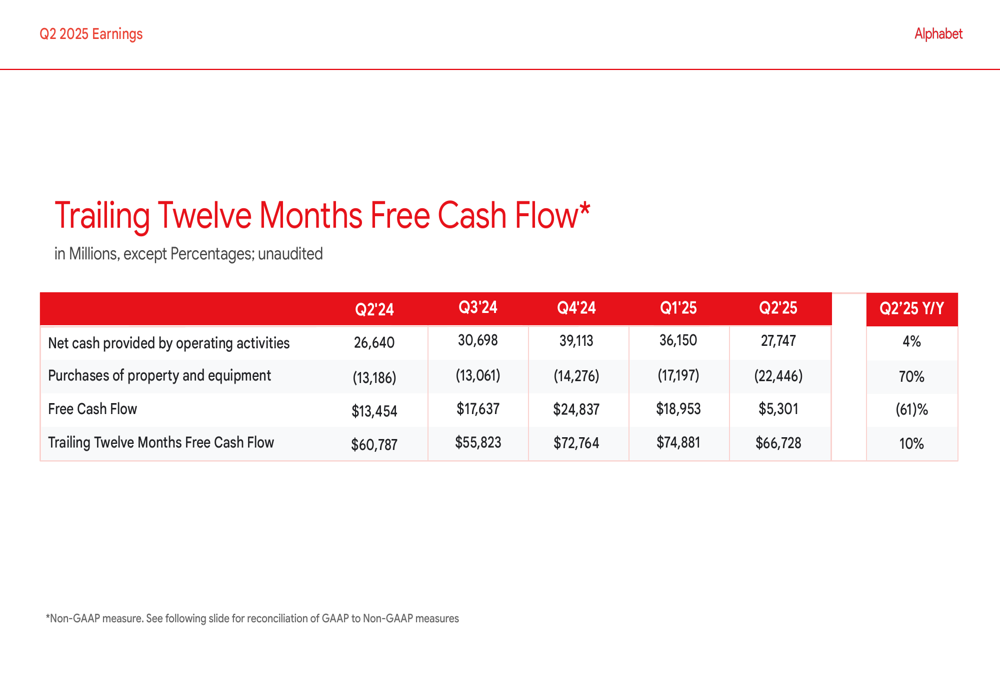

One of the most notable aspects of Alphabet’s Q2 results is the dramatic increase in capital expenditures, which rose 70% year-over-year to $22.45 billion. This represents the fifth consecutive quarter of significant capital investment growth.

The substantial increase in capital spending has impacted Alphabet’s quarterly free cash flow, which declined 61% year-over-year to $5.30 billion in Q2 2025. However, the trailing twelve months free cash flow remains healthy at $66.73 billion, up 10% compared to the previous year.

According to the earnings call, Alphabet has raised its capital expenditure outlook to $85 billion for 2025, focusing primarily on AI infrastructure and server investments. This aggressive investment strategy reflects the company’s commitment to maintaining its competitive position in the rapidly evolving AI landscape.

Forward-Looking Statements

Alphabet’s presentation suggests continued focus on AI development and cloud infrastructure expansion. The company anticipates tight cloud capacity supply to continue into 2026, necessitating sustained investment in infrastructure. Management expects 2026 to be a breakthrough year for "agentic experiences," which are projected to drive significant revenue growth.

While the company maintains a positive outlook, several challenges remain on the horizon. These include cloud capacity constraints that may limit growth potential, increasing competition in AI and cloud services from other tech giants, and potential regulatory challenges in key markets. Additionally, YouTube Ads revenue showed a slight decline of 1% year-over-year, potentially indicating competitive pressures in the video streaming space.

Despite these challenges, Alphabet’s strong financial position, with a market capitalization of $2.34 trillion and robust cash flows, positions the company well to navigate the competitive landscape while continuing to invest in future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.