Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

Ameresco, Inc. (NYSE:AMRC) released its Q1 2025 supplemental information on May 5, 2025, highlighting operational progress and financial results amid ongoing market challenges. The renewable energy solutions provider continues to expand its asset portfolio and project backlog, even as its stock trades significantly below its 52-week high of $39.68, closing at $12.00 with a 3.42% decline on the day. After-hours trading showed some recovery with a 5.87% gain to $12.27.

The company’s presentation emphasized its diversified business model spanning projects, recurring revenue streams, and services, positioning Ameresco to capitalize on the growing demand for clean energy solutions while building long-term value through its owned assets.

Quarterly Performance Highlights

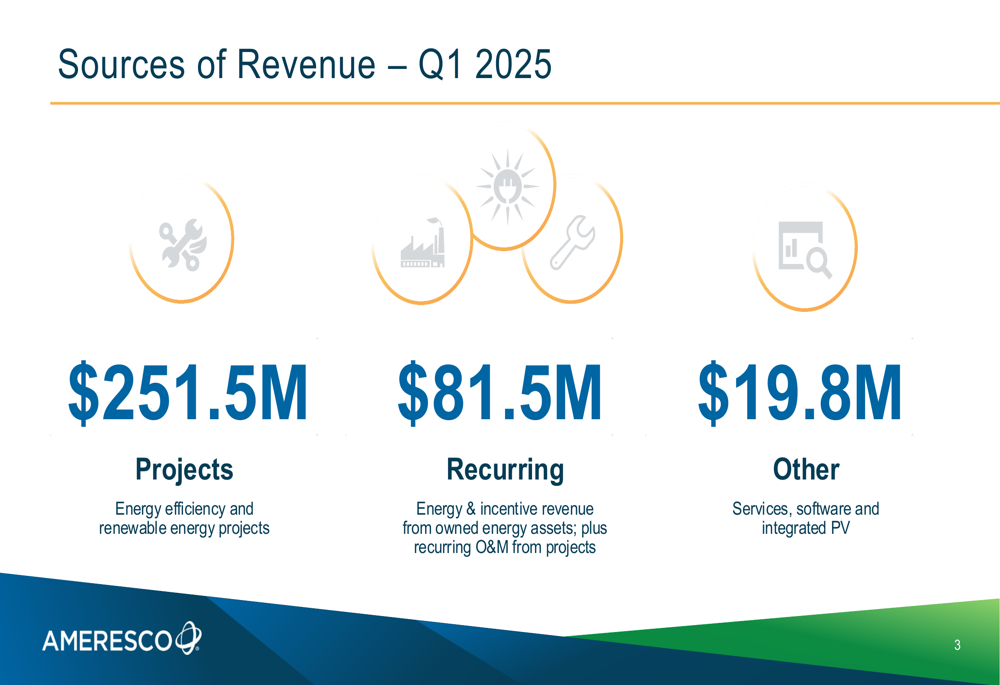

For Q1 2025, Ameresco reported total revenue of $353 million, with the majority coming from its projects segment. The revenue breakdown shows a business model that balances immediate project revenue with growing recurring income streams.

As shown in the following revenue breakdown chart:

Projects contributed $251.5 million (71% of total revenue), while recurring revenue sources generated $81.5 million from energy assets and operations & maintenance (O&M) services. Other revenue, including integrated PV, software, and services, added $19.8 million.

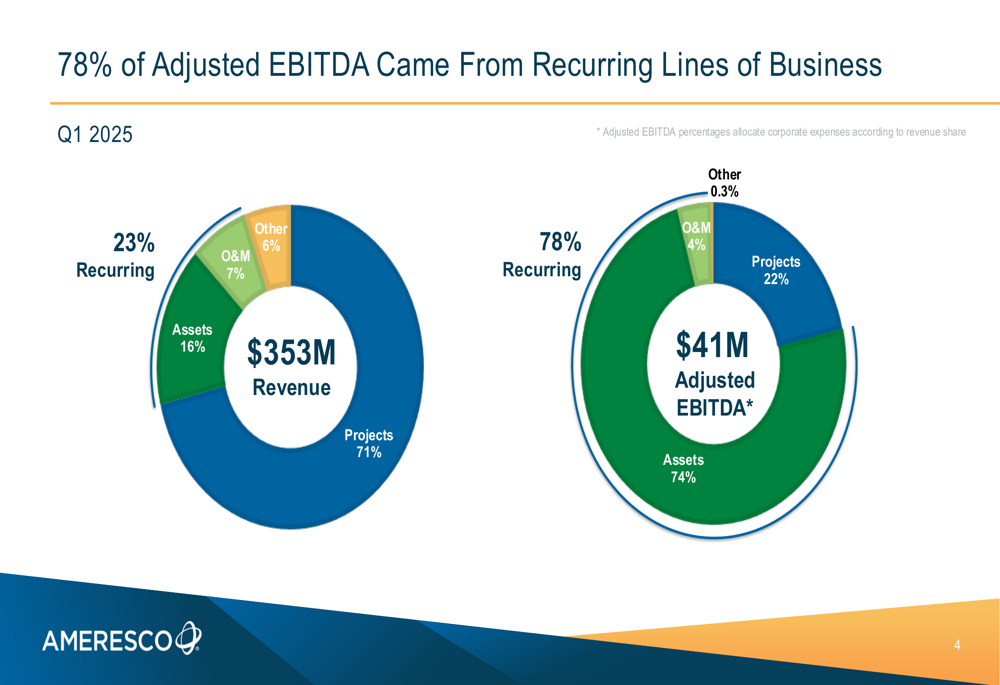

While projects dominate revenue generation, Ameresco’s adjusted EBITDA tells a different story about profitability sources. The company reported $41 million in adjusted EBITDA for Q1 2025, with a significant portion derived from its recurring business lines.

The following chart illustrates this important distinction between revenue and profit sources:

Energy assets contributed 74% of adjusted EBITDA despite representing only 16% of revenue, demonstrating the high-margin nature of Ameresco’s owned renewable energy facilities. Projects, while representing 71% of revenue, accounted for just 22% of adjusted EBITDA.

Detailed Financial Analysis

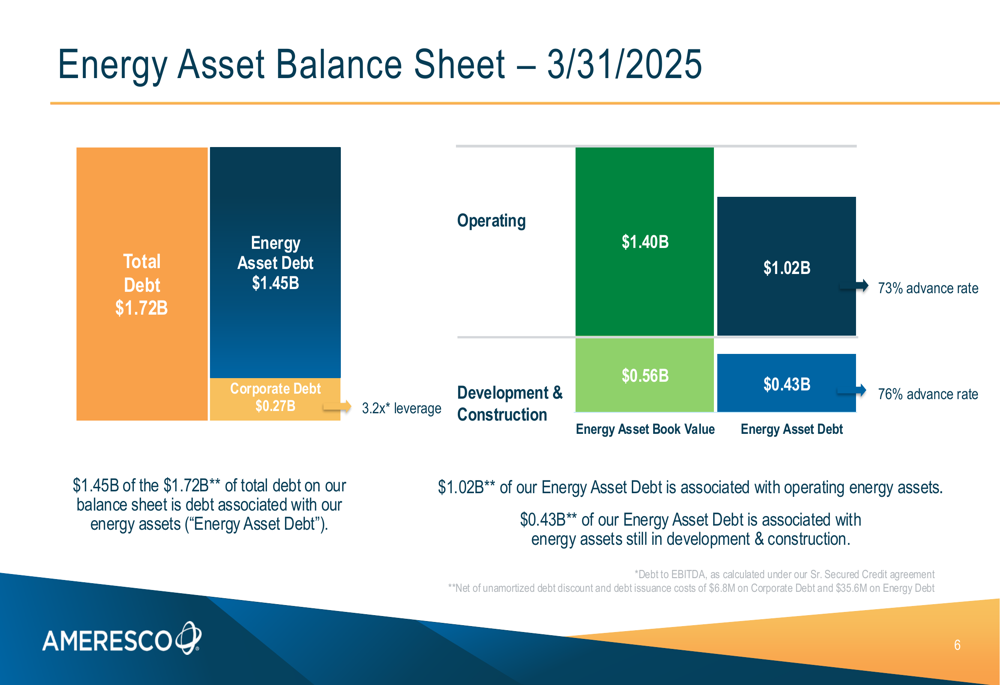

Ameresco’s financial position reflects its capital-intensive business model, with significant investments in energy assets balanced by project-based cash flow. The company’s total debt stands at $1.72 billion, primarily tied to its energy asset portfolio.

The debt structure is illustrated in this breakdown:

Of the total debt, $1.45 billion is directly related to energy assets, with $1.02 billion financing operating assets and $0.43 billion supporting assets under development. Corporate debt accounts for the remaining $0.27 billion. The company maintains a leverage ratio of 3.2x, with energy asset debt carrying advance rates of 73% for operating assets and 76% for development projects.

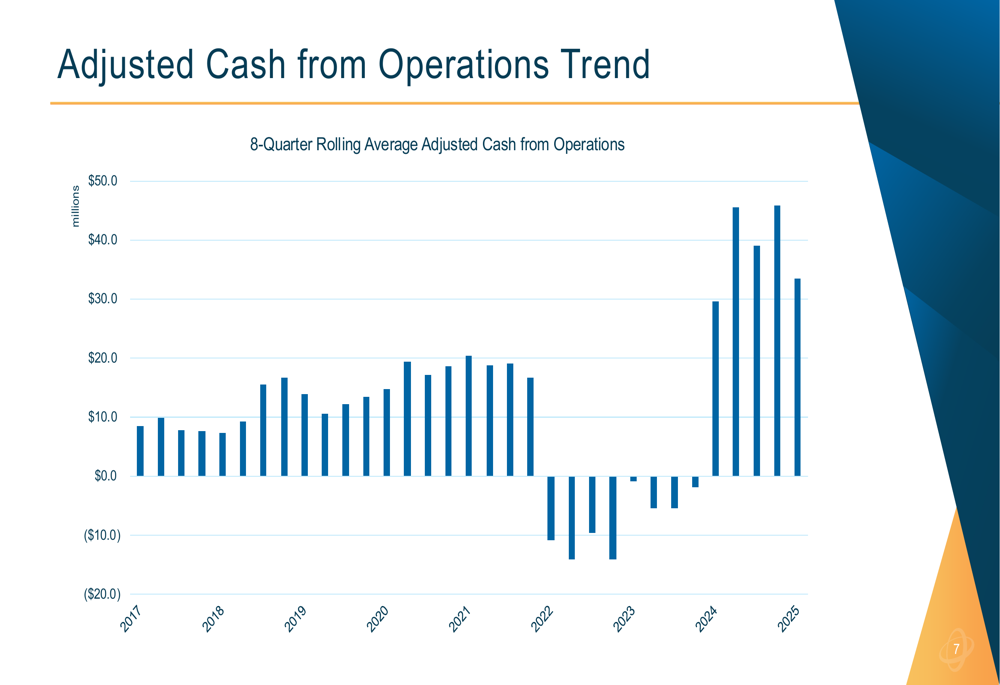

Ameresco has shown improvement in its cash flow generation, with adjusted cash from operations trending upward in recent quarters:

The 8-quarter rolling average has increased substantially since 2023, reaching approximately $45 million by Q1 2025, providing greater financial flexibility for future investments and potentially reducing reliance on external financing.

Strategic Initiatives & Energy Asset Portfolio

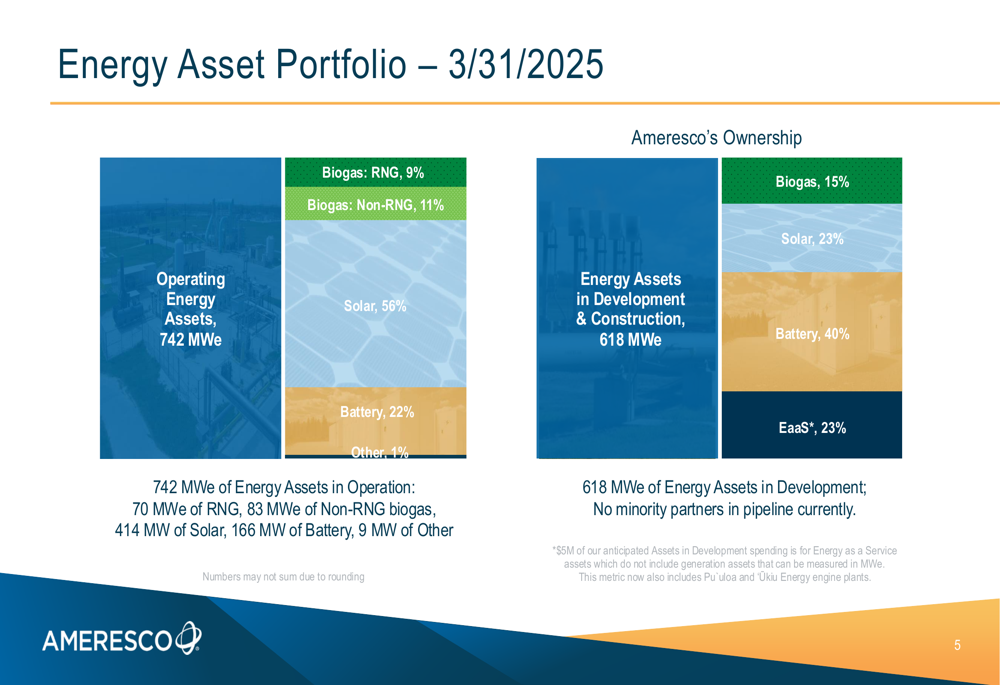

Ameresco continues to expand its energy asset portfolio, which represents a growing source of recurring revenue and adjusted EBITDA. As of March 31, 2025, the company’s operating assets totaled 742 MWe, with an additional 618 MWe in development.

The composition of these assets is shown in the following chart:

Solar installations dominate the operating portfolio at 56% (414 MW), followed by battery storage at 22% (166 MW), and biogas facilities (both RNG and non-RNG) at 20% (153 MWe combined). The development pipeline shows a strategic shift toward battery storage (40%) and energy-as-a-service solutions (23%), reflecting evolving market demands.

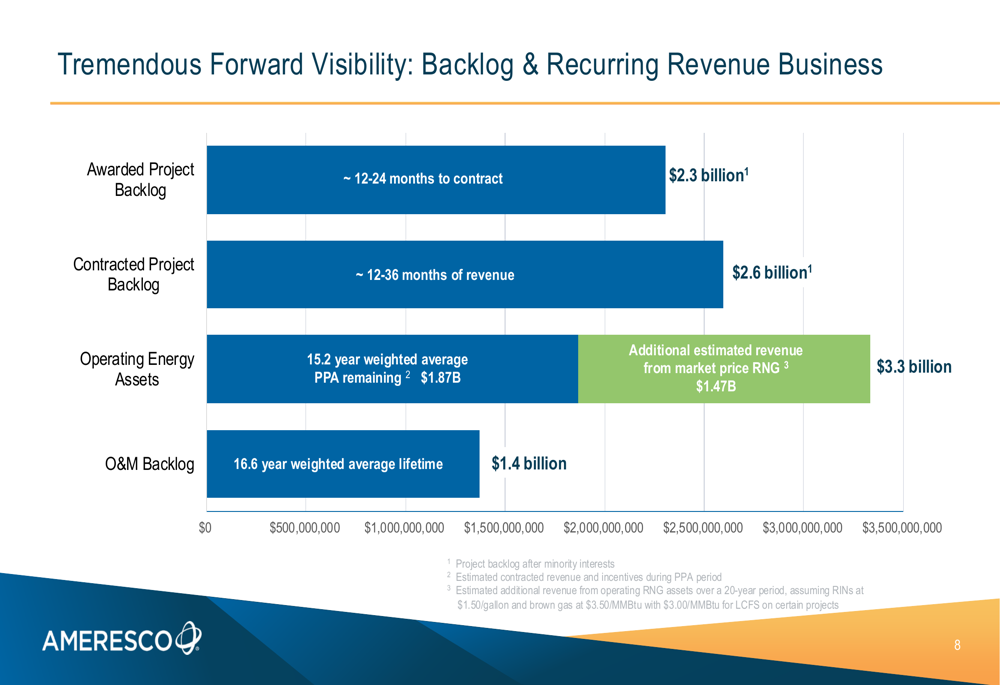

The company’s future revenue visibility is supported by a substantial backlog across multiple business segments:

Total (EPA:TTEF) project backlog stands at $4.9 billion, split between awarded ($2.3 billion) and contracted ($2.6 billion) projects. Additionally, operating energy assets are expected to generate $1.87 billion in revenue over their remaining contract terms (15.2-year weighted average), with potential for an additional $1.47 billion from market-priced renewable natural gas (RNG). O&M contracts add another $1.4 billion over their 16.6-year weighted average lifetime.

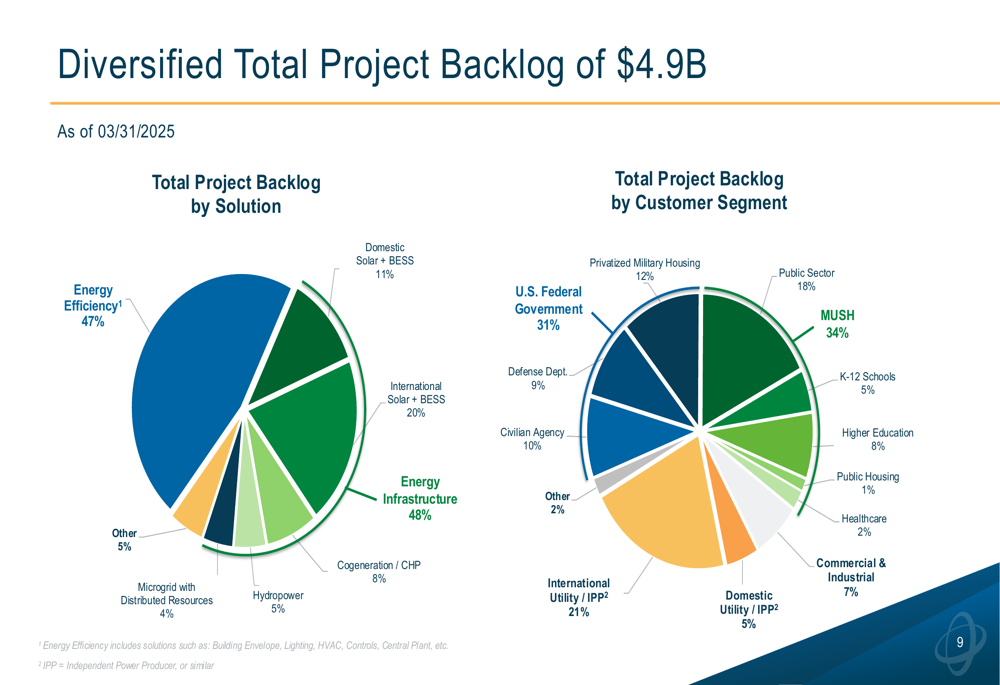

Ameresco’s project backlog demonstrates significant diversification across solutions and customer segments:

Energy efficiency projects represent 47% of the backlog, followed by international solar and battery energy storage systems (BESS) at 20%, and energy infrastructure at 16%. Customer diversification spans municipal, university, school, and hospital (MUSH) entities at 34%, U.S. federal government at 31%, and international utility/independent power producers (IPP) at 21%.

Forward-Looking Statements

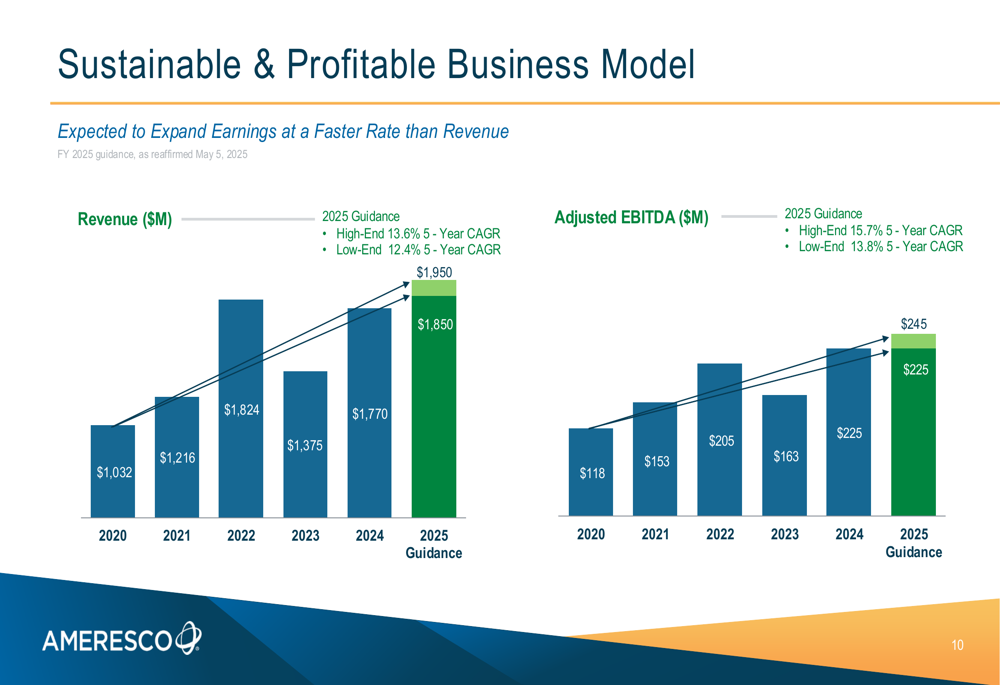

Ameresco reaffirmed its 2025 guidance on May 5, projecting continued growth in both revenue and adjusted EBITDA:

The company expects 2025 revenue to reach $1,950 million, representing a five-year CAGR of 12.4%-13.6% from 2020. Adjusted EBITDA is projected at $245 million, reflecting a five-year CAGR of 13.8%-15.7%. This guidance suggests accelerating profitability growth compared to revenue expansion, likely driven by the increasing contribution from high-margin recurring revenue streams.

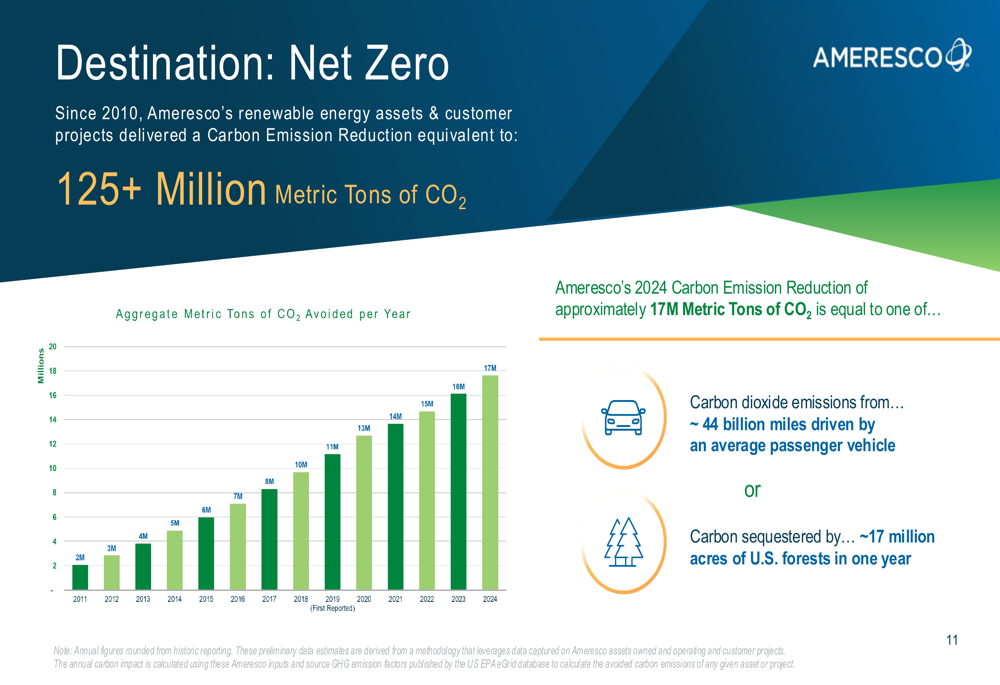

Ameresco also highlighted its environmental impact through carbon emission reductions:

The company’s projects have delivered carbon emission reductions equivalent to 125+ million metric tons of CO2 since 2010, with annual reductions reaching approximately 17 million metric tons in 2024. This environmental contribution underscores Ameresco’s alignment with global decarbonization trends and positions the company to benefit from increasing clean energy investments.

Market Reaction & Investor Perspective

Despite Ameresco’s operational progress and positive outlook, investor sentiment remains cautious. The stock has declined significantly from its 52-week high of $39.68 to close at $12.00 on May 5, 2025, though it showed some recovery in after-hours trading, rising 5.87% to $12.27.

This disconnect between operational performance and stock valuation follows a pattern observed after the company’s Q4 2024 earnings release, when the stock fell nearly 12% despite exceeding analyst expectations. The market’s hesitation may reflect concerns about the capital-intensive nature of Ameresco’s business model, potential project delays, or the impact of interest rates on financing costs.

However, the company’s growing recurring revenue base, substantial project backlog, and improving cash flow generation could eventually support a valuation recovery if Ameresco continues to execute on its growth strategy and delivers on its 2025 financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.