Palantir to report; Trump on Nvidia chip exports - what’s moving markets

Introduction & Market Context

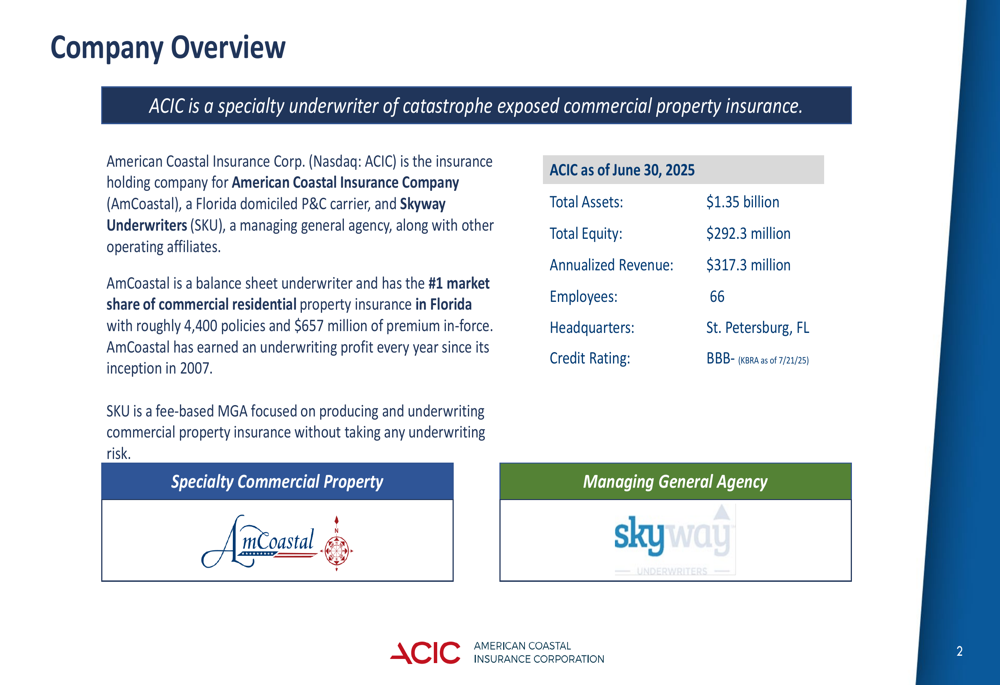

American Coastal Insurance Corporation (ACIC) presented its second quarter 2025 earnings results on August 6, 2025, revealing substantial growth and outperformance across key metrics despite softening conditions in the Florida commercial property market.

The specialty underwriter of catastrophe-exposed commercial property insurance reported significant year-over-year improvements in core income, premiums earned, and combined ratio, while also announcing a credit rating upgrade to investment grade status from KBRA.

As shown in the company overview slide, ACIC maintains the #1 market share position in Florida’s commercial residential property insurance market with approximately 4,400 policies and $657 million of premium in-force.

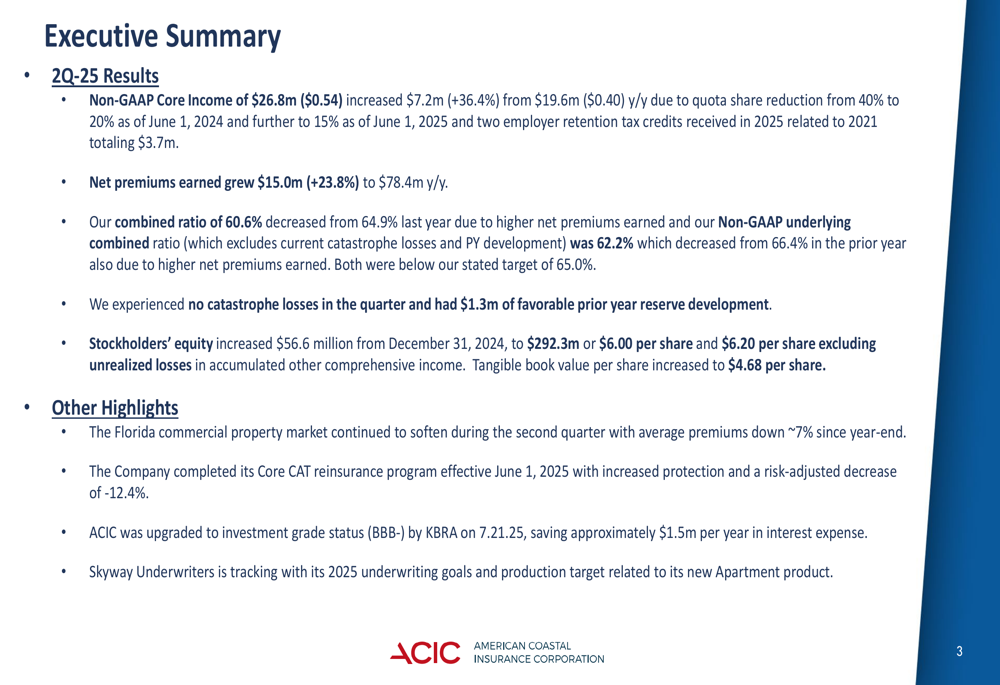

Executive Summary

ACIC reported Non-GAAP Core Income of $26.8 million ($0.54 per share) for Q2 2025, representing a 36.4% increase compared to the same period last year. This performance substantially exceeded analyst expectations of $0.38 per share.

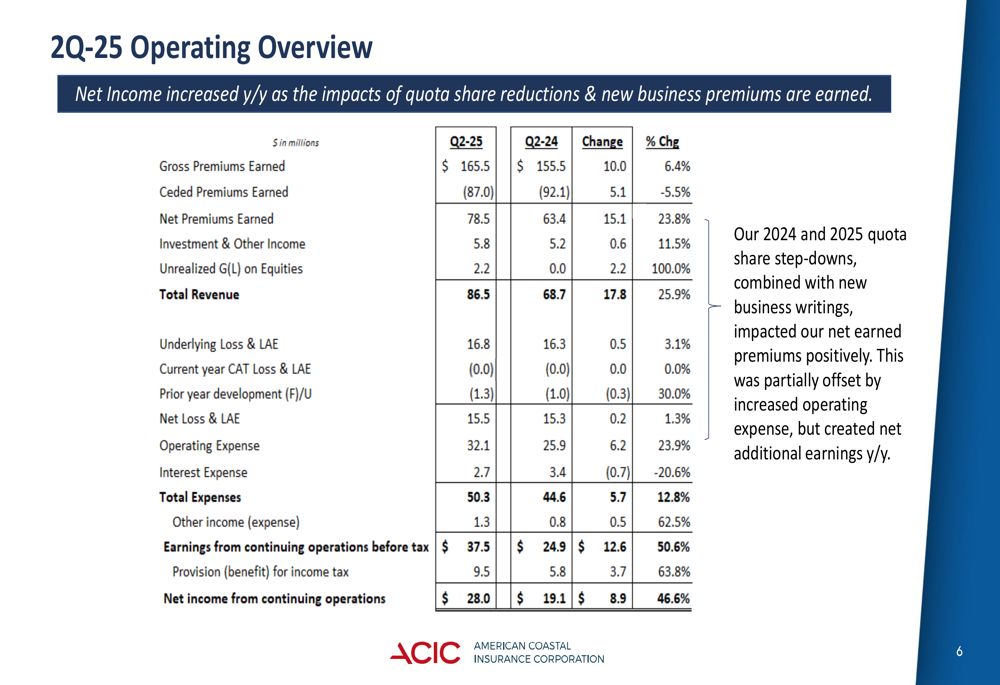

Net premiums earned grew by $15.0 million to $78.4 million, a 23.8% year-over-year increase, while the combined ratio improved to 60.6% from 64.9% in Q2 2024. The company reported no catastrophe losses during the quarter and benefited from $1.3 million in favorable prior year reserve development.

The executive summary slide highlights these achievements alongside other significant developments, including the company’s upgraded credit rating and the completion of its reinsurance program with favorable terms.

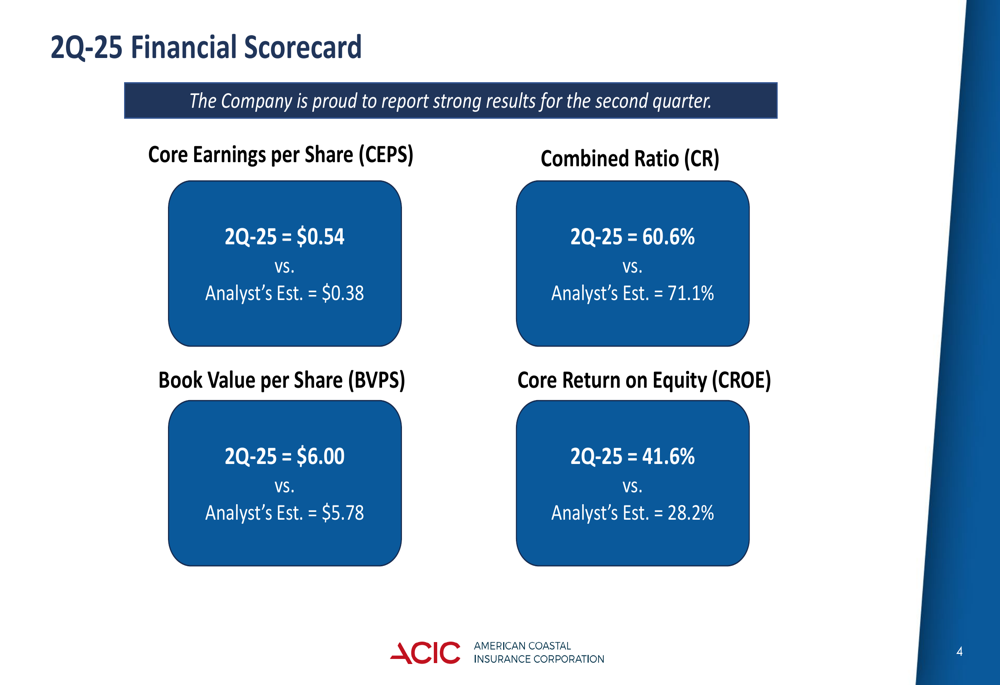

ACIC’s financial performance consistently outpaced analyst estimates across all key metrics, as illustrated in the financial scorecard. The company’s core earnings per share of $0.54 exceeded the analyst estimate of $0.38 by 42%, while the combined ratio of 60.6% significantly outperformed the expected 71.1%. Book value per share reached $6.00, above the estimated $5.78, and core return on equity stood at an impressive 41.6% compared to the anticipated 28.2%.

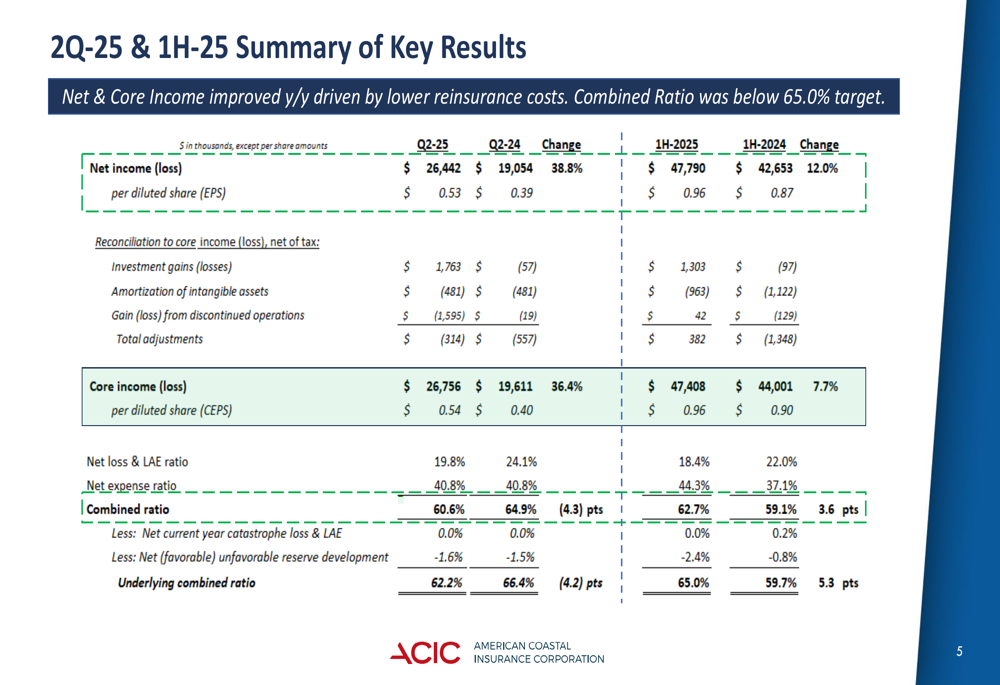

Quarterly Performance Highlights

The detailed financial results show ACIC’s net income for Q2 2025 reached $26.4 million ($0.53 per diluted share), representing a 38.8% increase from Q2 2024. For the first half of 2025, net income totaled $47.8 million ($0.96 per diluted share), up 12.0% from the same period last year.

The company’s combined ratio of 60.6% for Q2 2025 improved by 4.3 percentage points year-over-year, while the underlying combined ratio (which excludes catastrophe losses and prior year development) improved to 62.2% from 66.4% in the prior year period.

From an operational perspective, ACIC generated total revenue of $86.5 million in Q2 2025, a 25.9% increase compared to Q2 2024. This growth was primarily driven by the 23.8% increase in net premiums earned, which reached $78.5 million. The company’s earnings from continuing operations before tax surged by 50.6% to $37.5 million.

Detailed Financial Analysis

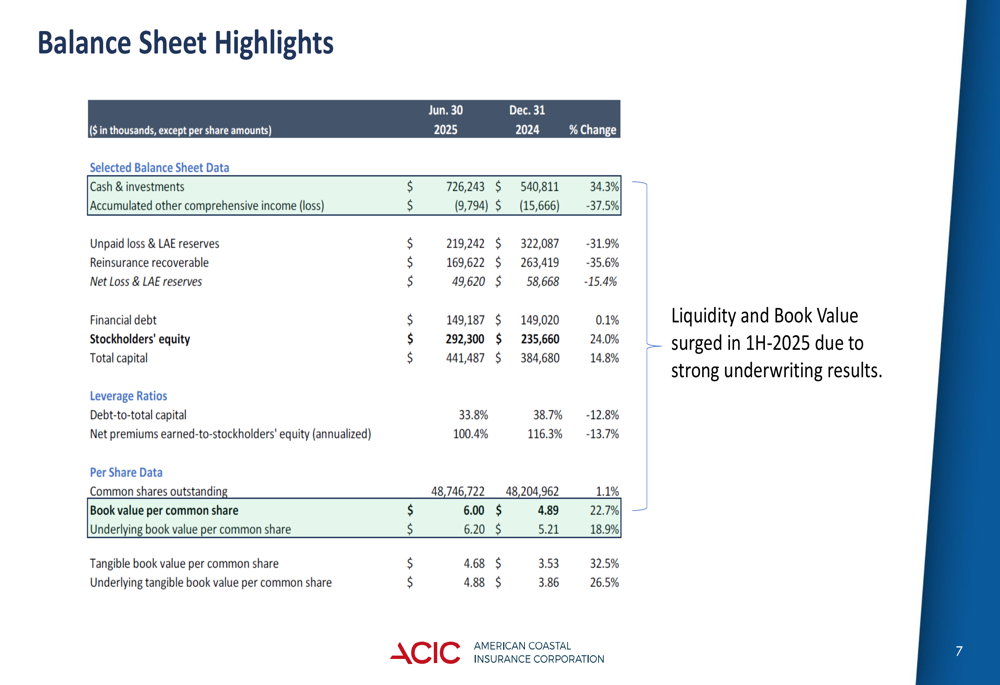

ACIC’s balance sheet continued to strengthen during the quarter, with stockholders’ equity increasing to $292.3 million as of June 30, 2025, up from $235.7 million at the end of 2024. This translates to a book value per common share of $6.00 and a tangible book value per common share of $4.68.

The company maintains a solid capital position with a debt-to-total capital ratio of 33.8%. Cash and investments totaled $726.2 million, providing substantial liquidity to support operations and growth initiatives.

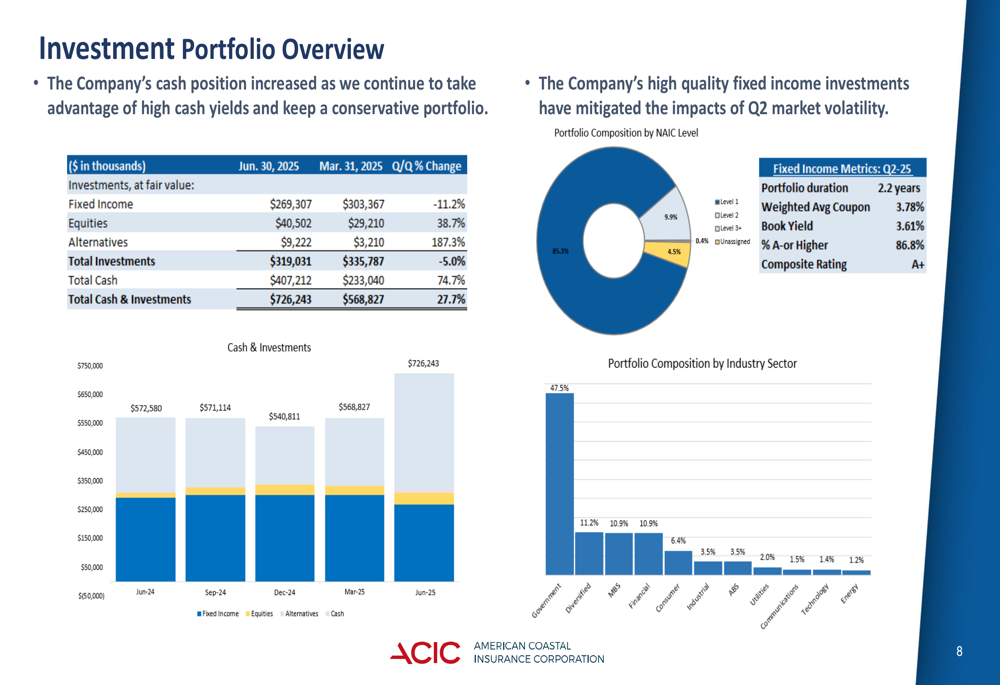

The investment portfolio remains conservatively positioned with a focus on high-quality fixed income securities. As of June 30, 2025, fixed income investments totaled $269.3 million, representing the largest allocation within the investment portfolio. The fixed income portfolio has a duration of 2.2 years and a weighted average coupon of 3.78%, with 86.8% of holdings rated A or higher.

Strategic Initiatives & Outlook

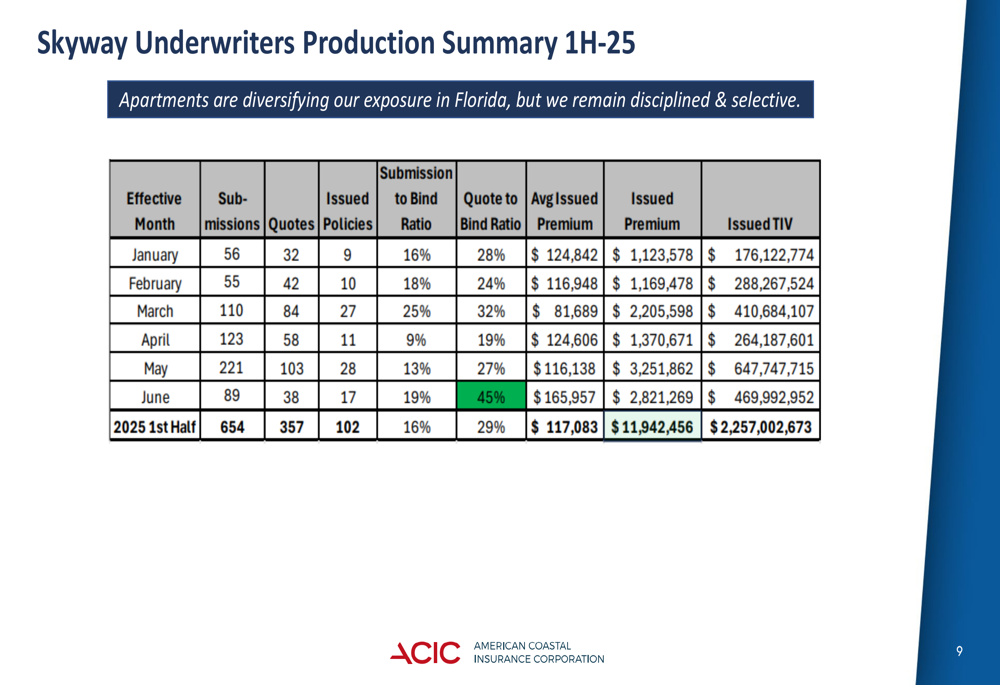

The company’s Skyway Underwriters division, which operates as a fee-based managing general agency, showed steady progress in the first half of 2025. The production summary indicates that Skyway processed 654 submissions and 357 quotes, resulting in 102 issued policies with an average premium of $117,083. Total (EPA:TTEF) issued premium for the period reached nearly $12 million, covering over $2.2 billion in total insured value.

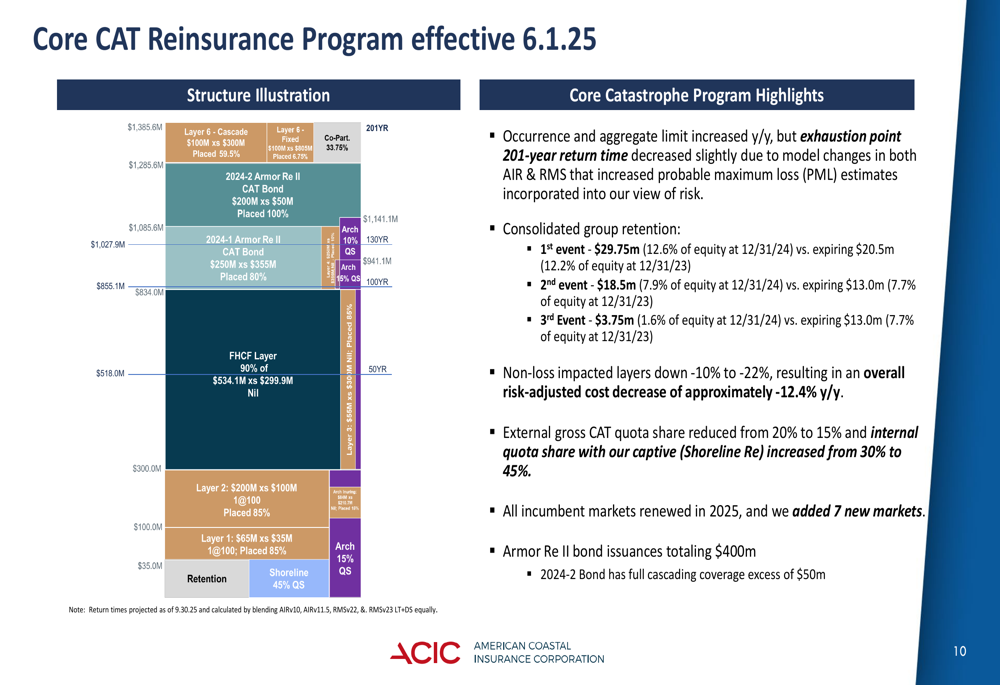

A key strategic achievement during the quarter was the completion of ACIC’s Core CAT reinsurance program, effective June 1, 2025. The program features increased occurrence and aggregate limits compared to the previous year, while benefiting from a risk-adjusted cost decrease of approximately 12.4%. The company reduced its external gross CAT quota share from 20% to 15% while increasing its internal quota share with captive reinsurer Shoreline Re from 30% to 45%.

The reinsurance structure provides comprehensive protection against catastrophic events, with clearly defined retention levels for first, second, and third events. This enhanced program reflects the company’s strong market position and improved risk profile.

The credit rating upgrade to investment grade status (BBB-) by KBRA on July 21, 2025, represents a significant milestone for ACIC and validates the company’s financial strength and disciplined underwriting approach. This upgrade could potentially lower borrowing costs and enhance the company’s competitive position in the market.

Looking ahead, ACIC appears well-positioned to navigate the softening Florida commercial property market, where average premiums have declined by approximately 7% since year-end. The company’s strong underwriting performance, improved reinsurance terms, and solid capital position provide a foundation for continued profitability despite market challenges.

This quarter’s results demonstrate a significant improvement from Q1 2025, when the company reported core income of $20.7 million with a year-over-year decrease. The Q2 performance indicates a successful turnaround and acceleration of growth, suggesting the company’s strategic initiatives are gaining traction in the marketplace.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.