SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

American Express Company (NYSE:AXP) reported solid second-quarter results on July 18, 2025, with revenue growth of 9% and adjusted earnings per share increasing 17% year-over-year. The financial services giant’s stock responded positively, rising 2.09% in premarket trading to $321.94, building on its previous close of $315.35.

The company’s Q2 performance demonstrates continued momentum from its first quarter, when it reported 8% revenue growth and exceeded EPS expectations. American Express has maintained its full-year guidance of 8-10% revenue growth and EPS between $15.00 and $15.50.

Quarterly Performance Highlights

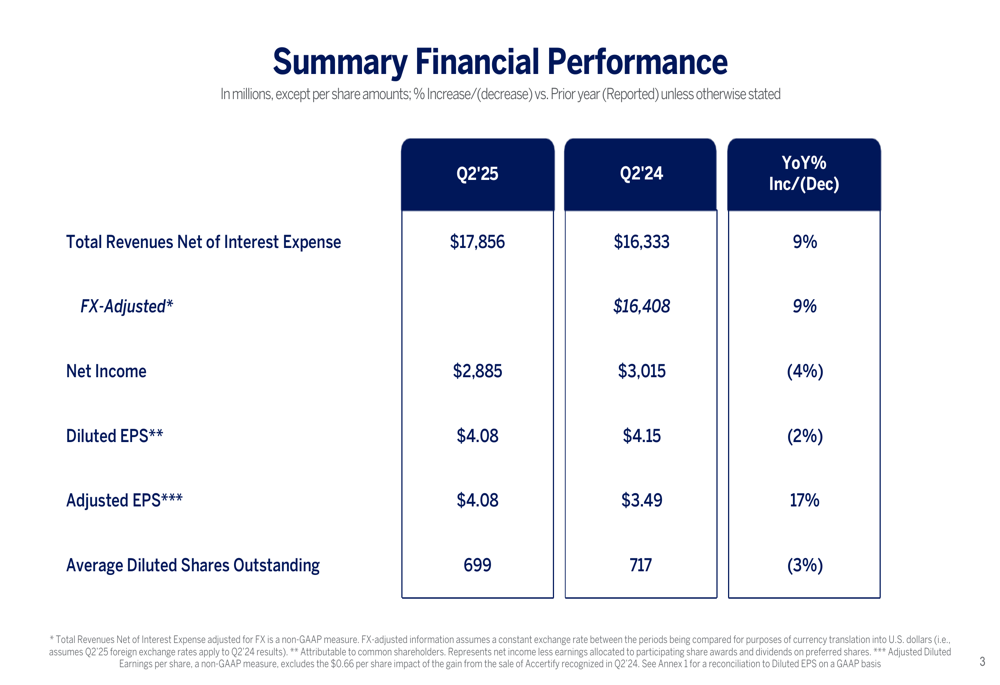

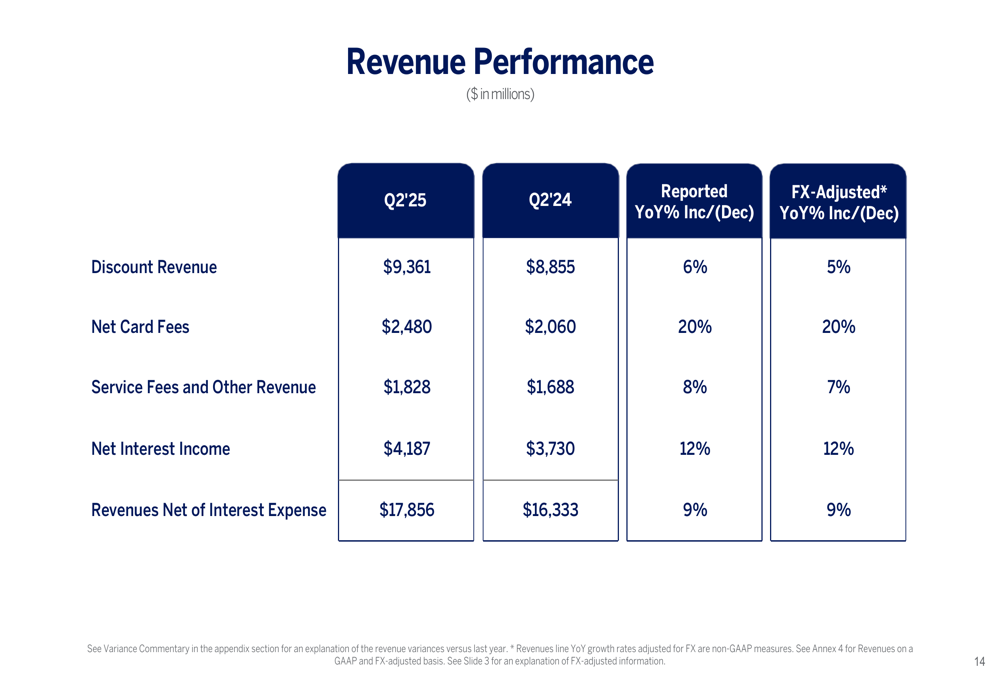

American Express delivered total revenues net of interest expense of $17.86 billion in the second quarter, representing a 9% increase from $16.33 billion in the same period last year. Net income was $2.89 billion, down 4% from $3.02 billion in Q2 2024, while diluted EPS reached $4.08, a 2% decrease from $4.15. However, when adjusted for the prior year gain on sale from Accertify, adjusted EPS increased 17% from $3.49.

As shown in the following summary financial performance slide, the company maintained strong revenue growth while continuing to invest in its business:

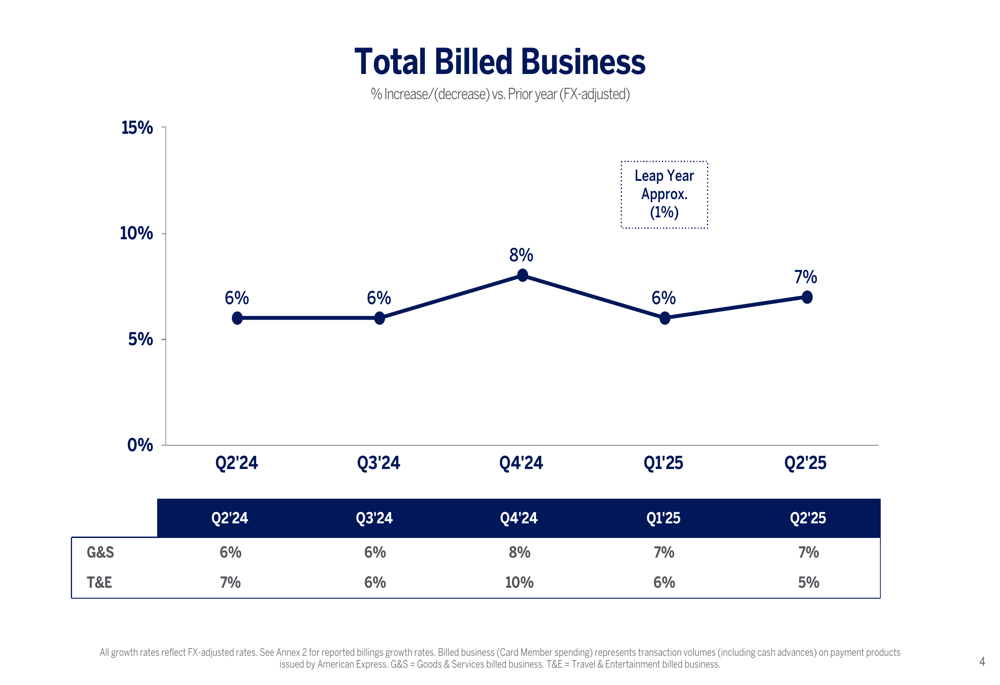

Billed business, a key indicator of customer spending, grew 7% year-over-year on an FX-adjusted basis. This growth was consistent across both goods and services (7%) and travel and entertainment (5%) categories, reflecting balanced spending patterns among cardholders.

The following chart illustrates the steady growth in billed business over recent quarters:

Detailed Financial Analysis

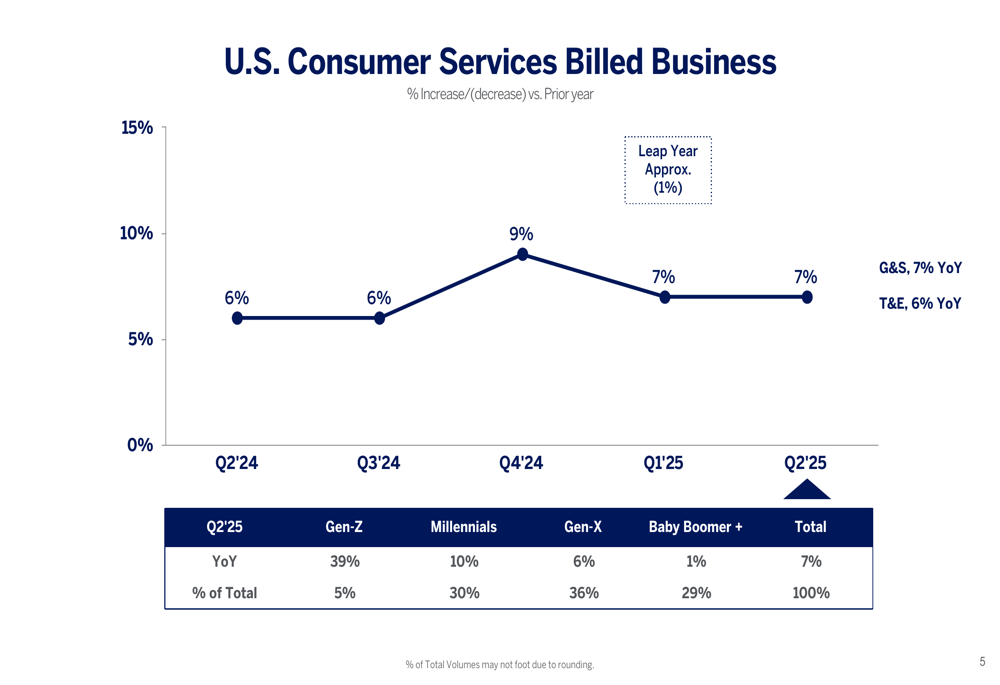

American Express’s performance varied across its business segments. U.S. Consumer Services showed solid growth with billed business up 7% year-over-year, maintaining the momentum seen in previous quarters. The company reported particularly strong engagement from younger generations, with Millennials and Gen-Z driving higher growth rates than older cardholders.

The following breakdown of U.S. Consumer Services billed business highlights generational differences in spending patterns:

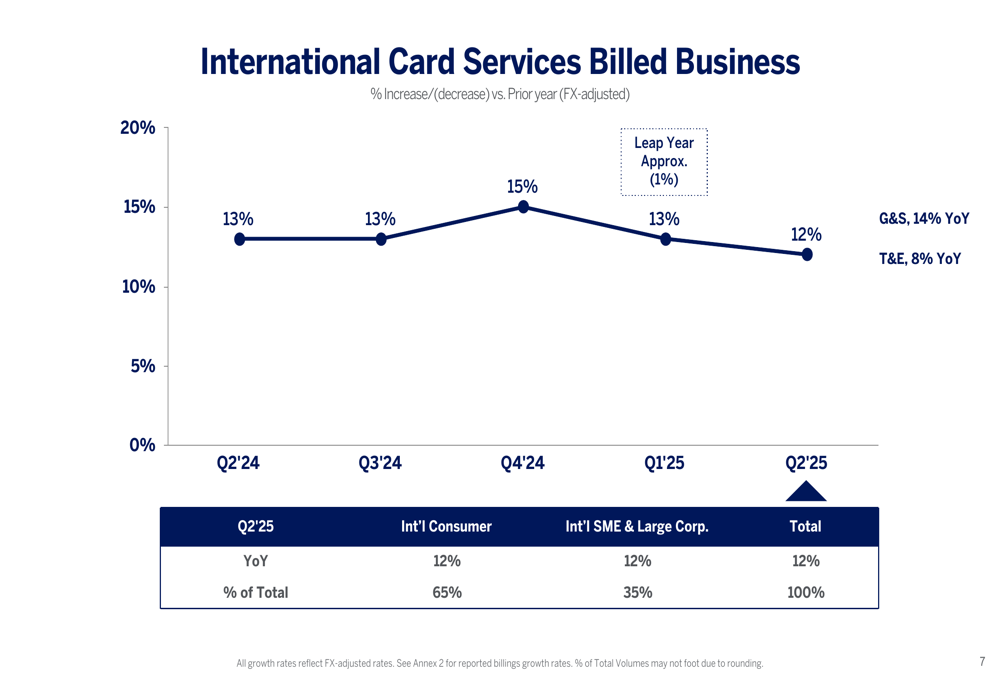

International Card Services emerged as the strongest performing segment, with billed business growth of 12% year-over-year. Both consumer and commercial segments within international markets showed robust 12% growth, significantly outpacing domestic performance.

The international growth trajectory is illustrated in this chart:

Commercial Services showed more modest growth at 2% year-over-year, with U.S. Small and Medium Enterprises (SME) growing at 2% and Large & Global Corporate accounts growing at 4%.

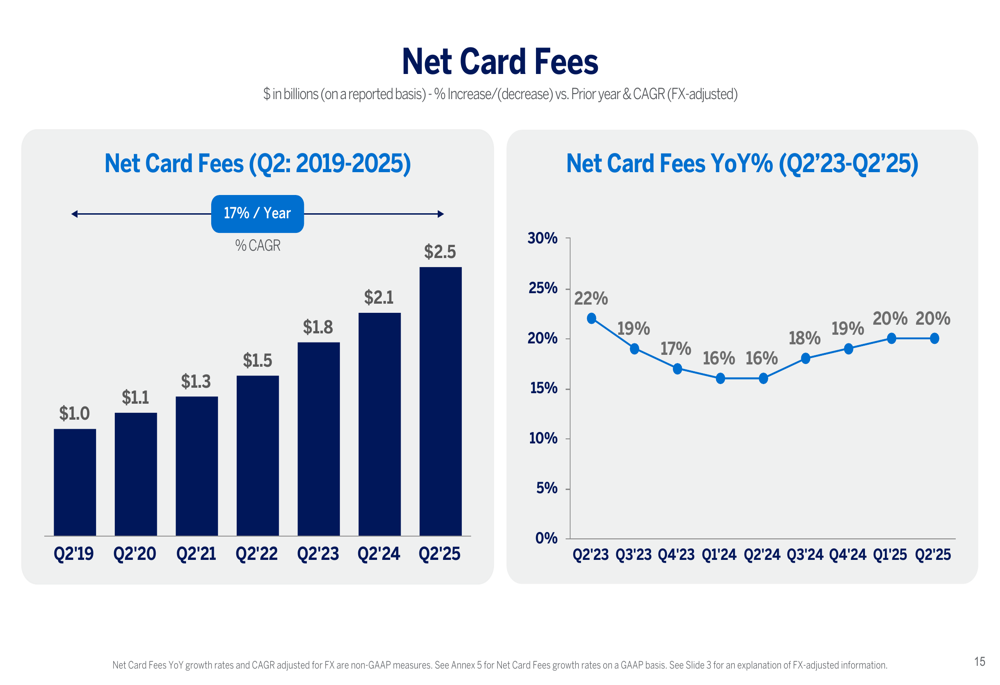

Revenue performance was particularly strong in fee-based categories. Net card fees grew an impressive 20% year-over-year to $2.48 billion, reflecting the success of American Express’s premium card strategy. Discount revenue increased 6% to $9.36 billion, while net interest income rose 12% to $4.19 billion.

The following revenue breakdown shows the contribution of each revenue stream:

The company’s focus on premium cards has driven sustained growth in card fee revenue, as shown in this multi-year trend:

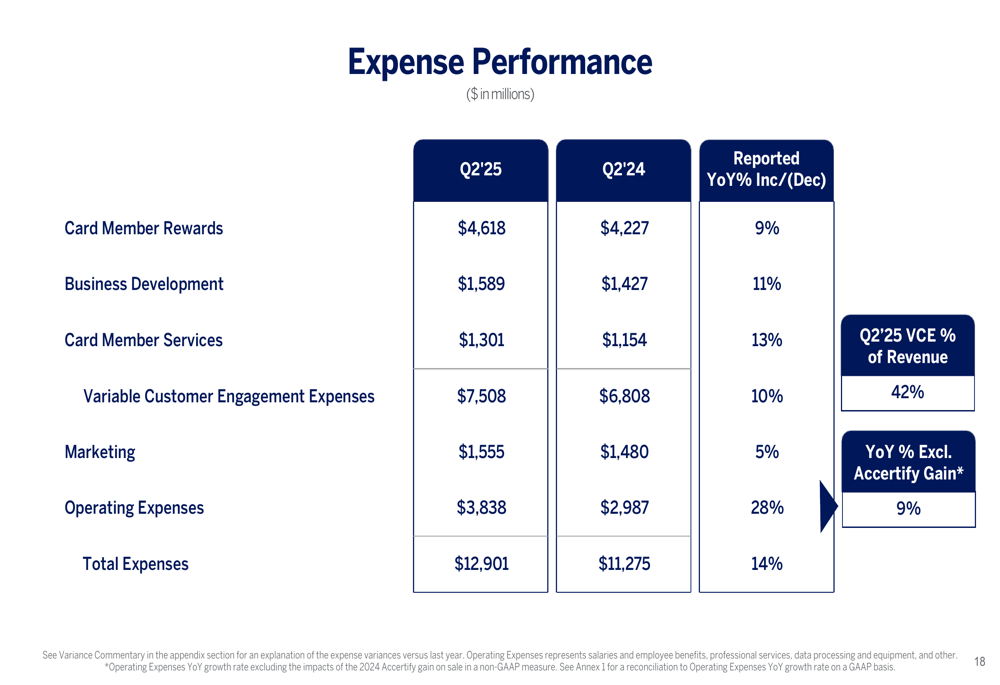

On the expense side, total expenses increased 14% year-over-year to $12.90 billion. Variable customer engagement expenses rose 10% to $7.51 billion, while operating expenses increased 28% to $3.84 billion. Marketing expenses grew more modestly at 5% to $1.56 billion.

The detailed expense breakdown is presented here:

Strategic Initiatives

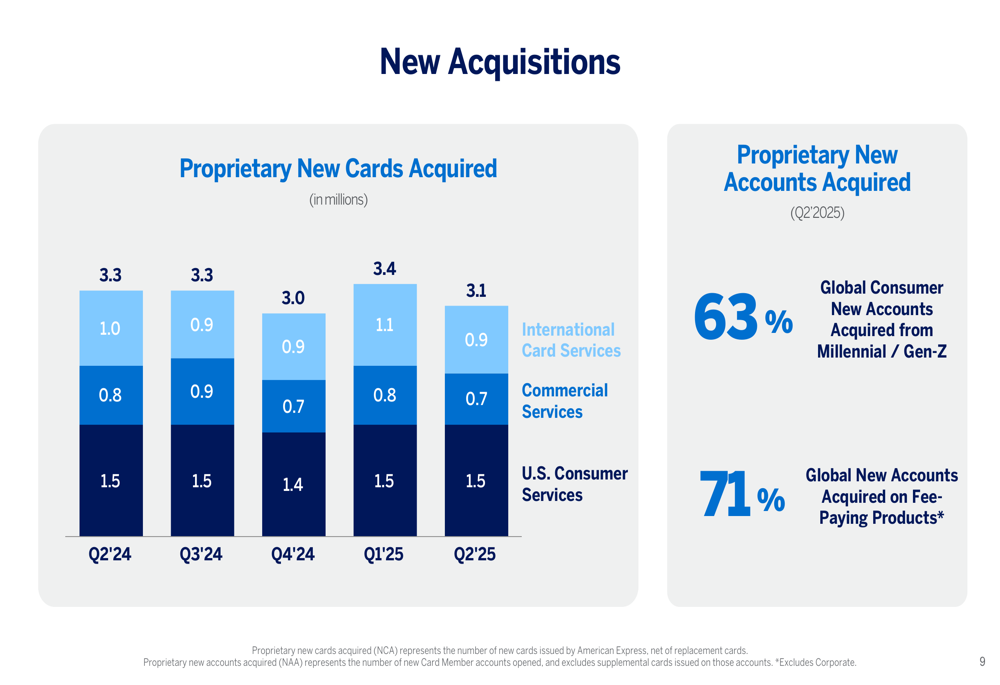

American Express continues to execute on its strategy of attracting premium customers and younger demographics. The company acquired 3.1 million new proprietary cards in Q2 2025, with 63% of global consumer new accounts coming from Millennial and Gen-Z customers. Additionally, 71% of global new accounts were on fee-paying products, underscoring the company’s success in positioning its premium offerings.

The following chart details new card acquisition trends:

The company announced major updates coming to the Consumer and Business Platinum Cards in the U.S. this fall, which are expected to further strengthen its premium card portfolio. American Express also revealed a partnership with Coinbase (NASDAQ:COIN) to launch the Coinbase One Card on the American Express Network, expanding its reach in the cryptocurrency space.

American Express’s digital capabilities continue to receive recognition, with the company ranking #1 in both U.S. Credit Card Mobile App and Website Experience for Customer Satisfaction by J.D. Power. These technological strengths support customer acquisition and retention efforts.

Credit metrics remained stable despite economic uncertainties, with 30+ days past due rates at 1.3% and net write-off rates at 2.0% of average card member loans and receivables. The company’s credit performance continues to outperform industry averages across all generations.

Forward-Looking Statements

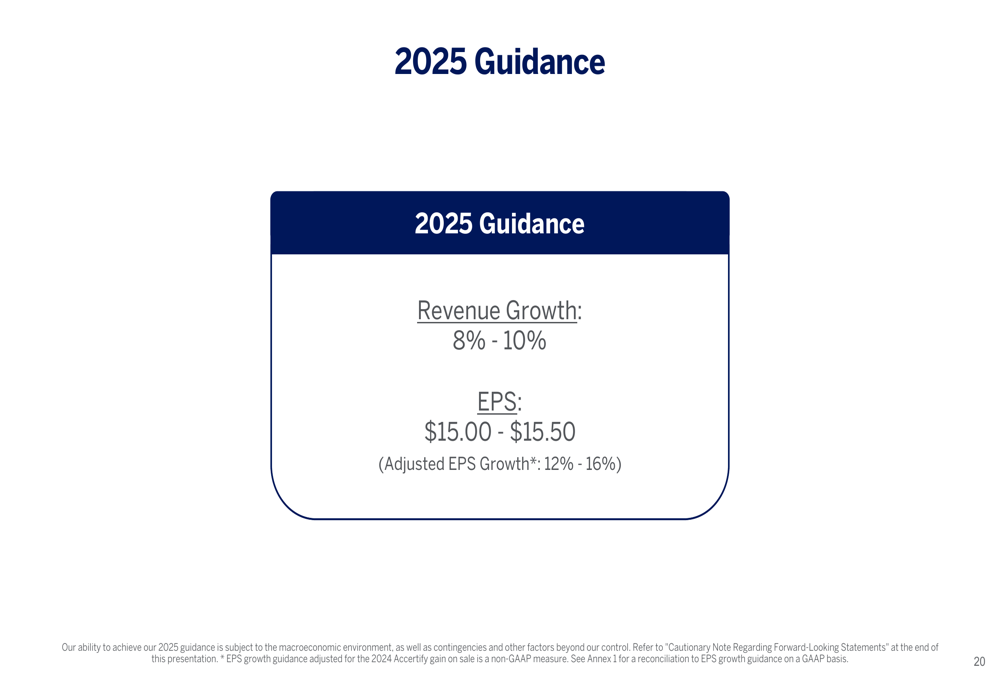

American Express reaffirmed its full-year 2025 guidance of 8-10% revenue growth and EPS between $15.00 and $15.50, representing adjusted EPS growth of 12-16%.

The company’s guidance is summarized in this slide:

Management expressed confidence in the company’s ability to continue executing its strategy of attracting premium customers and driving fee-based revenue growth. The strong performance in international markets and among younger demographics positions American Express well for sustained growth.

The Federal Reserve’s recent stress tests (CCAR) showed that American Express has the lowest projected credit card loss rate and highest projected return on assets under the Fed’s stress scenarios, highlighting the company’s strong risk management and financial resilience.

As American Express continues to invest in its premium card offerings and digital capabilities while expanding its international presence, the company appears well-positioned to deliver on its full-year targets despite macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.