U.S. inflation data ahead; Trump nominates new BLS head - what’s moving markets

American Outdoor Brands Inc (NASDAQ:AOUT) unveiled its fiscal year 2025 investor presentation on June 26, highlighting strong annual performance driven by its innovation strategy. The outdoor products company reported 10.6% revenue growth and an 80.8% surge in adjusted EBITDA, while outlining an ambitious path to double its business size in the coming years.

Executive Summary

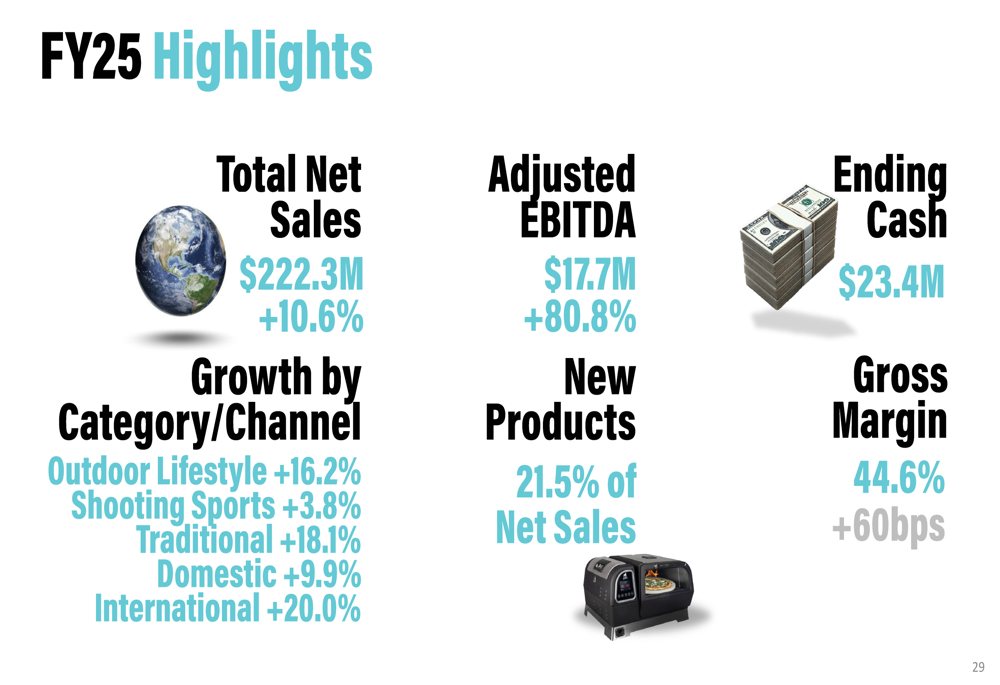

American Outdoor Brands delivered solid results for fiscal year 2025, with total net sales reaching $222.3 million, up 10.6% year-over-year, and adjusted EBITDA of $17.7 million, representing an impressive 80.8% increase. The company’s gross margin improved by 60 basis points to 44.6%, while new products contributed 21.5% of total net sales.

The company’s stock responded positively to its recent earnings report, with shares jumping 11.29% in premarket trading on June 27, according to market data. This follows a 9.42% aftermarket gain following the earnings announcement, despite a slight EPS miss of -$0.08 compared to the forecasted -$0.07.

As shown in the following chart of fiscal year 2025 highlights, the company saw growth across all categories and channels:

Innovation-Driven Strategy

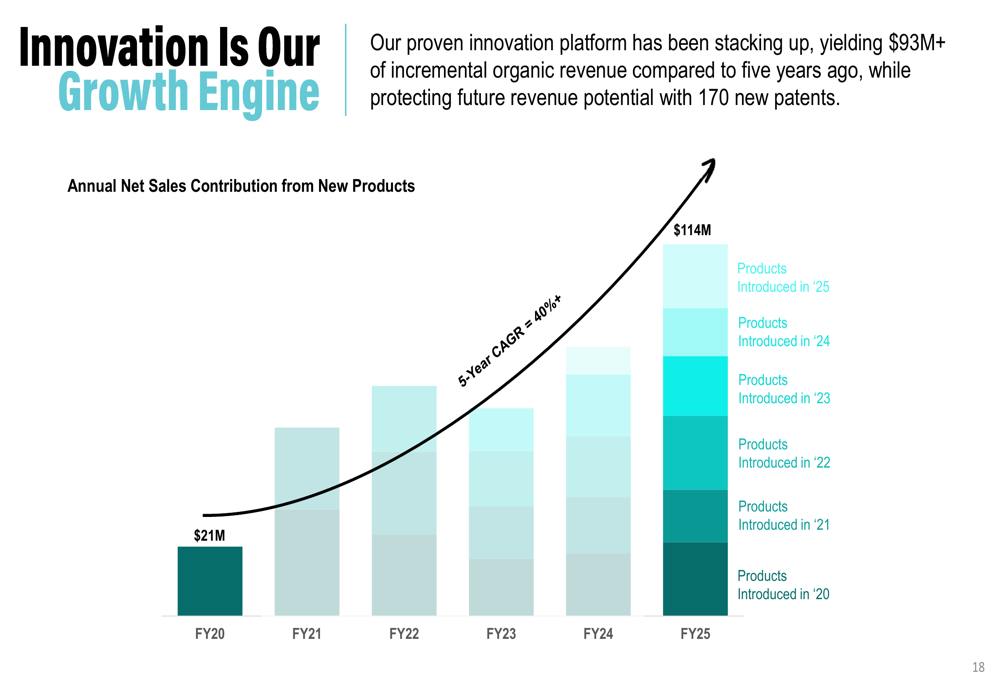

American Outdoor Brands positions itself primarily as an innovation company, leveraging its ability to identify and address consumer pain points in outdoor recreation markets. The company has secured 170 new patents over the past five years and generated over $93 million in incremental organic revenue compared to five years ago through its innovation platform.

The company’s product innovation strategy has shown impressive results, with new product revenue growing at a 40%+ CAGR over the past five years:

CEO Brian Murphy emphasized this focus in the recent earnings call, stating, "Our performance this year is the direct result of our relentless commitment to innovation." This strategy appears to be resonating with consumers, as the company cites research showing that 76% of consumers are willing to pay more for innovative products and 63% prefer to purchase new products from brands known for innovation and quality.

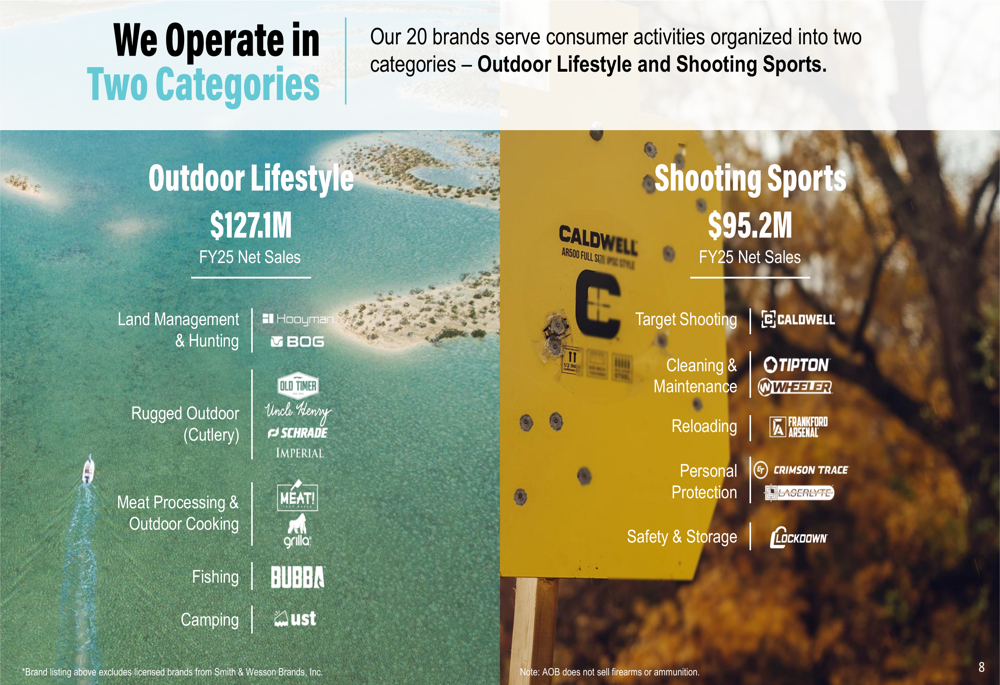

American Outdoor Brands operates across two main categories: Outdoor Lifestyle, which generated $127.1 million in FY25 net sales, and Shooting Sports, which contributed $95.2 million. The company’s brand portfolio includes names like BUBBA, Hooyman, and Old Timer in the Outdoor Lifestyle category, and Caldwell, Crimson Trace, and Tipton in Shooting Sports.

Growth Roadmap

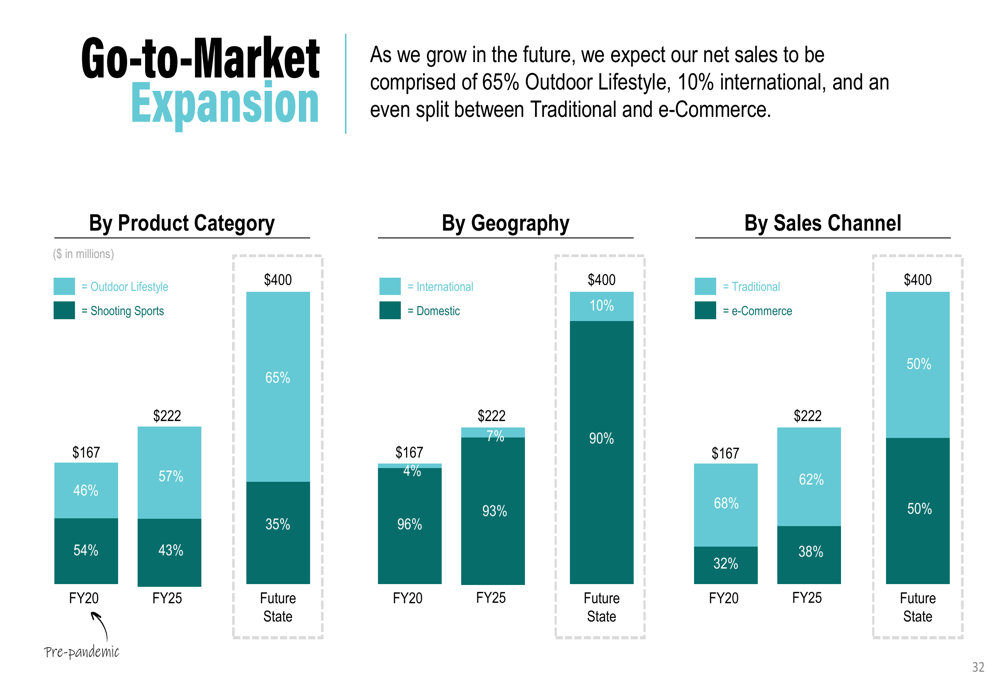

The company has outlined a four-pillar growth strategy aimed at reaching $400 million in future net sales, nearly double its current size. This strategy focuses on gaining market share, entering new product categories, expanding into new consumer markets, and broadening distribution channels.

American Outdoor Brands targets resilient consumer activities with approximately 175 million Americans participating in outdoor recreation. Its specific markets include 92 million outdoor cooking households, 54 million anglers, 86 million property owners, 15 million hunters, and 40 million target shooters.

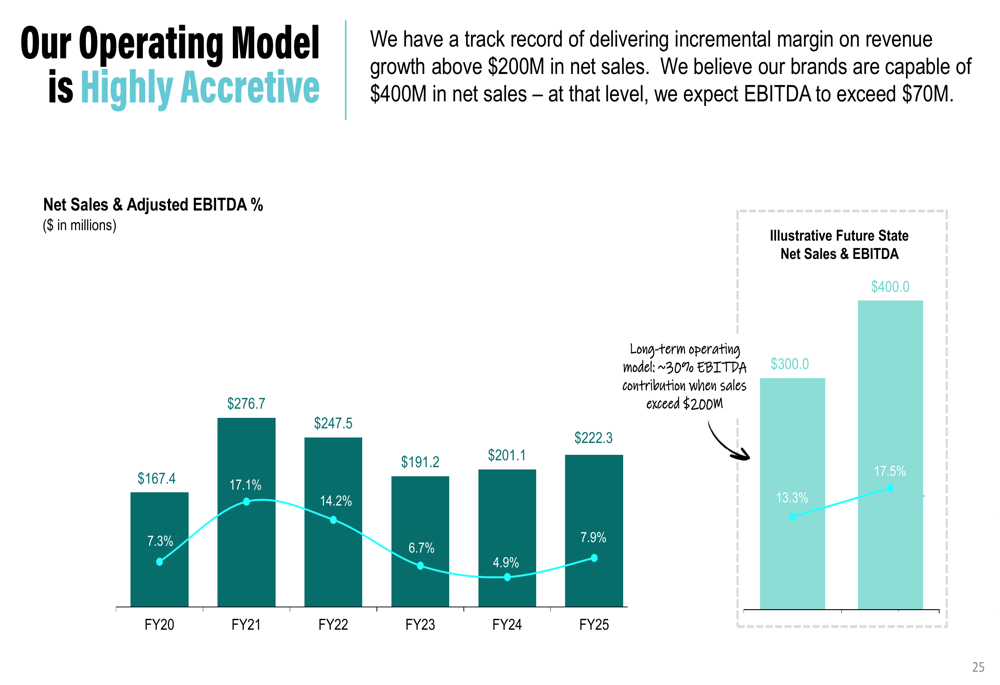

The company’s financial projections show an accretive operating model, with expectations that at $400 million in net sales, adjusted EBITDA would exceed $70 million, representing a 17.5% margin. This would be a significant improvement from the current 7.9% EBITDA margin at $222.3 million in sales.

As part of its growth strategy, American Outdoor Brands expects its future sales composition to shift more heavily toward the faster-growing Outdoor Lifestyle category, which would represent 65% of total sales (up from 57% currently). The company also anticipates international sales growing to 10% of the total, with an even split between traditional retail and e-commerce channels.

Financial Outlook & Challenges

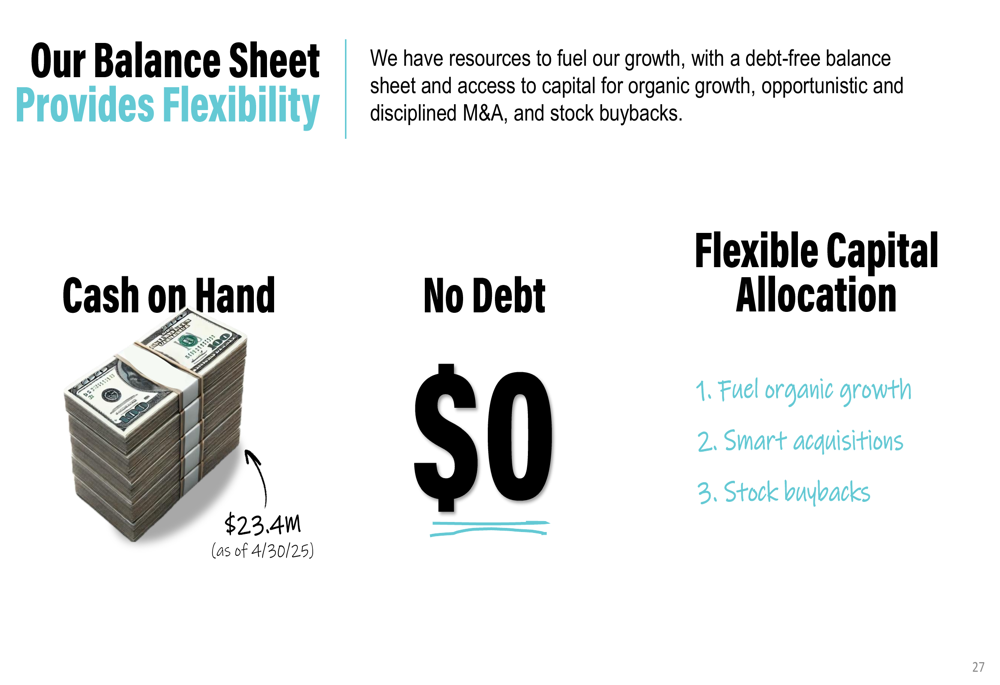

American Outdoor Brands maintains a strong, debt-free balance sheet with $23.4 million in cash as of April 30, 2025. This financial flexibility positions the company to pursue organic growth initiatives, opportunistic acquisitions, and stock buybacks.

However, the company faces several challenges that could impact its growth trajectory. In its recent earnings call, management suspended its FY 2026 net sales guidance due to uncertainties surrounding tariffs. Other potential headwinds include additional public company costs, cautious retailer inventory levels, and ongoing supply chain challenges.

Despite these concerns, American Outdoor Brands emphasizes its asset-light business model as a strategic advantage. The company maintains a small footprint with fewer than 300 employees and one distribution center, while outsourcing manufacturing to keep capital expenditure needs low at approximately 2% of net sales. This approach provides scalability, with infrastructure already in place to support up to $400 million in revenue.

The company summarizes its investment case with seven key considerations that highlight its market position, innovation capabilities, and financial strength:

While American Outdoor Brands’ presentation paints an optimistic picture of its growth prospects, investors should balance this against the uncertainties acknowledged in the company’s decision to suspend forward guidance. Nevertheless, the strong FY25 results and positive market reaction suggest confidence in the company’s innovation-driven strategy and its ability to navigate potential headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.