Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Amgen Inc (NASDAQ:AMGN) reported its first quarter 2025 financial results on May 1, showcasing continued growth across its diverse portfolio of products. The biotechnology giant’s shares declined 2.49% on the day of the earnings release, closing at $290.92, suggesting investors may have expected even stronger results despite the solid performance.

The Q1 results follow a strong 2024, when Amgen reported 23% year-over-year revenue growth in the third quarter. While Q1 2025’s growth rate of 9% represents a deceleration from that pace, the company still demonstrated robust performance across its key therapeutic areas and continued advancement of its pipeline candidates.

Quarterly Performance Highlights

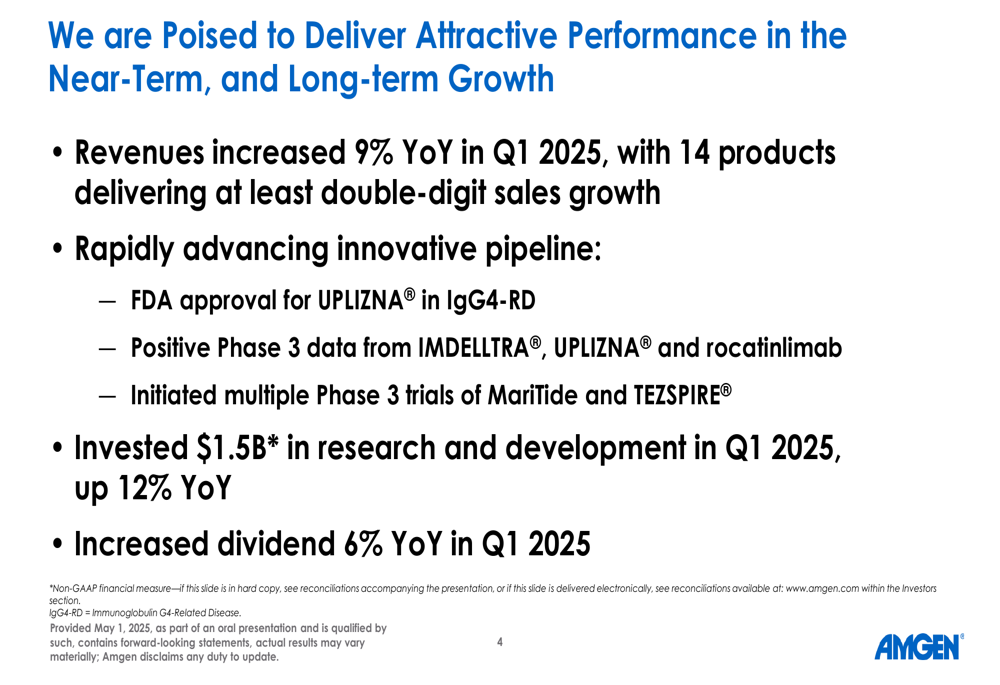

Amgen reported total revenue of $8.15 billion for Q1 2025, representing a 9% increase compared to the same period last year. Product sales grew 11% year-over-year to $7.87 billion, with 14 products delivering double-digit sales growth.

As shown in the following performance highlights slide, the company received FDA approval for UPLIZNA in IgG4-RD and reported positive Phase 3 data from multiple products:

The company’s investment in research and development reached $1.5 billion in the quarter, up 12% year-over-year, reflecting Amgen’s continued commitment to pipeline advancement. Additionally, the company increased its dividend by 6% compared to the previous year.

Therapeutic Area Performance

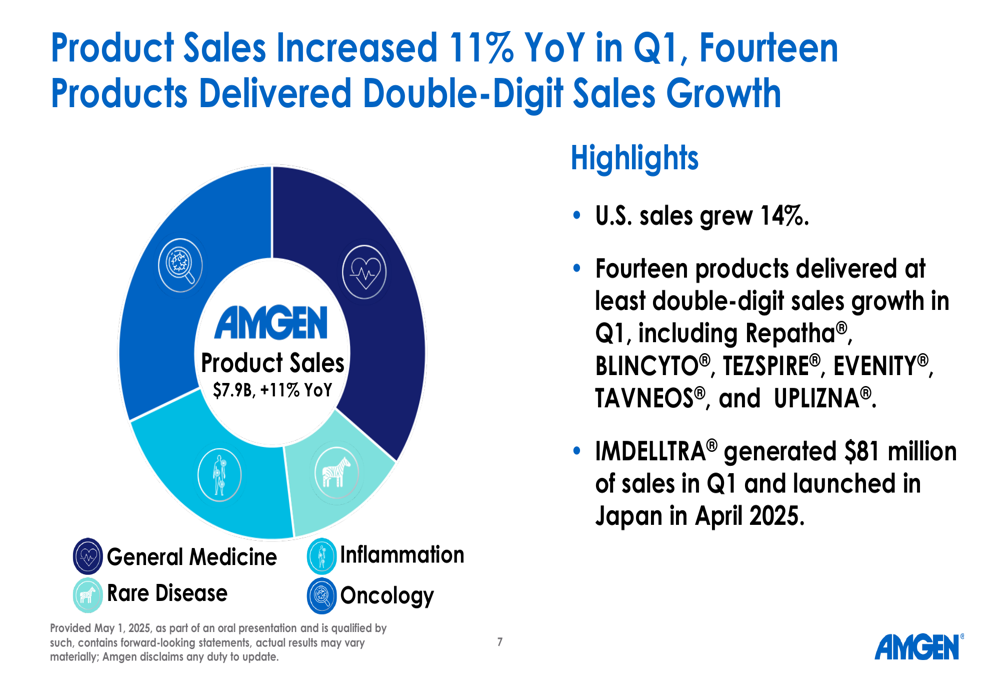

Amgen’s product sales were well-distributed across its four therapeutic areas: General Medicine, Rare Disease, Inflammation, and Oncology. The following chart illustrates the breakdown of the company’s $7.9 billion in product sales:

In General Medicine, which generated over $2 billion in sales during Q1, Repatha and the Bone Franchise (Prolia and EVENITY) led growth. Repatha sales increased 27% year-over-year to $656 million, while EVENITY sales grew 29% to $442 million. Prolia sales rose 10% to $1.1 billion, though the company expects sales erosion later in 2025 due to biosimilar competition.

The Rare Disease portfolio generated $1 billion in sales, with TAVNEOS standing out with 76% year-over-year growth to $90 million. However, TEPEZZA sales declined 10% to $381 million, which the company attributed to decreases in inventory levels.

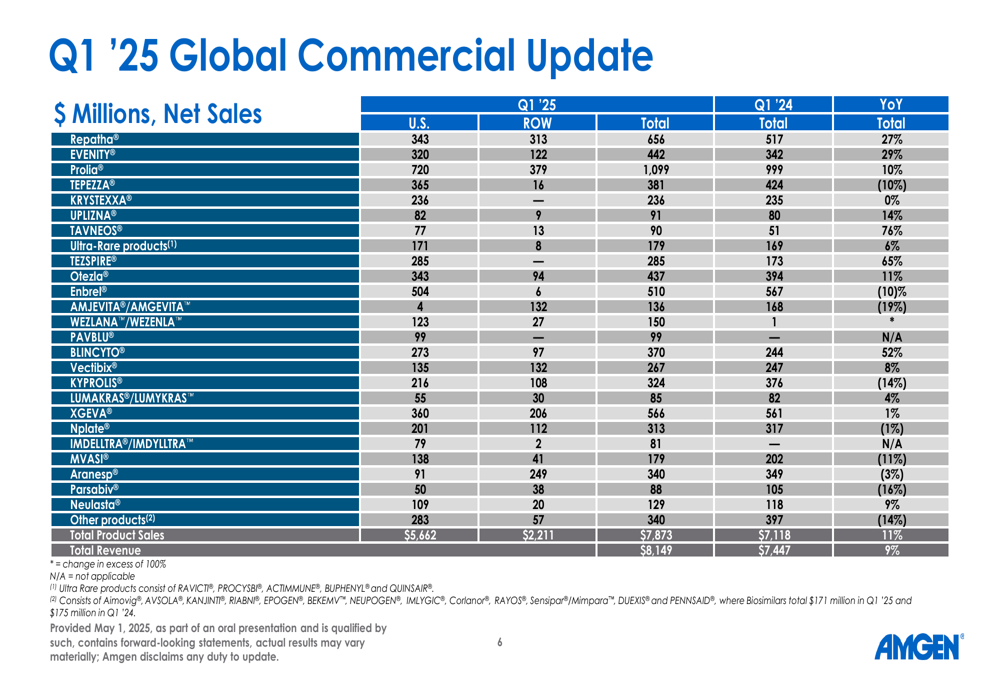

As shown in the following detailed breakdown of product sales, performance varied significantly across the portfolio:

In the Inflammation area, which generated over $1 billion in sales, TEZSPIRE was a standout performer with 65% year-over-year growth to $285 million. Otezla sales increased 11% to $437 million, while Enbrel sales declined 10% to $510 million.

The Oncology portfolio, which generated over $2 billion in sales, was highlighted by BLINCYTO’s 52% year-over-year growth to $370 million and the strong launch of IMDELLTRA, which generated $81 million in Q1 and was subsequently launched in Japan in April 2025.

Pipeline Developments

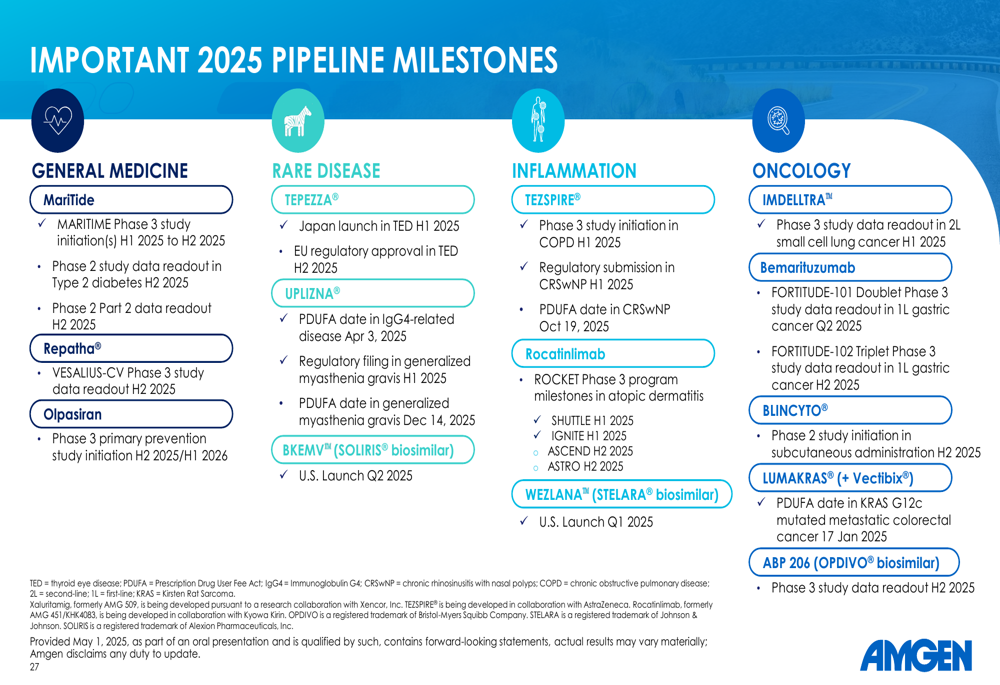

Amgen continues to advance its pipeline across all therapeutic areas. The company highlighted several key developments, including the FDA approval of UPLIZNA for the treatment of IgG4-RD in adult patients in April and positive Phase 3 data from multiple programs.

In the General Medicine pipeline, MariTide (maridebart cafraglutide, AMG 133) continues to progress with Phase 3 studies enrolling adults with overweight or obesity, with or without Type 2 diabetes mellitus. Additional Phase 3 studies across multiple indications are expected to initiate throughout 2025.

The company’s TEZSPIRE program is expanding beyond asthma, with Phase 3 studies initiated in COPD and positive data reported from the Phase 3 WAYPOINT study in patients with chronic rhinosinusitis with nasal polyps.

The following timeline highlights important pipeline milestones expected throughout 2025:

In Oncology, the company announced in April that the global Phase 3 DeLLphi-304 study of IMDELLTRA (tarlatamab) met its primary endpoint of improved overall survival in patients with small cell lung cancer who progressed on or after platinum-based chemotherapy. Detailed data will be presented at the upcoming ASCO meeting.

Additionally, the FDA granted Breakthrough Therapy Designation for subcutaneous blinatumomab in relapsed/refractory CD19-positive B-cell acute lymphoblastic leukemia, further validating the potential of this innovative delivery approach.

Financial Analysis

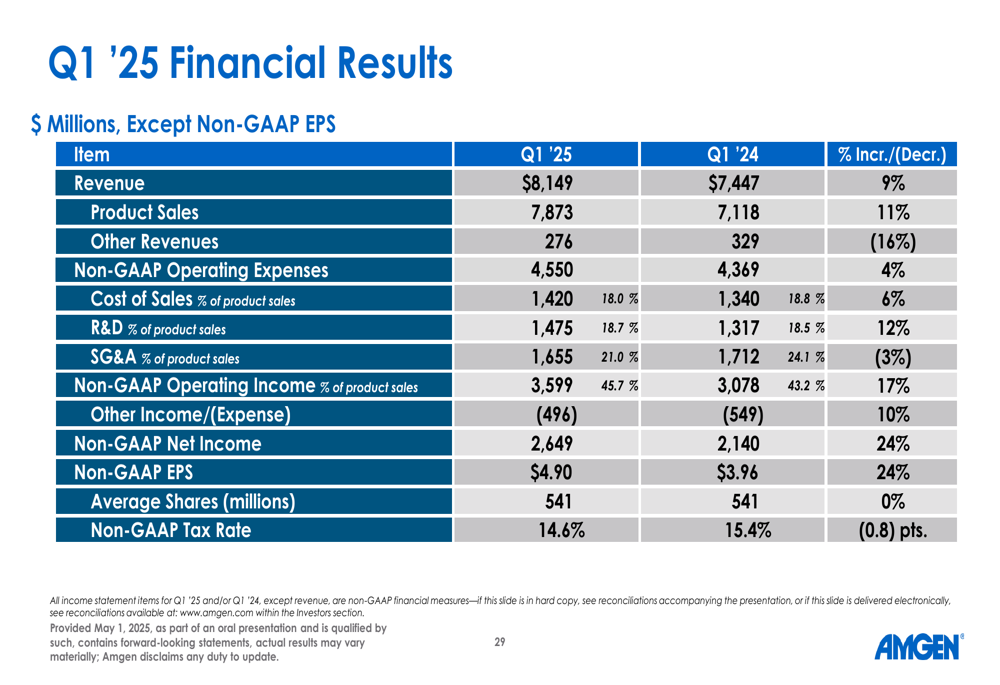

Amgen’s financial performance in Q1 2025 showed strong growth across key metrics. The following table summarizes the company’s financial results:

Non-GAAP operating income increased 17% year-over-year to $3.6 billion, while non-GAAP net income rose 24% to $2.65 billion. Non-GAAP earnings per share also increased 24% to $4.90.

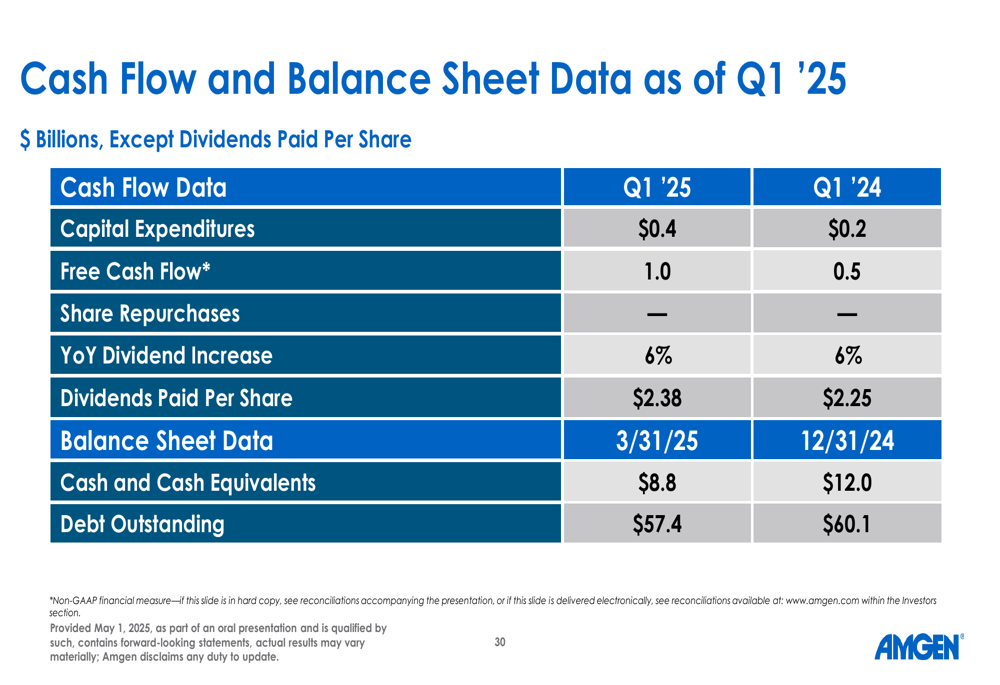

The company’s balance sheet remains solid with $8.8 billion in cash and cash equivalents, though it continues to carry substantial debt of $57.4 billion. Free cash flow for the quarter was $1.0 billion, as shown in the following slide:

Capital expenditures for the quarter were $0.4 billion, and the company paid dividends of $2.38 per share, representing a 6% increase year-over-year.

Forward Guidance

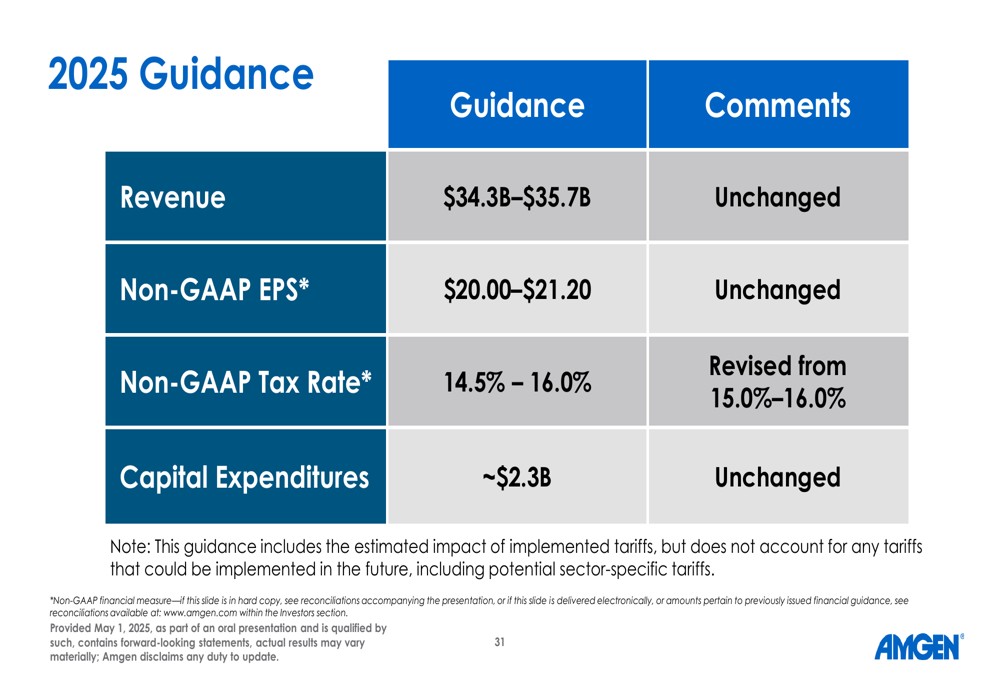

Amgen maintained its full-year 2025 guidance, projecting revenue between $34.3 billion and $35.7 billion and non-GAAP earnings per share between $20.00 and $21.20. The company expects a non-GAAP tax rate between 14.5% and 16.0% and capital expenditures of approximately $2.3 billion.

The following slide details the company’s 2025 guidance:

This guidance suggests Amgen expects continued growth throughout 2025, building on the momentum established in recent quarters. The projected revenue range represents growth from the $33.0-$33.8 billion range provided for 2024 in the previous quarter’s guidance.

The substantial capital expenditure projection of approximately $2.3 billion indicates continued investment in manufacturing capabilities and research infrastructure, particularly as the company advances key pipeline candidates like MariTide toward potential commercialization.

With a diverse portfolio of growth products across multiple therapeutic areas and a robust pipeline advancing through clinical development, Amgen appears well-positioned to maintain its growth trajectory despite facing biosimilar competition for established products like Prolia later in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.