Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

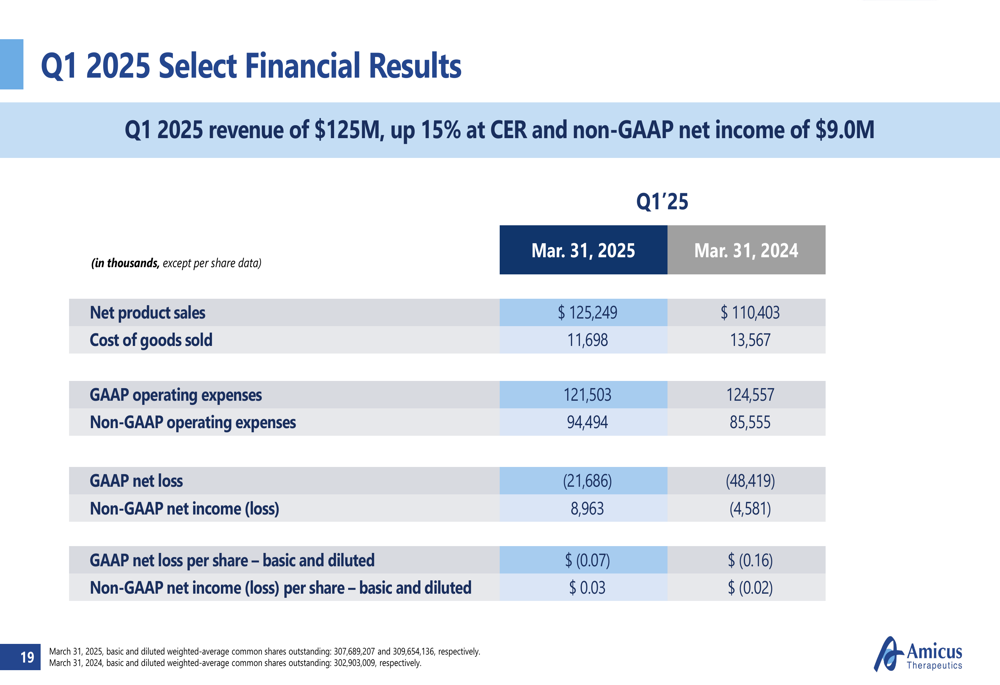

Amicus Therapeutics (NASDAQ:FOLD) reported 15% year-over-year revenue growth in its Q1 2025 financial results presentation on May 1, 2025. The rare disease-focused biotech company achieved total revenue of $125 million, driven by continued growth of its Fabry disease treatment Galafold and accelerating adoption of its Pompe disease therapy Pombiliti + Opfolda.

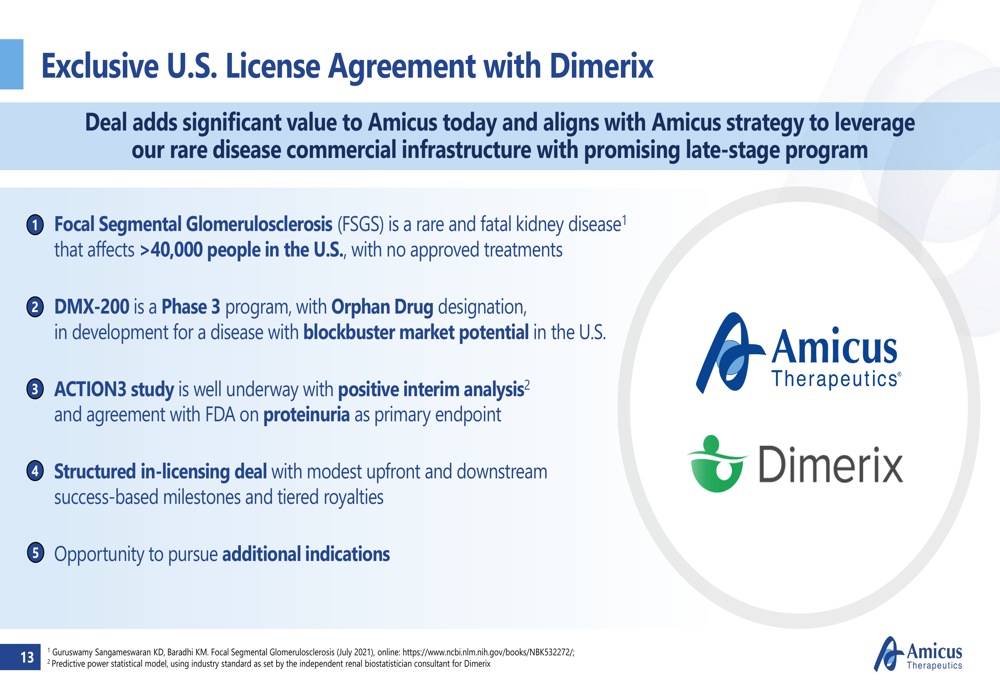

The company also announced a strategic expansion into rare kidney diseases through an exclusive U.S. licensing agreement with Dimerix for DMX-200, a Phase 3 program for focal segmental glomerulosclerosis (FSGS). This move diversifies Amicus’s portfolio beyond its current focus areas and targets a condition with no approved treatments.

Quarterly Performance Highlights

Amicus reported Q1 2025 revenue of $125 million, representing 15% growth at constant exchange rates (CER) compared to Q1 2024. The company achieved non-GAAP net income of $9.0 million ($0.03 per share), a significant improvement from a non-GAAP net loss of $4.6 million ($0.02 per share) in the same period last year.

As shown in the following financial results summary:

Galafold contributed $104.2 million in Q1 2025 revenue, representing 6% growth at CER. Meanwhile, Pombiliti + Opfolda generated $21.0 million, showing remarkable growth of 92% at CER compared to Q1 2024. The company’s GAAP net loss narrowed to $21.7 million from $48.4 million in the prior-year period, demonstrating progress toward profitability.

Product Performance

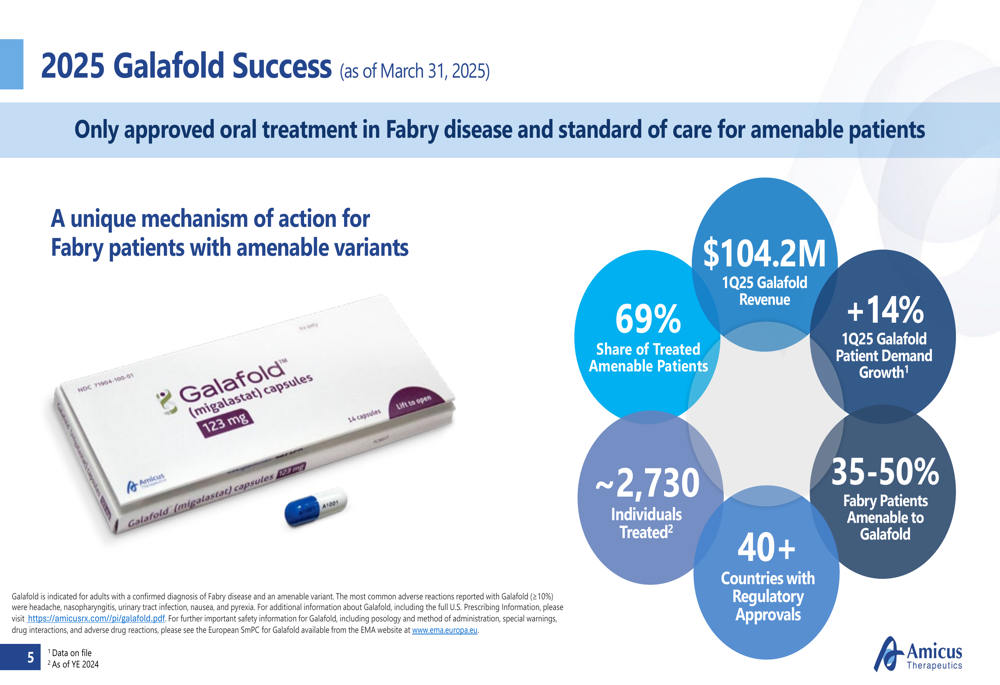

Galafold continues to be Amicus’s primary revenue driver, with the company highlighting its position as the "only approved oral treatment in Fabry disease and standard of care for amenable patients." The presentation emphasized Galafold’s strong market position, with approximately 2,730 individuals treated globally and a 69% share of treated amenable patients.

The following slide details Galafold’s market position and key metrics:

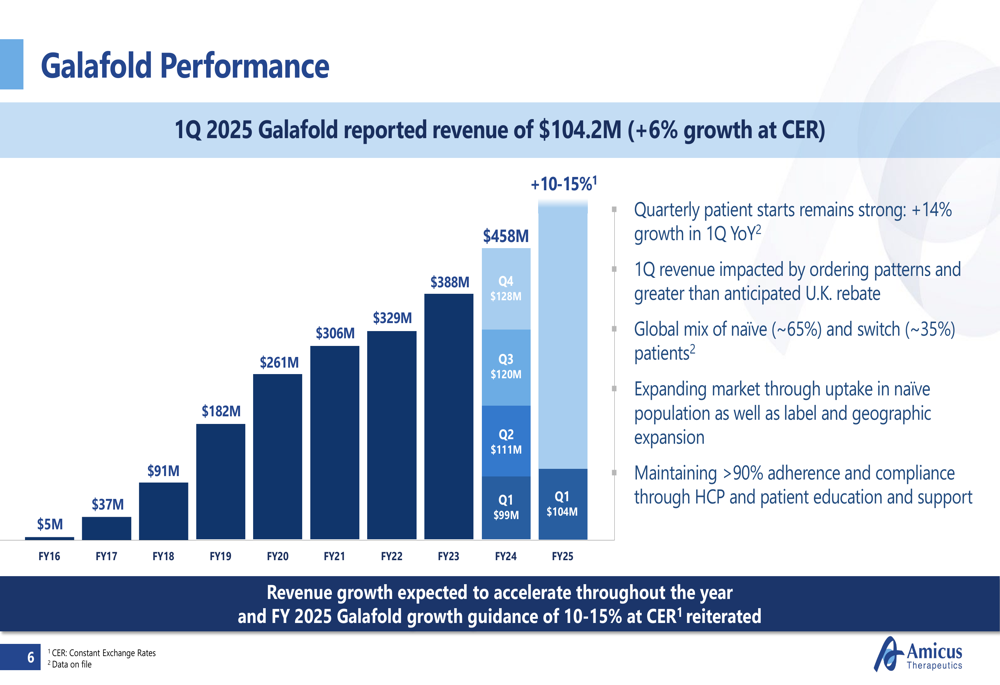

Galafold’s historical performance shows consistent growth since its launch, with annual revenue increasing from just $5 million in FY16 to $458 million in FY24. Management expects this growth trajectory to continue, reiterating FY 2025 Galafold growth guidance of 10-15% at CER.

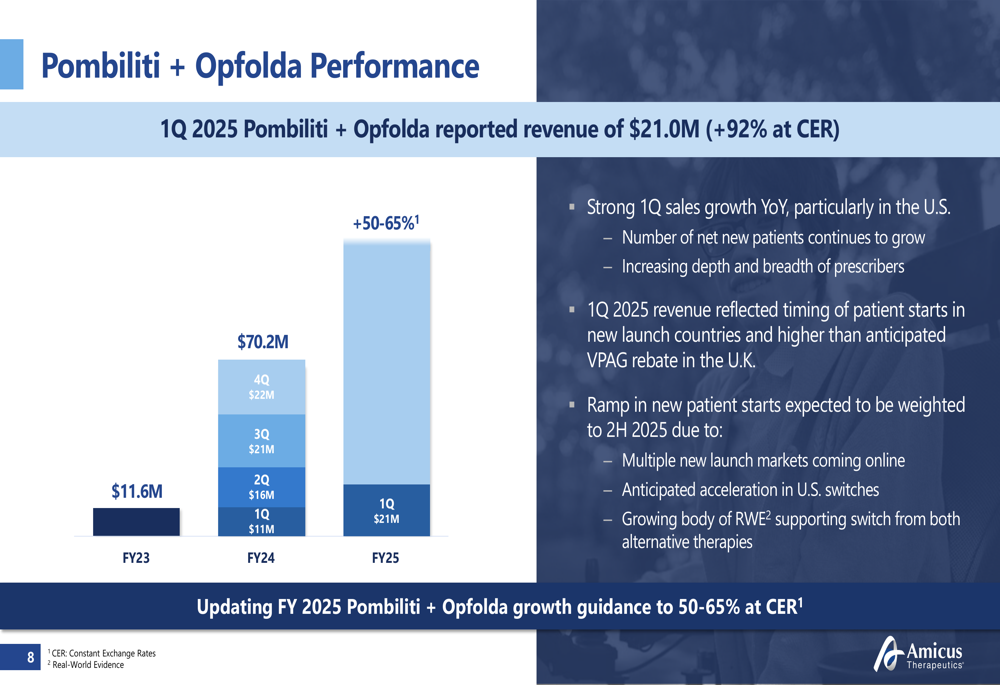

Pombiliti + Opfolda, Amicus’s treatment for late-onset Pompe disease, showed strong momentum with 92% revenue growth at CER. Management updated FY 2025 growth guidance for this product to 50-65% at CER, reflecting confidence in its commercial trajectory.

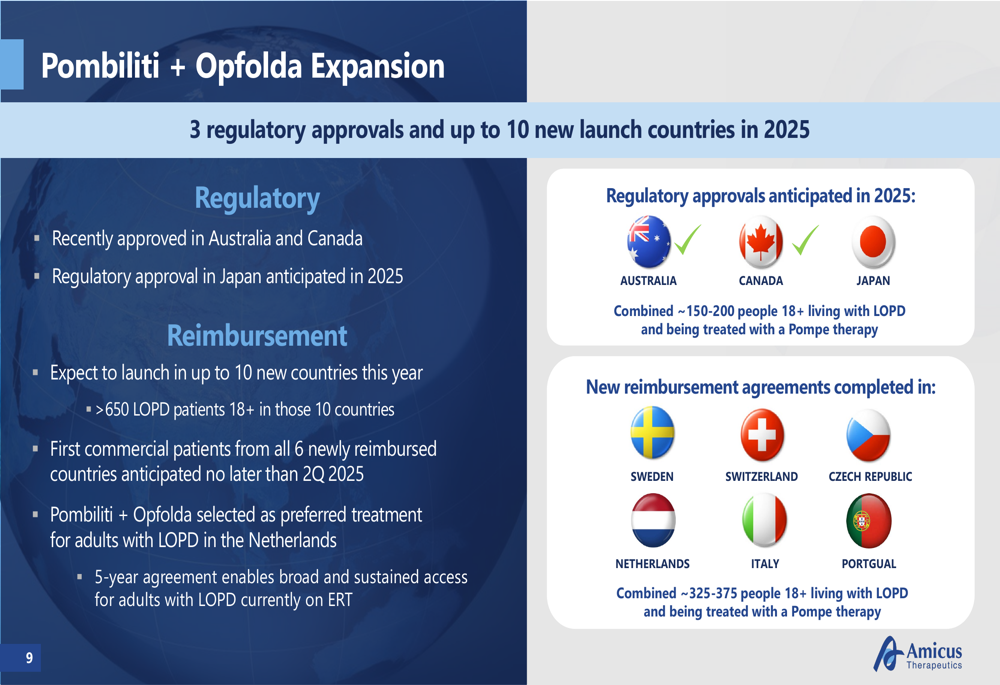

The company is expanding the global footprint of Pombiliti + Opfolda, with recent regulatory approvals in Australia and Canada, and anticipated approval in Japan in 2025. Amicus plans to launch in up to 10 new countries this year, targeting more than 650 late-onset Pompe disease patients aged 18 and older across these markets.

Strategic Expansion

A significant development announced in the presentation was Amicus’s exclusive U.S. licensing agreement with Dimerix for DMX-200, a Phase 3 program for FSGS, a rare kidney disease affecting more than 40,000 people in the United States with no approved treatments.

The following slide outlines the key aspects of this strategic partnership:

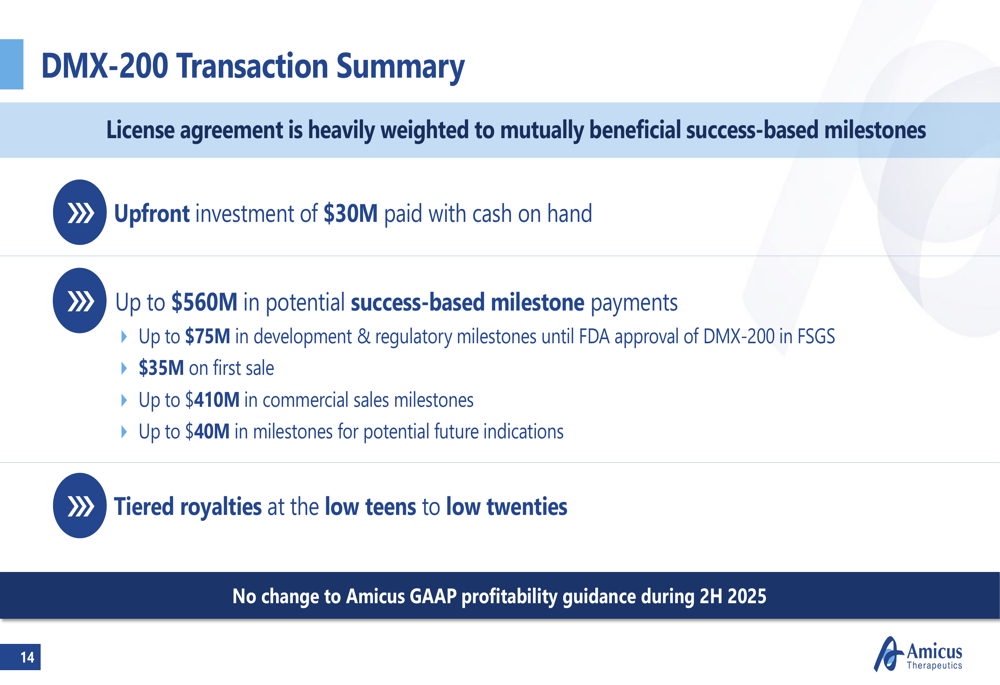

The transaction includes a $30 million upfront investment paid with cash on hand, with potential success-based milestone payments of up to $560 million. These include up to $75 million in development and regulatory milestones until FDA approval, $35 million on first sale, up to $410 million in commercial sales milestones, and up to $40 million for potential future indications, along with tiered royalties.

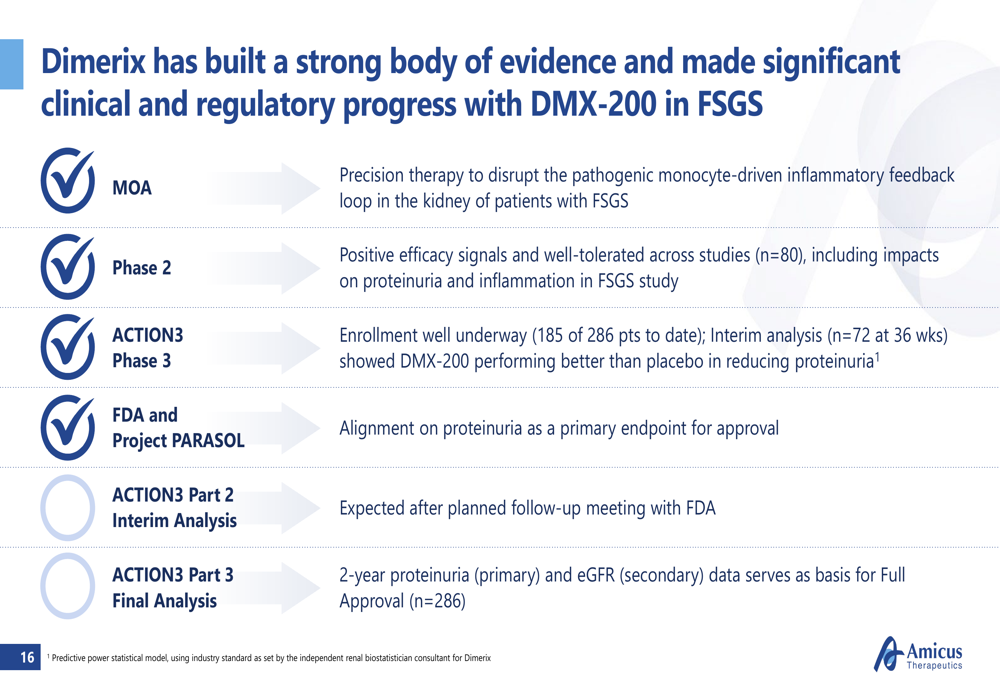

The DMX-200 program is well-advanced, with the Phase 3 ACTION3 study already enrolling patients. An interim analysis of 72 patients at 36 weeks showed DMX-200 performing better than placebo in reducing proteinuria, and the FDA has agreed on proteinuria as a primary endpoint for approval.

Financial Outlook

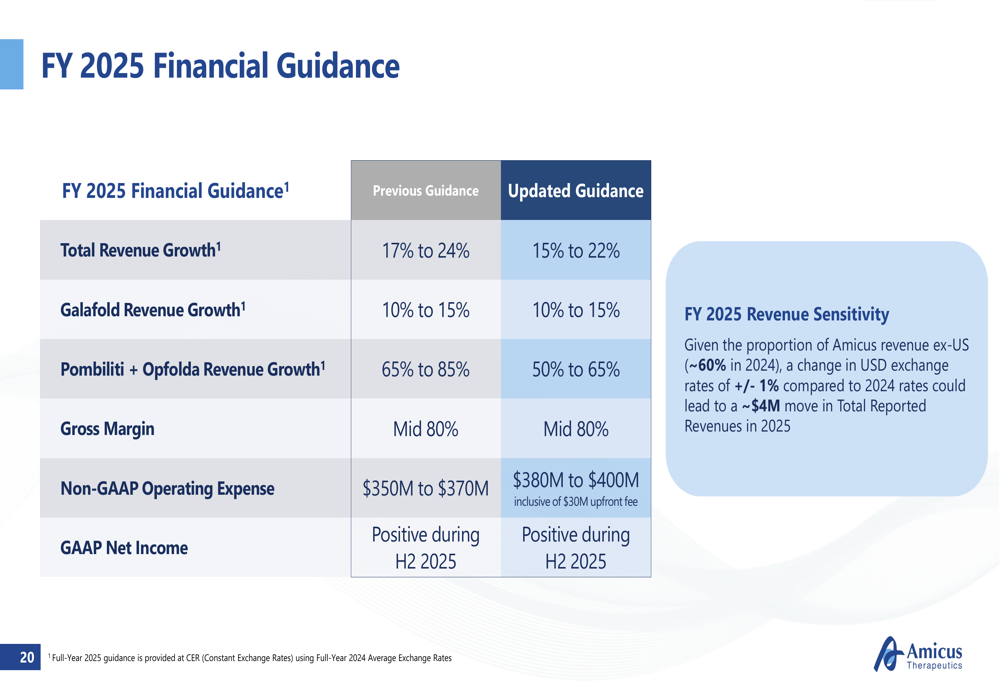

Amicus updated its financial guidance for FY 2025, projecting total revenue growth of 15-22%, with Galafold revenue growth of 10-15% and Pombiliti + Opfolda revenue growth of 50-65% at CER. The company expects gross margins in the mid-80% range and non-GAAP operating expenses of $380-400 million, inclusive of the $30 million upfront fee for DMX-200.

The following slide details the company’s updated financial guidance:

Notably, Amicus expects to achieve positive GAAP net income during the second half of 2025, marking an important milestone in its path to sustainable profitability. The company projects surpassing $1 billion in total annual revenue by FY 2028, driven by continued growth of its existing products and potential contributions from pipeline assets.

Forward-Looking Statements

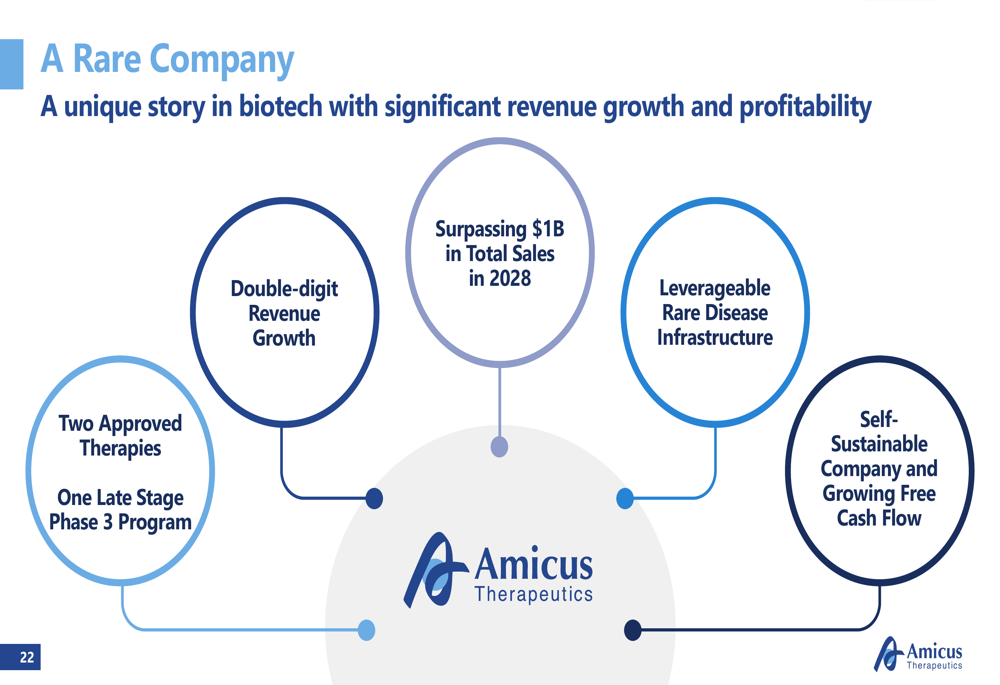

Amicus outlined its strategic priorities for 2025, focusing on delivering revenue growth, advancing clinical studies, and achieving GAAP profitability. The company emphasized its position as "a rare company" with two approved therapies and one late-stage Phase 3 program, projecting double-digit revenue growth and leverageable rare disease infrastructure.

Management highlighted the company’s transition to a self-sustainable business model with growing free cash flow, positioning Amicus for long-term success in the rare disease space. The DMX-200 licensing deal represents a strategic expansion into rare kidney diseases, complementing the company’s existing focus on Fabry and Pompe diseases.

While the presentation was generally positive, investors should note that the stock was down 2.47% in premarket trading on the day of the announcement, suggesting potential market concerns about aspects of the quarterly results or forward guidance. The recent performance represents a significant pullback from the company’s 52-week high of $12.65, with the stock trading near $7.49 in premarket activity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.