Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Amphastar Pharmaceuticals (NASDAQ:AMPH) presented its corporate strategy on May 7, 2025, highlighting a significant pivot toward proprietary and biosimilar products amid recent financial headwinds. The presentation comes after the company’s disappointing Q4 2024 results, where it missed analyst expectations with an EPS of $0.92 against a forecast of $0.97, causing an 11% stock drop. Currently trading at $24.43, Amphastar remains well below its 52-week high of $53.96.

Strategic Initiatives

Amphastar’s presentation emphasized a fundamental transformation of its business model, moving away from its historical reliance on generic drugs toward higher-margin proprietary and biosimilar products. This strategic evolution is projected to dramatically reshape the company’s pipeline composition by 2026.

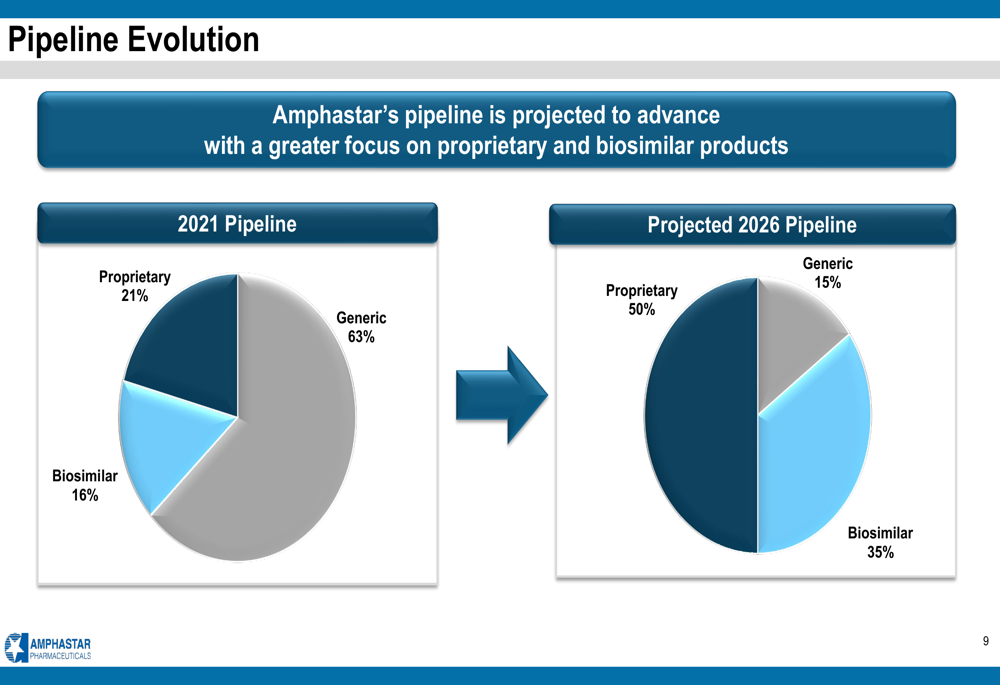

As shown in the following chart of Amphastar’s pipeline evolution:

The company plans to reduce its generic portfolio from 63% in 2021 to just 15% by 2026, while increasing proprietary products from 21% to 50% and biosimilars from 16% to 35%. This shift aligns with Amphastar’s "Three-H Focus" strategy of High Quality, High Efficiency, and High Technology, which has contributed to significant margin expansion in recent years.

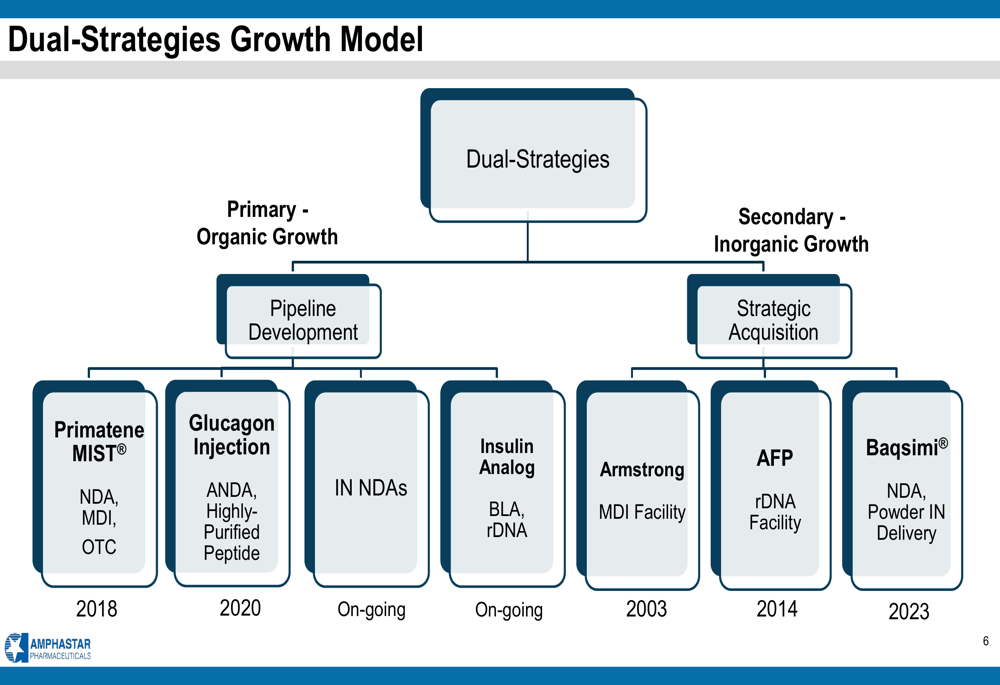

The company’s strategic approach is built on a dual-growth model combining organic pipeline development with strategic acquisitions:

Detailed Financial Analysis

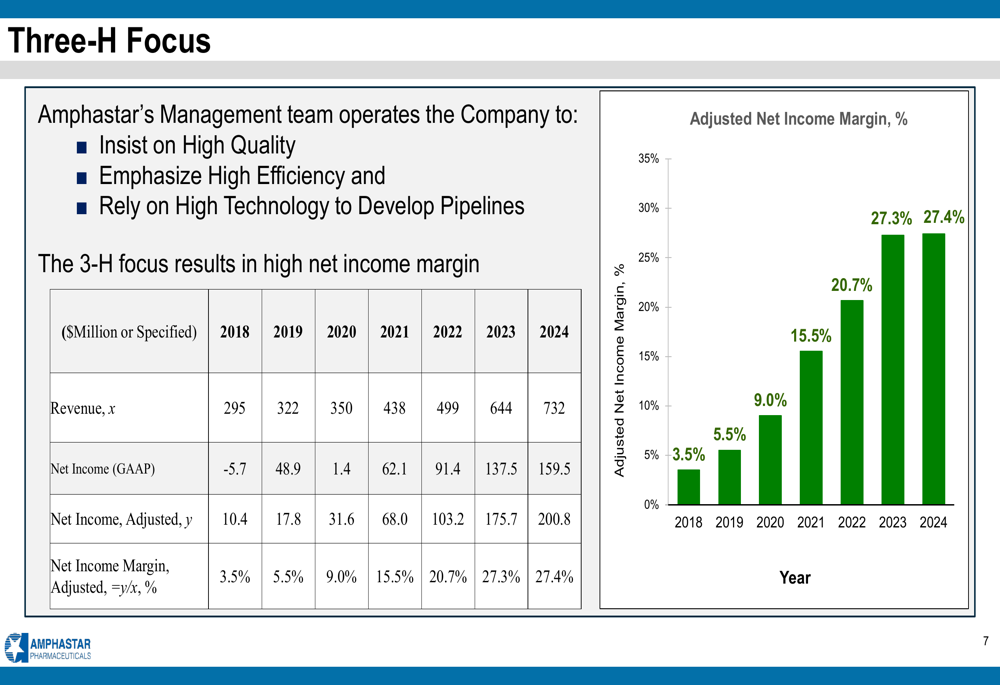

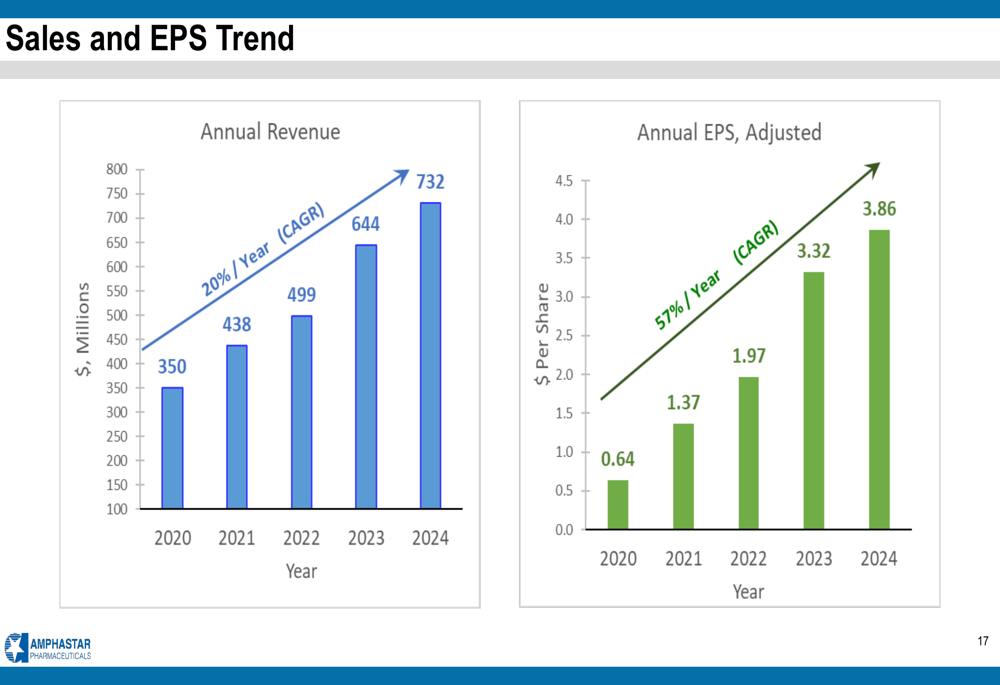

Historically, Amphastar has demonstrated strong financial performance, with revenue growing from $295 million in 2018 to $732 million in 2024, representing a 20% compound annual growth rate (CAGR) from 2020-2024. More impressively, adjusted net income margin expanded from just 3.5% in 2018 to 27.4% in 2024.

The following chart illustrates this margin expansion:

Similarly, adjusted earnings per share grew at a 57% CAGR between 2020 and 2024, reaching $3.86 per share last year:

However, recent quarterly performance has shown signs of pressure. The company’s Q4 2024 results revealed declining gross margins (46.5%, down from 54% year-over-year) and revenue that fell short of analyst expectations. This contrast between long-term growth and recent challenges suggests Amphastar may be experiencing headwinds as it navigates its strategic transition.

Competitive Industry Position

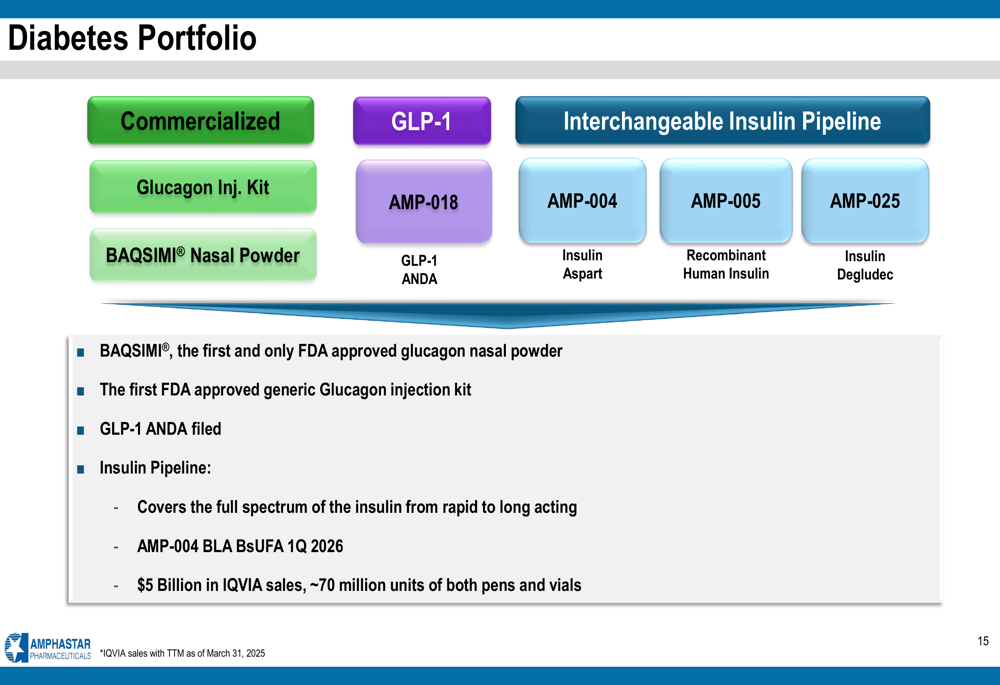

Amphastar’s diabetes portfolio has emerged as a cornerstone of its proprietary product strategy. The company has built a comprehensive offering spanning treatment options for diabetes patients:

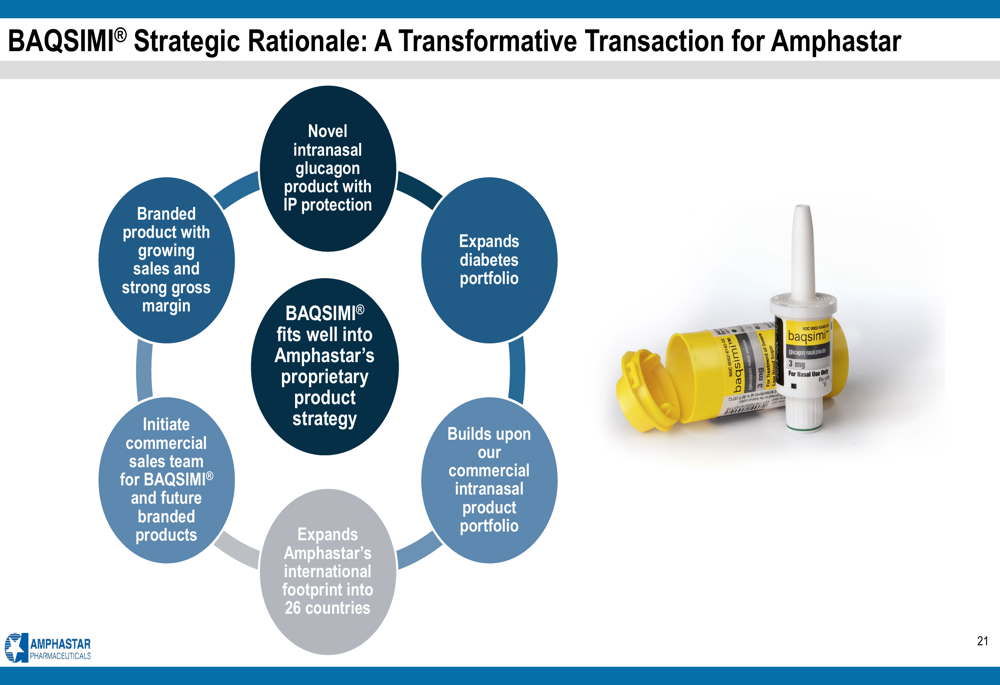

The 2023 acquisition of BAQSIMI, a nasal glucagon powder for severe hypoglycemia, represents a pivotal element of this strategy. BAQSIMI is the first and only FDA-approved glucagon nasal powder, offering significant advantages over traditional injection kits.

The strategic rationale for the BAQSIMI acquisition extends beyond product diversification:

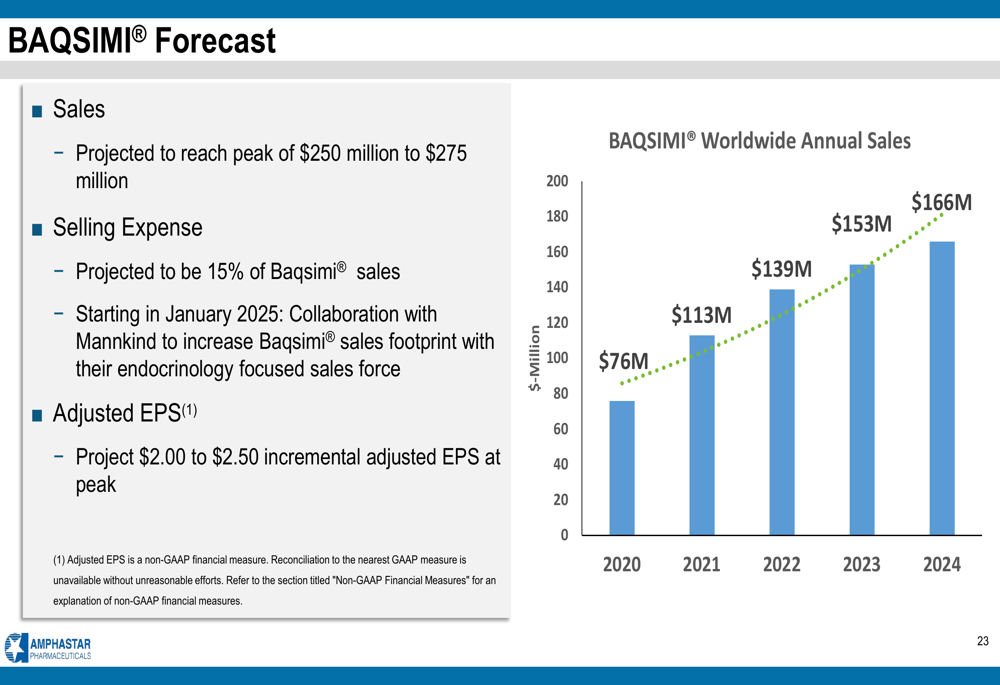

Amphastar projects BAQSIMI to reach peak sales of $250-275 million, with a collaboration with MannKind (NASDAQ:MNKD) beginning in January 2025 to expand its sales footprint:

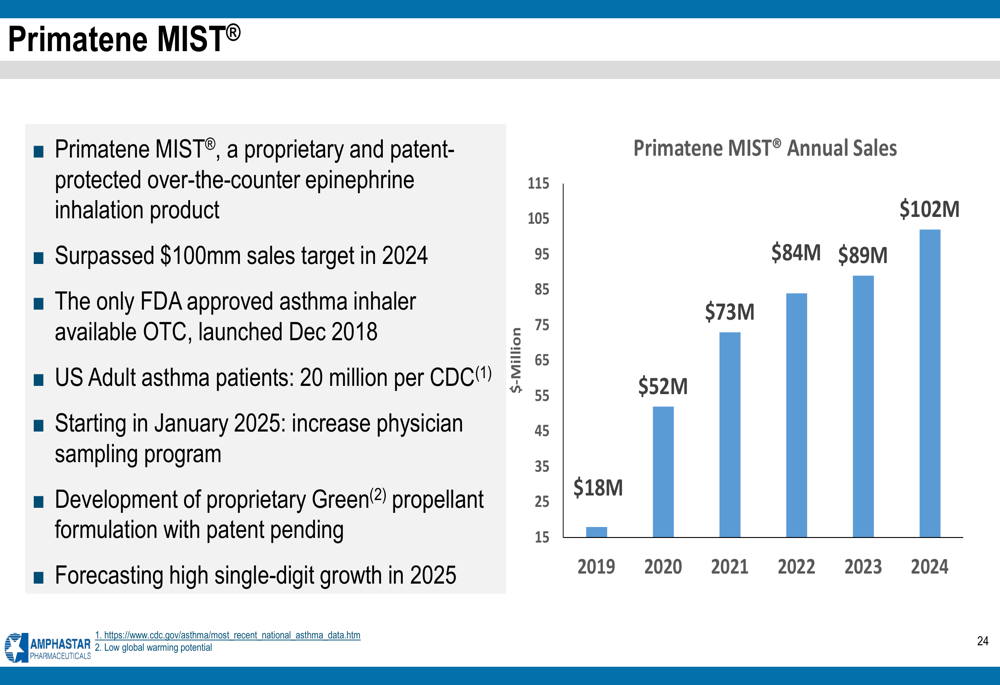

Another key proprietary product is Primatene MIST, an over-the-counter epinephrine inhalation product for asthma symptoms. The product surpassed $100 million in sales in 2024, growing steadily since its 2018 launch:

Forward-Looking Statements

Despite the company’s optimistic presentation, management has tempered near-term expectations, projecting flat sales in 2025 before returning to growth in 2026. This outlook contrasts with the presentation’s emphasis on upcoming catalysts and pipeline developments.

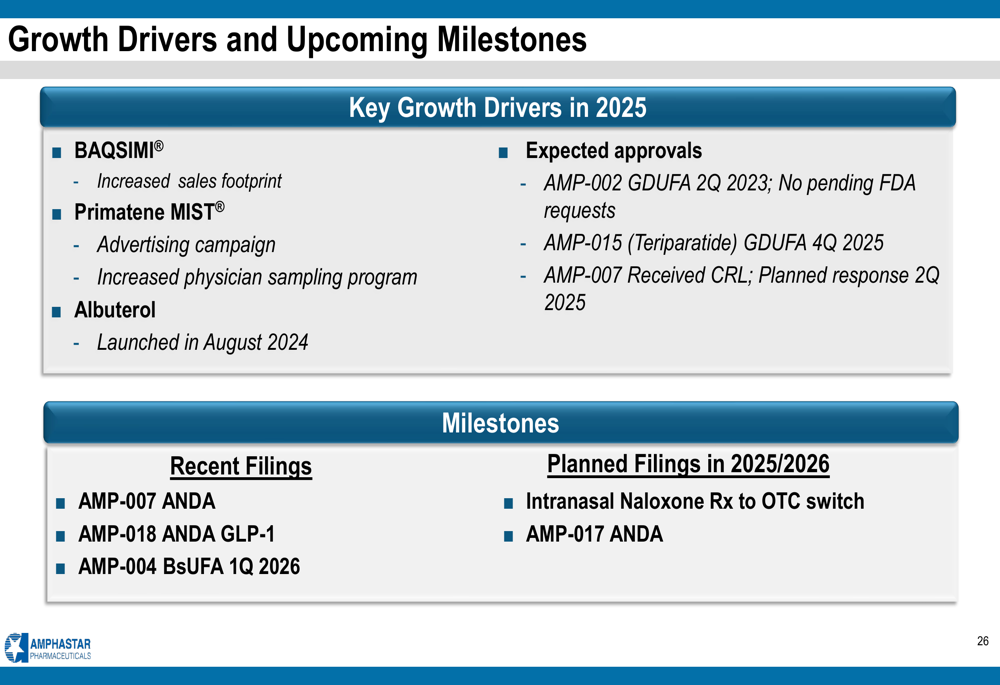

Key growth drivers for 2025 include continued expansion of BAQSIMI and Primatene MIST, while the pipeline features several potential approvals and filings:

Particularly significant is the company’s insulin biosimilar program, with AMP-004 targeting a BsUFA date in Q1 2026. This product aims at a $5 billion market with approximately 70 million units of both pens and vials.

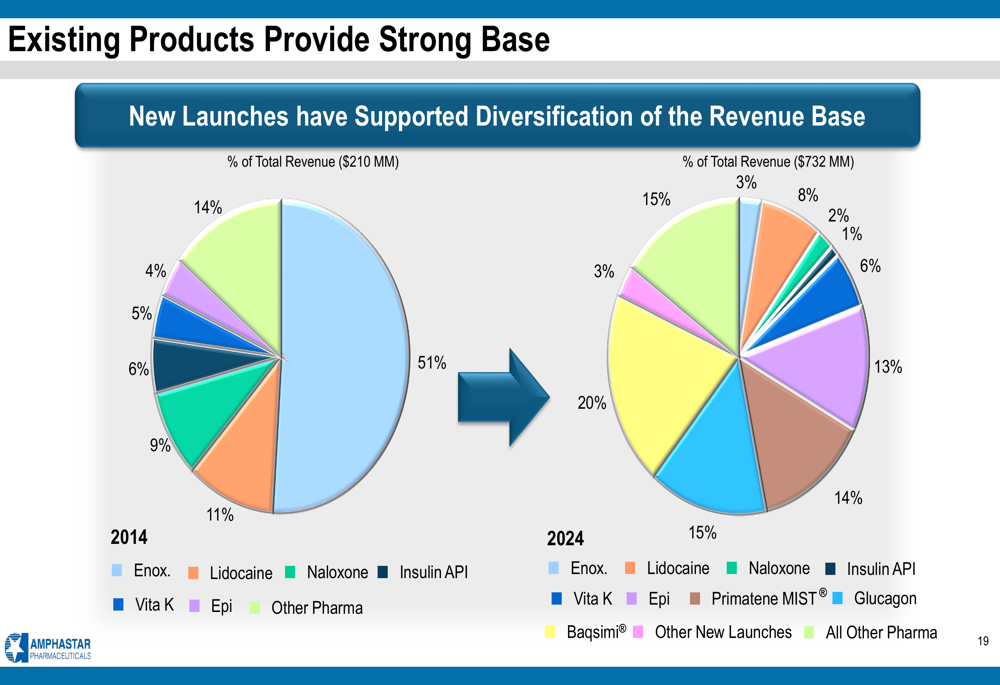

The company’s product revenue base has diversified significantly since 2014, reducing dependency on any single product:

Analyst Perspectives

While Amphastar’s presentation paints an optimistic picture of its strategic transformation, analysts have expressed concerns about the company’s ability to meet financial targets amid declining margins and competitive pressures. The recent earnings miss has raised questions about the timeline for realizing the benefits of the company’s strategic shift.

However, according to available data, the stock may be undervalued at current levels, trading at a P/E ratio of 9.65. Management has been actively buying back shares, and analysts maintain price targets suggesting significant upside potential from current levels.

As Amphastar navigates its transition toward higher-margin proprietary products, investors will be closely watching whether the company can overcome near-term challenges to deliver on its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.