Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Amplify Energy Corp (NYSE:AMPY) presented its August 2025 investor presentation on August 6, highlighting the company’s strategic focus on its Beta field development while divesting non-core assets. The presentation comes as the company’s stock trades at $3.76, down 1.05% on the day and significantly below its 52-week high of $7.76.

The oil and gas producer, which recently reported strong Q1 2025 earnings with EPS of $3.8 (vastly exceeding forecasts of $0.21), is working to convince investors of its underlying value proposition despite recent negative free cash flow.

Strategic Initiatives

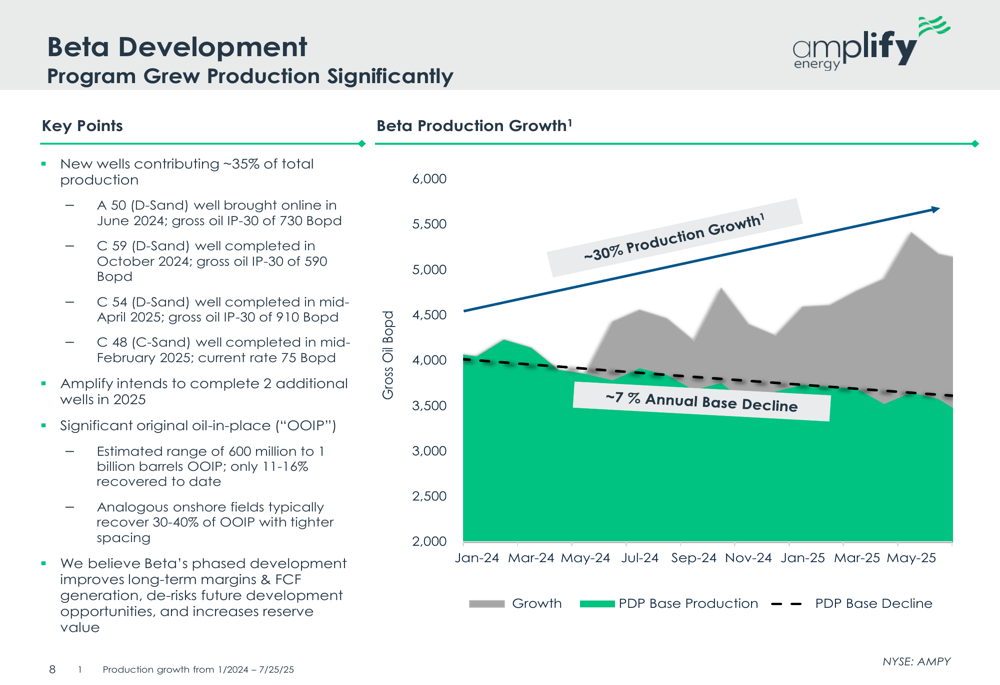

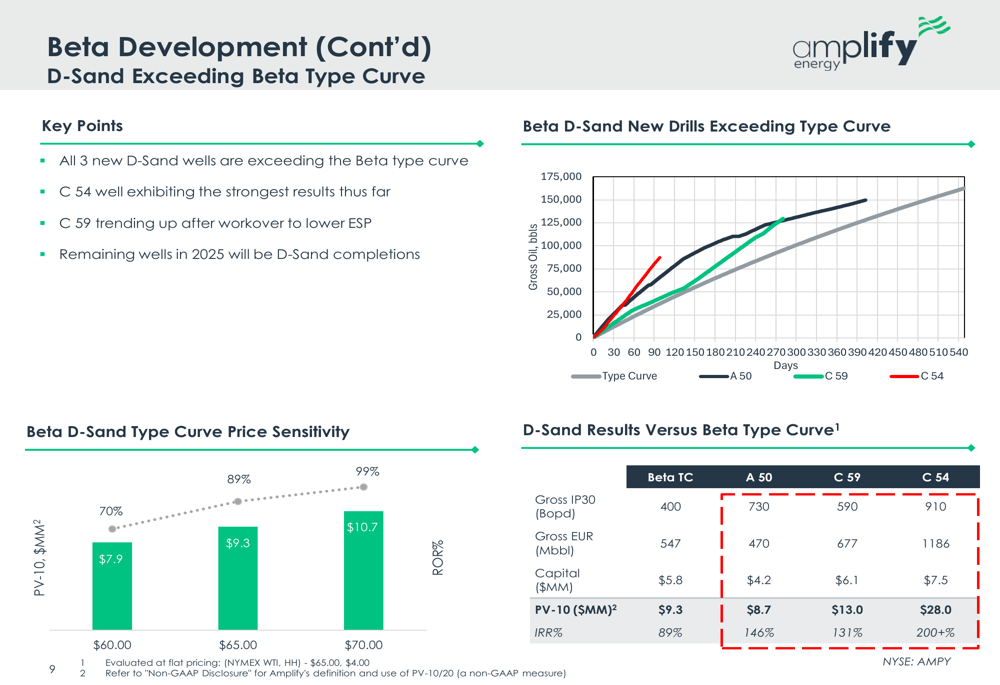

Amplify’s presentation emphasized its successful Beta field development program, which has contributed approximately 35% of the company’s total production. The company completed four development wells in 2025, with all three new D-Sand wells exceeding the Beta type curve.

As shown in the following chart of Beta’s production growth versus base decline, the development program has achieved approximately 30% production growth against a modest 7% base decline:

The company highlighted that its Beta wells are significantly outperforming the type curve, with the C 54 well exhibiting particularly strong results at 850 barrels of oil per day (gross). This performance translates to superior economics compared to other U.S. basins:

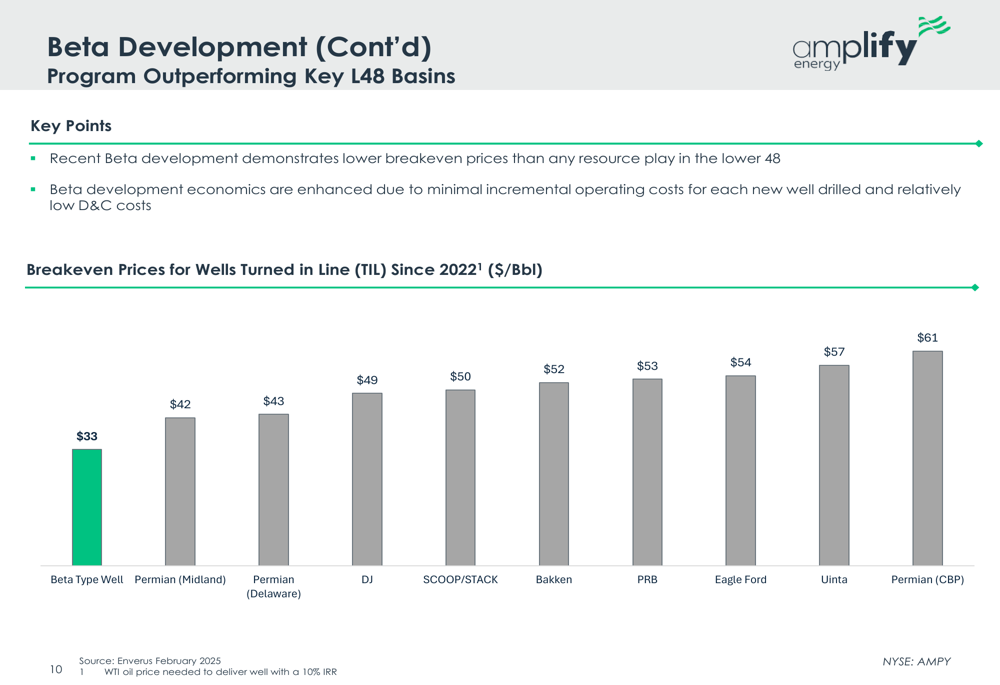

A key competitive advantage for Amplify is the lower breakeven prices of its Beta development program compared to major U.S. basins. The presentation showed Beta wells achieving a $33 breakeven price, substantially below the $42-61 range seen in other key regions:

Simultaneously, Amplify is pursuing portfolio optimization through asset sales. The company has already divested its non-operated Eagle Ford asset for $23 million and is currently marketing its East Texas and Oklahoma assets. This strategy aims to focus the portfolio on its highest-return opportunities while strengthening the balance sheet.

Financial Performance & Outlook

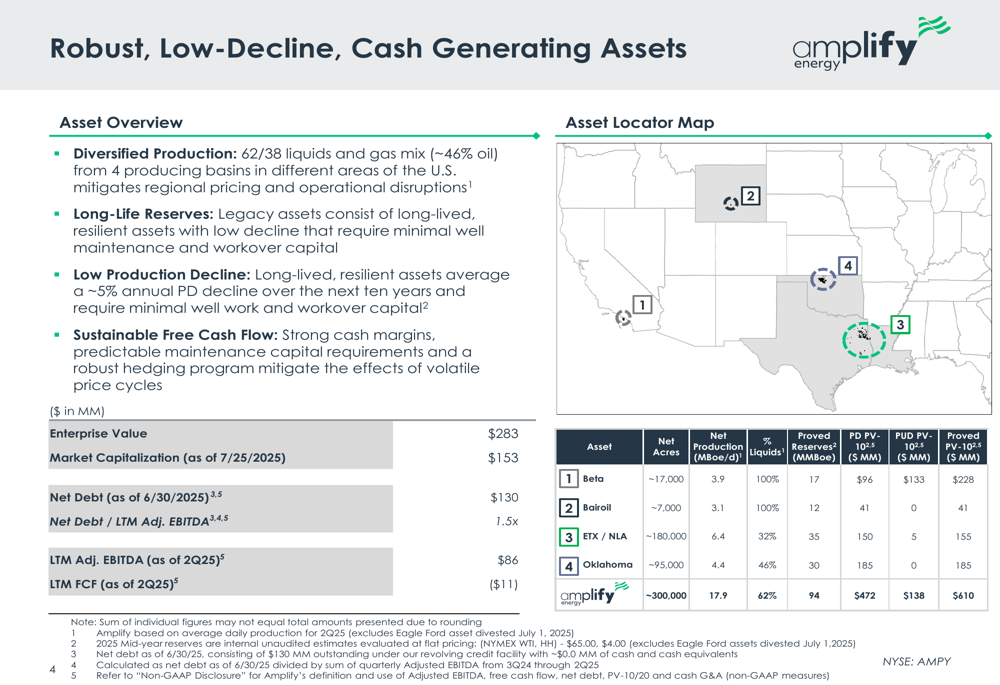

Amplify reported an enterprise value of $283 million, comprising a market capitalization of $153 million (as of July 25, 2025) and net debt of $130 million (as of June 30, 2025). The company has reduced its net debt by approximately $60 million since year-end 2022, lowering its leverage ratio from 2.0x to 1.5x.

The company’s asset portfolio is diversified across four producing basins with a 62/38 liquids and gas mix (approximately 46% oil). These assets feature a low annual production decline rate of about 5%, which supports sustainable cash flow generation.

The following slide provides a comprehensive overview of Amplify’s assets and key financial metrics:

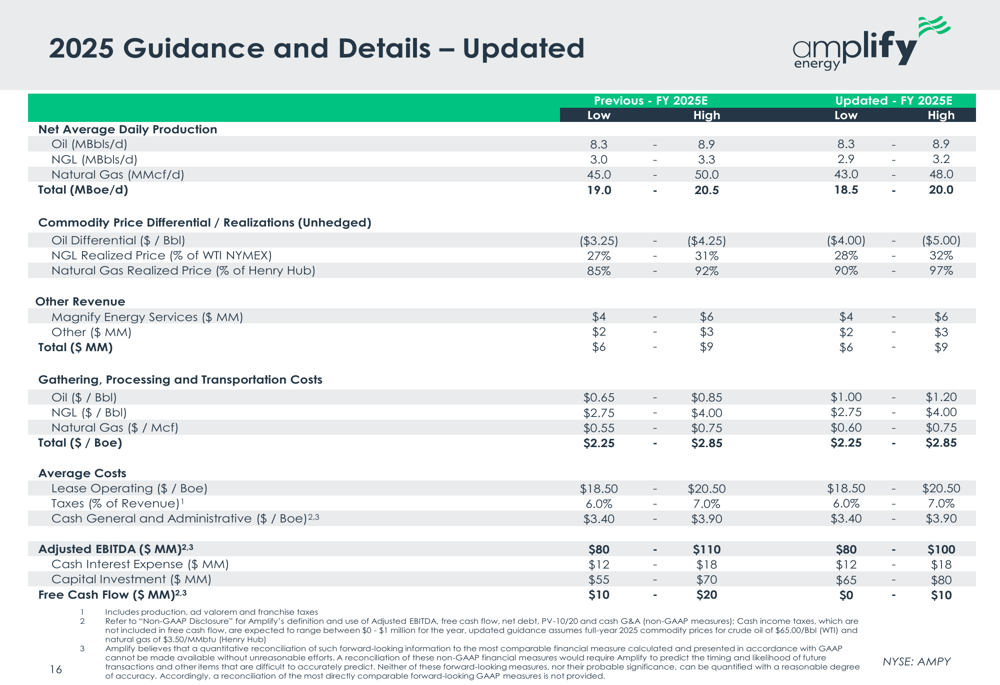

For 2025, Amplify provided the following updated guidance:

Despite reporting negative free cash flow of $11 million for the last twelve months, management projects positive free cash flow of $0-10 million for 2025. This improvement is expected to come from operational efficiencies and the company’s robust hedging program, which provides downside protection in weak commodity environments.

Valuation & Investment Thesis

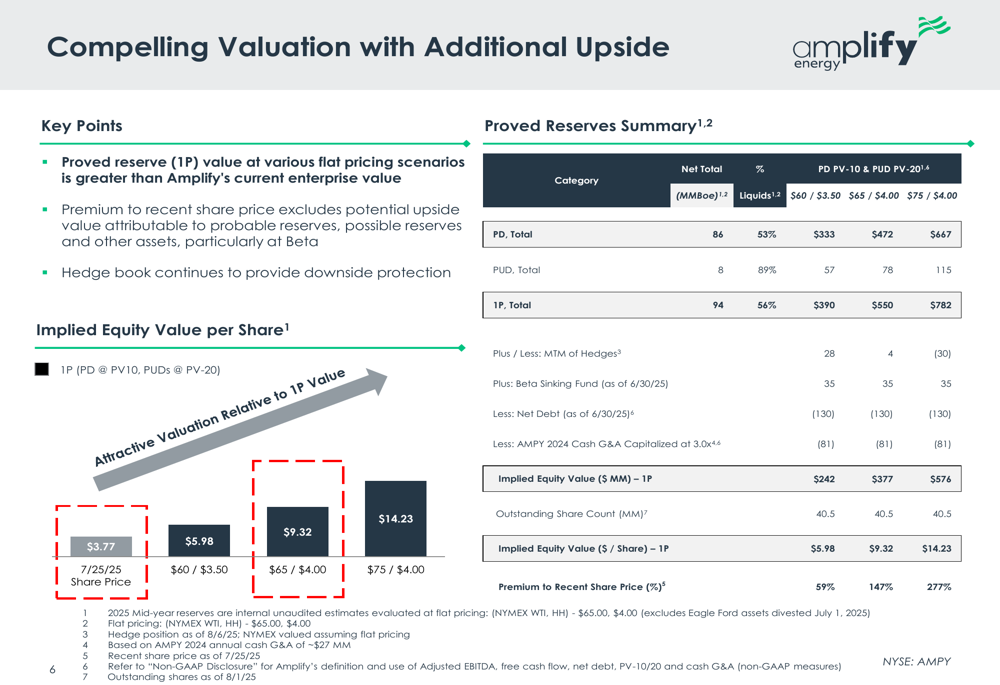

A central theme of Amplify’s presentation was the significant disconnect between its current market valuation and the implied value of its proved reserves. At $65 oil and $4.00 natural gas pricing, the company calculates an implied equity value of $9.32 per share, representing a 147% premium to its recent share price.

The following chart illustrates this valuation gap across various commodity price scenarios:

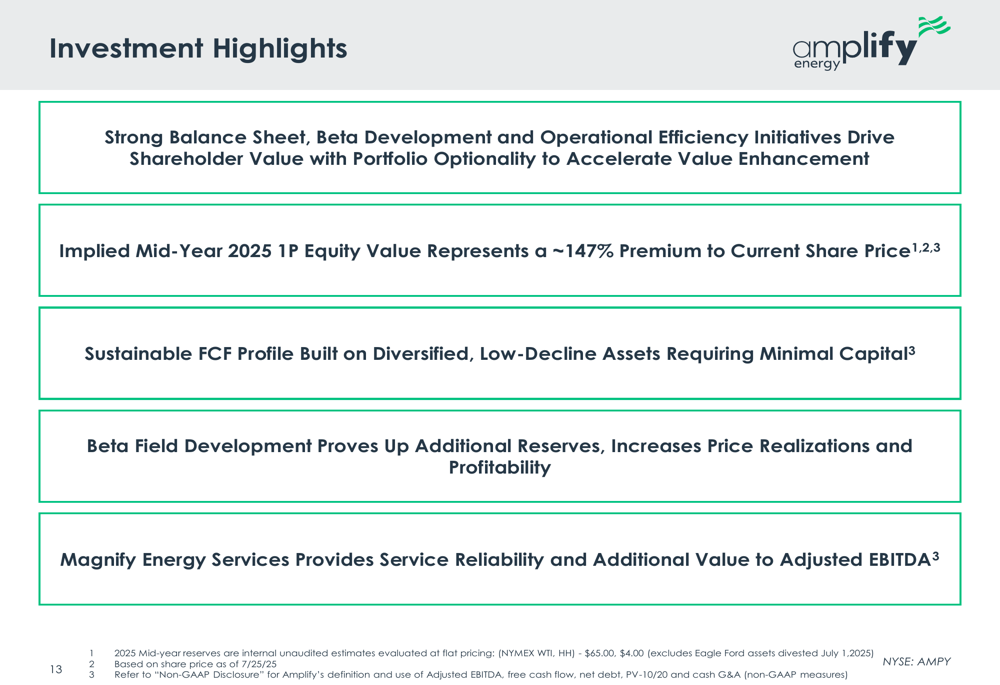

Amplify’s investment thesis rests on several key pillars:

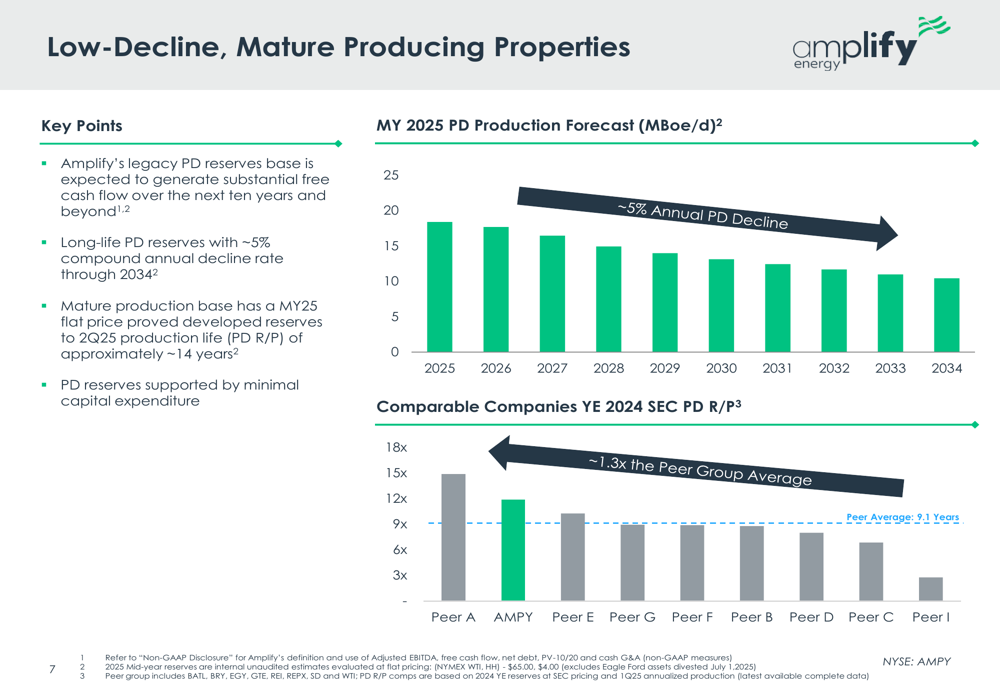

The company’s mature, low-decline production base is expected to generate substantial free cash flow over the next decade with minimal capital expenditure. Amplify’s proved developed reserves to production ratio (PD R/P) of approximately 14 years exceeds the peer average, as shown in this comparative analysis:

Risks & Challenges

While Amplify’s presentation painted an optimistic picture, several challenges remain. The company’s Q1 2025 results showed Adjusted EBITDA of $19.4 million, down $2.4 million from the previous quarter. If annualized, this would fall below the lower end of the company’s 2025 guidance range of $80-100 million.

The company’s ability to achieve positive free cash flow in 2025 remains uncertain given the negative $11 million FCF over the last twelve months. This execution risk is reflected in the stock’s current trading price, which sits well below both the 52-week high of $7.76 and the company’s calculated implied value.

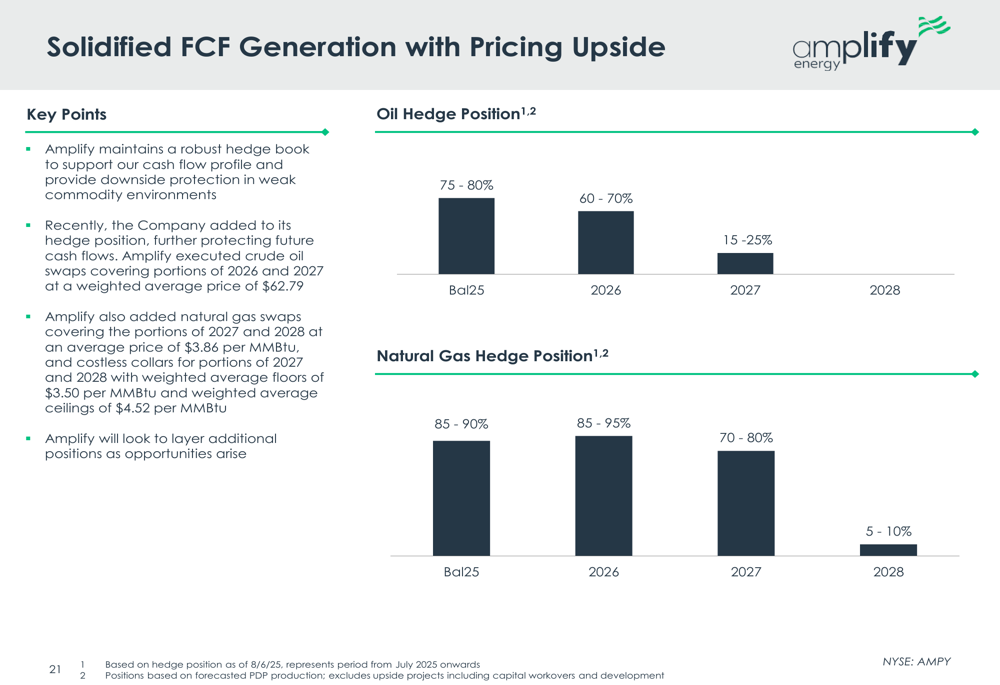

Amplify’s future performance remains heavily dependent on oil prices, though the company has mitigated some of this risk through its hedging program. As shown in the following chart, Amplify maintains a robust hedge book to protect cash flow:

Additionally, the successful execution of the company’s asset divestiture strategy will be crucial for streamlining operations and strengthening the balance sheet. During the Q1 earnings call, management emphasized their target of reducing leverage to 0.5-1x and noted that further development at Beta is contingent on oil prices reaching the $60s.

With a P/E ratio of 10.03 and a Price/Book multiple of just 0.31, Amplify presents a potentially undervalued opportunity for investors willing to bet on the company’s ability to execute its strategic initiatives and capitalize on its Beta field success in an uncertain commodity price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.