Gold prices rise from 2-wk low with focus on Russia-Ukraine, Jackson Hole

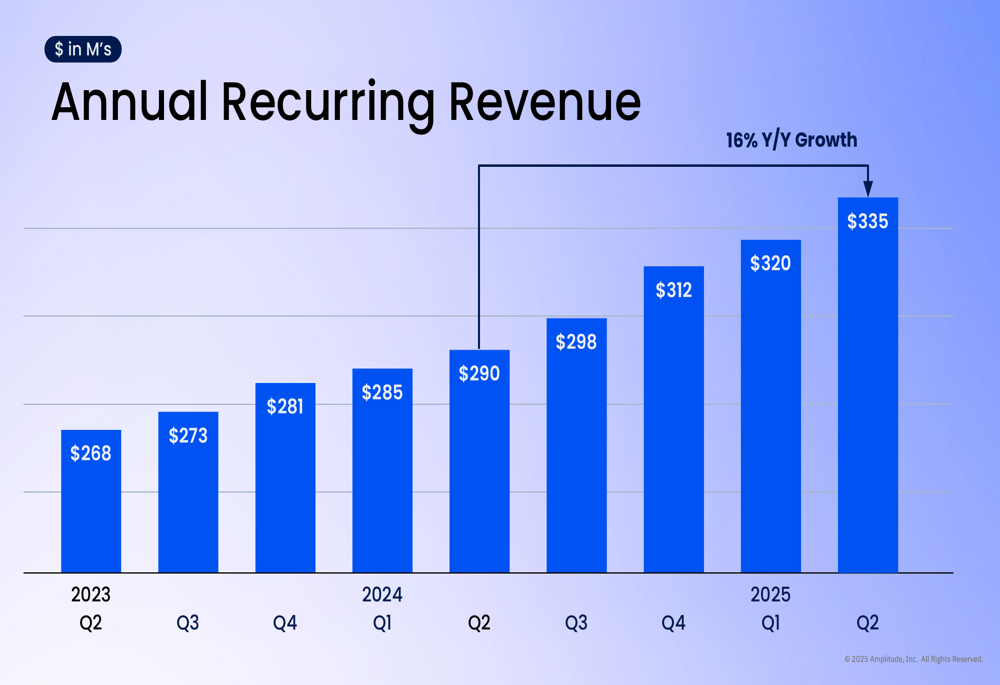

Amplitude Inc (NASDAQ:AMPL) released its second quarter 2025 investor presentation on August 6, showcasing accelerating revenue growth and improved customer metrics. The digital analytics platform provider reported $83.3 million in revenue, up 14% year-over-year, while its annual recurring revenue (ARR) reached $335 million, representing a 16% increase compared to the same period last year.

Quarterly Performance Highlights

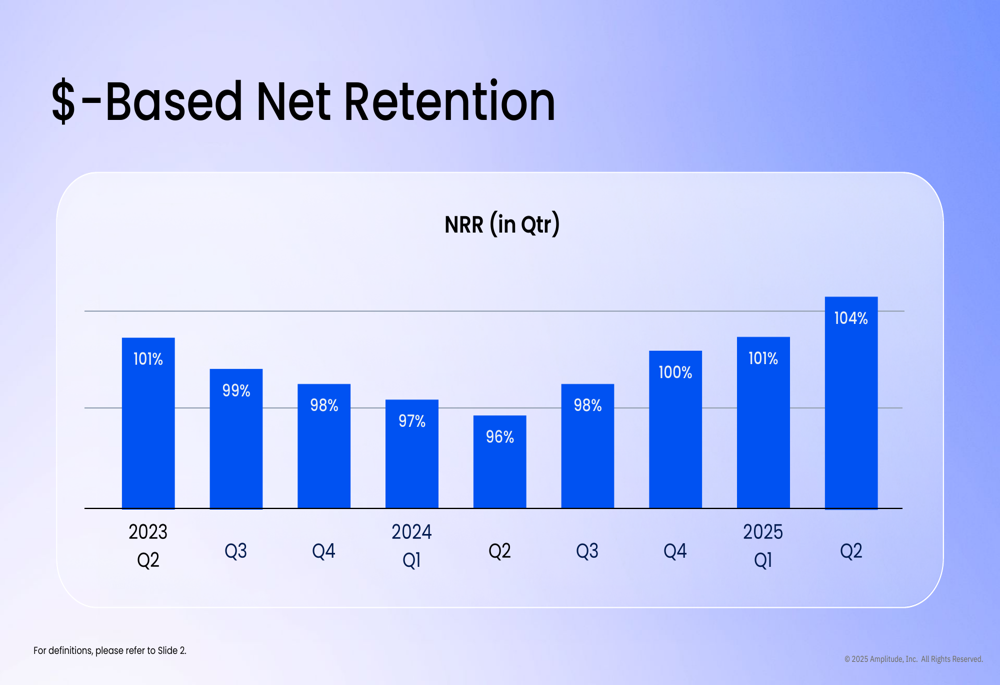

Amplitude demonstrated improved performance across key metrics in Q2 2025. The company’s dollar-based net retention rate reached 104%, a significant improvement from 96% in Q2 2024, indicating stronger customer expansion and reduced churn. This marks the third consecutive quarter of improvement in this critical SaaS metric.

As shown in the following chart of quarterly revenue growth, Amplitude has maintained consistent revenue expansion:

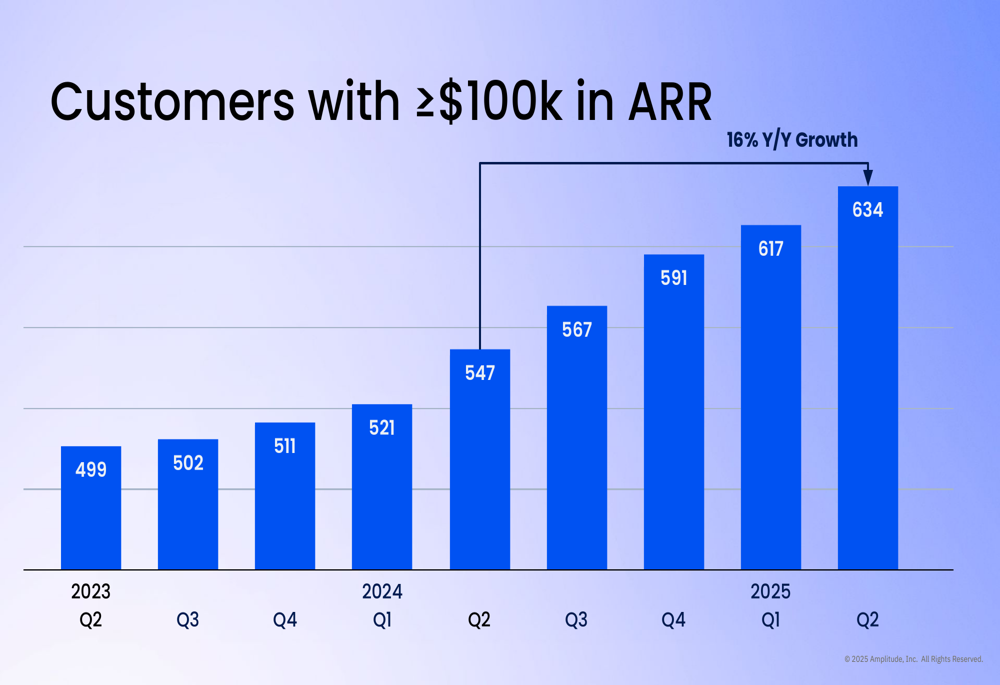

The company’s customer base continued to grow, with 634 customers generating over $100,000 in ARR, a 16% year-over-year increase. This enterprise customer growth has been a consistent trend over the past two years:

Amplitude’s CFO highlighted the company’s improving financial efficiency, with free cash flow reaching $18.2 million in Q2, compared to $6.8 million in the same quarter last year. The company maintains a strong balance sheet with $288 million in cash and investments.

Detailed Financial Analysis

Amplitude’s ARR growth has accelerated in recent quarters, reaching $335 million in Q2 2025, up 16% year-over-year. This represents an improvement from the 12% ARR growth reported in Q1 2025.

The following chart illustrates Amplitude’s ARR progression over the past two years:

A key driver of Amplitude’s improved performance has been the recovery in customer retention rates. After declining through 2023 and early 2024, the net retention rate has steadily improved to 104% in the most recent quarter:

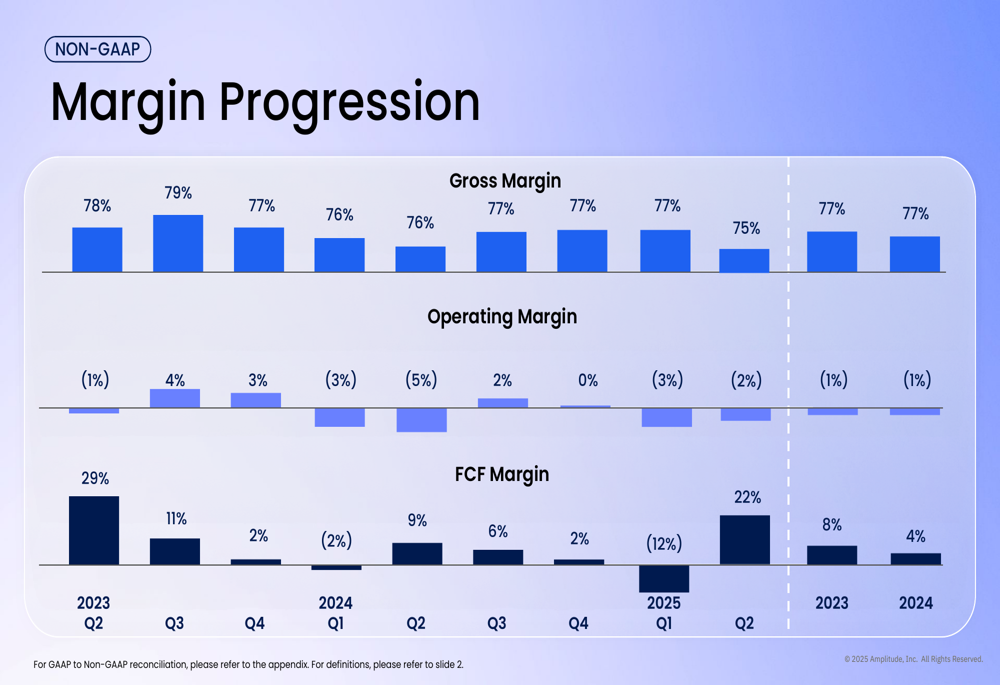

The company has also made significant progress in improving its margins across multiple dimensions. As shown in the following chart, gross margins have remained stable in the 75-79% range, while operating margins have improved from negative territory toward break-even, and free cash flow margins have shown substantial improvement:

Strategic Initiatives

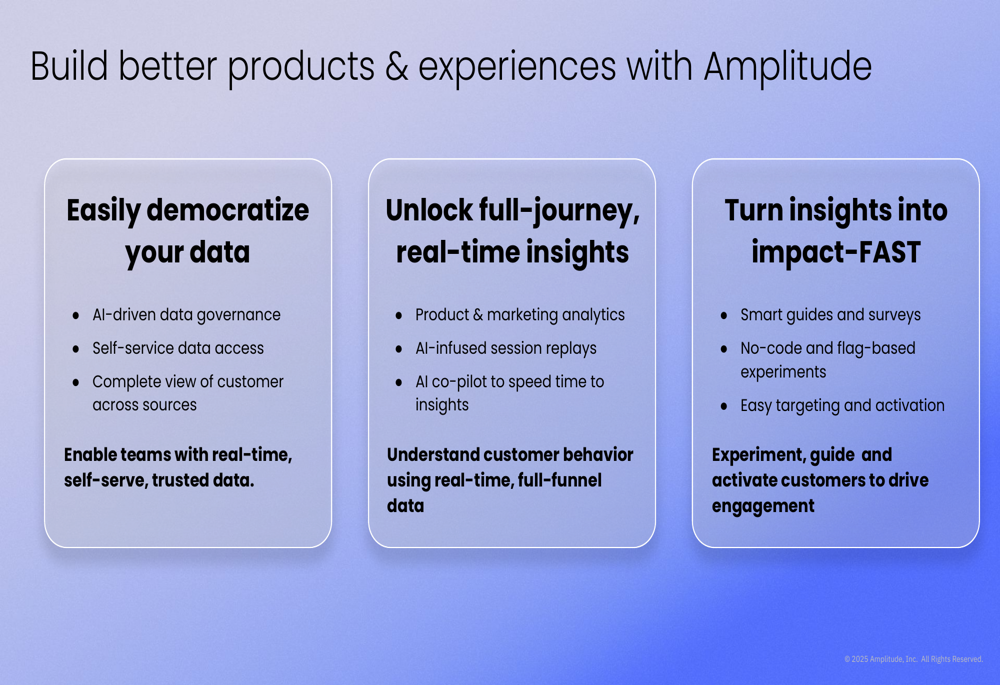

Amplitude’s presentation emphasized its platform strategy, focusing on three key value propositions: democratizing data access, unlocking real-time insights, and turning insights into business impact. The company reported that 34% of its customers now use more than one Amplitude product, indicating traction in its cross-selling efforts.

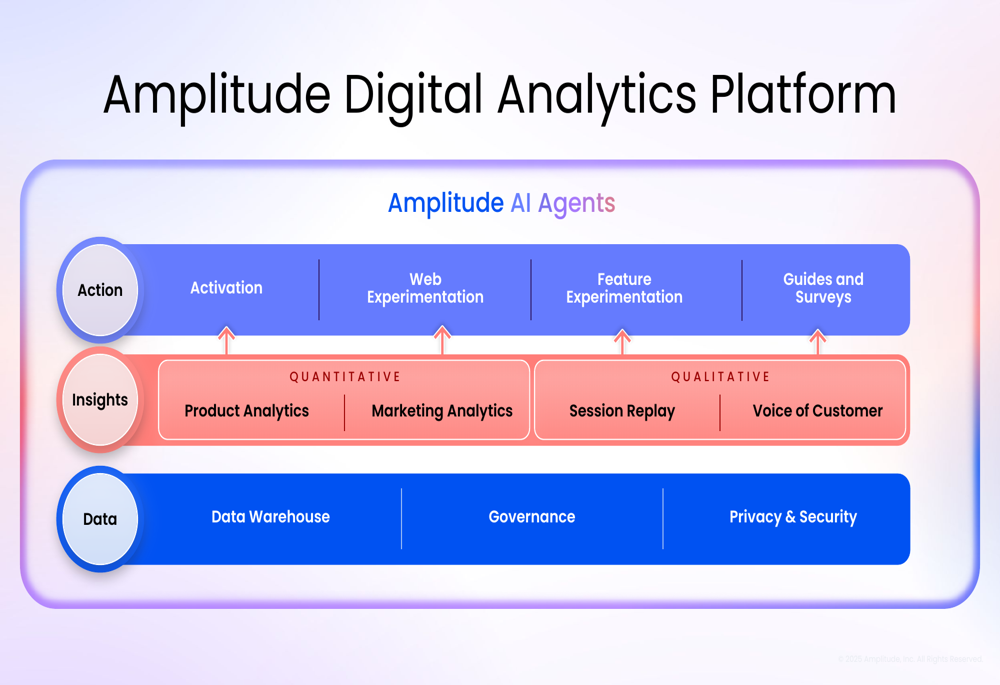

The company’s digital analytics platform architecture integrates data, insights, and action capabilities:

Amplitude highlighted the growing complexity of digital applications as a key market driver, noting there are now 8.9 million+ apps worldwide and 1.1 billion+ websites. The company positions its platform as a solution for understanding complex user journeys that typically involve around 2,500 distinct events per product.

The company’s value proposition centers on helping businesses understand and optimize these complex customer journeys:

Forward-Looking Statements

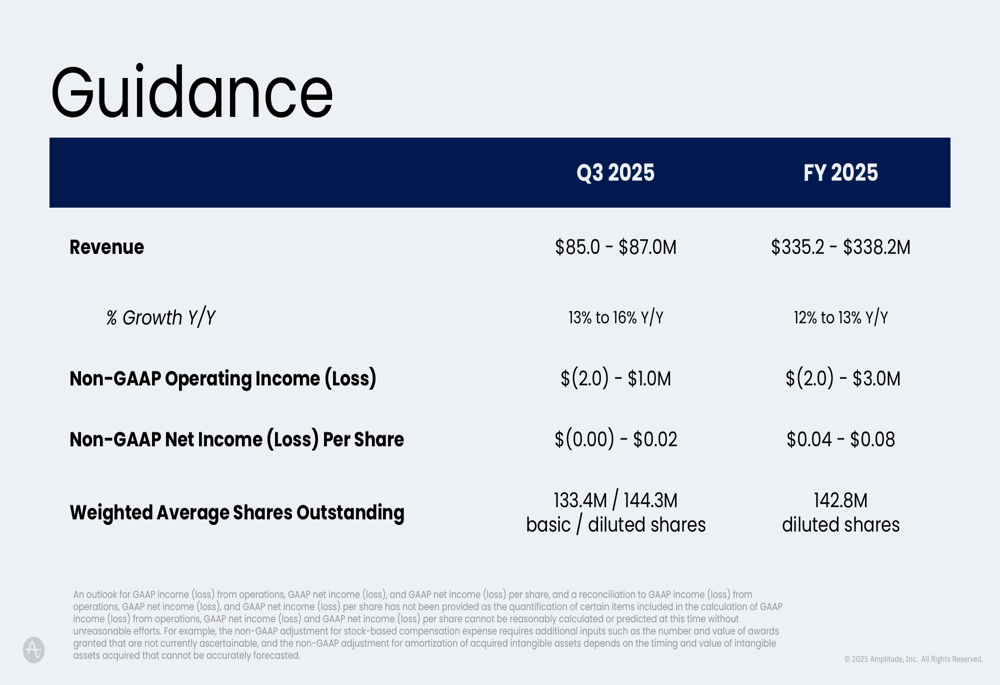

Amplitude provided guidance for both Q3 and full-year 2025, projecting continued growth:

For Q3 2025, Amplitude expects revenue between $85.0 million and $87.0 million, representing 13-16% year-over-year growth. The company anticipates a non-GAAP operating income/loss between $(2.0) million and $1.0 million.

For the full fiscal year 2025, Amplitude projects revenue between $335.2 million and $338.2 million, reflecting 12-13% year-over-year growth. This guidance represents a slight increase from the $329-333 million range provided during the Q1 earnings call. The company expects non-GAAP operating income/loss between $(2.0) million and $3.0 million and non-GAAP earnings per share between $0.04 and $0.08.

Amplitude’s stock closed at $12.22 on August 6, near the middle of its 52-week range of $7.55 to $14.88. The company’s improving metrics and accelerating growth could provide support for the stock, which has recovered significantly from its lows earlier in the year.

The company’s financial priorities remain focused on accelerating net new ARR, platform consolidation, and achieving growth with leverage, as it continues to expand its customer base and increase multi-product adoption across its platform.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.