ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Andritz AG (VIE:ANDR) reported its financial results for the first three quarters of 2025, showcasing a significant 20% year-over-year increase in order intake despite an 8% decline in revenue. The Austrian industrial engineering group’s shares rose 4.27% following the announcement, as investors responded positively to the company’s maintained profitability and strong order backlog.

The company’s presentation, delivered on October 30, 2025, highlighted Andritz’s resilience in challenging market conditions, with a comparable EBITA margin holding steady at 8.5% despite the revenue contraction. The results reflect Andritz’s strategic focus on service business growth and selective acquisitions to strengthen its market position.

Quarterly Performance Highlights

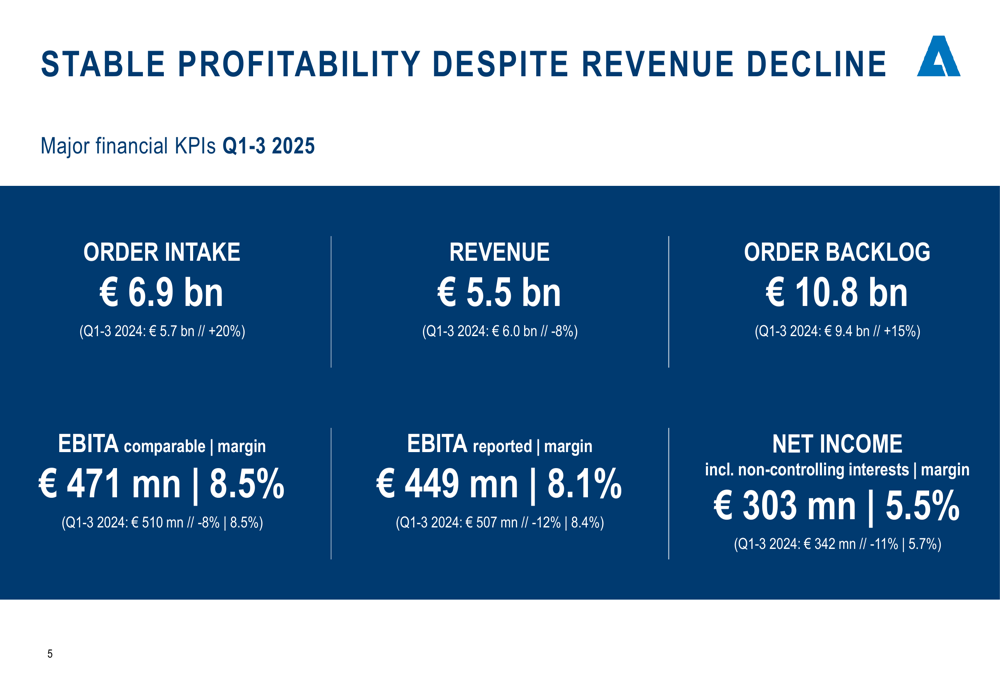

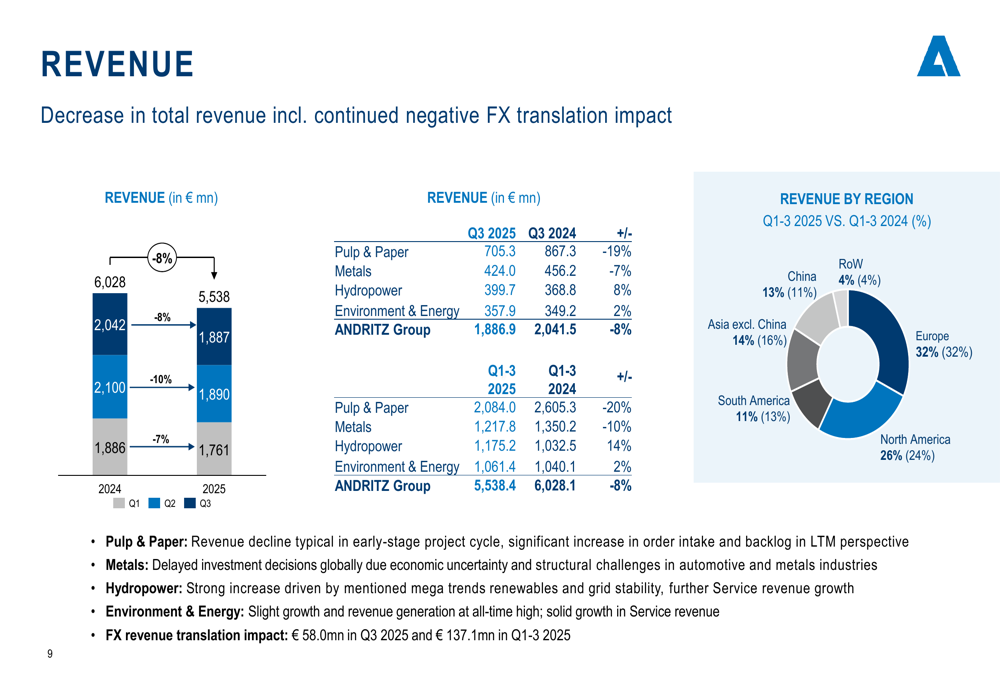

Andritz reported robust financial performance for the first nine months of 2025, with order intake reaching €6.9 billion, up 20% from €5.7 billion in the same period of 2024. This growth occurred despite an 8% decline in revenue to €5.5 billion, down from €6.0 billion in Q1-3 2024.

As shown in the following comprehensive overview of key financial metrics:

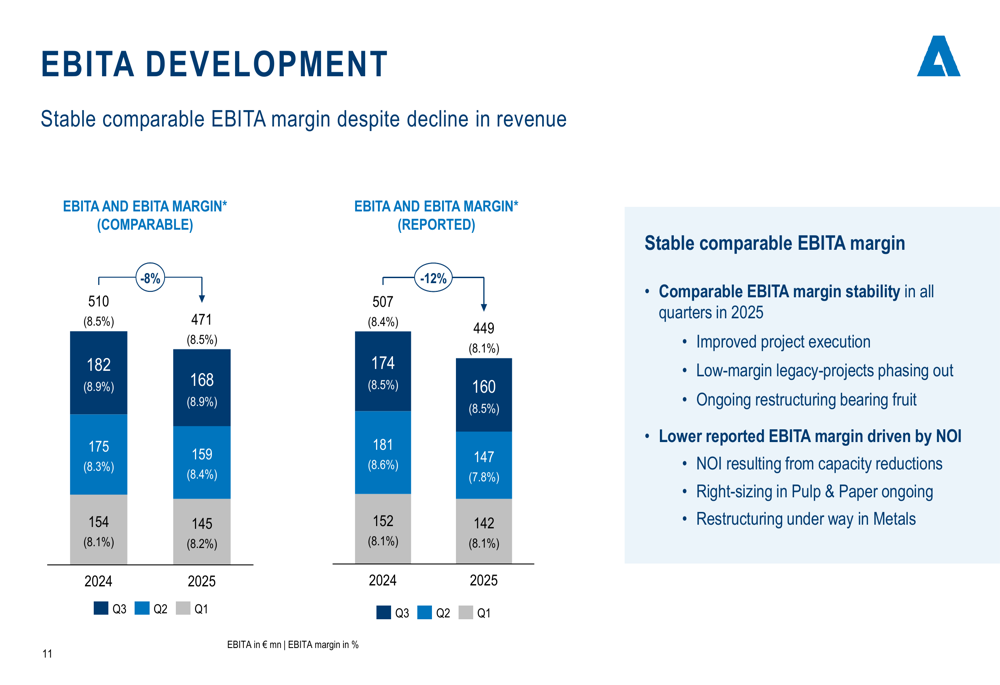

The order backlog increased by 15% year-over-year to €10.8 billion, providing strong visibility for future revenue. While the comparable EBITA remained stable at 8.5%, the reported EBITA margin decreased slightly to 8.1% from 8.4% in the previous year. Net income declined by 11% to €303 million.

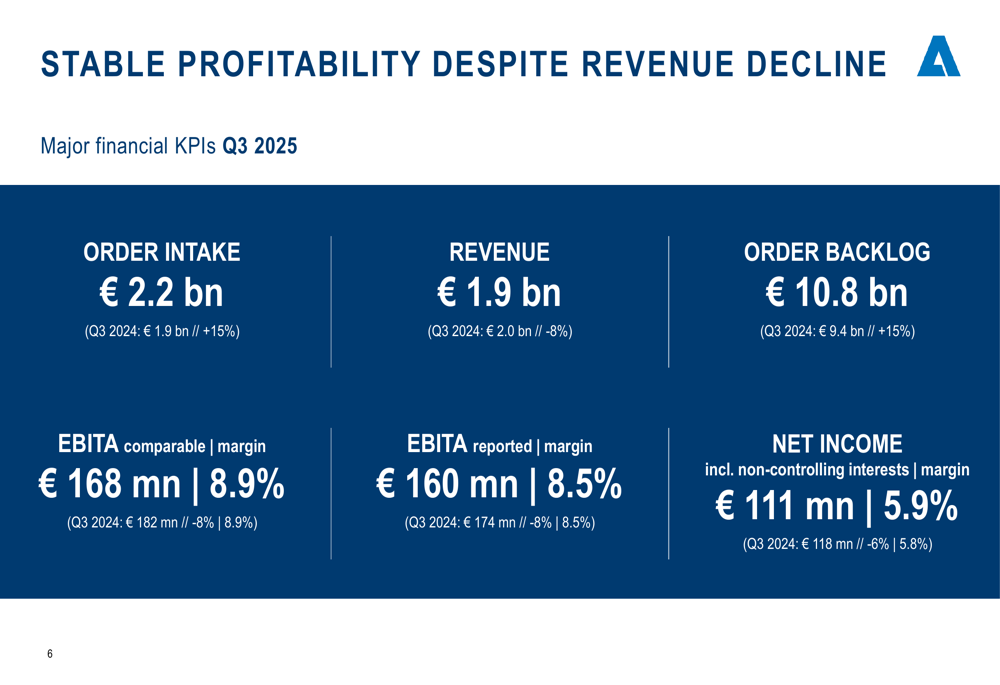

The third quarter of 2025 showed similar trends, with order intake growing by 15% to €2.2 billion while revenue decreased by 8% to €1.9 billion compared to Q3 2024:

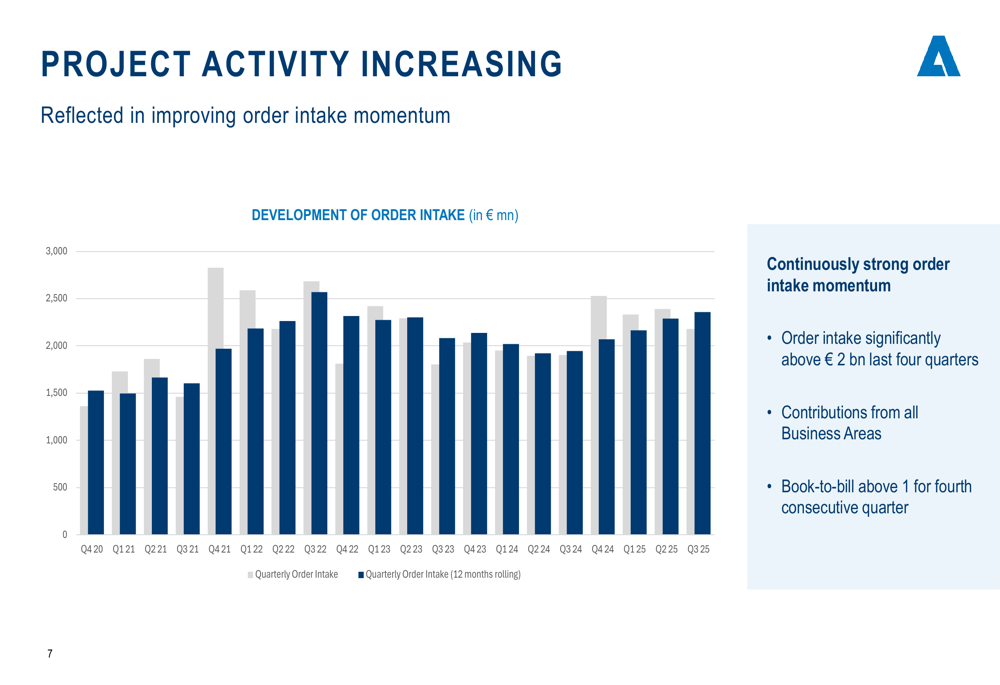

The company’s order intake has maintained strong momentum, with quarterly figures consistently above €2 billion in the last four quarters. This performance is particularly notable given the challenging macroeconomic environment:

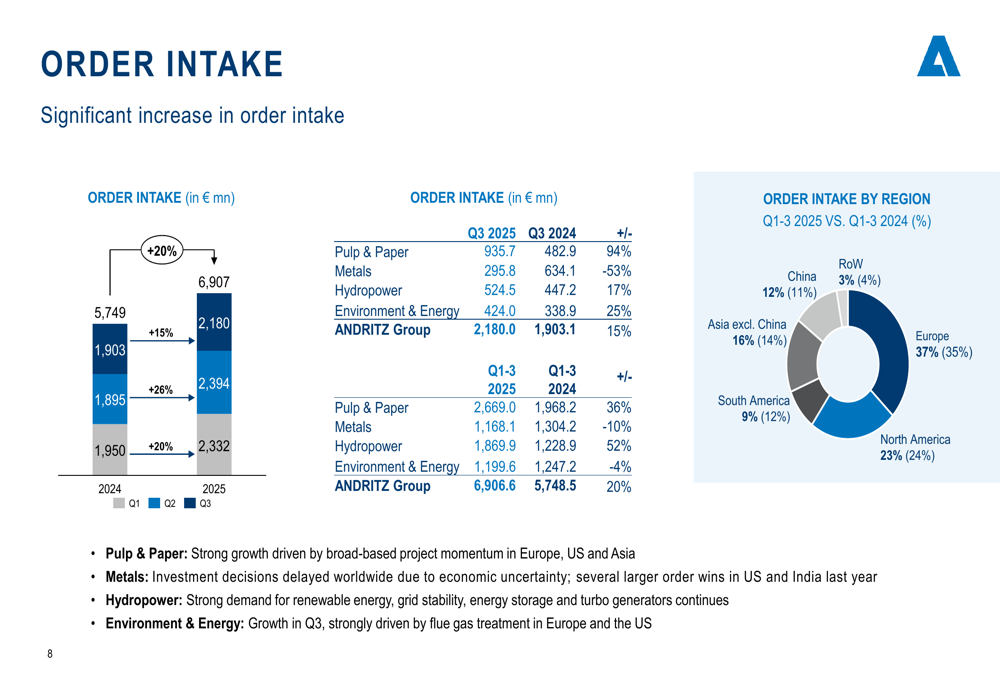

Breaking down the order intake by business area, Pulp & Paper showed the strongest growth at 27% for Q1-3 2025, followed by Environment & Energy at 18% and Hydropower at 17%. The Metals segment experienced a 3% decline due to delayed investment decisions:

Revenue performance varied significantly across business areas. While Hydropower saw a substantial 20% increase and Environment & Energy grew by 5%, both Pulp & Paper and Metals experienced declines of 16% and 14% respectively:

Detailed Financial Analysis

Despite the revenue decline, Andritz maintained a stable comparable EBITA margin of 8.5%, demonstrating effective cost management and operational efficiency. The EBITA development shows consistent margin performance throughout 2025:

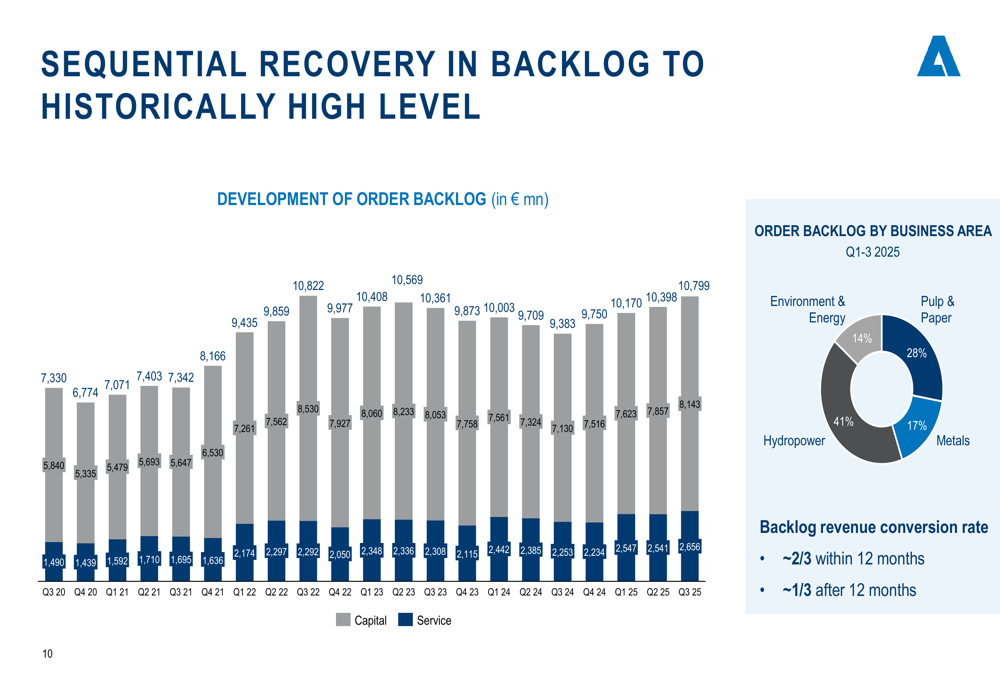

The company’s order backlog continued to grow, reaching €10.8 billion by the end of Q3 2025, providing a solid foundation for future revenue. Approximately two-thirds of this backlog is expected to convert to revenue within 12 months:

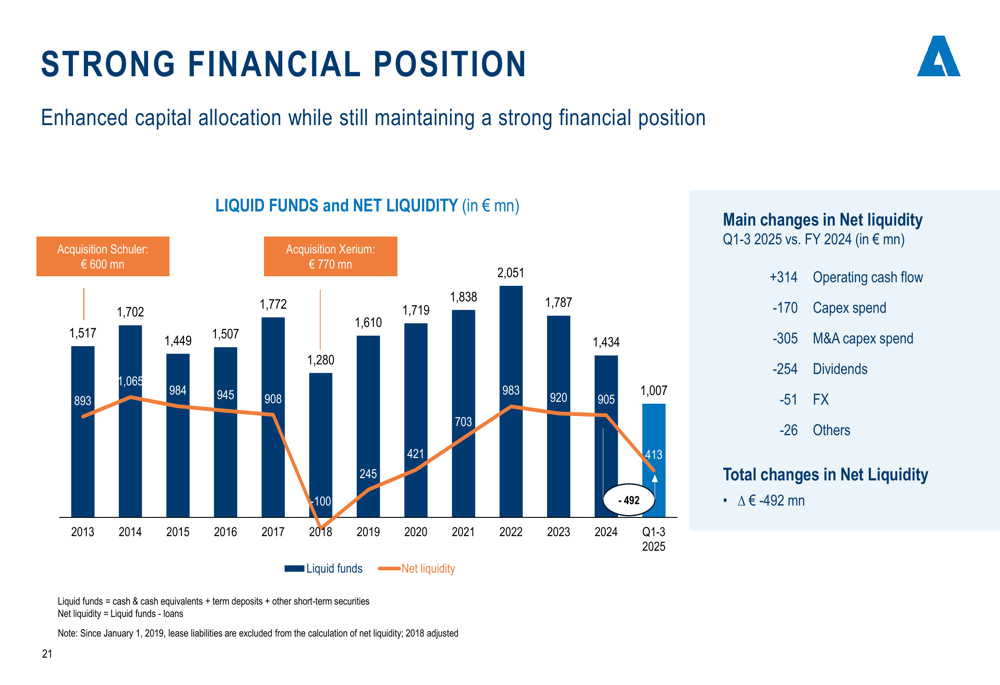

Andritz has maintained a strong financial position despite increased M&A spending. The company reported liquid funds of €1,006 million for Q1-3 2025, supporting its strategic acquisitions while maintaining financial stability:

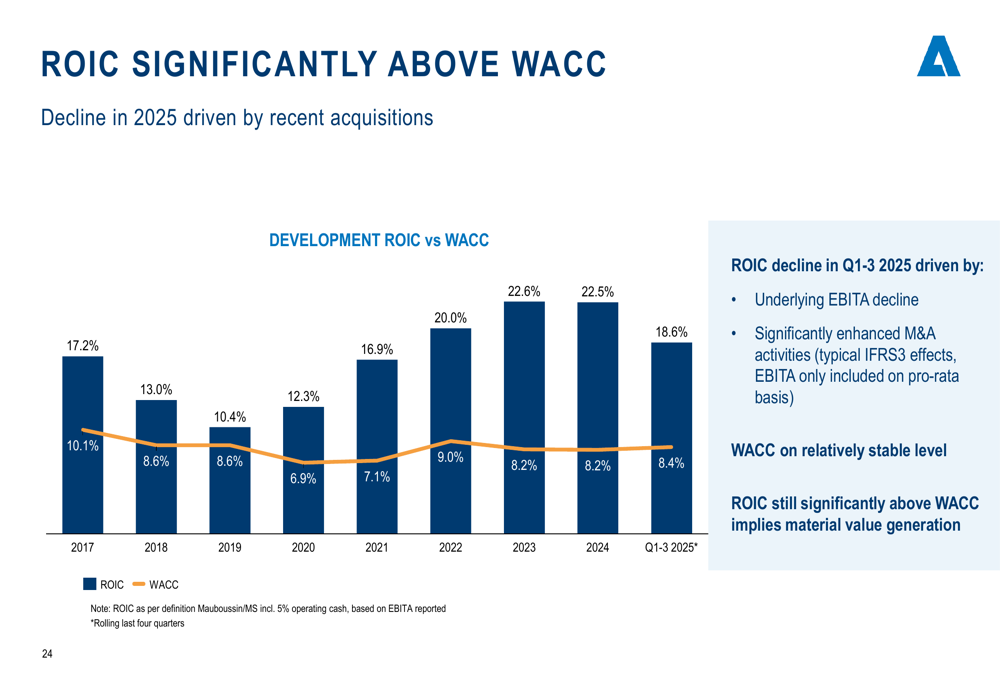

The return on invested capital (ROIC) remains significantly above the weighted average cost of capital (WACC), indicating efficient capital allocation and value creation, although there was a decline in 2025 due to recent acquisitions:

Strategic Initiatives

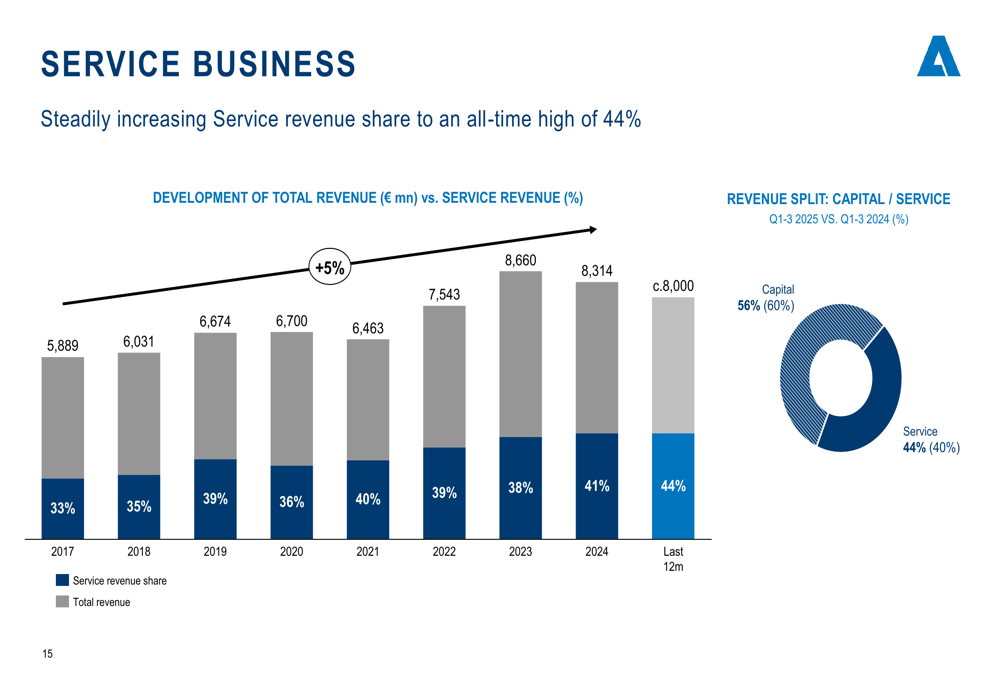

A key strategic focus for Andritz has been growing its service business, which reached an all-time high of 44% of total revenue in Q1-3 2025, up from 40% in the same period of 2024. This shift helps stabilize revenue and improve margins:

The company completed several strategic acquisitions in 2025 to strengthen its market position across multiple business areas:

- LDX (USA) in Q1 2025, a provider of emission reduction technologies

- A. Celli Paper (Italy) in Q2 2025, a supplier of machinery for tissue, paper, and board grades

- Diamond Power (USA) in Q2 2025, a designer and manufacturer of advanced boiler cleaning systems

- Salico Group (Italy) in Q2 2025, specializing in equipment for strip and plate finishing

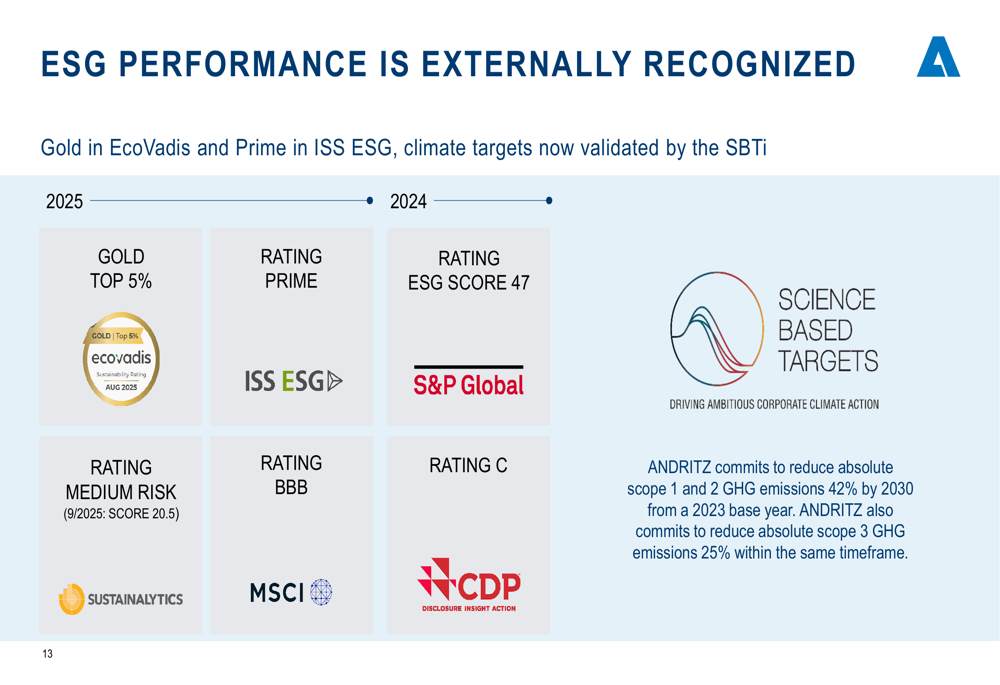

Andritz has also made significant progress in sustainability, receiving Gold status from EcoVadis and Prime status from ISS ESG. The company has committed to reducing absolute scope 1 and 2 GHG emissions by 42% and scope 3 emissions by 25% by 2030:

Forward-Looking Statements

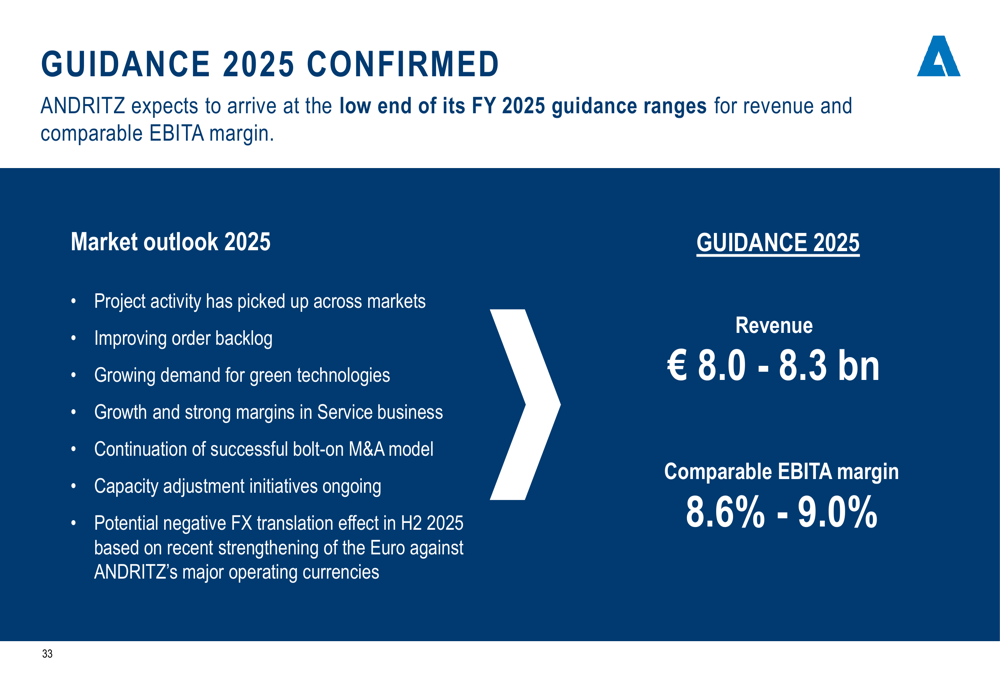

Andritz confirmed its guidance for 2025, expecting to achieve the lower end of its revenue target range of €8.0-8.3 billion and comparable EBITA margin of 8.6-9.0%. The company noted potential negative impacts from FX translation effects but expects no direct adverse impact from increasing trade barriers:

Looking further ahead, Andritz reaffirmed its mid-term targets for 2027, aiming for revenue of €9-10 billion and a comparable EBITA margin above 9%. These targets are based on assumptions of growth in capital sales, increasing demand for green technologies, and mix improvements:

The company provided a detailed breakdown of its 2027 comparable EBITA margin targets by business area, with Pulp & Paper and Environment & Energy expected to achieve the highest margins:

Competitive Industry Position

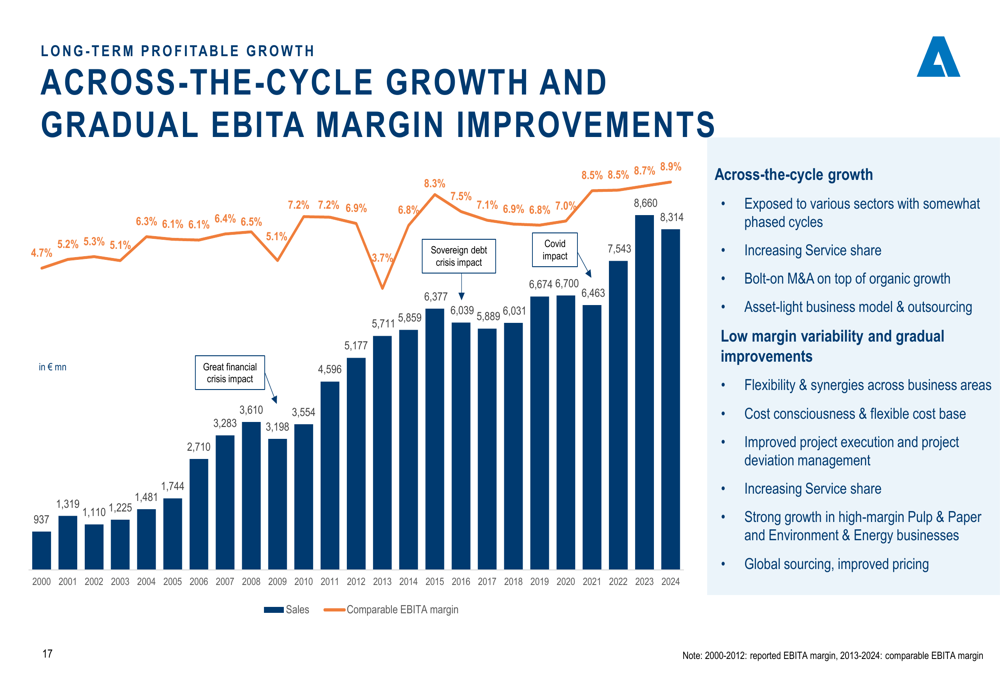

Andritz has demonstrated long-term profitable growth over the past two decades, with gradual EBITA margin improvements and across-the-cycle growth due to its diversified exposure across various sectors:

During the earnings call, CEO Dr. Joachim Schönbeck expressed satisfaction with the turnaround in order intake, stating, "We are happy that we could turn around the order intake now in Q3 by a solid growth of 25%." CFO Vanessa Hellwing added, "Our main leading indicator is still pointing upwards," highlighting the company’s positive outlook.

The company faces some challenges, particularly in the automotive and steel industries, which could impact future growth in the Metals segment. Market saturation in mature segments might also limit growth opportunities. However, Andritz sees strong potential in hydropower and identified green hydrogen and carbon capture as emerging opportunities.

Andritz’s strategic focus on service business growth, targeted acquisitions, and sustainability initiatives positions it well to navigate current market challenges while building a foundation for future growth. With a strong order backlog and stable margins despite revenue headwinds, the company appears well-positioned to achieve its mid-term targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.