Barclays now sees two Fed cuts this year, says jumbo Fed cuts ’very unlikely’

Antero Midstream Corp (NYSE:AM) shares rose 3.47% to $16.55 on May 1, 2025, as the company released its first quarter earnings presentation highlighting continued operational efficiency and strategic positioning to capitalize on growing natural gas demand in the Appalachian region.

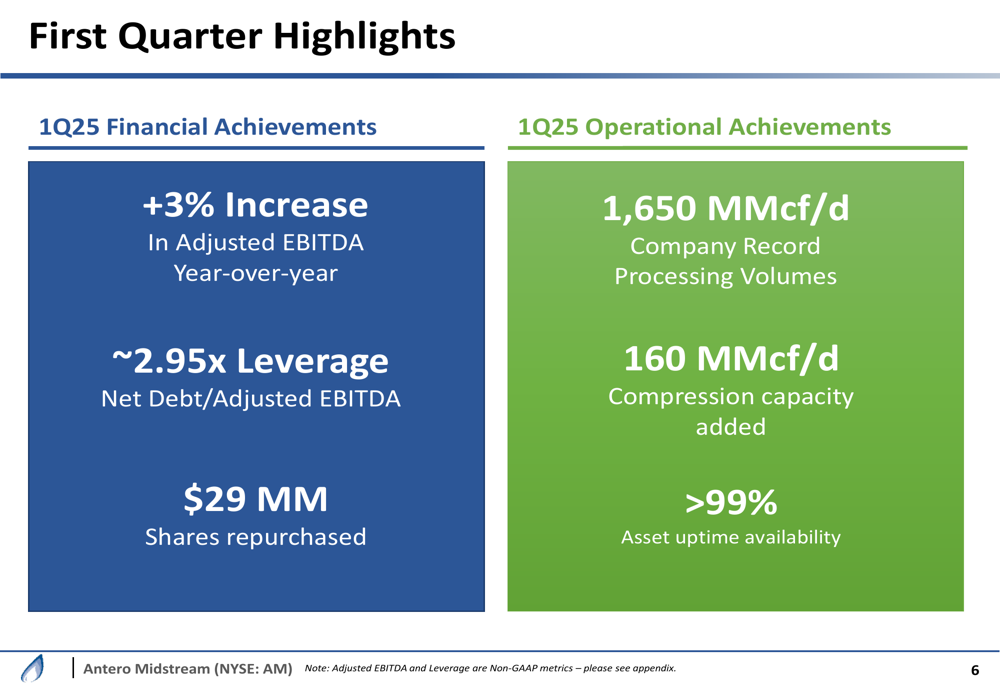

Quarterly Performance Highlights

Antero Midstream reported a 3% year-over-year increase in adjusted EBITDA for Q1 2025, continuing its pattern of consistent growth. The company maintained strong operational performance with over 99% asset uptime availability and achieved record processing volumes of 1,650 MMcf/d during the quarter.

The midstream operator also reported significant progress in its financial management, maintaining a leverage ratio of approximately 2.95x Net Debt/Adjusted EBITDA while repurchasing $29 million in shares during the quarter.

As shown in the following quarterly highlights slide, the company balanced operational achievements with financial discipline:

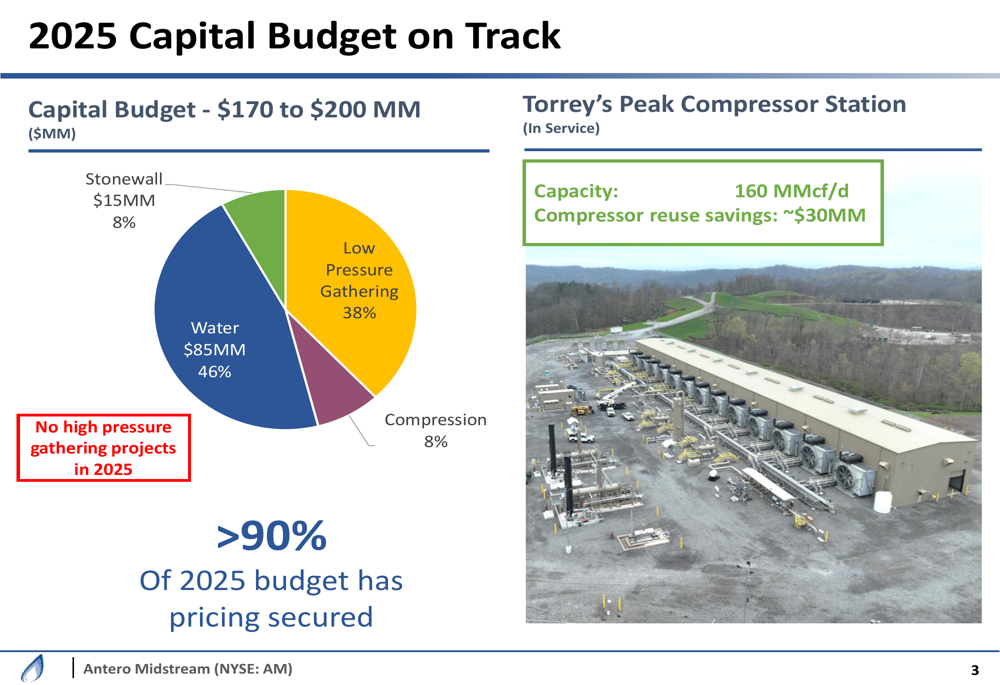

Capital Allocation and Efficiency

Antero Midstream’s 2025 capital budget remains on track at $170-200 million, with over 90% of pricing already secured. The budget allocation demonstrates the company’s strategic focus, with 46% directed toward water infrastructure, 38% to low pressure gathering, and 8% each to Stonewall and compression projects. Notably, the company has no high pressure gathering projects planned for 2025.

The presentation highlighted the Torrey’s Peak Compressor Station, which provides 160 MMcf/d of capacity with approximately $30 million in compressor reuse savings, demonstrating the company’s focus on capital efficiency.

The following capital budget breakdown illustrates Antero’s disciplined approach to infrastructure investment:

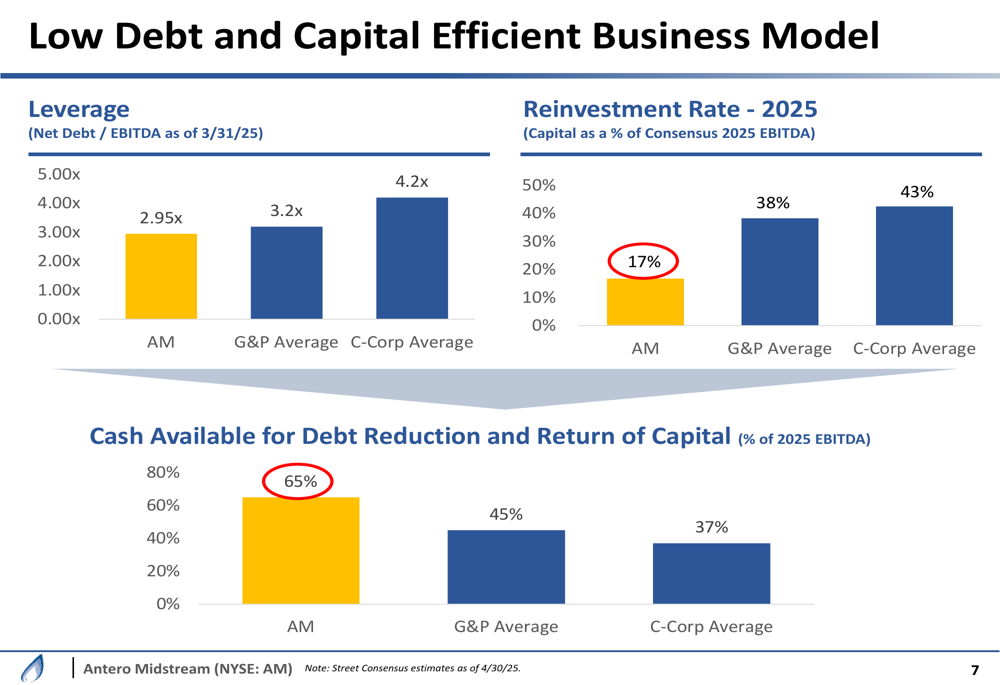

Competitive Industry Position

Antero Midstream emphasized its advantageous position compared to industry peers. With a leverage ratio of 2.95x, the company maintains lower debt levels than both G&P averages (3.2x) and C-Corp averages (4.2x). Similarly, its reinvestment rate of 17% (capital as a percentage of 2025 EBITDA) significantly undercuts industry averages of 38-43%.

This capital efficiency translates to greater financial flexibility, with 65% of 2025 EBITDA available for debt reduction and return of capital, compared to just 45% for G&P averages and 37% for C-Corp averages.

The following comparative analysis clearly demonstrates Antero’s financial advantages relative to competitors:

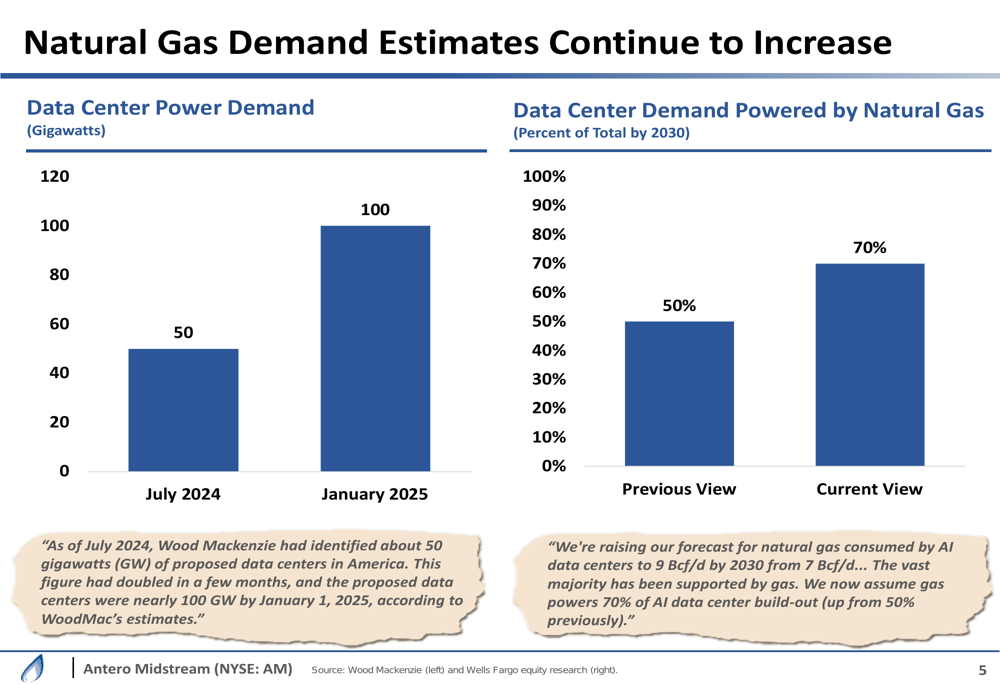

Growth Drivers and Market Opportunities

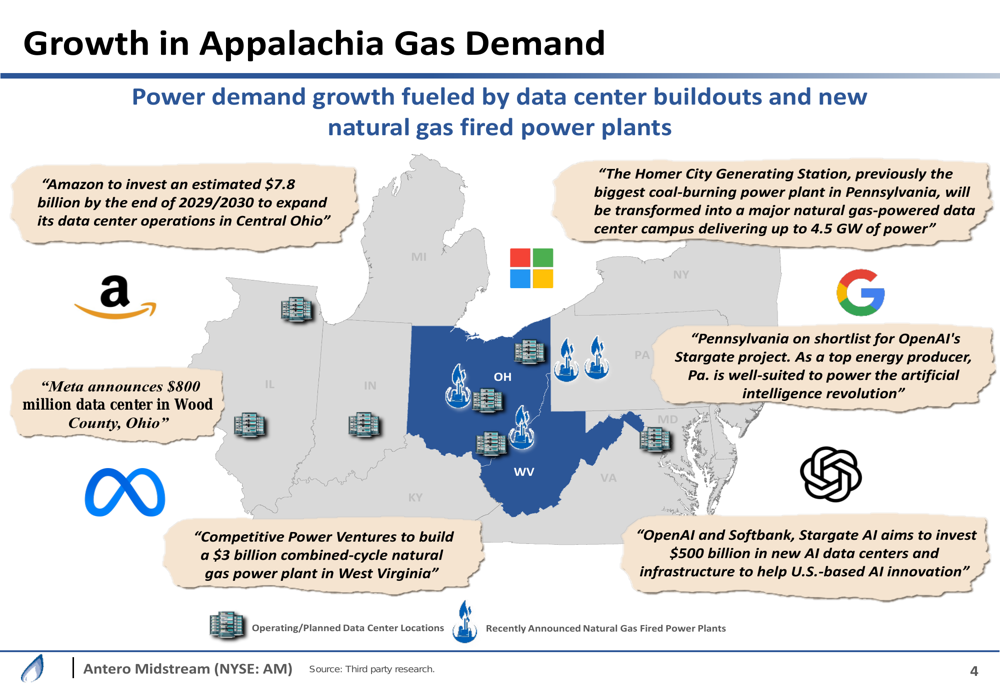

A significant portion of the presentation focused on emerging growth opportunities in the Appalachian region, particularly driven by data center buildouts and new natural gas-fired power plants. The company highlighted several major investments, including Amazon (NASDAQ:AMZN)’s estimated $7.8 billion investment in Central Ohio, Meta (NASDAQ:META)’s $800 million data center in Wood County, Ohio, and Competitive Power Ventures’ $3 billion natural gas power plant in West Virginia.

These developments align with broader industry trends, as data center power demand has doubled from 50 gigawatts in July 2024 to 100 gigawatts in January 2025. Additionally, the percentage of data center demand powered by natural gas is projected to reach 70% by 2030, up from previous estimates of 50%.

The following chart illustrates the dramatic increase in natural gas demand for data centers:

The geographic concentration of these investments in Antero’s operational territory presents significant growth opportunities, as shown in this regional development map:

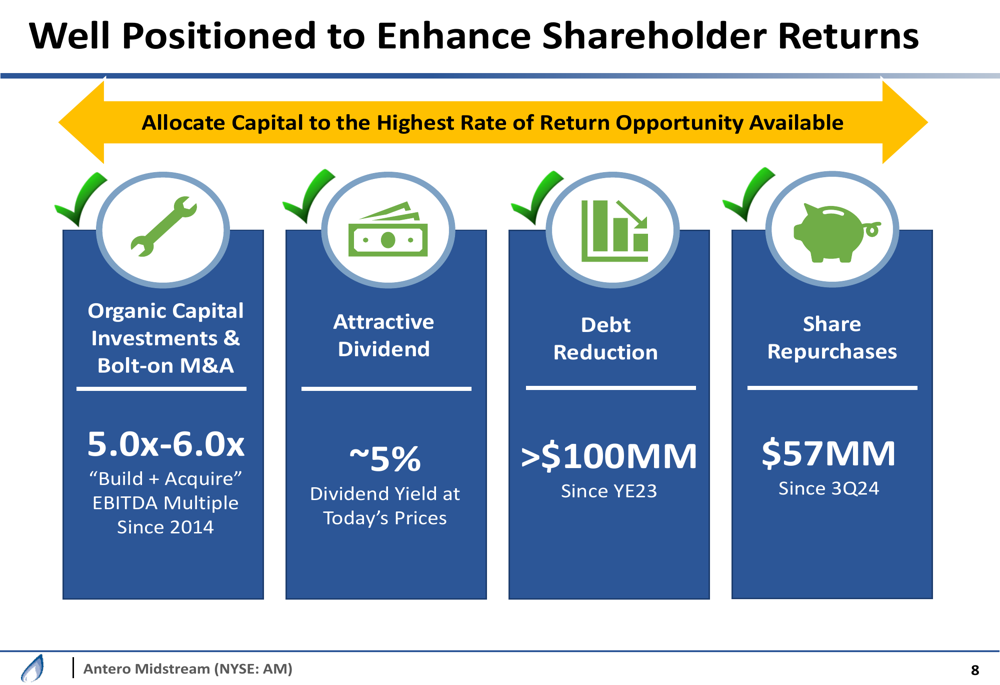

Shareholder Return Strategy

Antero Midstream outlined a multi-faceted approach to enhancing shareholder returns. The strategy balances organic capital investments and bolt-on acquisitions (with a 5.0x-6.0x "Build + Acquire" EBITDA multiple since 2014) with an attractive dividend yield of approximately 5% at current prices.

The company has reduced debt by more than $100 million since year-end 2023 and executed $57 million in share repurchases since Q3 2024. This balanced capital allocation approach aims to maximize returns across various opportunities.

The following slide outlines Antero’s comprehensive shareholder return strategy:

Forward-Looking Statements

Looking ahead, Antero Midstream appears well-positioned to benefit from the growing natural gas demand in the Appalachian region, particularly as data centers and power plants increase their consumption. The company’s low leverage, efficient capital allocation, and strategic positioning in a high-demand region provide a solid foundation for continued growth.

The Q1 2025 results continue the positive momentum seen in the previous quarter, where the company reported its tenth consecutive year of EBITDA growth and achieved record free cash flow after dividends of $250 million for 2024. With its disciplined approach to capital allocation and strategic focus on high-return opportunities, Antero Midstream demonstrates a clear path for sustainable growth and shareholder returns in the midstream sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.