SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Apellis Pharmaceuticals (NASDAQ:APLS) presented its second quarter 2025 financial results on July 31, 2025, highlighting recent regulatory approvals and strategic initiatives amid challenging year-over-year revenue comparisons. The company’s stock rose 5.53% in premarket trading to $20.05, suggesting positive investor reception despite mixed financial results.

The presentation comes after a challenging period for Apellis, whose stock has experienced significant pressure over the past year. The biotech firm continues to position itself as the leader in complement C3-targeting therapies, with its flagship products SYFOVRE for geographic atrophy and EMPAVELI for rare diseases.

Quarterly Performance Highlights

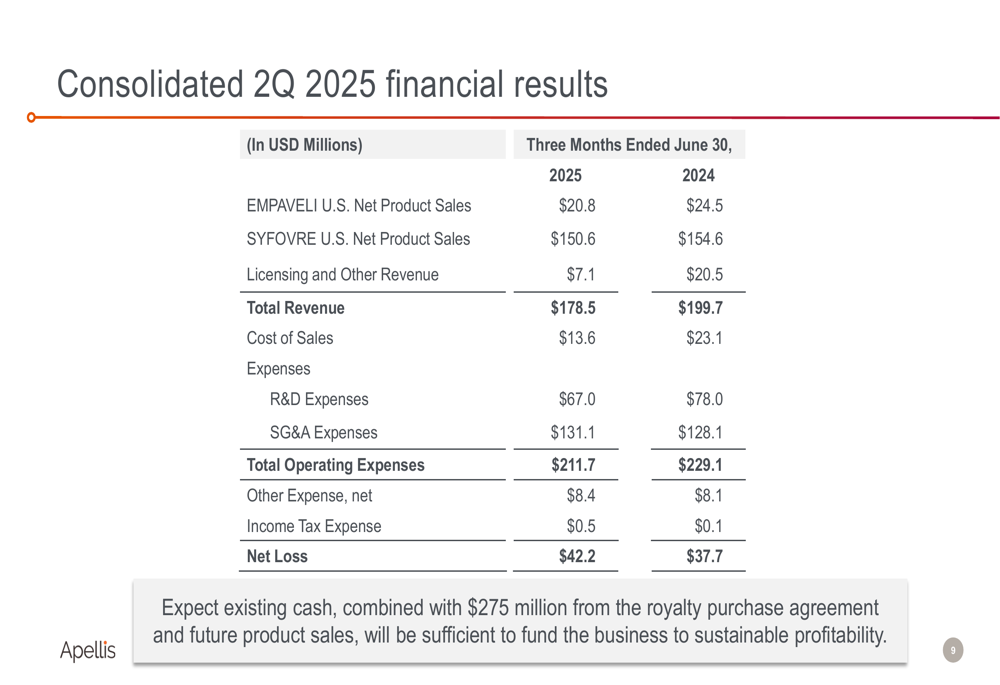

Apellis reported total revenue of $178.5 million for Q2 2025, representing a decline from $199.7 million in the same period last year. The company posted a net loss of $42.2 million, compared to a $37.7 million loss in Q2 2024.

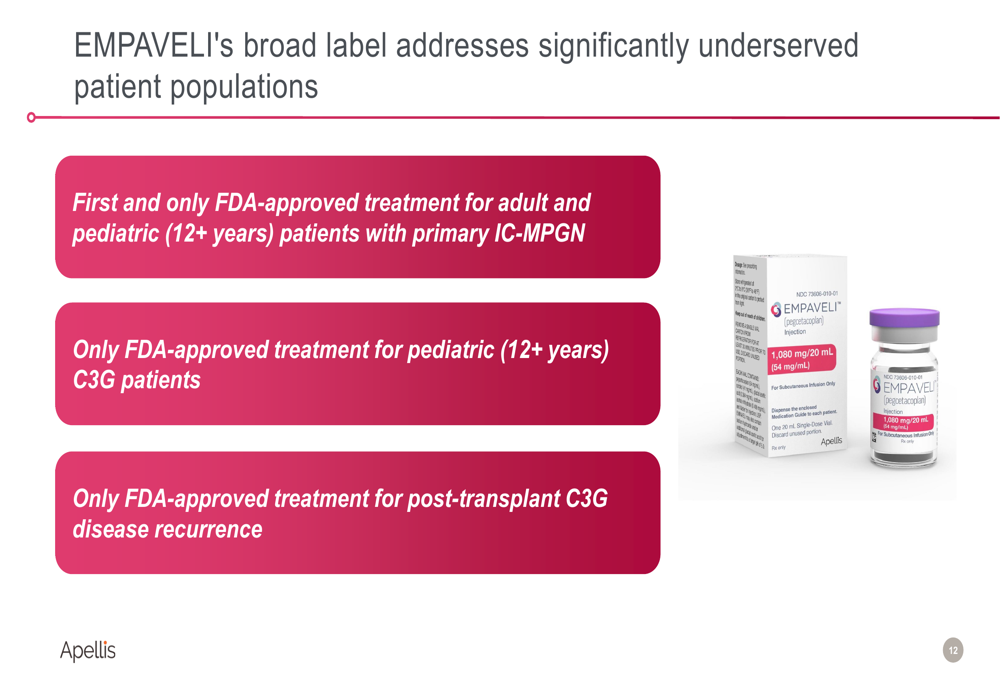

The quarter’s most significant development was the FDA approval of EMPAVELI for the treatment of C3G and primary IC-MPGN, providing the first approved therapy for these rare kidney diseases. This regulatory milestone expands EMPAVELI’s potential market significantly.

As shown in the comprehensive financial results:

The financial results reveal mixed performance across key metrics. While total revenue declined year-over-year, operating expenses also decreased from $229.1 million to $211.7 million, primarily driven by lower R&D expenses ($67.0 million vs. $78.0 million) and reduced cost of sales ($13.6 million vs. $23.1 million). However, SG&A expenses increased slightly to $131.1 million.

SYFOVRE Performance and Market Position

SYFOVRE generated approximately $151 million in Q2 2025 revenue, maintaining its dominant position in the geographic atrophy (GA) market with over 60% market share. The company reported 6% quarter-over-quarter injection growth and noted that SYFOVRE accounted for 55% of new patient starts in Q2 2025.

The presentation highlighted SYFOVRE’s market leadership, attributing it to the product’s differentiated clinical profile:

Apellis emphasized SYFOVRE’s ability to demonstrate robust and increasing effects over time, its flexible dosing schedule (approved for as few as 6 doses per year), and favorable payer positioning. The company also highlighted data presented at the American Society of Retina Specialists (ASRS) demonstrating SYFOVRE’s ability to preserve retinal tissue through 48 months of treatment.

The company is implementing several initiatives to drive SYFOVRE demand, including direct-to-consumer campaigns, emphasizing early intervention, and educating healthcare providers on reimbursement practices.

EMPAVELI Expansion and New Approvals

The most significant development in Q2 was EMPAVELI’s FDA approval for C3G and primary IC-MPGN, addressing previously underserved patient populations:

EMPAVELI generated approximately $21 million in Q2 2025 revenue from its original indication in paroxysmal nocturnal hemoglobinuria (PNH). The company reported a ~97% patient compliance rate and continued strong safety profile with zero meningococcal infections.

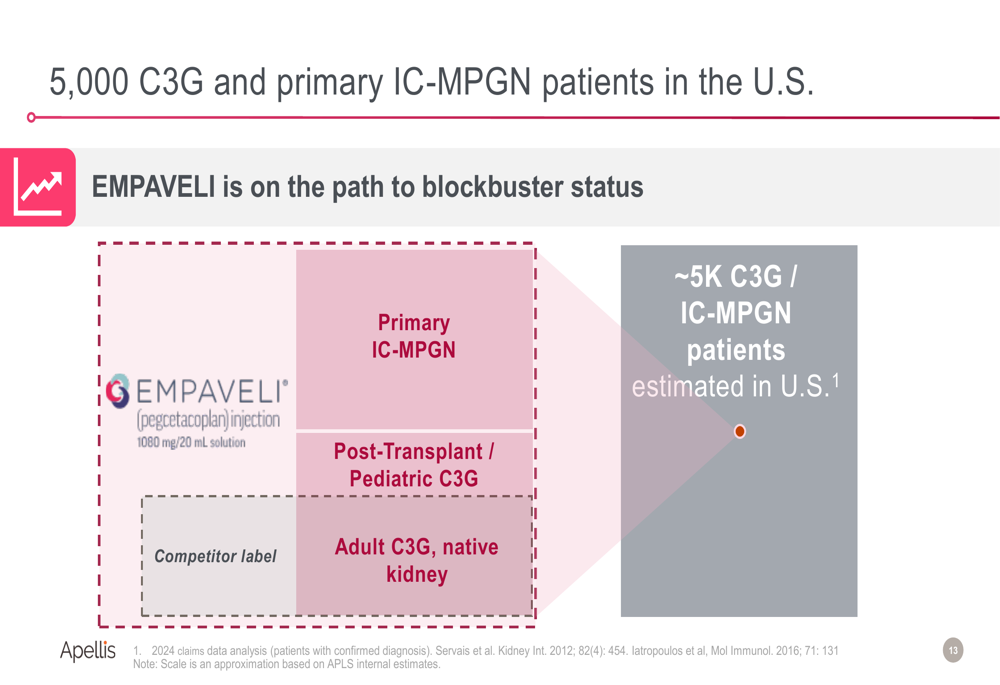

Apellis is positioning EMPAVELI for potential blockbuster status, citing an estimated ~5,000 C3G/IC-MPGN patients in the U.S. based on 2024 claims data analysis:

The company is also expanding EMPAVELI into additional kidney indications, with plans to initiate pivotal trials in Delayed Graft Function (DGF) and Primary Focal Segmental Glomerulosclerosis (FSGS) by year-end. These conditions represent significant unmet medical needs, with DGF occurring in 30-35% of deceased donor kidneys and approximately 13,000 U.S. patients having primary FSGS.

Financial Analysis and Capital Strategy

A key financial development was Apellis’ agreement to receive up to $300 million in non-dilutive capital from a capped royalty purchase agreement for ex-U.S. royalties of Aspaveli (EMPAVELI’s brand name outside the U.S.). The company will receive $275 million upfront in exchange for 90% of future ex-U.S. royalties, with an additional $25 million in potential milestone payments contingent on European regulatory approvals.

This strategic financial move strengthens Apellis’ balance sheet as it pursues sustainable profitability. The company stated that its existing cash, combined with the $275 million from the royalty agreement and future product sales, will be sufficient to fund operations to profitability.

Pipeline and Strategic Initiatives

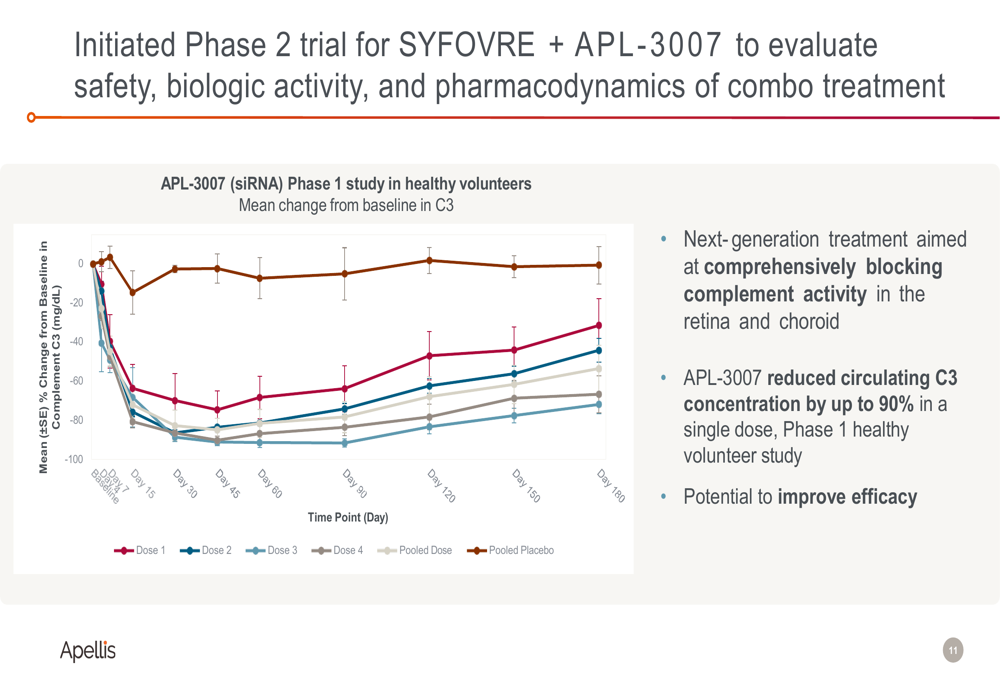

Apellis presented promising data from its pipeline, particularly for APL-3007, a small interfering RNA (siRNA) therapy being developed as a next-generation treatment for retinal diseases:

The Phase 1 study in healthy volunteers demonstrated that APL-3007 reduced circulating C3 concentration by up to 90% with a single dose. Apellis is initiating a Phase 2 study of SYFOVRE in combination with APL-3007, aiming to improve efficacy in geographic atrophy.

Forward-Looking Statements

Looking ahead, Apellis is focused on several key initiatives:

1. Maximizing EMPAVELI’s potential in C3G and primary IC-MPGN through disease awareness campaigns, establishing it as the treatment of choice, and securing broad insurance access

2. Expanding EMPAVELI into new kidney indications with pivotal trials in DGF and FSGS

3. Driving SYFOVRE demand through direct-to-consumer campaigns and healthcare provider education

4. Advancing combination therapy with SYFOVRE and APL-3007

The Q2 2025 results represent a transitional period for Apellis as it balances current revenue challenges with significant regulatory achievements and pipeline advancements. While the company continues to post net losses, the non-dilutive funding and potential new market opportunities provide a pathway toward sustainable profitability.

Investors will be watching closely to see if the recent EMPAVELI approval and planned expansion into additional indications can offset the slight revenue decline in SYFOVRE and help return the company to a growth trajectory in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.