United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Apellis Pharmaceuticals (NASDAQ:APLS) presented its second quarter 2025 financial results on July 31, highlighting recent regulatory approvals and market expansion despite a year-over-year revenue decline. The company’s stock has faced downward pressure, closing at $23.97 in aftermarket trading, down 4.1% following the earnings announcement. While maintaining market leadership in geographic atrophy treatments with over 60% market share, Apellis is navigating the balance between current performance and future growth opportunities.

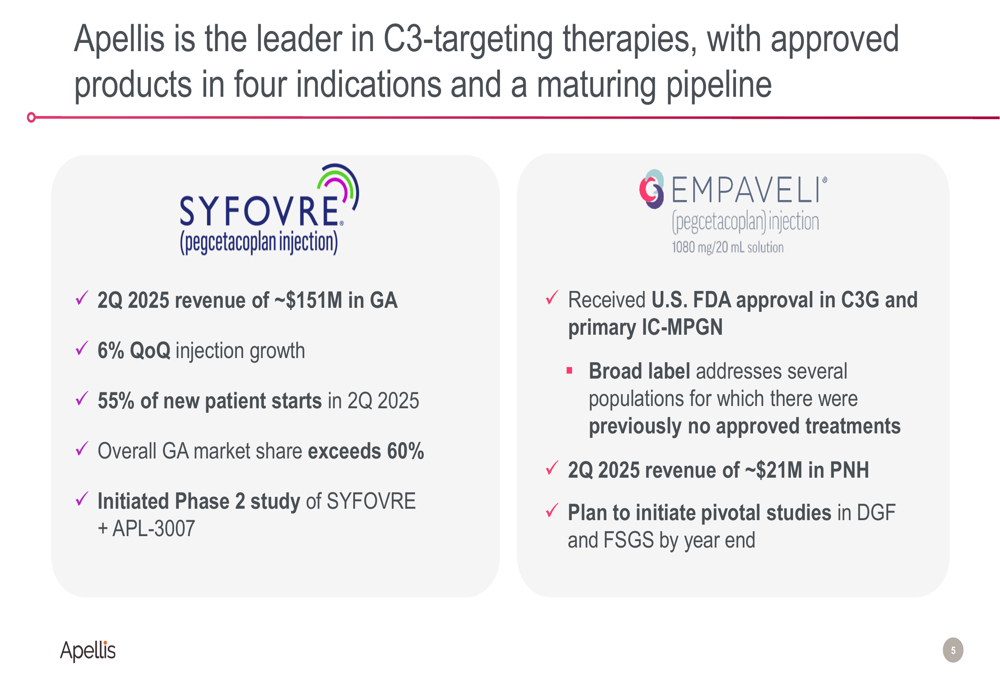

The company’s presentation emphasized its leadership in C3-targeting therapies, with approved products in four indications and a maturing pipeline. Most notably, Apellis received FDA approval for EMPAVELI in the treatment of C3G and primary IC-MPGN, marking the first time patients can be treated with a C3-targeting therapy for these conditions.

As shown in the following slide highlighting Apellis’ leadership in C3-targeting therapies:

Quarterly Performance Highlights

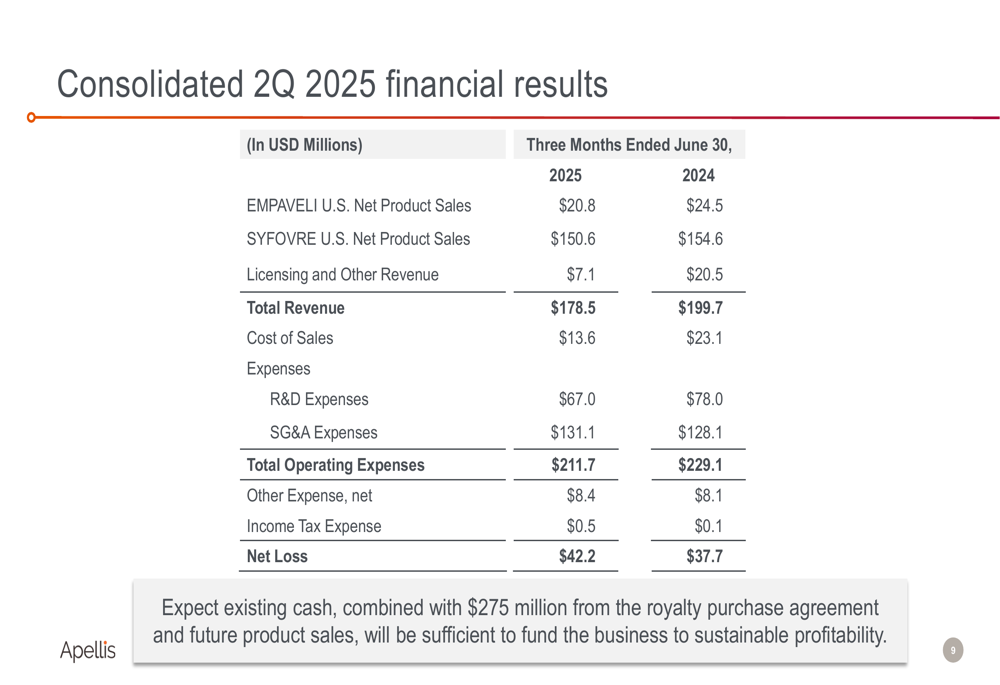

Apellis reported total revenue of $178.5 million for Q2 2025, down from $199.7 million in the same period last year. SYFOVRE generated approximately $151 million in revenue from geographic atrophy treatments, while EMPAVELI contributed about $21 million from PNH treatments. Despite the year-over-year revenue decline, the company highlighted a 6% quarter-over-quarter growth in SYFOVRE injections.

The company’s consolidated financial results reveal the current state of operations:

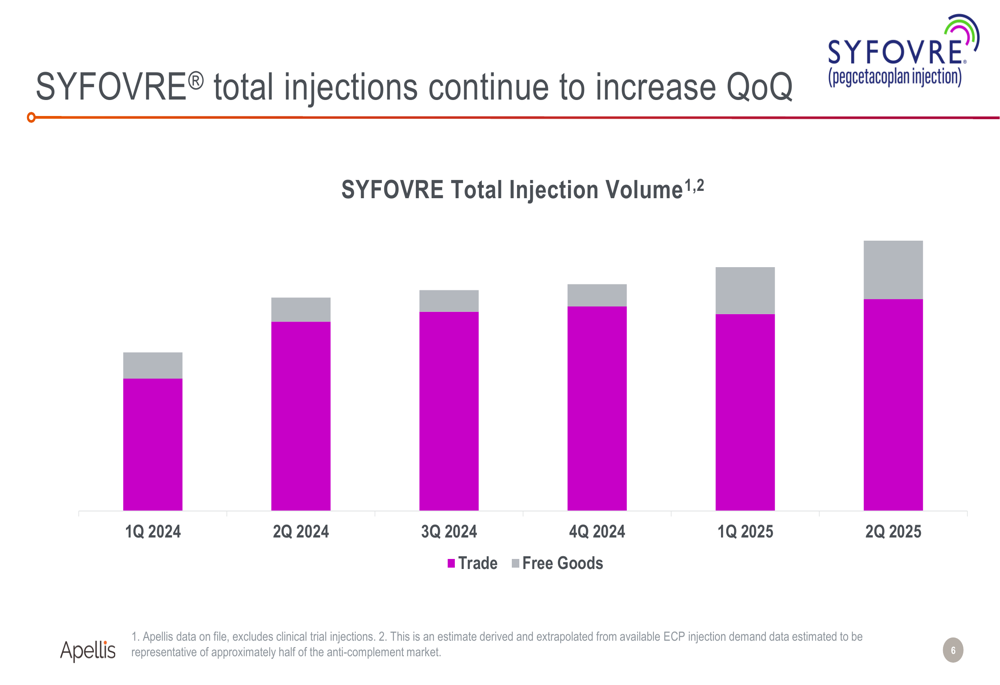

SYFOVRE continues to show steady growth in total injections quarter-over-quarter, as illustrated in the following chart:

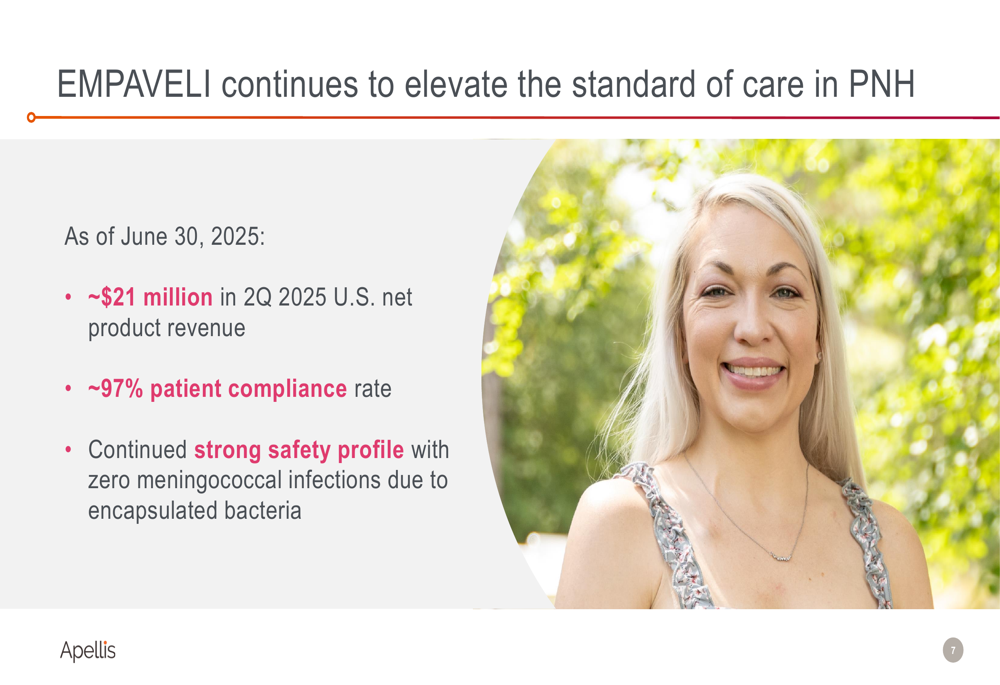

For EMPAVELI in the PNH indication, Apellis reported strong patient compliance and safety metrics:

Strategic Initiatives

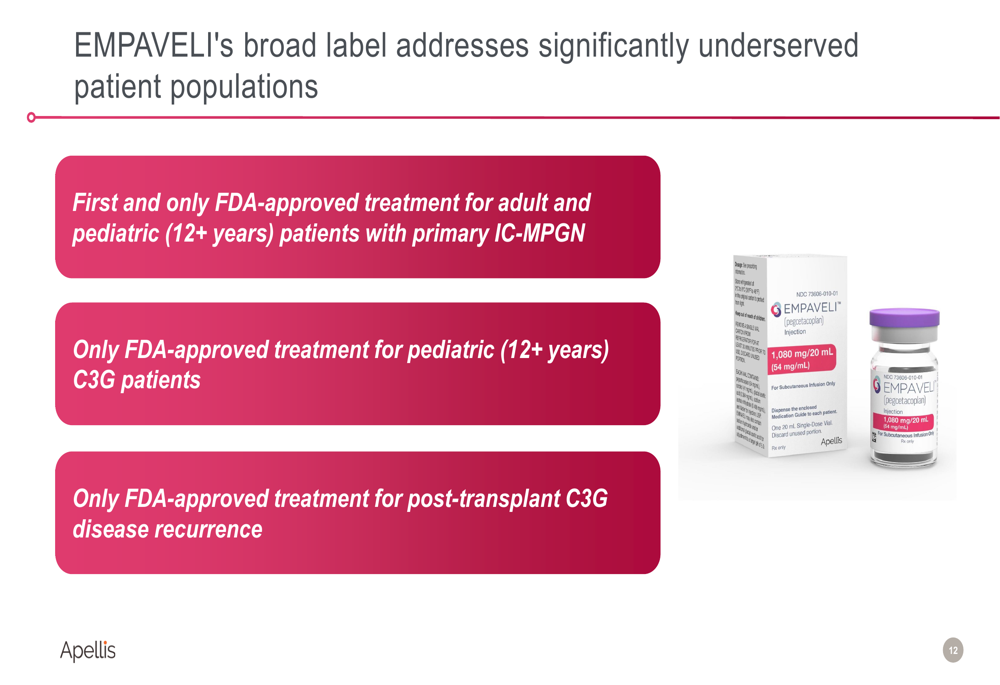

The most significant strategic development was the FDA approval of EMPAVELI for C3G and primary IC-MPGN, positioning Apellis as the first company to offer a C3-targeting therapy for these conditions. The approval provides a broad label that addresses previously untreated populations.

The approval details are shown in the following slide:

Apellis emphasized the unique positioning of EMPAVELI with its broad label addressing underserved populations:

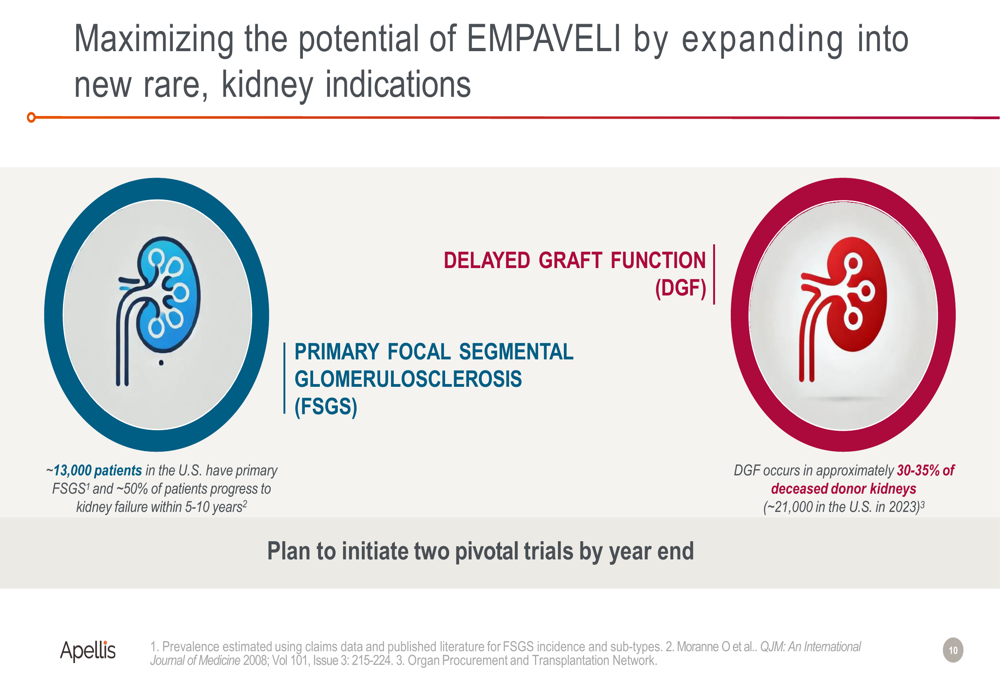

The company is also expanding EMPAVELI into additional kidney indications, specifically Delayed Graft Function (DGF) and Primary Focal Segmental Glomerulosclerosis (FSGS). These expansions target significant patient populations, with approximately 13,000 patients in the U.S. having primary FSGS and DGF occurring in approximately 30-35% of deceased donor kidneys.

The kidney indication expansion strategy is outlined here:

Additionally, Apellis is advancing a combination therapy of SYFOVRE and APL-3007, initiating a Phase 2 trial to evaluate safety, biologic activity, and pharmacodynamics. This next-generation treatment aims to comprehensively block complement activity in the retina and choroid, potentially improving efficacy.

Detailed Financial Analysis

Beyond the top-line figures, Apellis reported R&D expenses of $67.0 million in Q2 2025, down from $78.0 million in Q2 2024. SG&A expenses increased slightly to $131.1 million from $128.1 million in the prior year. The company posted a net loss of $42.2 million, compared to $37.7 million in Q2 2024.

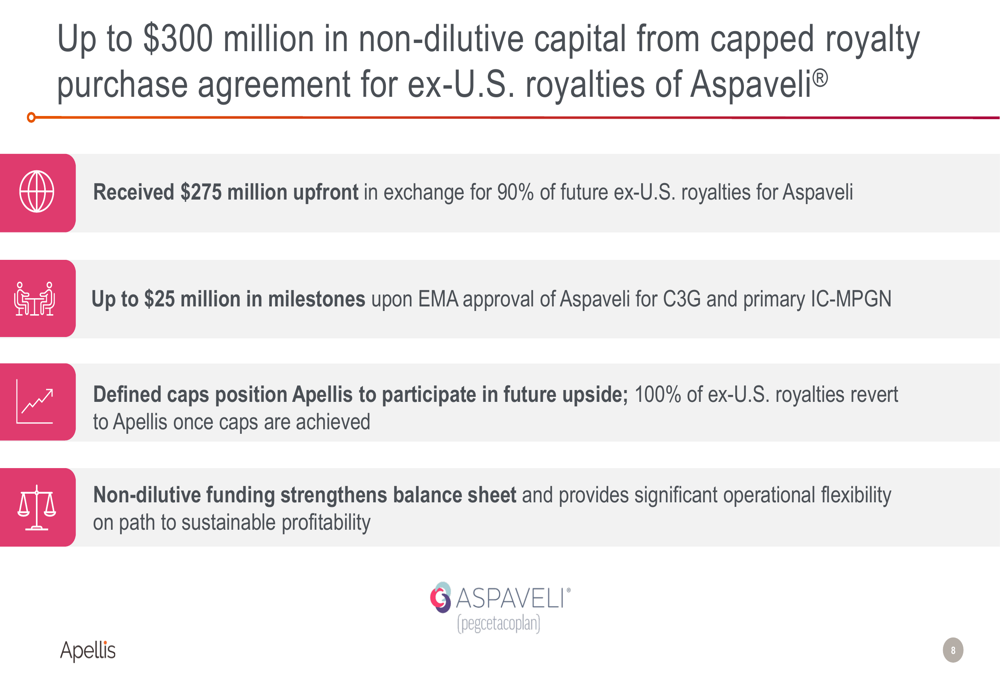

Apellis significantly strengthened its balance sheet through a royalty purchase agreement for ex-U.S. royalties of Aspaveli. The company received $275 million upfront in exchange for 90% of future ex-U.S. royalties, with the potential for an additional $25 million in milestones upon EMA approval of Aspaveli for C3G and primary IC-MPGN.

The terms of this non-dilutive funding arrangement are detailed here:

Forward-Looking Statements

Apellis projects that its existing cash, combined with the $275 million from the royalty purchase agreement and future product sales, will be sufficient to fund operations to sustainable profitability. The company is positioning EMPAVELI for potential blockbuster status, estimating approximately 5,000 C3G/IC-MPGN patients in the U.S.

The company outlined several initiatives to drive SYFOVRE demand and new patient starts, including connecting with patients through direct-to-consumer campaigns, highlighting the importance of early intervention, broadening reach to the eyecare community, and educating professionals on reimbursement best practices.

SYFOVRE’s market positioning is reinforced by its differentiated clinical profile:

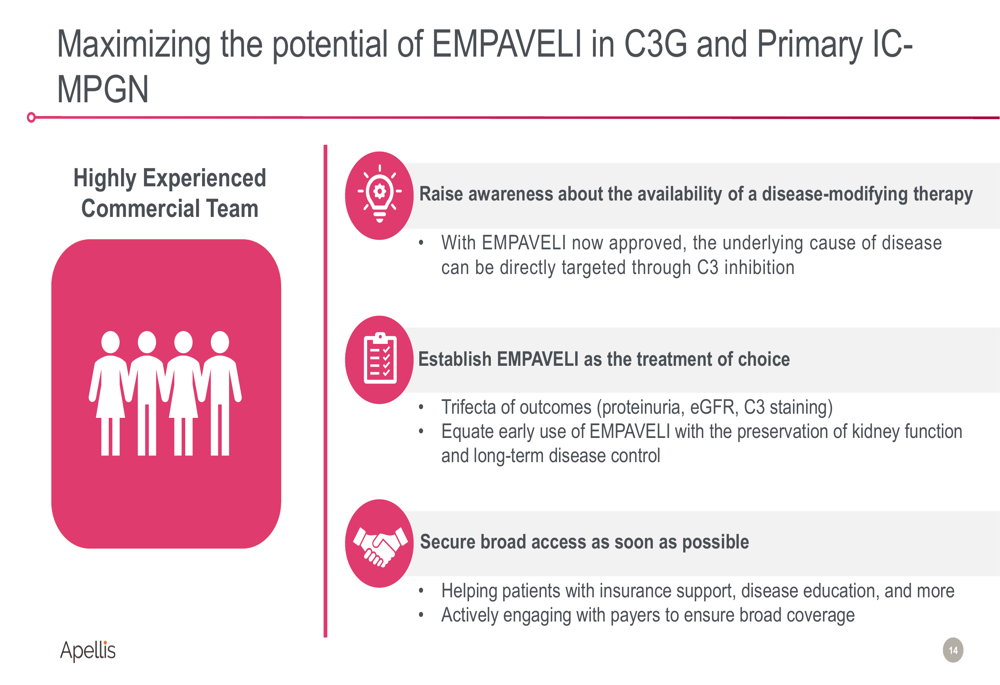

Apellis is also implementing a strategic plan to maximize EMPAVELI’s potential in C3G and Primary IC-MPGN:

Despite the positive developments in product approvals and market expansion, investors appear concerned about the year-over-year revenue decline and increased net loss. The company’s focus on long-term growth through new indications and combination therapies will be critical to reversing the recent stock price decline and achieving the projected path to profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.