Denison Mines announces $250 million convertible notes offering

Introduction & Market Context

Appian Corporation (NASDAQ:APPN) released its Q2 2025 earnings presentation on August 7, 2025, revealing strong cloud subscription growth and positive adjusted EBITDA. The low-code automation platform provider saw its shares jump 9.46% in premarket trading to $29.50, recovering some ground after closing at $26.95 the previous day.

The company continues its strategic shift toward a subscription-based revenue model while emphasizing AI integration within business processes as a key differentiator in the increasingly competitive automation market.

Quarterly Performance Highlights

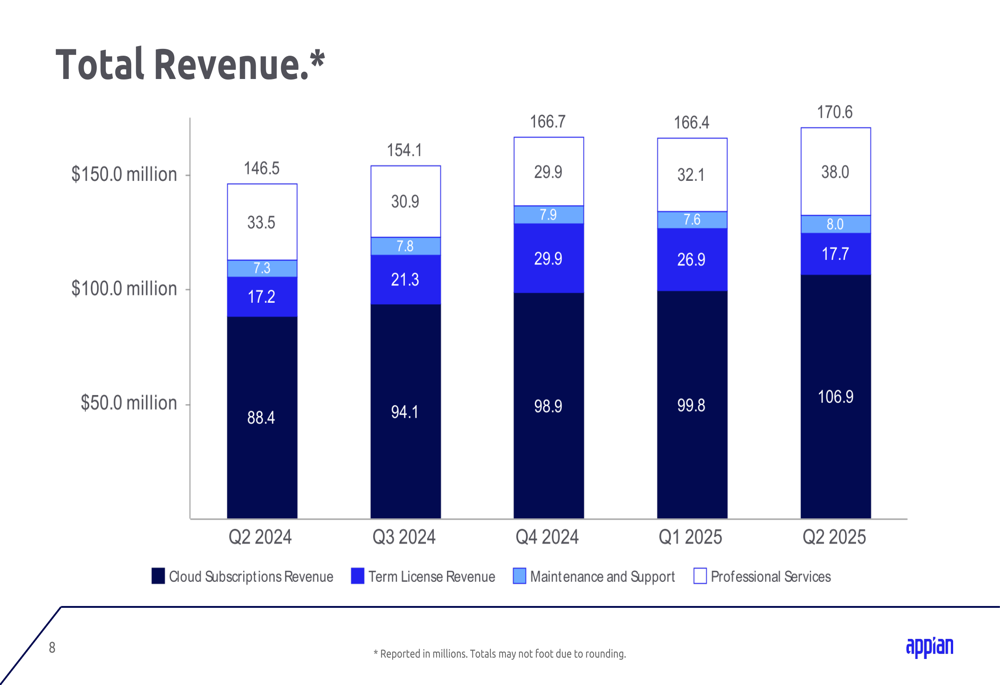

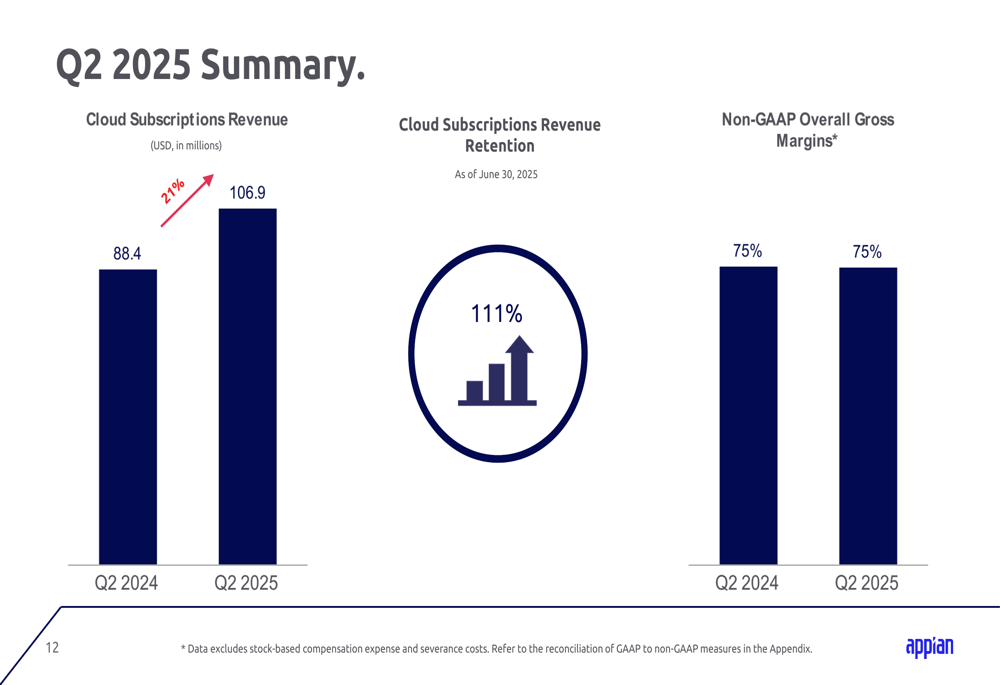

Appian reported total revenue of $170.6 million for Q2 2025, representing a 17% year-over-year increase. Cloud subscriptions revenue, the company’s primary growth driver, reached $106.9 million, up 21% compared to Q2 2024.

As shown in the following chart of quarterly revenue breakdown:

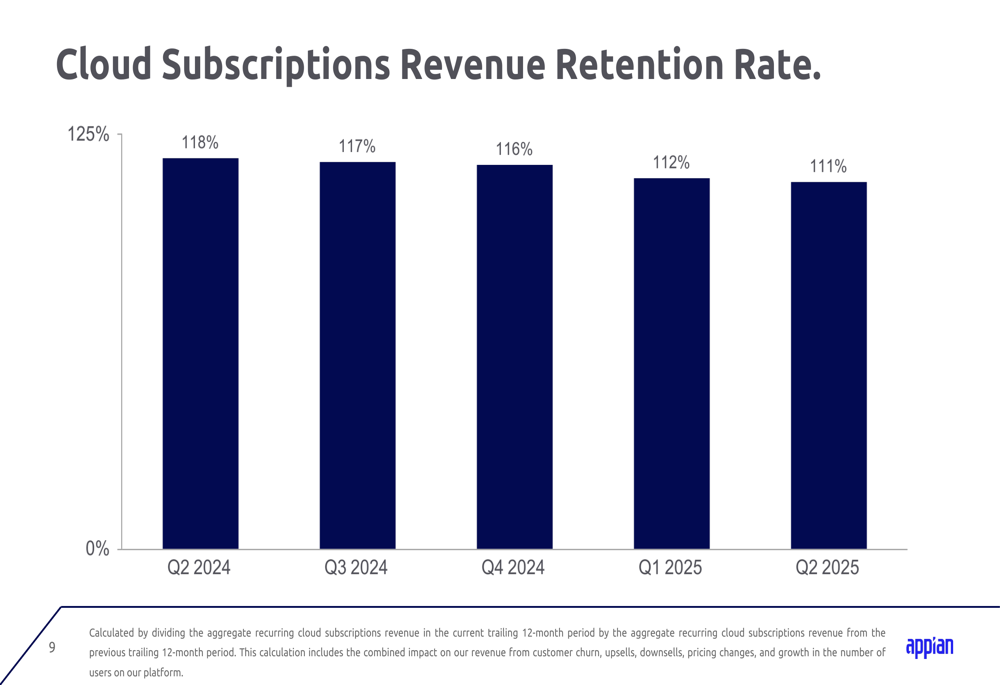

The company maintained a cloud subscriptions revenue retention rate of 111%, though this metric has been gradually declining from 118% in Q2 2024.

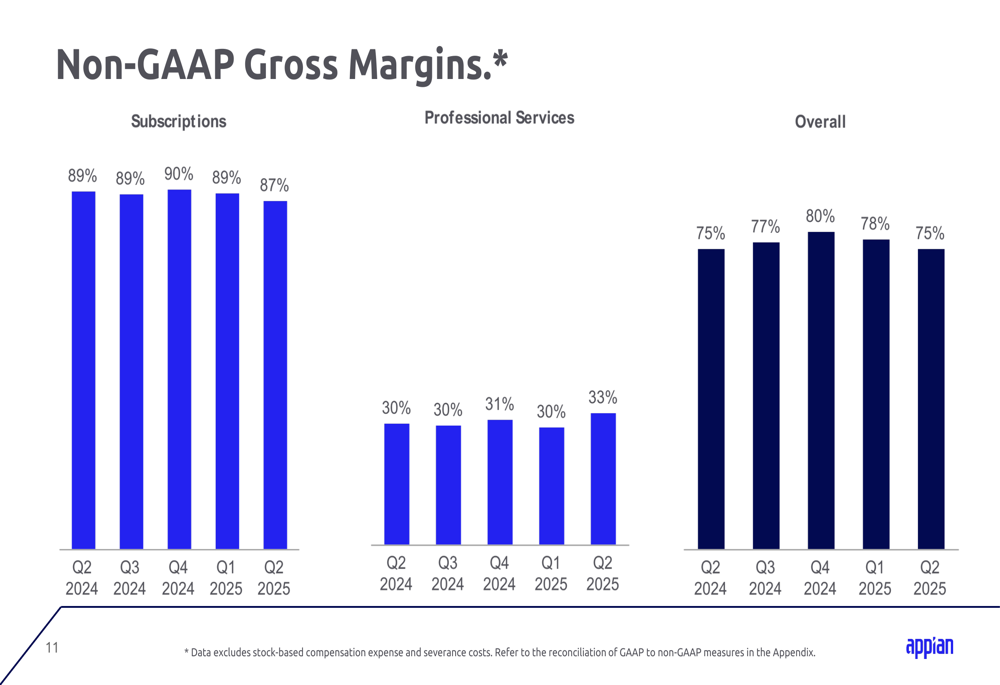

Appian achieved an adjusted EBITDA of $8.1 million for the quarter, demonstrating continued profitability. The company’s non-GAAP gross margins remained strong at 75% overall, with subscriptions gross margin at 87% and professional services gross margin improving to 33% compared to 30% in the same period last year.

Detailed Financial Analysis

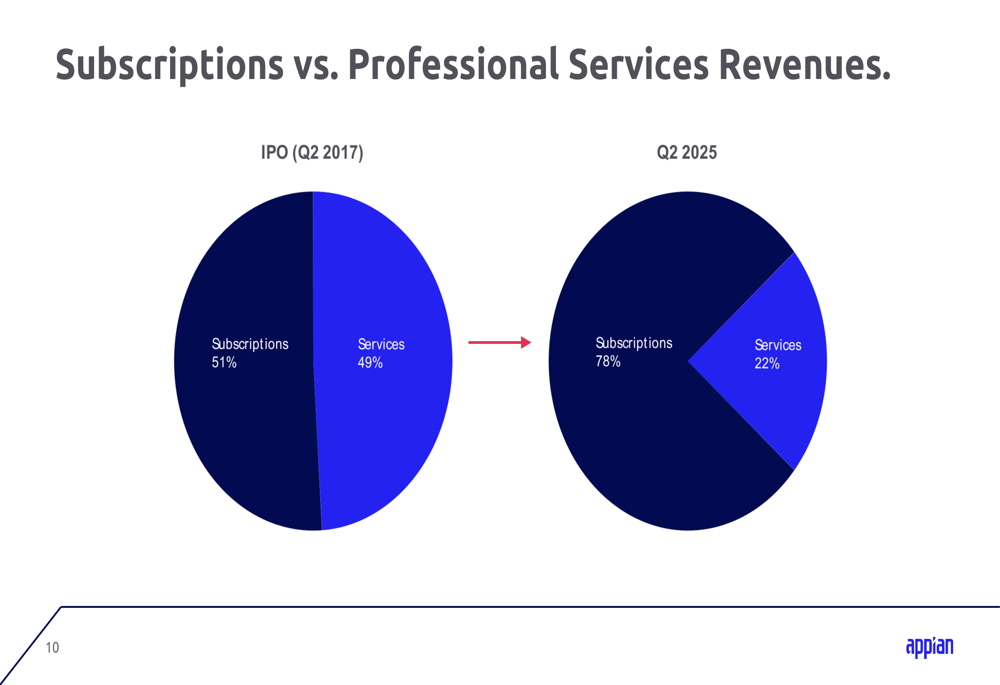

Appian’s business model continues to evolve toward higher-margin subscription revenue. The company highlighted that subscriptions now account for 78% of total revenue, compared to just 51% at the time of its IPO in Q2 2017.

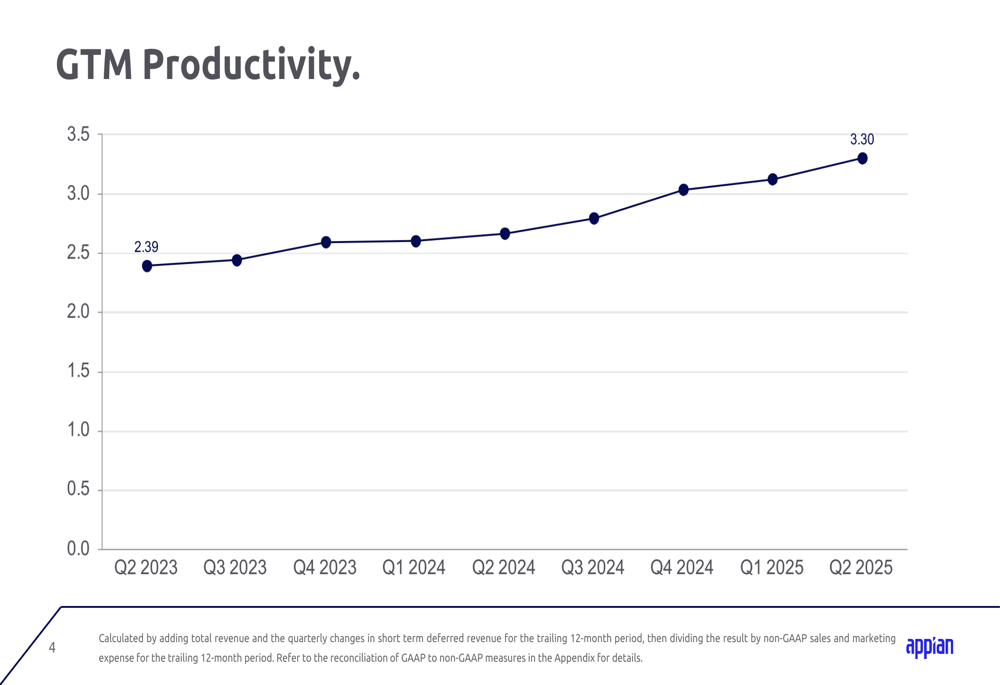

The company’s go-to-market efficiency has also improved significantly, with GTM productivity increasing from 2.39 in Q2 2023 to 3.30 in Q2 2025. This metric, calculated by dividing trailing 12-month revenue plus changes in short-term deferred revenue by non-GAAP sales and marketing expense, indicates Appian is generating more revenue per dollar spent on sales and marketing.

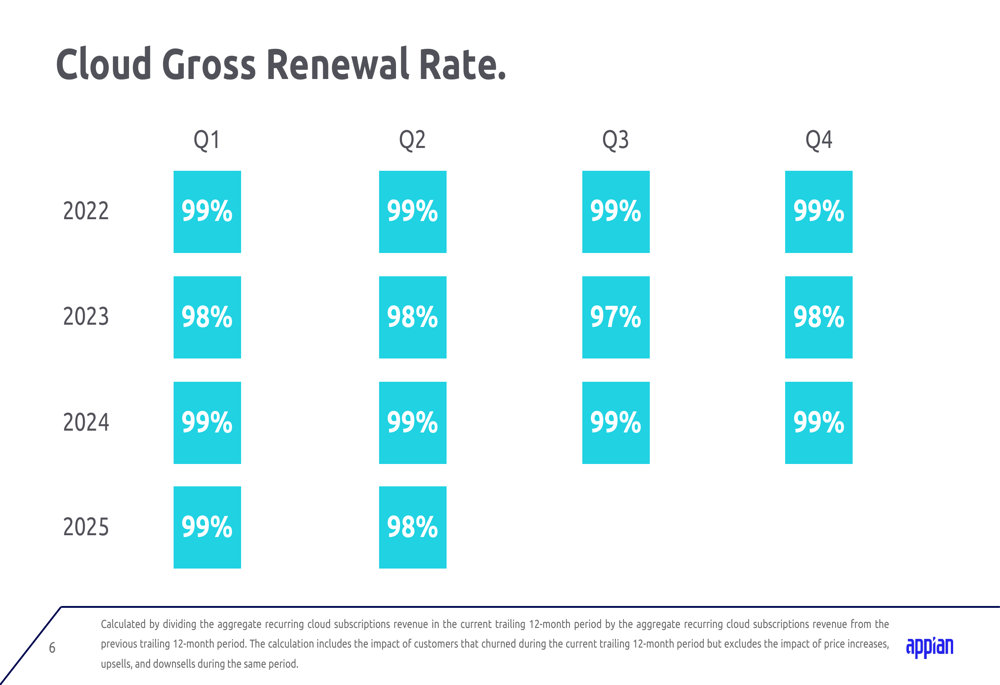

Customer retention remains strong, with a cloud gross renewal rate of 98% in Q2 2025, consistent with historical performance in the 97-99% range.

Strategic Initiatives

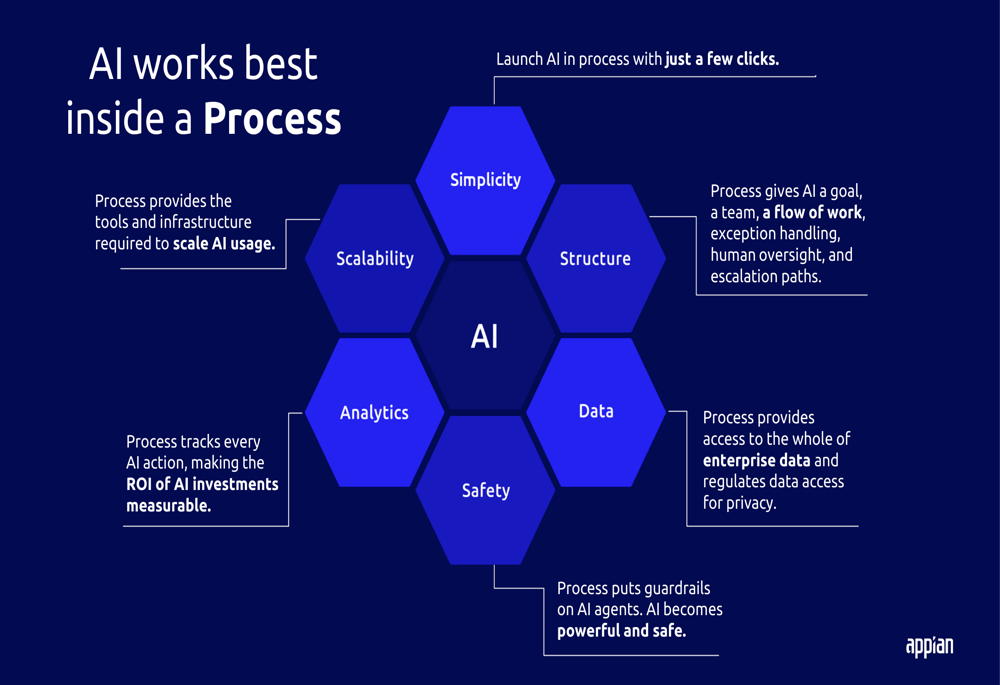

Appian is positioning itself at the intersection of process automation and artificial intelligence. The company’s presentation emphasized that "AI works best inside a process," highlighting six key benefits of this integration: simplicity, scalability, analytics, safety, structure, and data access.

This strategic focus builds on momentum reported in Q1 2025, when the company noted that AI adoption among its cloud customers had reached 70%, with production AI usage growing nearly eightfold year-over-year.

The company’s emphasis on AI as "a worker, not a helper" appears to be resonating with customers, particularly in the government sector where Appian reported strong bookings growth in Q1.

Forward-Looking Statements

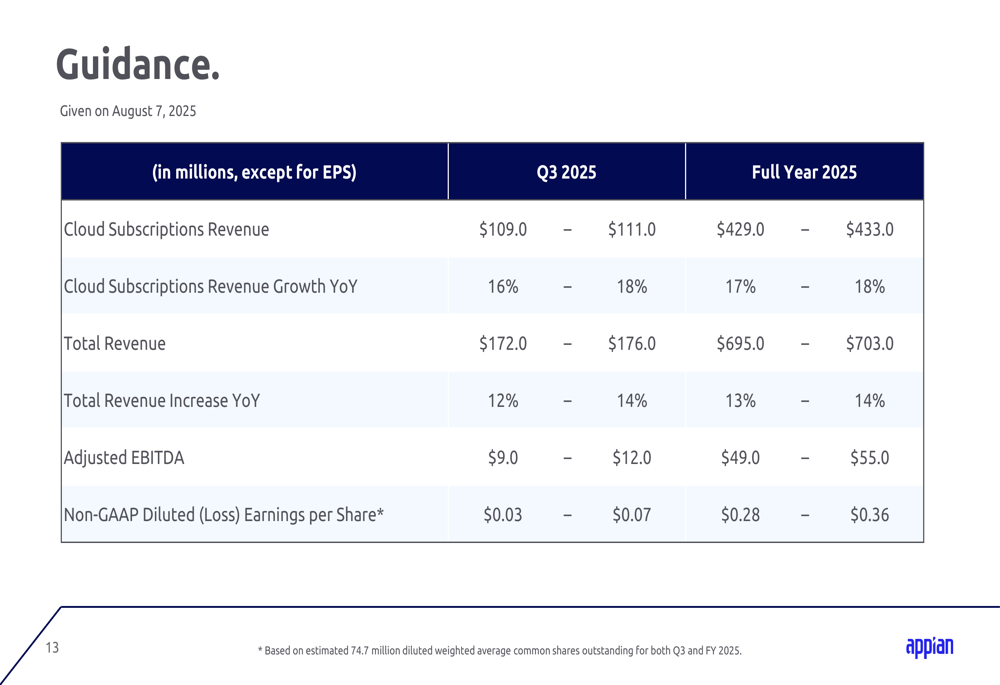

Appian provided guidance for both Q3 2025 and the full year, projecting continued growth in cloud subscriptions revenue and total revenue.

For Q3 2025, the company expects:

- Cloud subscriptions revenue between $109.0-$111.0 million (16-18% YoY growth)

- Total (EPA:TTEF) revenue between $172.0-$176.0 million (12-14% YoY growth)

- Adjusted EBITDA between $9.0-$12.0 million

For the full year 2025, Appian raised its guidance to:

- Cloud subscriptions revenue between $429.0-$433.0 million (17-18% YoY growth)

- Total revenue between $695.0-$703.0 million (13-14% YoY growth)

- Adjusted EBITDA between $49.0-$55.0 million

This updated guidance represents an increase from the previous outlook provided in Q1, when the company projected full-year cloud subscription revenue of $419-$423 million and total revenue of $680-$688 million.

The company’s Q2 2025 performance summary highlights the key metrics driving its growth:

With consistent cloud revenue growth, improving profitability metrics, and a strategic focus on AI integration, Appian appears well-positioned to maintain its growth trajectory through the remainder of 2025, despite ongoing challenges in the broader technology sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.