Raytheon awarded $71 million in Navy contracts for missile systems

Aramark Holdings (NYSE:ARMK) reported strong financial results in its Q3 fiscal 2025 presentation on August 5, highlighting revenue growth across segments and significant margin expansion. Despite the positive results, the company’s stock was down 3.97% in premarket trading, suggesting investors may have expected even stronger performance.

Quarterly Performance Highlights

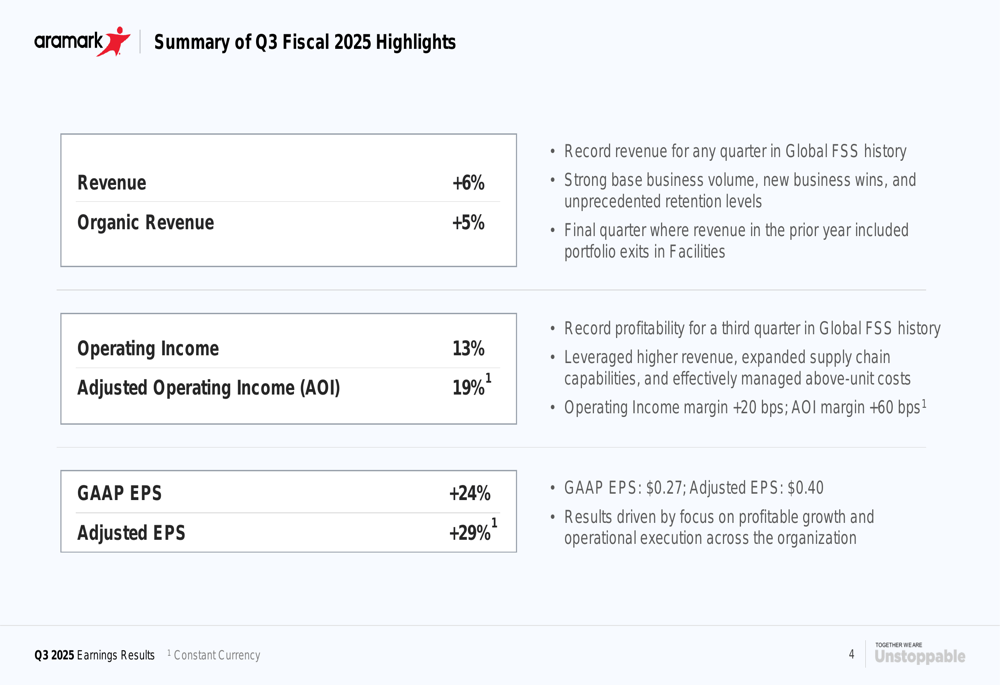

Aramark delivered solid growth in the third quarter, with revenue increasing by 6% and organic revenue rising by 5%. The company reported a 13% increase in operating income and a 19% jump in adjusted operating income (AOI), reflecting successful cost management and operational efficiencies.

"We achieved record revenue for a Global FSS quarter, driven by strong base business performance," the company noted in its presentation. The quarter was also the final one to include portfolio exits in Facilities.

Earnings per share showed significant improvement, with GAAP EPS increasing by 24% to $0.27 and adjusted EPS rising by 29% to $0.40. The company attributed these gains to higher revenue levels, supply chain improvements, and disciplined cost management.

As shown in the following financial highlights slide:

Segment Analysis

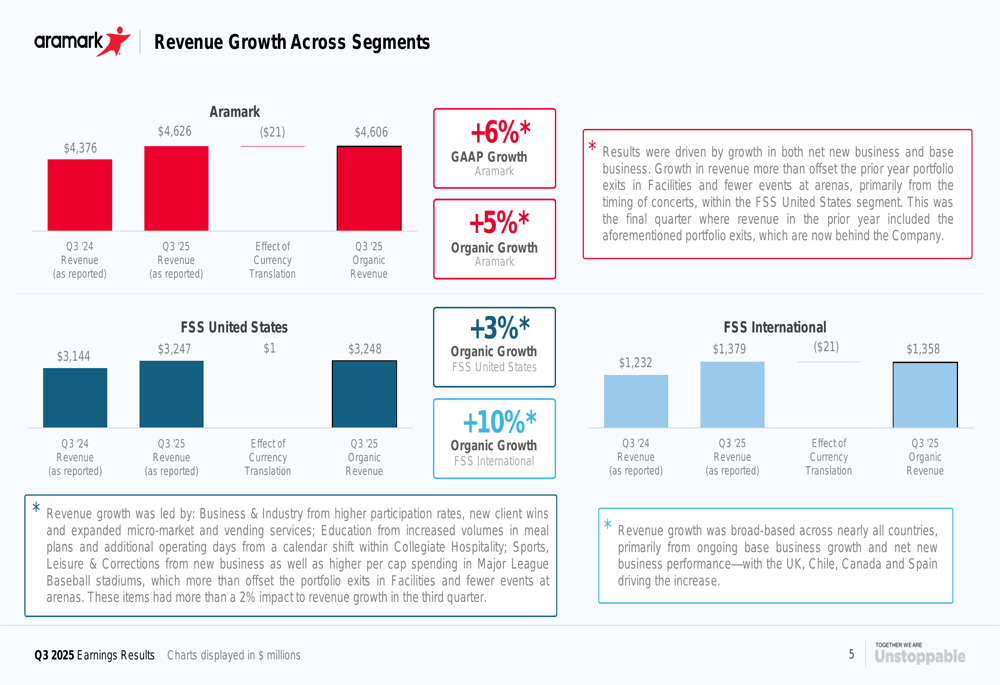

Revenue growth was uneven across Aramark’s business segments. While FSS United States posted organic growth of 3%, FSS International delivered a robust 10% organic growth rate. The international growth was broad-based, with particularly strong performance in the UK, Chile, Canada, and Spain.

The company’s U.S. business saw growth across multiple sectors, including Business & Industry, Education, and Sports/Leisure/Corrections. Meanwhile, the international segment continued its expansion into new markets, including Germany and Korea.

The following slide illustrates revenue growth across segments:

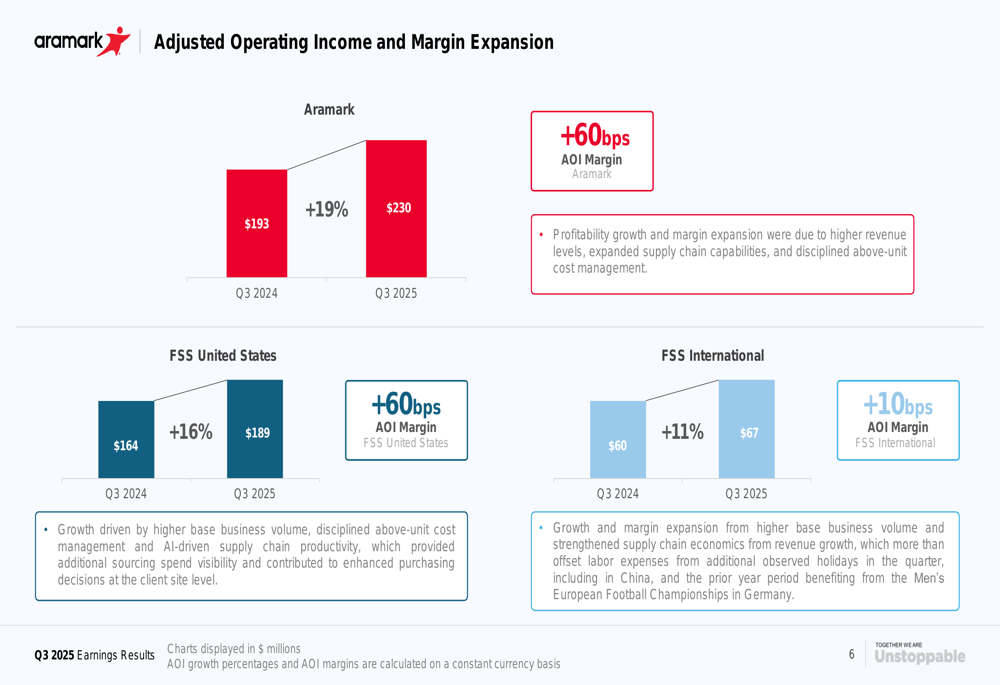

Profitability also improved across the board, with Aramark’s overall AOI margin increasing by 60 basis points. FSS United States saw a similar 60 basis point improvement in AOI margin, while FSS International’s margin expanded by 10 basis points.

The margin expansion was primarily driven by higher revenue levels, enhanced supply chain capabilities, and effective cost management, as shown in this slide:

Client Retention and Business Growth

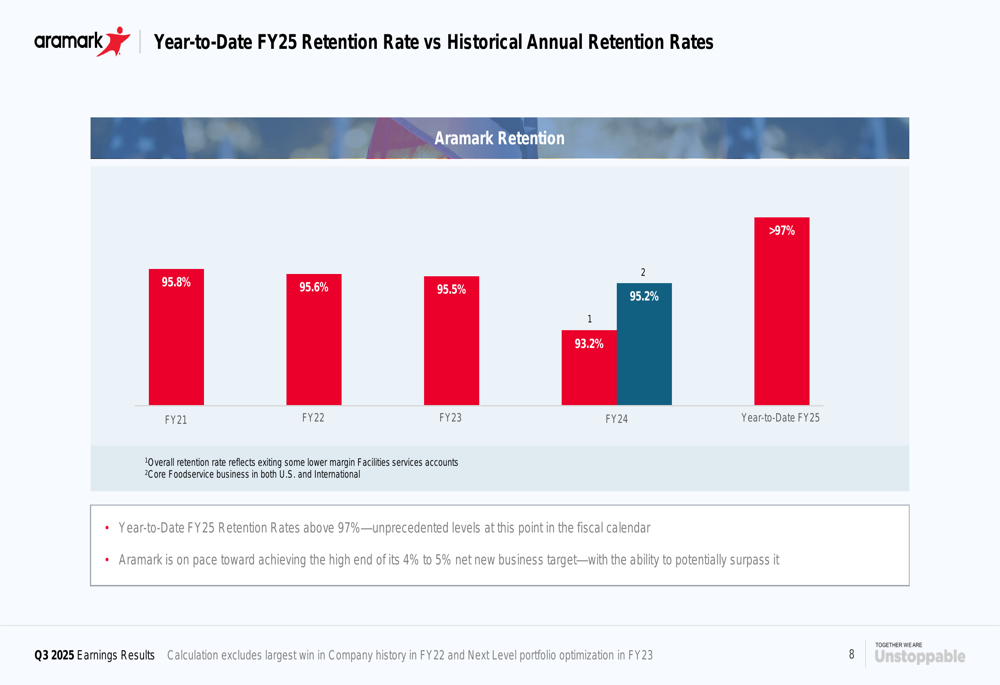

One of the most impressive aspects of Aramark’s performance was its client retention rate, which exceeded 97% year-to-date in fiscal 2025. The company described this retention level as "unprecedented" and indicated it was on pace to achieve the high end of its 4% to 5% net new business target.

The strong retention rates suggest Aramark is successfully maintaining client relationships while continuing to add new business. This performance stands in contrast to the previous quarter (Q2 2025), where the company reported a revenue miss despite an EPS beat.

The following slide shows Aramark’s retention rate compared to historical performance:

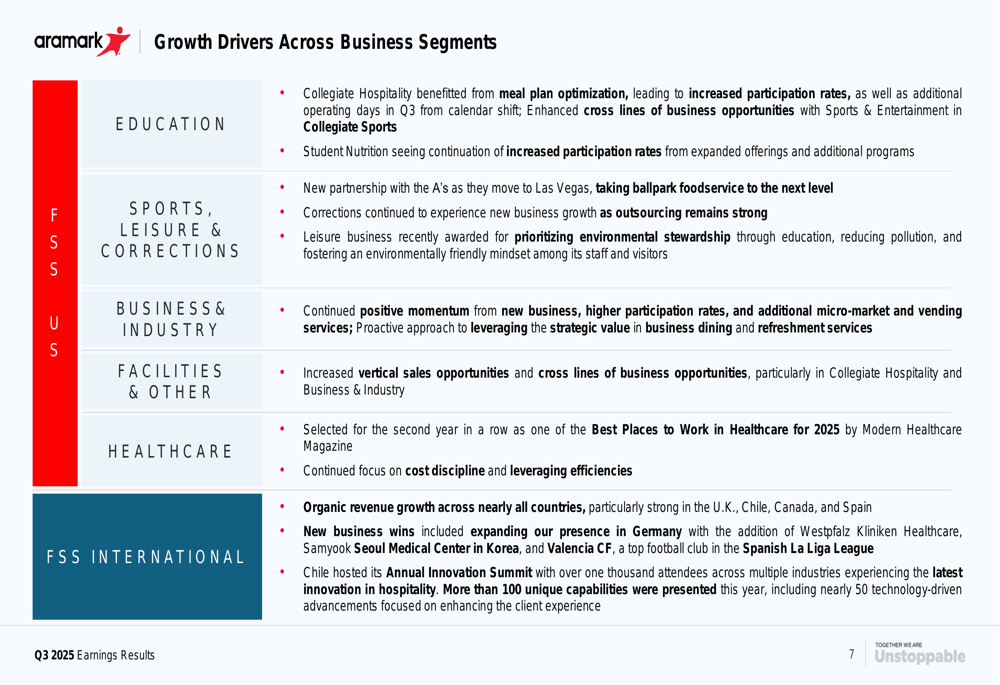

Growth drivers varied across business segments. In Education, the company benefited from meal plan optimization and cross-lines of business in Collegiate Sports. The Sports/Leisure/Corrections segment saw a new partnership with the A’s and continued growth in corrections. Business & Industry experienced momentum from new business and higher participation rates.

The company’s growth drivers across segments are detailed in this slide:

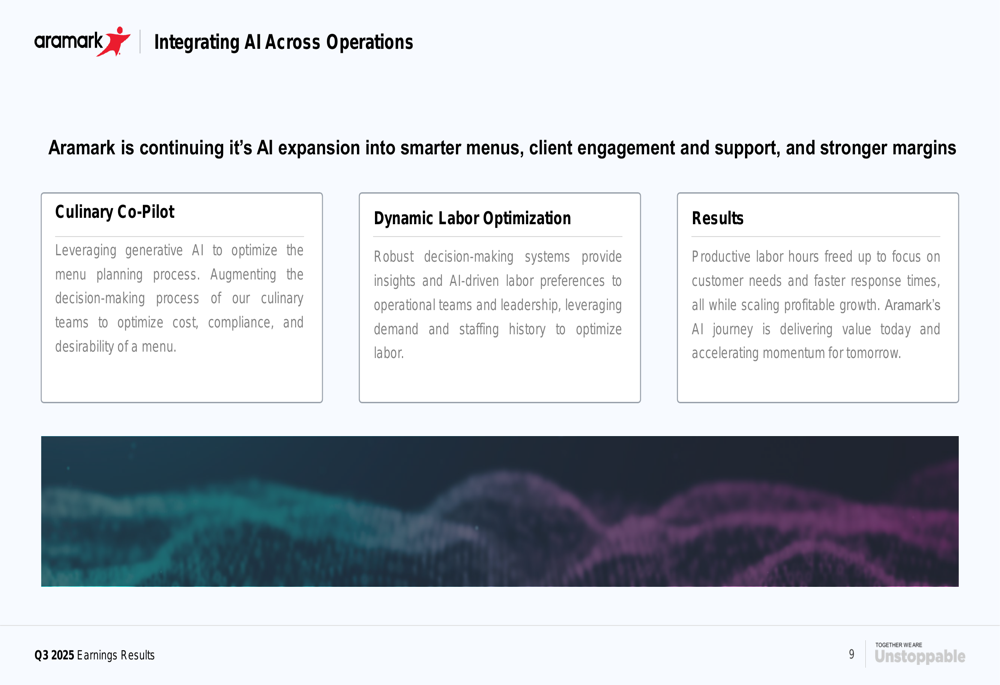

Strategic Initiatives: AI Integration

Aramark highlighted its expanding use of artificial intelligence across operations as a key strategic initiative. The company is implementing AI in three main areas: menu planning, client engagement and support, and margin enhancement.

The "Culinary Co-Pilot" uses AI to optimize menu planning, while "Dynamic Labor Optimization" provides AI-driven labor preferences. These initiatives are designed to improve labor productivity, enhance customer service, and scale profitable growth.

As illustrated in the following slide on AI integration:

Forward-Looking Statements

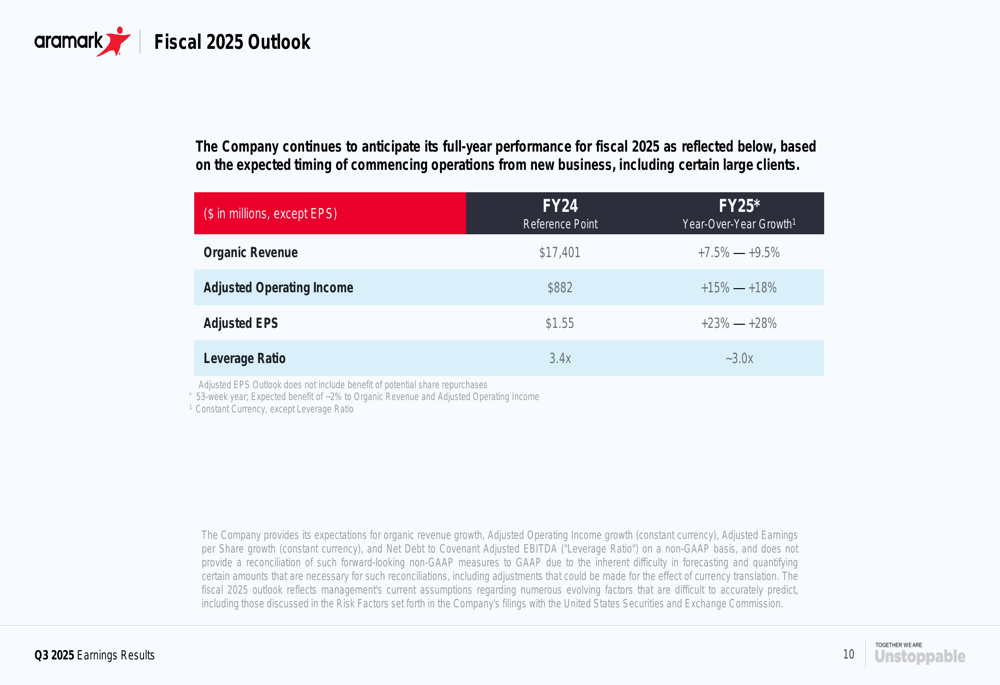

Looking ahead, Aramark provided a positive outlook for fiscal 2025. The company expects organic revenue to grow between 7.5% and 9.5%, adjusted operating income to increase by 15% to 18%, and adjusted EPS to rise by 23% to 28%. The leverage ratio is projected to be approximately 3.0x.

The company’s financial outlook is summarized in this slide:

These projections reflect Aramark’s confidence in its business model and growth strategy. However, the premarket stock decline of 3.97% suggests investors may have concerns about the company’s ability to meet these targets or about broader economic factors affecting the food service and facilities management industry.

Key modeling assumptions for fiscal 2025 include net interest expense of approximately $330 million, an adjusted tax rate of around 26%, and a share count of approximately 271 million. The company also noted that seasonality drives AOI margin, primarily in Q1 and Q4 for Education and Sports/Entertainment businesses.

Aramark’s ability to continue its growth trajectory will depend on successful execution of its AI initiatives, maintaining its high client retention rates, and navigating potential economic headwinds in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.