AIG earnings beat by $0.50, revenue topped estimates

Introduction & Market Context

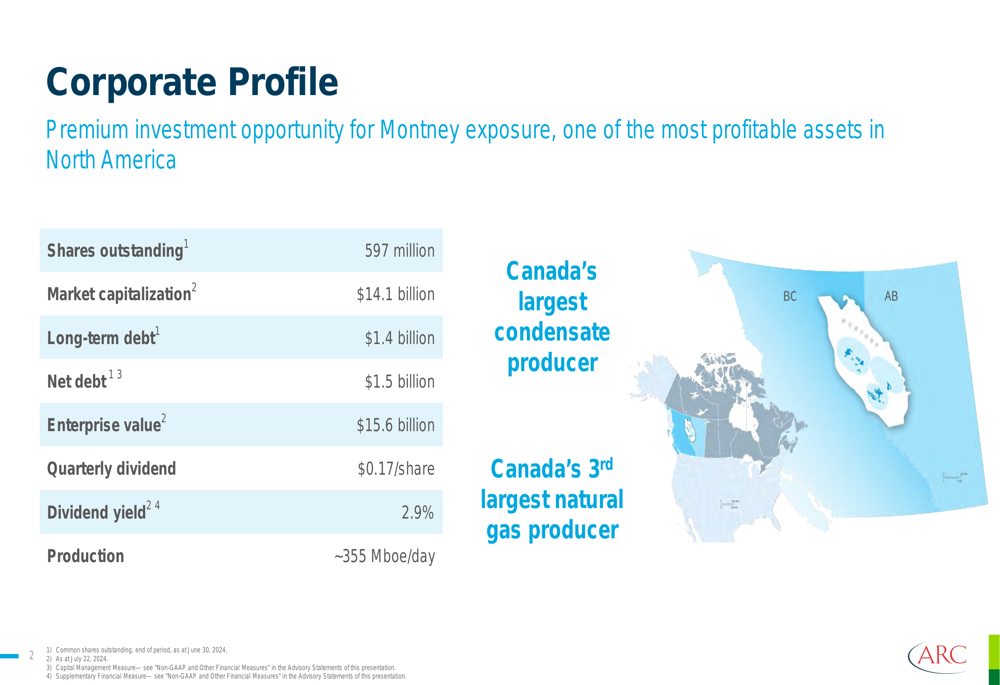

ARC Resources Ltd . (TSX:ARX), Canada’s largest condensate producer and third-largest natural gas producer, presented its Q2 2024 investor slides outlining the company’s strategic direction and growth plans. With a market capitalization of $14.1 billion and an enterprise value of $15.6 billion, ARC maintains a strong financial position with relatively low long-term debt of $1.4 billion and net debt of $1.5 billion.

The company’s current production stands at approximately 355,000 barrels of oil equivalent per day (boe/d), with operations concentrated in the prolific Montney formation spanning British Columbia and Alberta. ARC’s shares closed at $30.79 on June 18, 2025, near its 52-week high of $31.56, reflecting investor confidence in the company’s execution and growth strategy.

As shown in the following corporate profile, ARC offers a quarterly dividend of $0.17 per share, representing a 2.9% yield, as part of its commitment to shareholder returns:

Strategic Initiatives

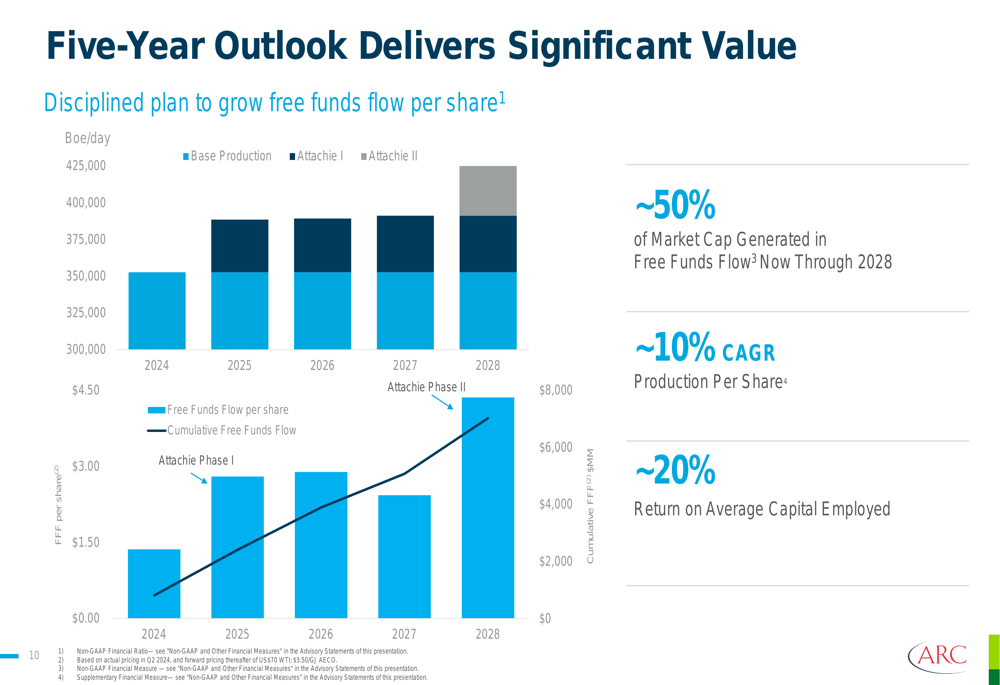

ARC Resources has outlined an ambitious five-year plan focused on disciplined growth and shareholder returns. The company aims to more than double free funds flow per share by 2028 through strategic Montney development while reducing share count. Management has committed to returning essentially all free funds flow to shareholders, supported by world-class assets with decades of inventory runway and owned infrastructure with secured long-term market access.

The five-year outlook projects production growth from approximately 350,000 boe/d in 2024 to over 400,000 boe/d by 2028, with cumulative free funds flow expected to exceed $8 billion during this period. This represents approximately 50% of the company’s current market capitalization generated in free funds flow through 2028, with production per share growing at a compound annual growth rate (CAGR) of approximately 10%.

As illustrated in the following chart, ARC’s five-year plan shows significant production and free funds flow growth potential:

The company’s capital allocation strategy balances reinvestment for growth with shareholder returns. ARC has reduced its reinvestment rate over time and expects it to reach approximately 50% by 2028, allowing for increased returns to shareholders. The company prioritizes balance sheet strength with an investment-grade rating, growing the base dividend with the business rather than commodity prices, and executing share repurchases when intrinsic value exceeds share price.

ARC’s return of capital strategy includes a sustainable dividend with projected growth of over 10% CAGR in dividend per share while maintaining a conservative payout ratio of approximately 15% of funds from operations. The company has already reduced its share count by more than 18% since September 2021 and aims to reduce it to pre-business combination levels.

Detailed Asset Portfolio

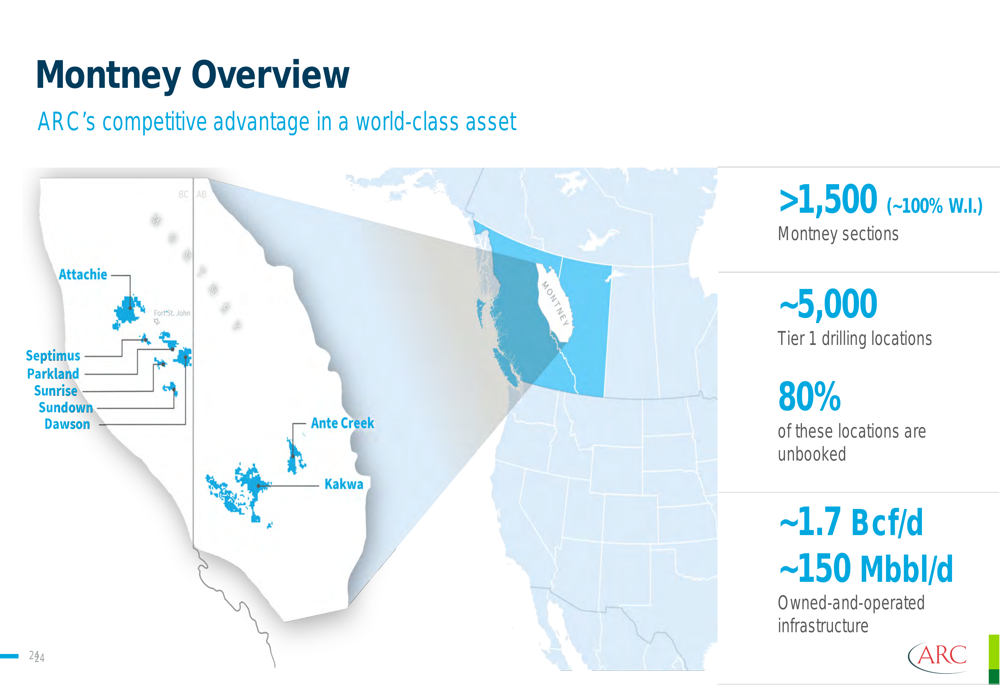

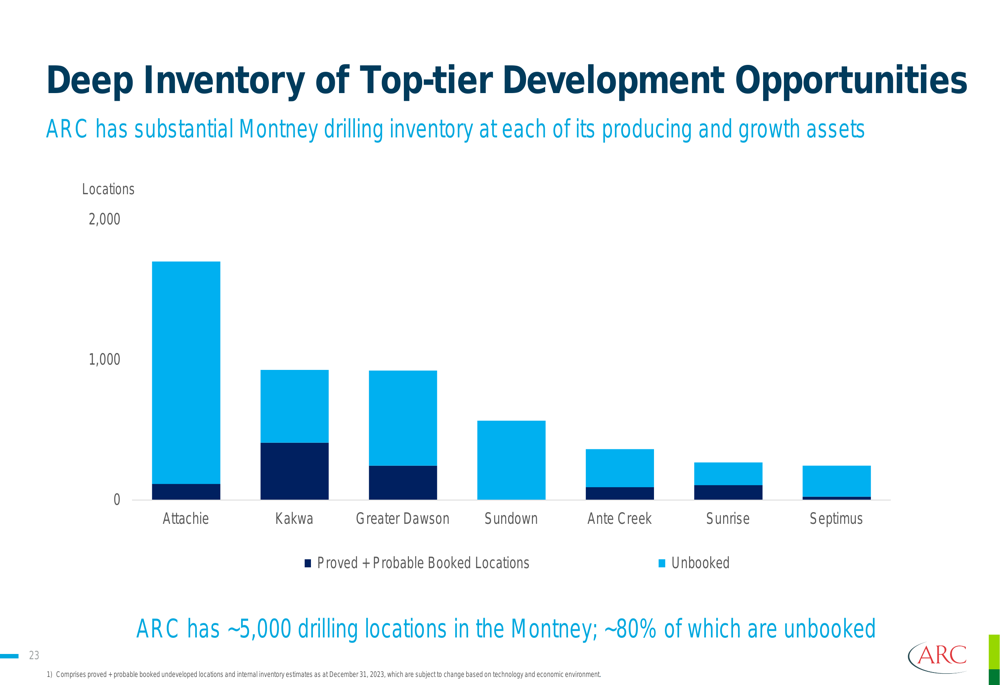

ARC Resources has transformed from a company with dispersed assets across Alberta and British Columbia in 2014 to the largest Montney producer with a concentrated, high-quality asset base. The company now controls over 1 million Montney acres with approximately 5,000 drilling locations, 80% of which remain unbooked, providing decades of development potential.

The company’s Montney assets include:

- Kakwa: 175,000 boe/d with capacity to sustain this level for the next 15 years

- Greater Dawson: Flagship asset delivering superior free funds flow with a long inventory runway

- Sunrise: Highly efficient, dry natural gas play interconnected to Coastal GasLink for West Coast LNG

- Attachie: ARC’s largest and most economic undeveloped asset with over 300 net sections in condensate-rich Montney

The following map provides an overview of ARC’s extensive Montney assets:

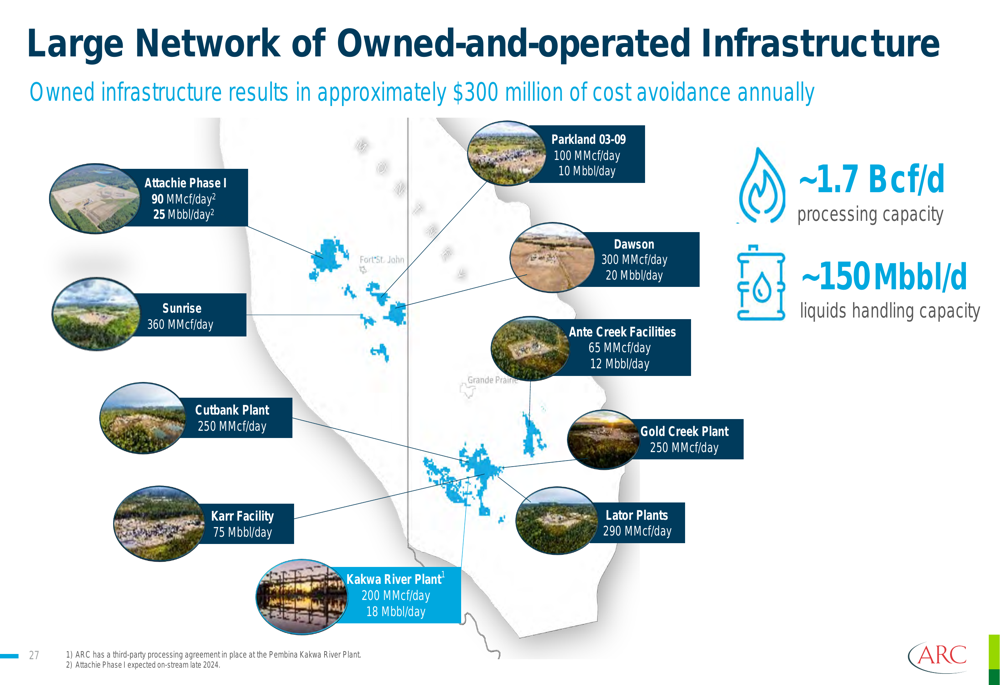

A key competitive advantage for ARC is its large network of owned-and-operated infrastructure, which results in approximately $300 million of cost avoidance annually. The company’s infrastructure includes processing capacity of approximately 1.7 Bcf/d and liquids handling capacity of approximately 150 Mbbl/d, providing operational flexibility and cost control.

As shown in the following infrastructure map, ARC’s facilities are strategically positioned across its core operating areas:

The company’s drilling inventory is substantial, with approximately 5,000 locations across its Montney assets. Approximately 80% of these locations are unbooked, providing significant future development potential beyond the currently booked reserves. The following chart illustrates the breakdown of drilling locations by region:

Attachie Development

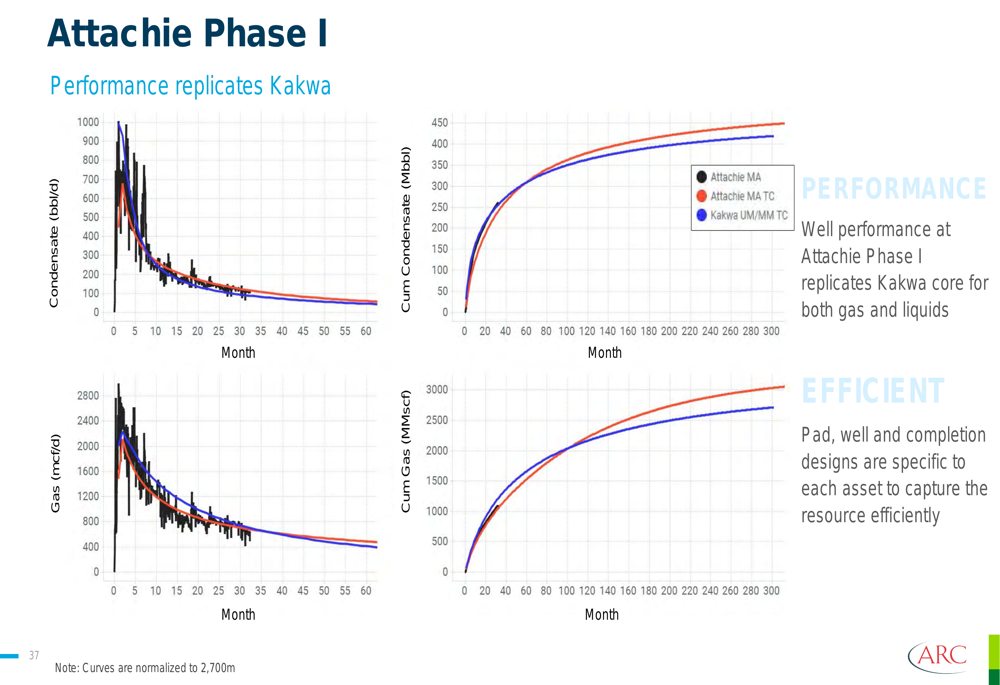

A key growth driver for ARC Resources is the Attachie Phase I development, which is described as the company’s largest and most economic undeveloped asset. The project is targeting full production capacity in 2025, with expected output of 40,000 boe/d (60% liquids and 40% natural gas).

The company has invested $740 million to construct and initially fill facilities to capacity, with projected asset-level funds flow of approximately $500 million in 2025. The project is expected to pay out in 2027 and deliver above cost of capital returns even at US$50/bbl WTI and C$2.50/mcf AECO pricing.

The following overview highlights key aspects of the Attachie Phase I development:

ARC reports that the Attachie Phase I project is tracking on-time and on-budget with no safety incidents. The TCPL sales line, water ponds, and major pipeline bridge are complete, while plant construction is approximately 75% complete. Liquids and gathering pipelines are on schedule and nearing completion, with the project on track to be electrified at start-up.

Well performance at Attachie Phase I is replicating results from the Kakwa core area for both gas and liquids production, as shown in the following performance comparison:

Marketing Strategy

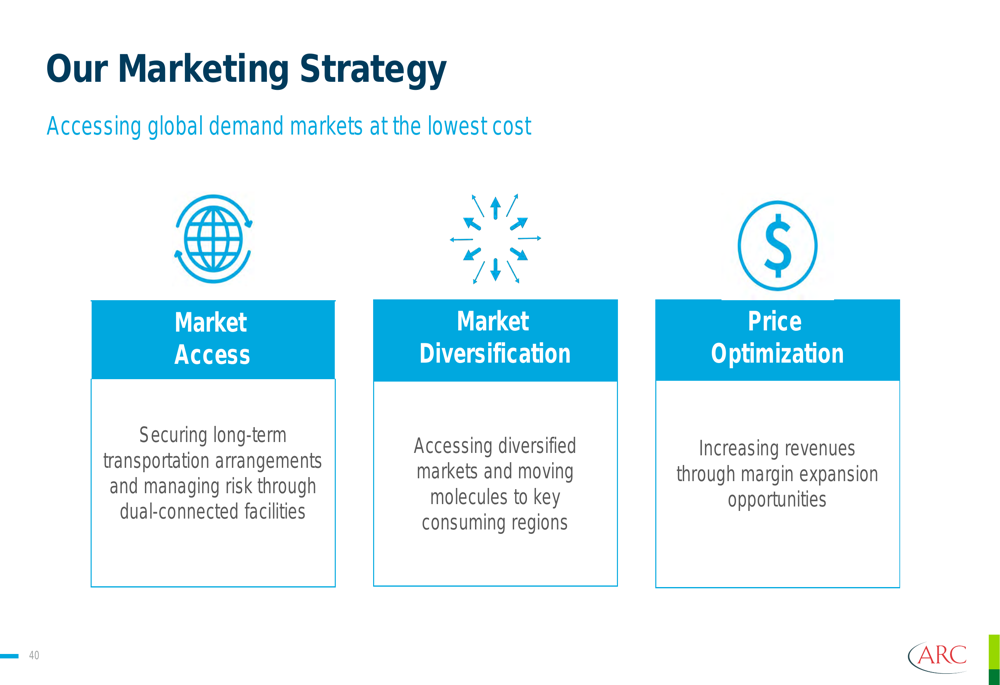

ARC Resources has implemented a comprehensive marketing strategy focused on securing global demand market access at the lowest cost. The strategy encompasses three key components: market access through long-term transportation arrangements, market diversification by accessing various consuming regions, and price optimization through margin expansion opportunities.

The company’s approach to natural gas marketing has resulted in an average premium to AECO pricing of 25% over the past decade. ARC’s natural gas portfolio is diversified across multiple pricing hubs, including Station 2, AECO, Malin (OTC:MLLNF), Dawn, and Henry Hub, reducing exposure to any single market.

As illustrated in the following marketing strategy overview, ARC is positioned to optimize value across its production portfolio:

For condensate, ARC notes that long-term demand remains resilient, with approximately 35% of Western Canadian Sedimentary Basin (WCSB) condensate demand met by imports from the U.S. market. Demand from oil sands operations continues to grow, supporting strong pricing for ARC’s condensate production.

Forward-Looking Statements

Looking ahead, ARC Resources has provided guidance for 2024 production of 350,000-360,000 boe/d, with capital expenditures of $1.75-1.85 billion. The company’s five-year plan targets production growth to over 400,000 boe/d by 2028, with a focus on increasing free funds flow per share at a CAGR of approximately 20%.

According to the Q1 2025 earnings report, ARC is on track with its growth plans, with guidance for 2025 production between 380,000 and 395,000 boe/d. The company anticipates Q2 2025 production to reach 380,000 boe/d, with second-half production expected to increase to 390,000-400,000 boe/d.

ARC’s CEO Terry Anderson emphasized the company’s financial goals in the Q1 2025 earnings call, stating, "Under strip prices, we are on track to generate 10% of our market cap in free cash flow this year." The company maintains a strong balance sheet with a net debt-to-cash flow ratio of 0.5x, providing financial flexibility to execute its growth strategy while returning capital to shareholders.

With its concentrated Montney asset base, extensive owned infrastructure, and disciplined capital allocation approach, ARC Resources is positioned to deliver on its five-year plan of doubling free funds flow per share while maintaining its commitment to shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.