Street Calls of the Week

ArcticZymes Technologies ASA (OB:AZT) presented its second quarter 2025 financial results on August 14, showing signs of recovery after a challenging first quarter. The company reported 5% revenue growth and a 50% increase in EBITDA, driven primarily by strong performance in its Biomanufacturing segment, which offset weakness in Molecular Tools.

Quarterly Performance Highlights

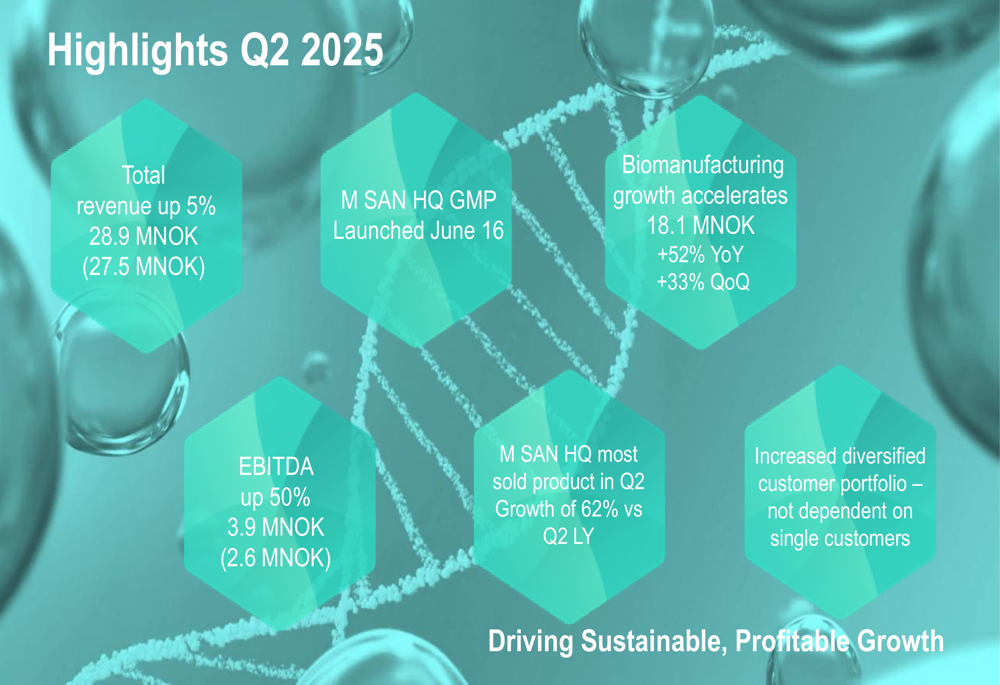

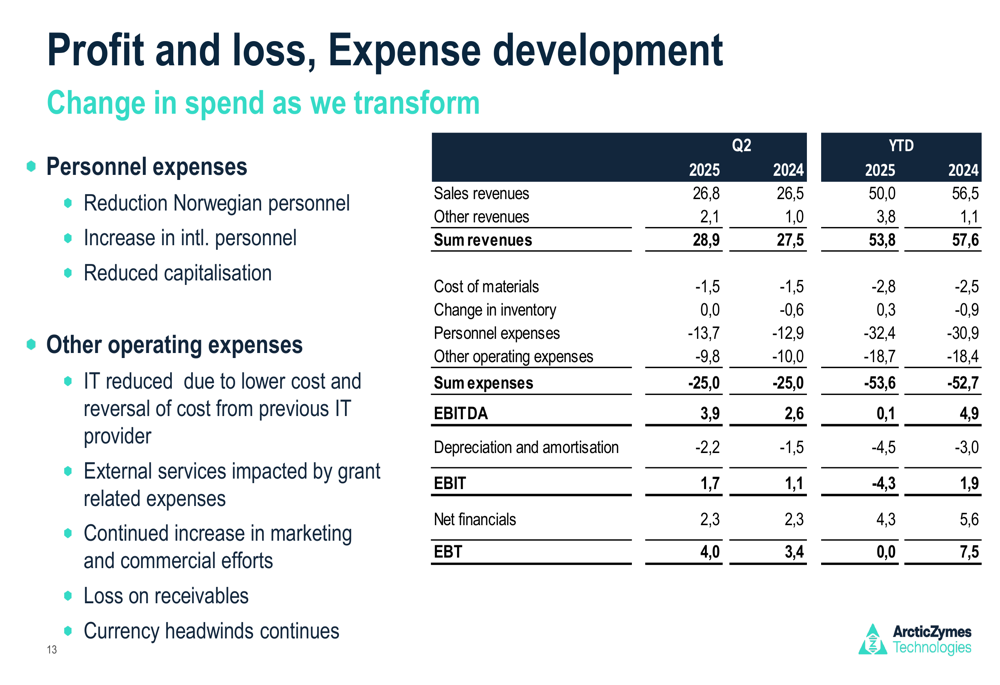

ArcticZymes reported total revenue of 28.9 million NOK for Q2 2025, up 5% from 27.5 million NOK in the same period last year. EBITDA increased by 50% to 3.9 million NOK, compared to 2.6 million NOK in Q2 2024, representing an EBITDA margin improvement from 9.5% to 13.5%.

The company’s performance marks a significant turnaround from Q1 2025, when it reported a revenue decline and negative EBITDA margin of -16%. This recovery is reflected in the company’s stock price, which has risen from 16.3 NOK after Q1 results to 19.2 NOK as of August 13, 2025.

As shown in the following highlights from the company’s presentation:

Segment Analysis

The company’s two main business segments showed dramatically different performance trajectories in Q2 2025, creating a tale of two businesses within ArcticZymes.

Biomanufacturing Strength

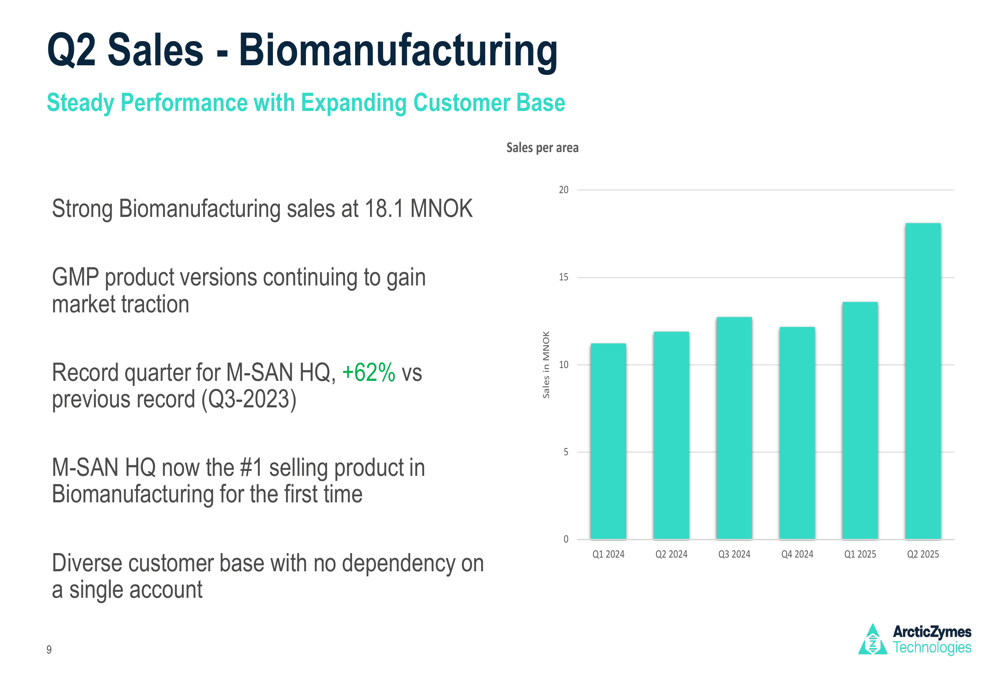

The Biomanufacturing segment delivered exceptional results with sales of 18.1 million NOK, representing 52% year-over-year growth and 33% quarter-over-quarter improvement. This segment now accounts for approximately 67% of total product sales, up from around 45% a year ago.

A key driver of this growth was the strong performance of M-SAN HQ, which became the company’s best-selling product for the first time, with 62% growth compared to Q2 2024. The company also highlighted its expanding and diversified customer base in this segment, reducing dependency on any single account.

The following chart illustrates the strong performance in the Biomanufacturing segment:

Molecular Tools Challenges

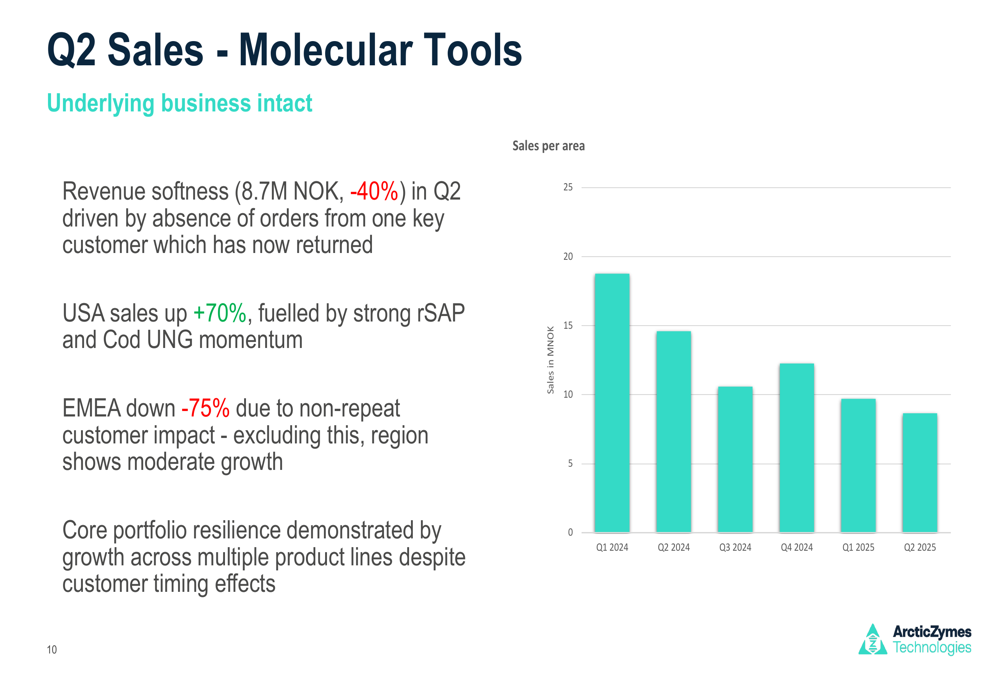

In contrast, the Molecular Tools segment faced significant headwinds, with revenue declining 40% to 8.7 million NOK. This weakness was primarily attributed to the absence of orders from one key customer, though management noted this customer has now returned.

Despite the overall decline, there were some positive indicators within this segment. USA sales increased by 70%, driven by strong momentum in rSAP and Cod UNG products. The company also emphasized the resilience of its core portfolio, with growth across multiple product lines despite customer timing effects.

The following chart details the performance of the Molecular Tools segment:

Strategic Initiatives

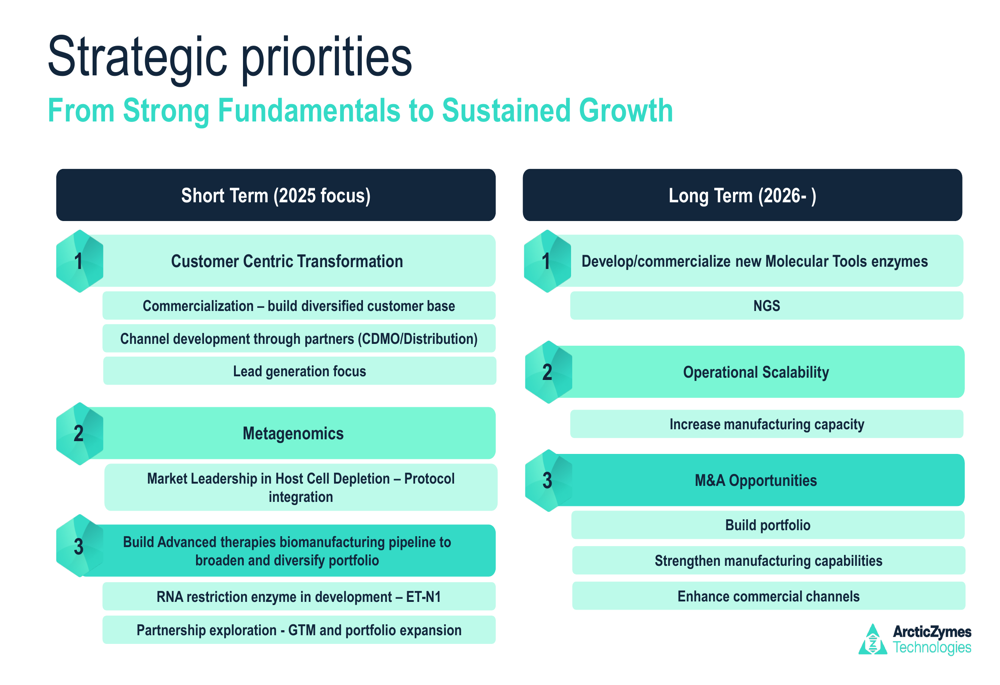

ArcticZymes outlined several strategic priorities aimed at driving sustainable, profitable growth. A significant milestone was the launch of GMP-grade M-SAN on June 16, which enables use in late-stage and commercial biomanufacturing workflows. This product was the single most sold item in Q2 and is expected to unlock new customer segments in viral vector and vaccine production.

The company’s strategic roadmap includes both short-term and long-term priorities:

For 2025, ArcticZymes is focusing on customer-centric transformation, market leadership in host cell depletion for metagenomics, and building its advanced therapies biomanufacturing pipeline. Longer-term goals include developing new Molecular Tools enzymes, increasing manufacturing capacity, and exploring M&A opportunities.

Financial Analysis

ArcticZymes maintained strong profitability despite mixed segment performance. The company’s gross margins remain above 90% on all products, and it continues to hold a strong cash position with no debt.

The detailed profit and loss statement shows the company’s financial performance for the quarter:

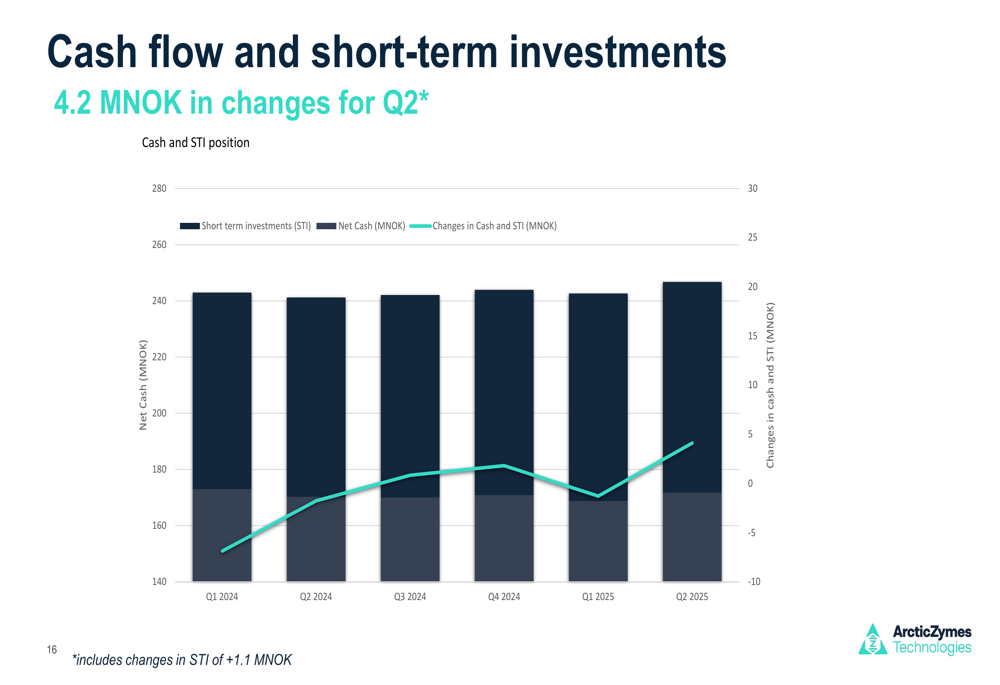

The company’s cash flow remained positive, with 4.2 million NOK in changes for Q2. ArcticZymes maintains a solid cash reserve of 240 million NOK, providing financial flexibility for potential investments and M&A activities.

Forward-Looking Statements

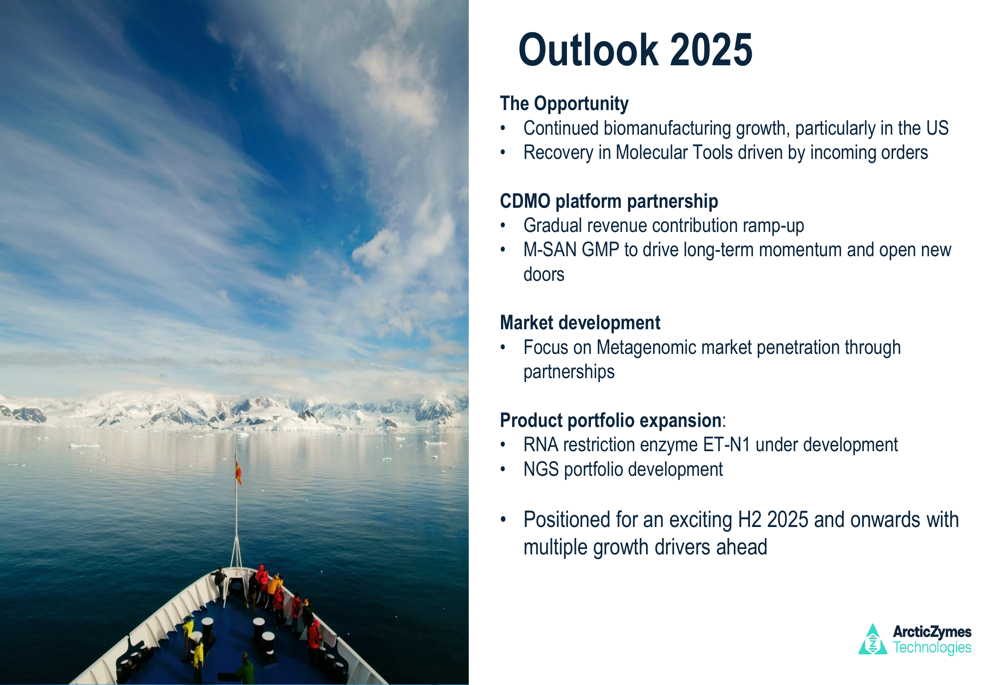

Looking ahead to the remainder of 2025, ArcticZymes expects continued growth in its Biomanufacturing segment, particularly in the US market, and a recovery in Molecular Tools driven by incoming orders from the previously absent key customer.

The company anticipates gradual revenue contribution from its CDMO platform partnership, with M-SAN GMP expected to drive long-term momentum. Additional growth drivers include focus on Metagenomic market penetration through partnerships and product portfolio expansion, including the development of RNA restriction enzyme ET-N1.

CEO Michael Akoh expressed confidence in the company’s strategic direction, noting that ArcticZymes is "positioned for an exciting H2 2025 and onwards with multiple growth drivers ahead." This optimism follows his Q1 statement that the company is "just tapping into the biomanufacturing nuclease market," suggesting significant growth potential in this area.

As ArcticZymes navigates the contrasting performance of its business segments, investors will be watching closely to see if the strong Biomanufacturing momentum can continue to offset challenges in Molecular Tools, and whether the company’s strategic initiatives will deliver the sustainable, profitable growth it promises.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.