Gold prices add to record high amid fiscal, tariff concerns

Introduction & Market Context

Arcutis Biotherapeutics (NASDAQ:ARQT) presented its second quarter 2025 financial results on August 6, showcasing substantial revenue growth and continued progress toward profitability. The dermatology-focused biopharmaceutical company reported significant commercial momentum for its ZORYVE portfolio across multiple indications, with strategic initiatives aimed at further expanding its market presence.

Despite the strong quarterly performance, Arcutis shares dipped 1.66% in aftermarket trading to $15.07, following a modest 0.23% gain during regular trading hours. The stock has traded between $8.03 and $17.75 over the past 52 weeks, currently sitting near the middle of that range.

Quarterly Performance Highlights

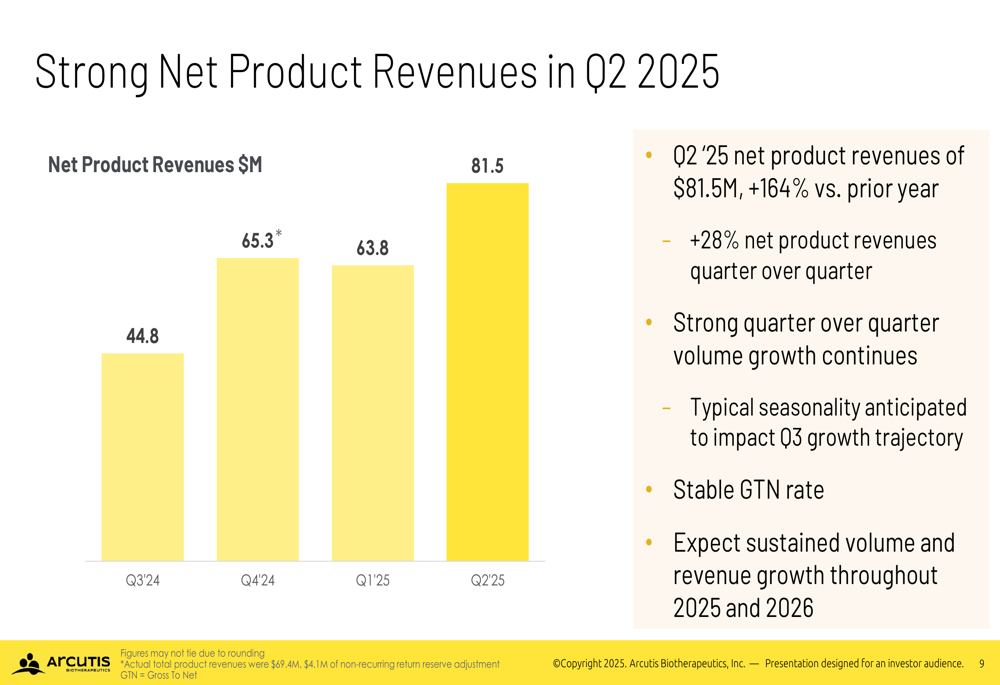

Arcutis reported Q2 2025 net product revenue of $81.5 million, representing a 164% increase year-over-year and a 28% sequential improvement from Q1. This performance continues the company’s strong growth trajectory, with management highlighting robust volume growth as a key driver.

As shown in the following chart of quarterly revenue growth:

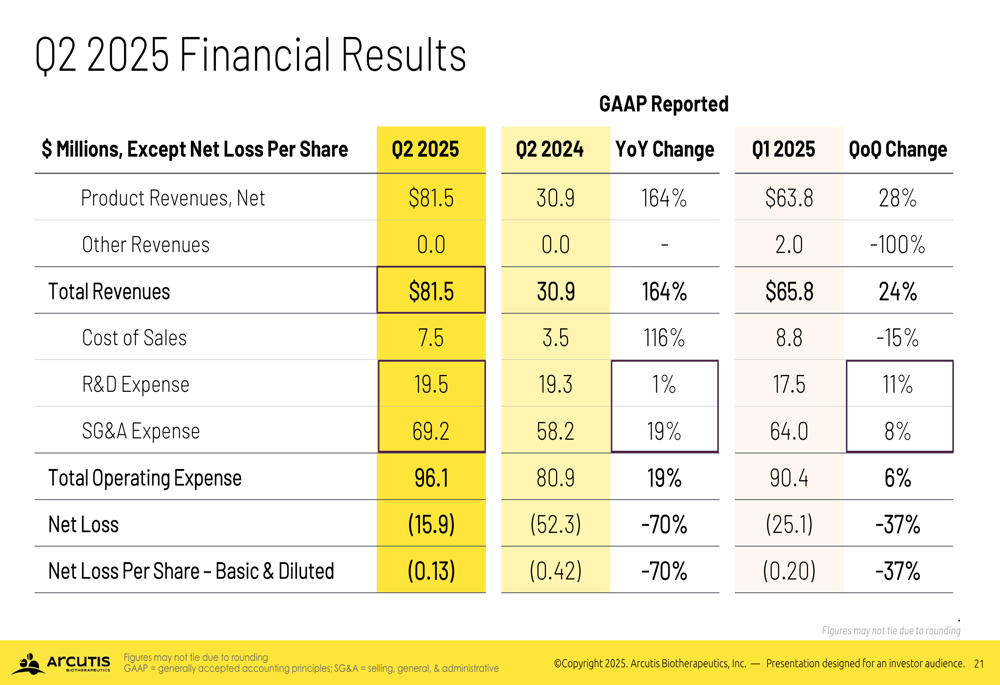

The company’s net loss narrowed significantly to $15.9 million ($0.13 per share) in Q2 2025, compared to a loss of $52.3 million ($0.42 per share) in the same period last year and $25.1 million ($0.20 per share) in Q1 2025. This represents a 70% year-over-year improvement in net loss and a 37% sequential reduction.

The detailed financial results demonstrate the company’s improving operational efficiency:

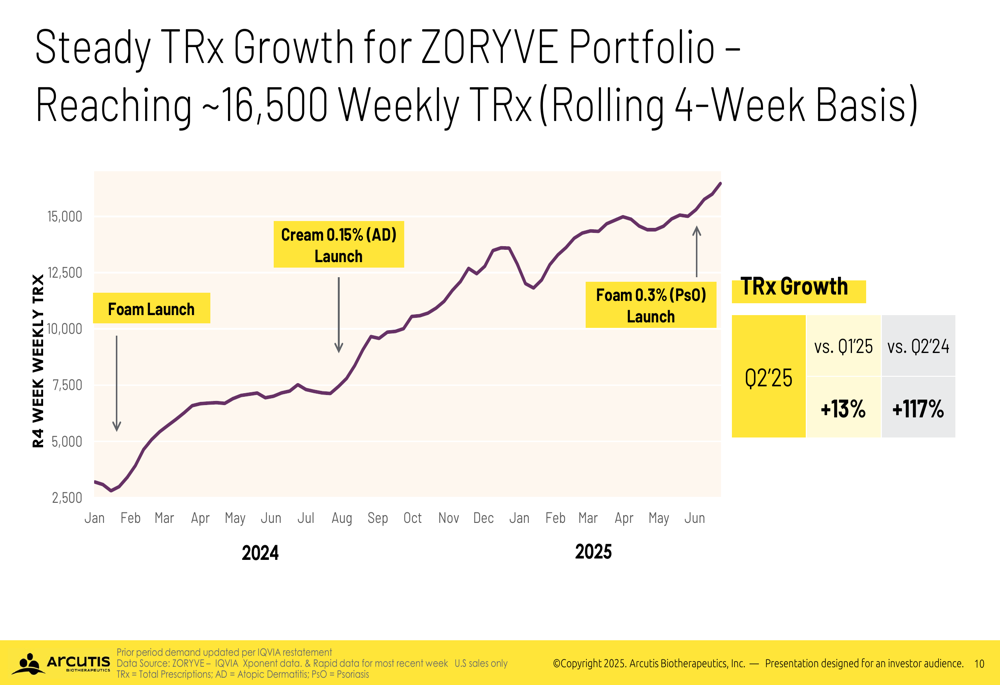

Prescription volume for the ZORYVE portfolio showed consistent growth, reaching approximately 16,500 weekly total prescriptions (TRx) on a rolling 4-week basis. TRx growth increased 13% compared to Q1 2025 and 117% versus Q2 2024, highlighting the strong market adoption of Arcutis’ products.

The following chart illustrates the steady prescription growth trajectory:

Commercial Strategy and Product Portfolio

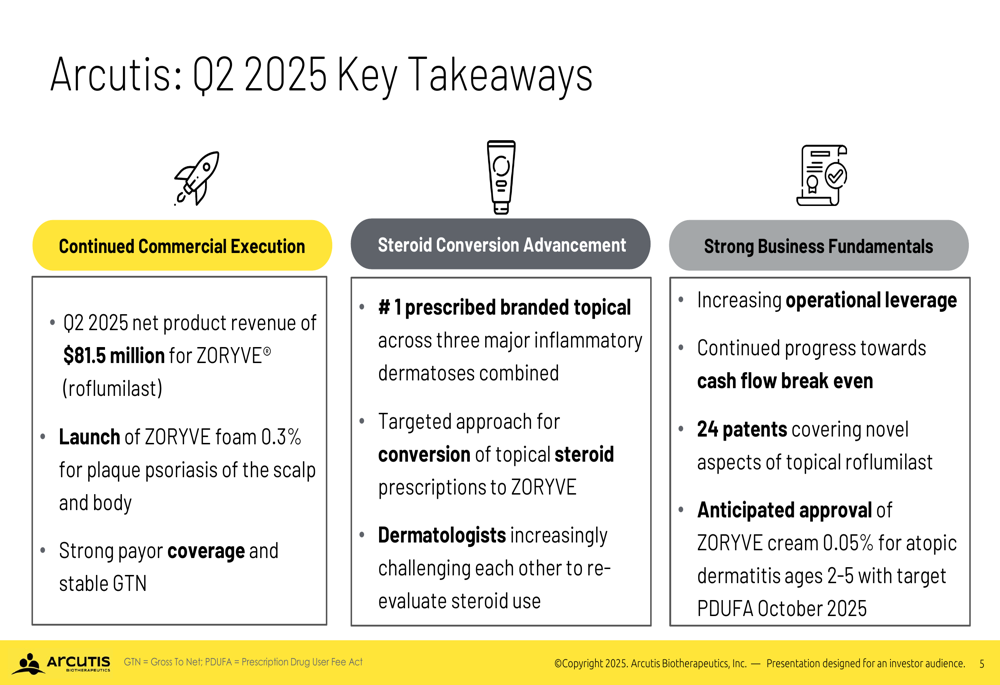

Arcutis’ commercial strategy centers on expanding its ZORYVE portfolio across multiple dermatological conditions while converting patients from topical steroids to its steroid-free alternatives. The company highlighted that ZORYVE has become the #1 prescribed branded topical across three major inflammatory dermatoses.

The key takeaways from the quarter emphasize the company’s commercial execution and strategic positioning:

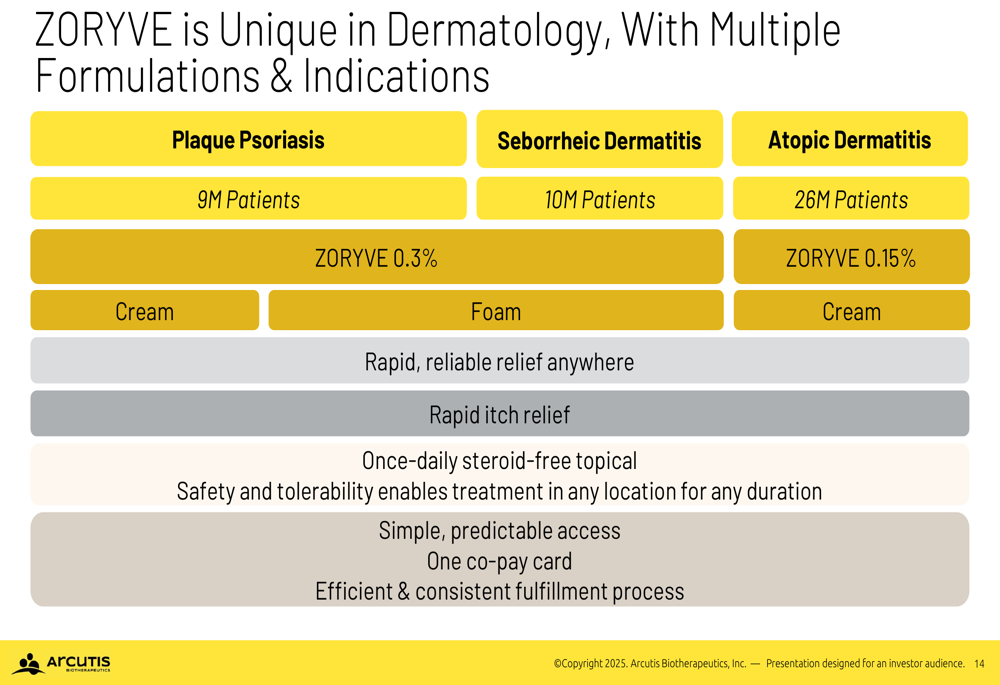

A core strength of Arcutis’ commercial approach is its comprehensive product portfolio addressing multiple conditions with different formulations. ZORYVE is now available in various formulations targeting plaque psoriasis, seborrheic dermatitis, and atopic dermatitis, providing treatment options for approximately 45 million potential patients.

As illustrated in the following slide, the company’s diverse product offerings create a unique position in the dermatology market:

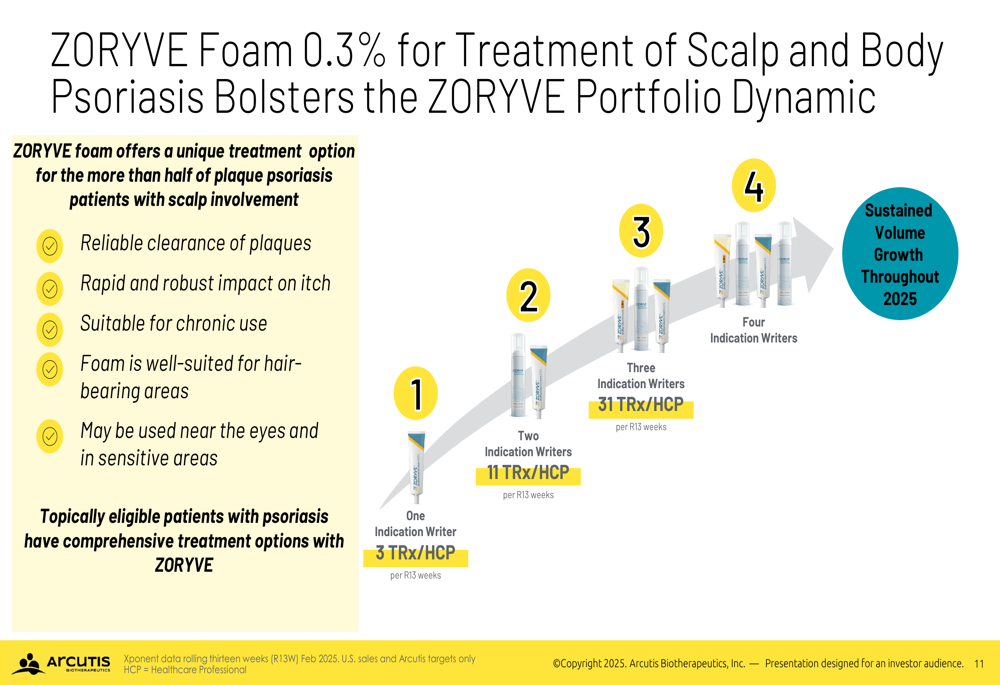

The recent launch of ZORYVE Foam 0.3% for scalp and body psoriasis has strengthened the portfolio’s dynamics. Data presented shows that healthcare providers prescribing across multiple indications generate significantly higher prescription volumes, with four-indication writers producing substantially more prescriptions than single-indication writers.

Pipeline and Regulatory Updates

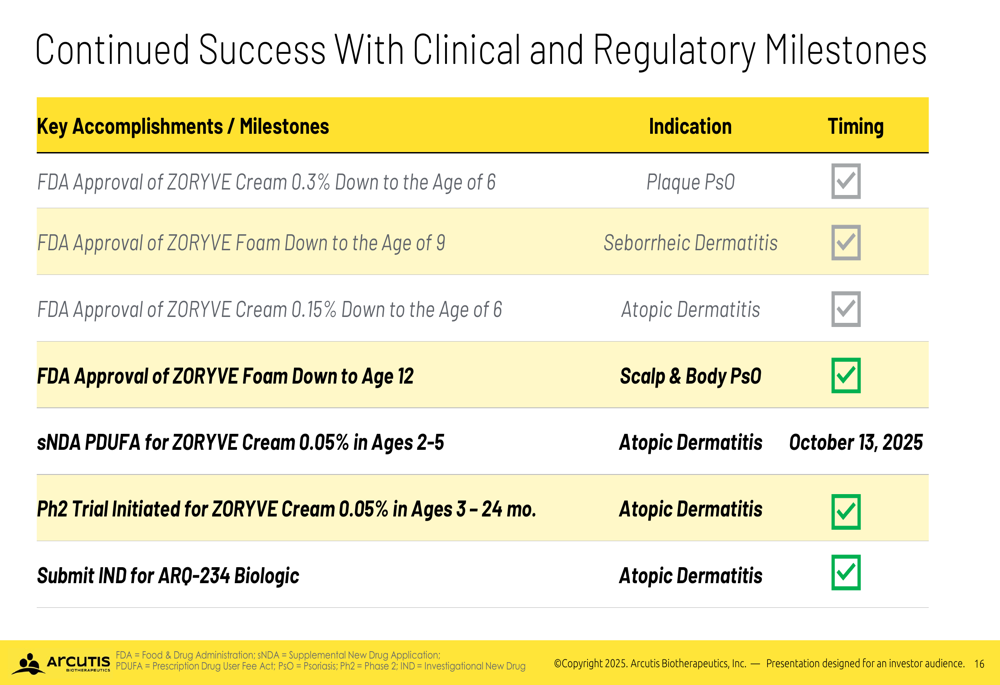

Arcutis continues to advance its clinical and regulatory initiatives, with several important milestones achieved and upcoming events that could drive future growth. The company has received multiple FDA approvals for various ZORYVE formulations across different age groups and indications.

The following slide summarizes the company’s recent regulatory successes and upcoming milestones:

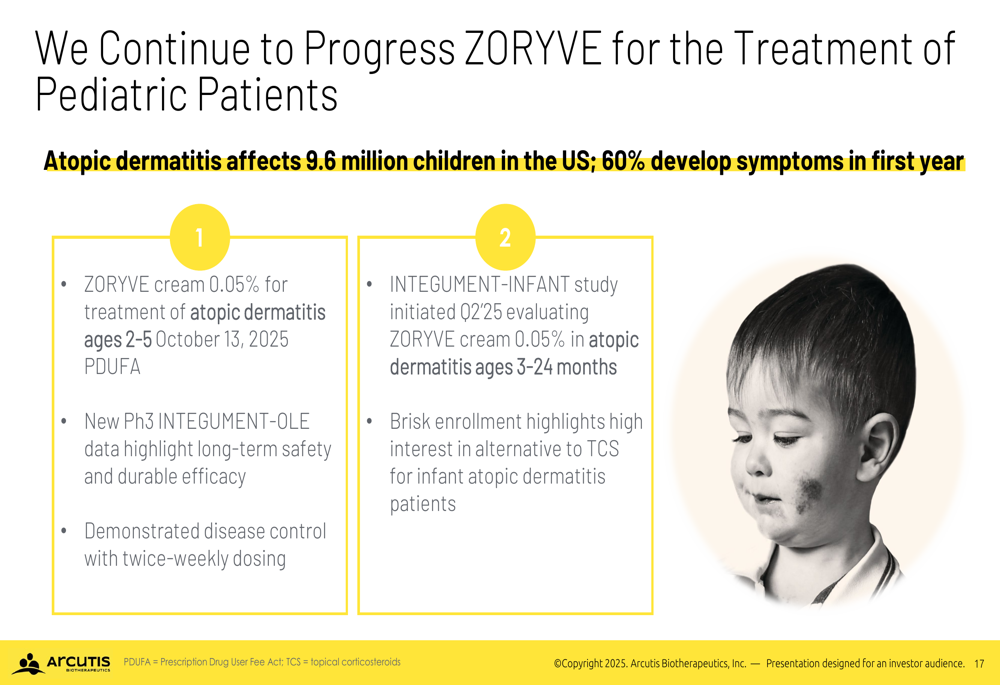

A key near-term catalyst is the PDUFA date of October 13, 2025, for ZORYVE Cream 0.05% for atopic dermatitis in children ages 2-5. Additionally, the company has initiated a Phase 2 trial for ZORYVE Cream 0.05% in infants ages 3-24 months with atopic dermatitis, potentially expanding its addressable market further.

As shown in the following slide, pediatric development remains a strategic priority:

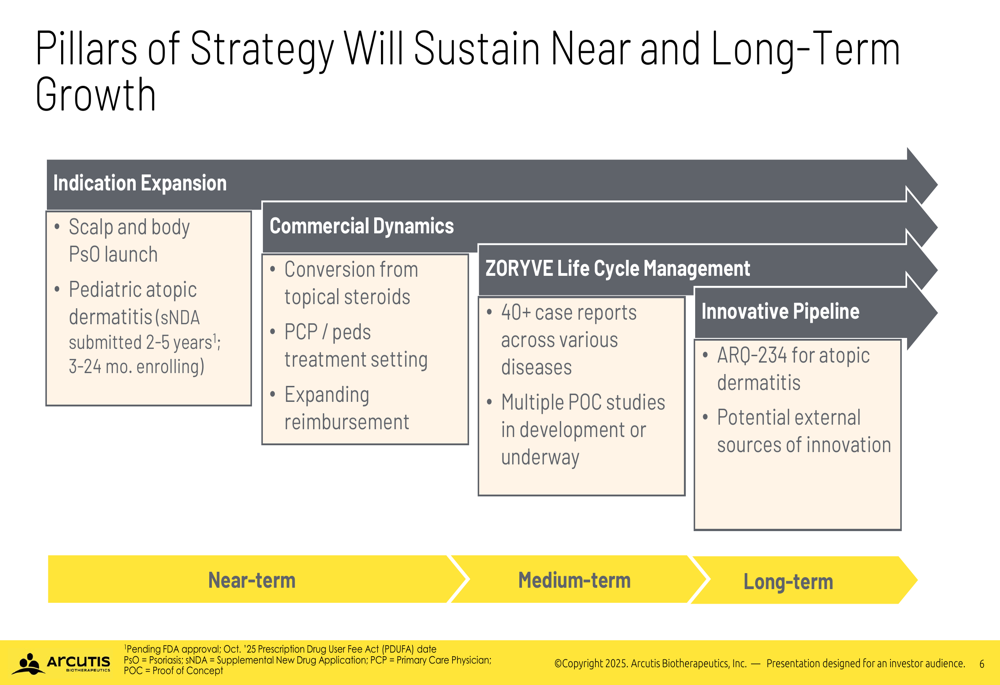

The company’s long-term growth strategy is built on four pillars: indication expansion, commercial dynamics, lifecycle management, and innovative pipeline development. This approach mirrors successful strategies employed by biologics like Humira and Dupixent, which significantly increased their market potential through indication expansion.

Financial Position and Outlook

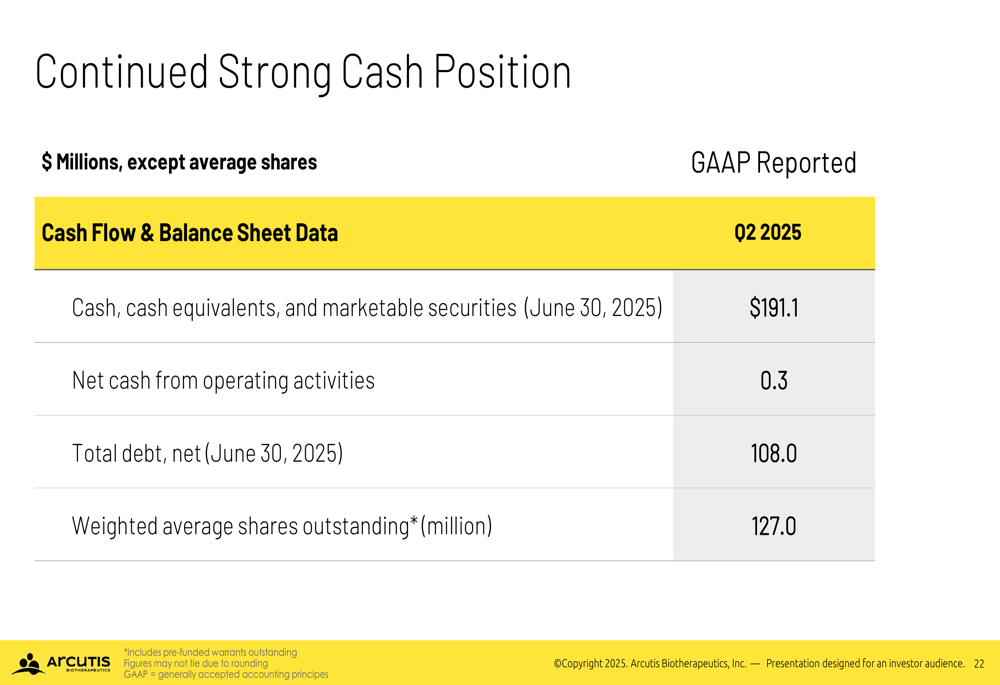

Arcutis reported a strong financial position with $191.1 million in cash, cash equivalents, and marketable securities as of June 30, 2025. Notably, the company achieved positive cash flow from operations of $0.3 million during the quarter, marking significant progress toward sustainable profitability.

The following slide details the company’s financial position:

Management expects continued volume and revenue growth throughout 2025 and 2026, though noted that typical seasonality may impact Q3 growth trajectory. The company maintains a stable gross-to-net (GTN) rate and continues to make progress toward cash flow breakeven.

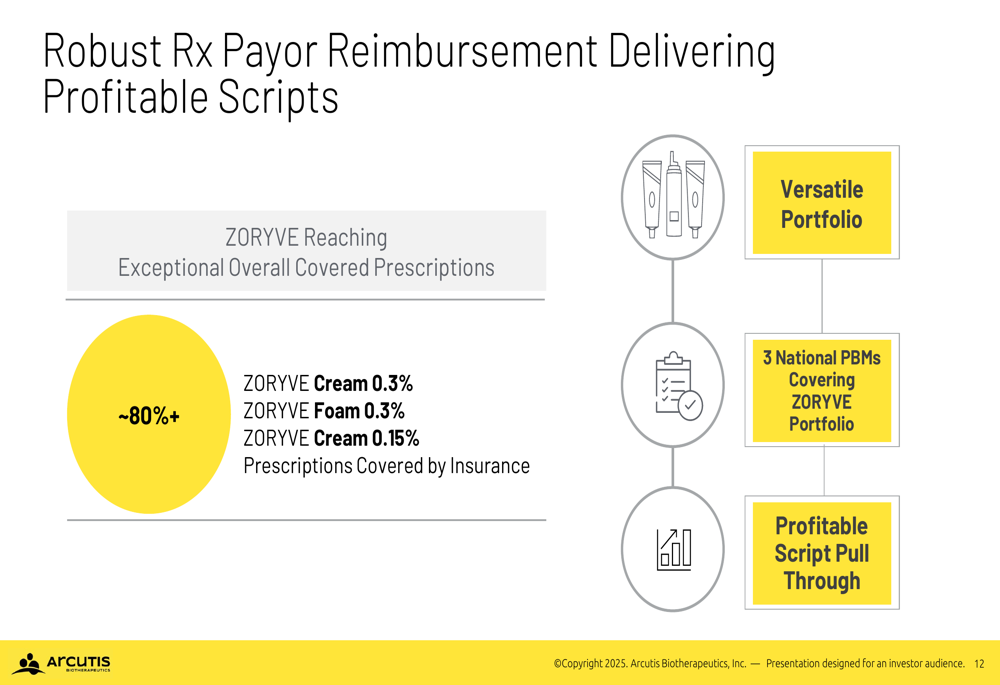

Insurance coverage remains robust, with over 80% of ZORYVE prescriptions covered across all formulations. This strong reimbursement profile supports profitable script pull-through and sustainable commercial growth.

While the overall outlook remains positive, investors should note that the company’s ARQ-255 program did not meet efficacy thresholds in Phase 1b trials to advance to Phase 2, representing a setback in one area of the pipeline. However, the core ZORYVE franchise continues to demonstrate strong commercial momentum and expansion potential across multiple indications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.