SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Aritzia Inc . (TSX:ATZ) presented its Q1 fiscal 2026 investor presentation on July 10, 2025, revealing robust financial performance and strategic growth initiatives. The Canadian fashion retailer, positioned in the "Everyday Luxury" segment between mid-market and sub-luxury brands, continues to capitalize on its strong momentum from Q4 2025.

The company’s stock closed at $74.58 on the presentation date, representing significant growth from its 52-week low of $36.51, though slightly down 0.71% for the day. Aritzia (OTC:ATZAF)’s market positioning strategy focuses on delivering high-quality products, aspirational shopping environments, and engaging client service across both physical and digital channels.

Q1 2026 Financial Highlights

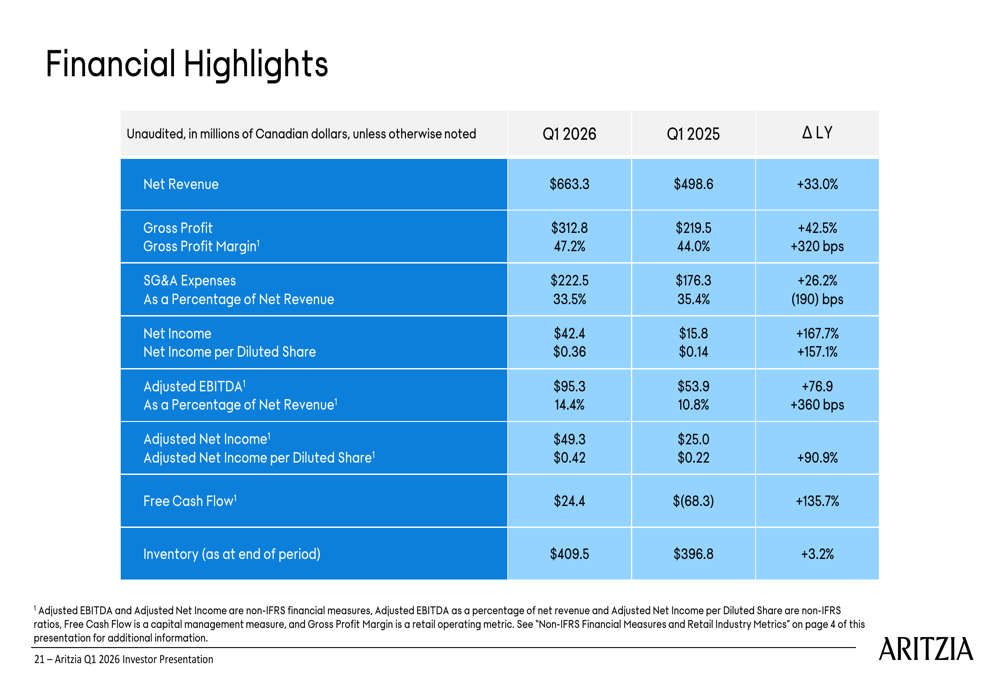

Aritzia delivered exceptional Q1 2026 results, with net revenue reaching $663.3 million, a 33.0% increase compared to $498.6 million in Q1 2025. This strong performance follows the company’s impressive Q4 2025 results, where revenue reached $895 million with 31% year-over-year growth.

Gross profit surged 42.5% to $312.8 million, with gross profit margin expanding significantly by 320 basis points to 47.2%. This margin improvement reflects the company’s enhanced operational efficiencies and favorable product mix. SG&A expenses as a percentage of net revenue decreased by 190 basis points to 33.5%, demonstrating improved cost management.

Net income more than doubled to $42.4 million, representing a 167.7% increase from the previous year, while adjusted EBITDA rose 76.9% to $95.3 million. The company’s free cash flow improved dramatically to $24.4 million, compared to negative $68.3 million in the same period last year.

The following table summarizes Aritzia’s Q1 2026 financial performance:

Strategic Growth Initiatives

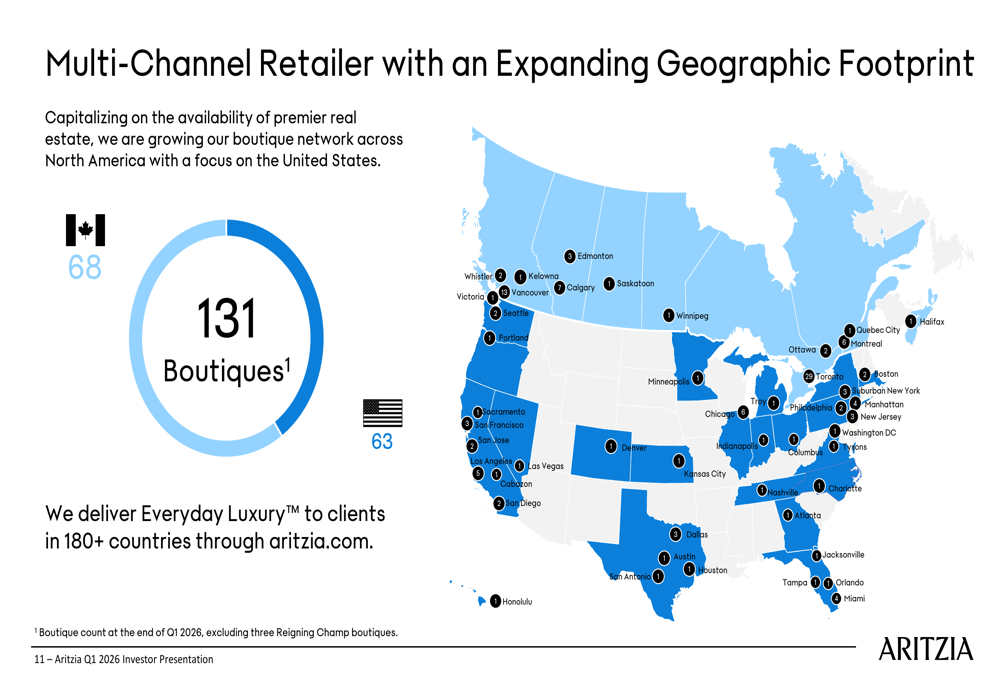

Aritzia’s growth strategy centers around three key pillars: geographic expansion, digital growth, and increased brand awareness. The company currently operates 131 boutiques across North America, with 68 in Canada and 63 in the United States, and delivers products to clients in over 180 countries through its eCommerce platform.

The following map illustrates Aritzia’s current boutique network across North America:

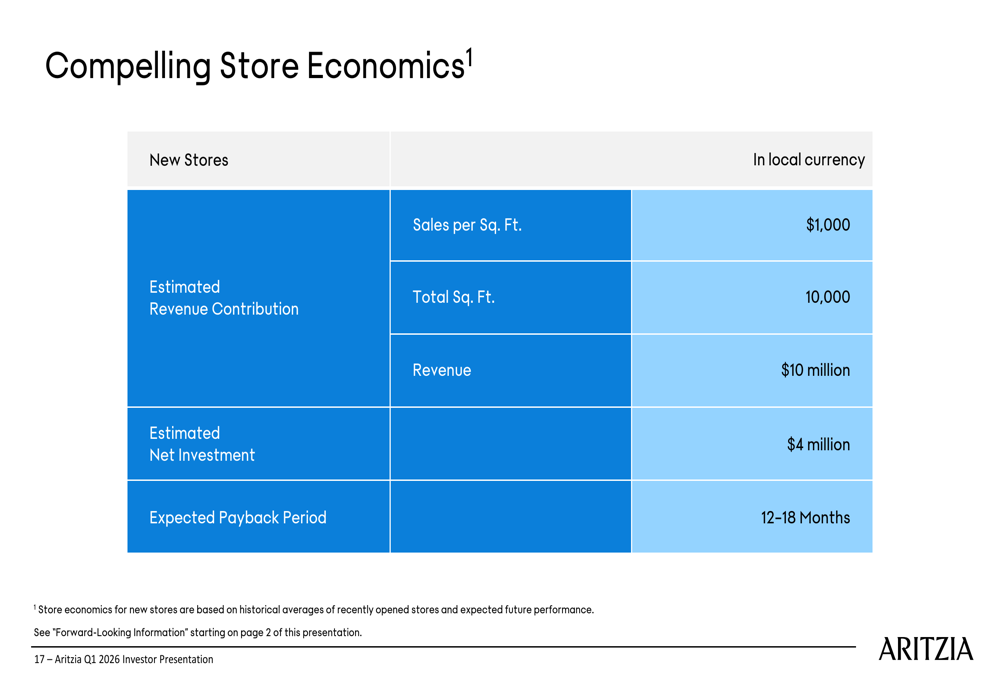

Geographic expansion remains a primary focus, with plans to open a minimum of 12 new boutiques in fiscal 2026, almost all in the United States. The company has identified the opportunity for over 150 locations in the US market and aims to open 8-10 new US boutiques annually through fiscal 2027. Aritzia’s compelling store economics support this expansion, with new stores generating approximately $10 million in revenue on a $4 million investment, yielding an expected payback period of just 12-18 months.

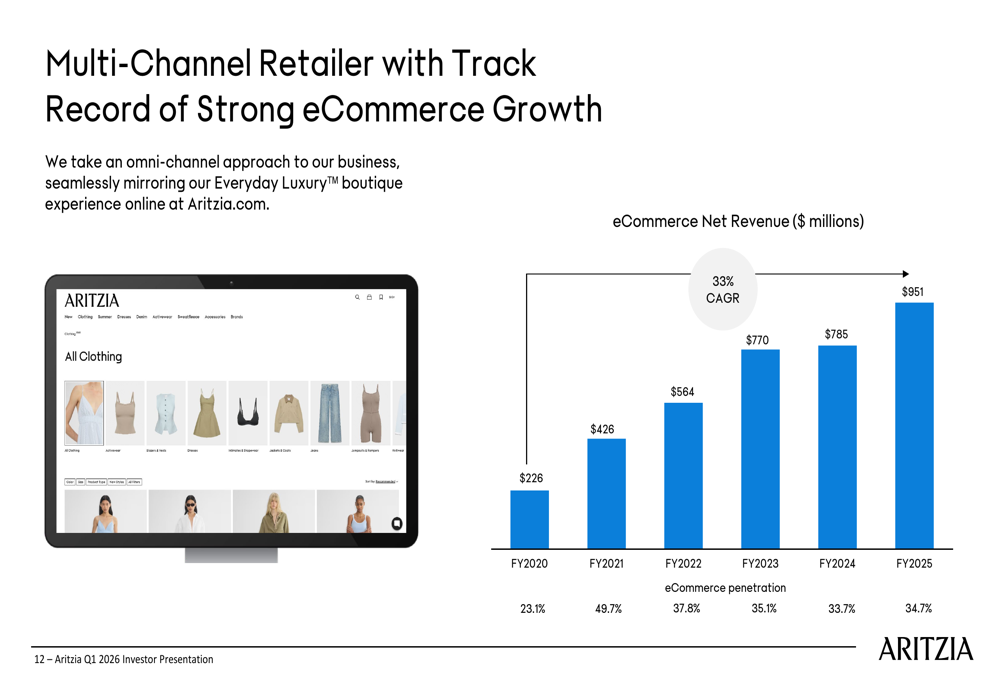

Digital growth represents another significant opportunity, with eCommerce net revenue growing at a 33% CAGR from fiscal 2020 to fiscal 2025. eCommerce penetration has increased from 23.1% to 34.7% of total net revenue during this period, reflecting the company’s successful omni-channel strategy.

The chart below shows Aritzia’s impressive eCommerce growth trajectory:

Aritzia’s "eCommerce 2.0" strategy focuses on connecting clients to its Everyday Luxury™ offerings online through tailored product discovery, creative innovation, and intuitive experience. The company is investing in enhanced digital experiences, including digital selling tools, fit analytics, site optimization, and personalization to drive continued eCommerce growth.

FY2026 Outlook and Long-Term Vision

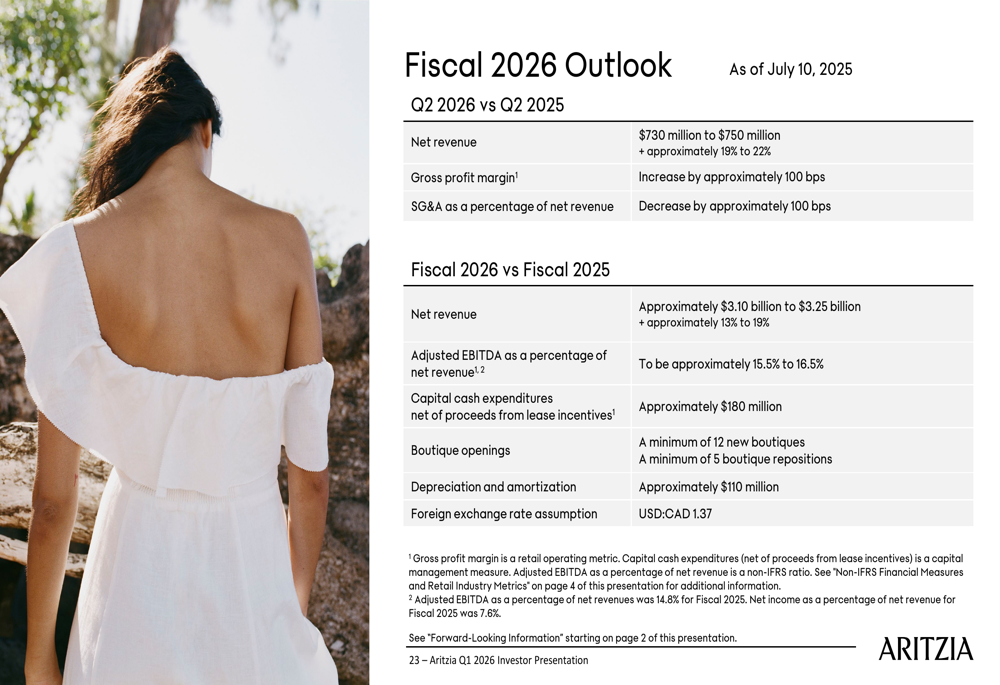

For the second quarter of fiscal 2026, Aritzia expects net revenue between $730 million and $750 million, representing approximately 19% to 22% growth compared to Q2 2025. The company anticipates gross profit margin to increase by approximately 100 basis points and SG&A as a percentage of net revenue to decrease by approximately 100 basis points.

For the full fiscal year 2026, Aritzia projects net revenue between $3.10 billion and $3.25 billion, representing 13% to 19% growth over fiscal 2025. Adjusted EBITDA margin is expected to range between 15.5% and 16.5% of net revenue. The company plans capital expenditures of approximately $180 million (net of proceeds from lease incentives).

The following table details Aritzia’s fiscal 2026 outlook:

Looking further ahead, Aritzia’s long-term growth plan targets fiscal 2027 net revenue between $3.5 billion and $3.8 billion, representing a 15-17% CAGR from fiscal 2022 to fiscal 2027. The company expects both US revenue and eCommerce revenue to more than double during this period, with total clients also projected to double. Adjusted EBITDA margin is expected to reach approximately 19% by fiscal 2027.

Financial Position and Capital Allocation

Aritzia maintains a strong financial position with $292.6 million in cash and cash equivalents as of Q1 fiscal 2026, plus $314.0 million available under its revolving credit facility and line of credit. The company has up to 4.2 million shares available for repurchase under its Normal Course Issuer Bid (NCIB).

Capital allocation priorities include funding operations, investing in growth, and returning cash to shareholders. From fiscal 2024 to fiscal 2027, Aritzia plans approximately $750 million in cumulative capital expenditures (net of proceeds from lease incentives), primarily for distribution centers and retail square footage growth. The company anticipates building a cash balance exceeding $1 billion by fiscal 2027.

Inventory management remains disciplined, with inventory up just 3.2% year-over-year to $409.5 million at the end of Q1 2026, despite the 33% revenue growth during the same period. This efficiency in inventory management contributes to the company’s strong cash flow generation.

While the presentation maintains an optimistic outlook, it’s worth noting that during the Q4 2025 earnings call, management acknowledged potential consumer slowdown later in the year and tariff impacts that could create 400 basis points of gross margin pressure. These challenges, while mentioned as risks in the presentation, are not quantified as specifically in the slides.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.