What’s OpenAI’s impact on Microsoft, Oracle and the software sector

Introduction & Market Context

Armstrong World Industries (NYSE:AWI) reported strong second-quarter 2025 results on July 29, 2025, showcasing double-digit growth across all key metrics and prompting management to raise full-year guidance. The company’s stock responded positively in premarket trading, rising 3.66% to $175, building on its previous close of $168.82.

The results continue the momentum seen in Q1 2025, when the company also exceeded analyst expectations. AWI’s performance comes amid mixed signals in the construction materials sector, with the company successfully navigating input cost inflation and market uncertainties through pricing power and operational efficiency.

Quarterly Performance Highlights

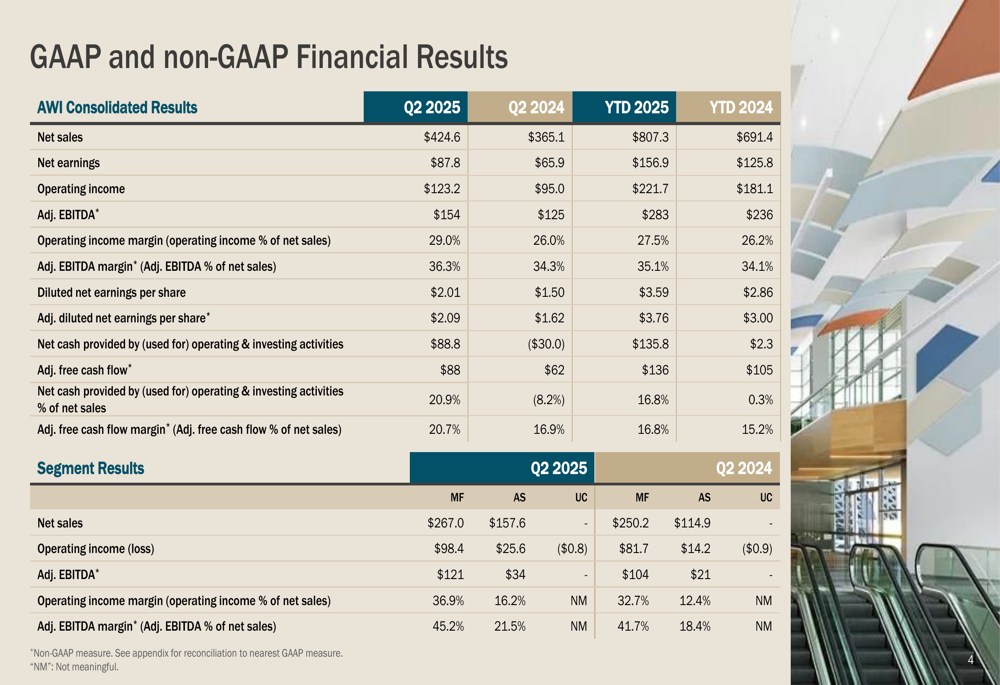

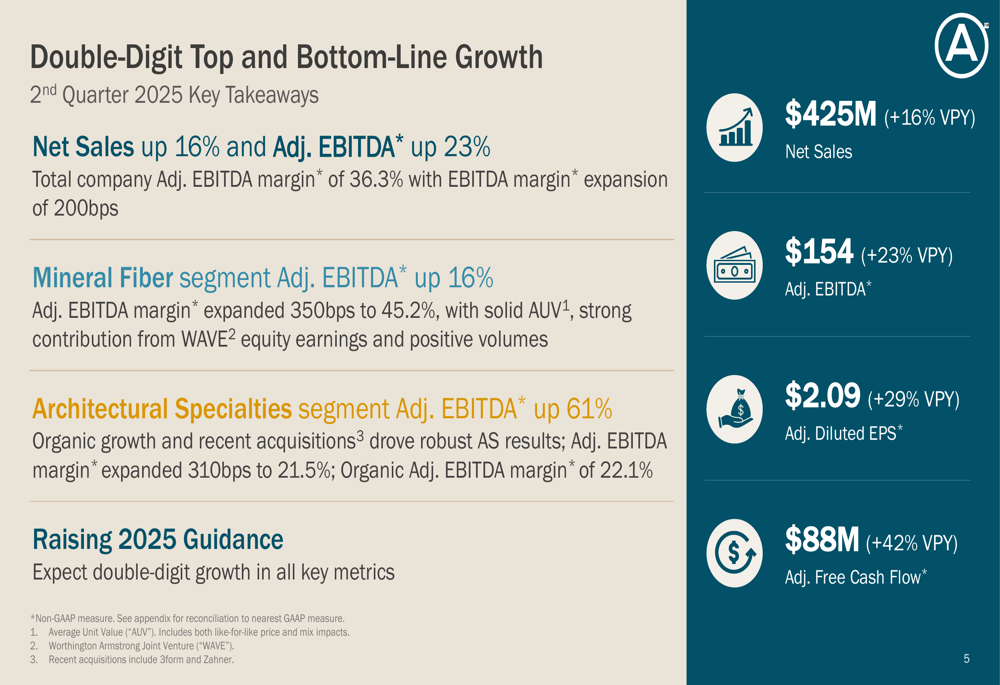

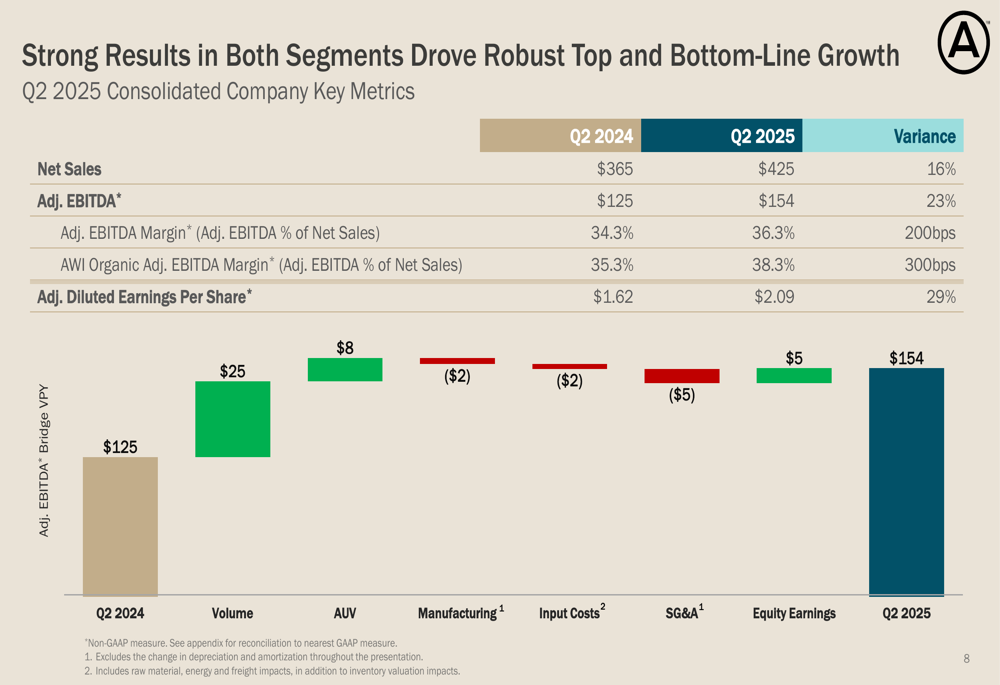

Armstrong World Industries delivered impressive results across all key financial metrics in Q2 2025, with consolidated net sales reaching $424.6 million, a 16% increase compared to Q2 2024. Adjusted EBITDA grew 23% to $154 million, while adjusted diluted earnings per share rose 29% to $2.09.

As shown in the following comprehensive financial results table:

The company’s performance was driven by strong results in both operating segments. The Mineral Fiber segment, which represents approximately 63% of total sales, posted a 7% increase in net sales to $267 million, with adjusted EBITDA rising 16% to $121 million. The Architectural Specialties segment delivered even stronger growth, with net sales up 37% to $157.6 million and adjusted EBITDA surging 61% to $34 million.

The following slide highlights the key takeaways from the quarter, emphasizing the double-digit growth in both revenue and earnings:

Detailed Financial Analysis

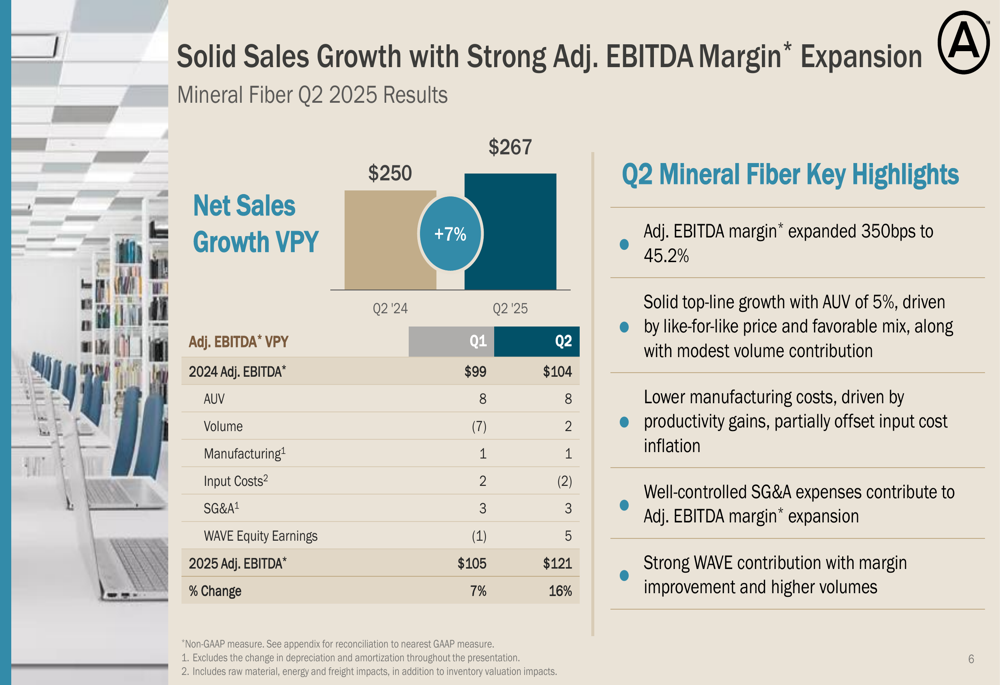

The Mineral Fiber segment’s strong performance was driven by a combination of solid average unit value (AUV) growth of 5%, primarily from like-for-like pricing and favorable mix, along with modest volume contribution. The segment’s adjusted EBITDA margin expanded an impressive 350 basis points to 45.2%, benefiting from productivity gains, well-controlled SG&A expenses, and strong contribution from WAVE equity earnings.

As illustrated in this detailed breakdown of the Mineral Fiber segment’s performance:

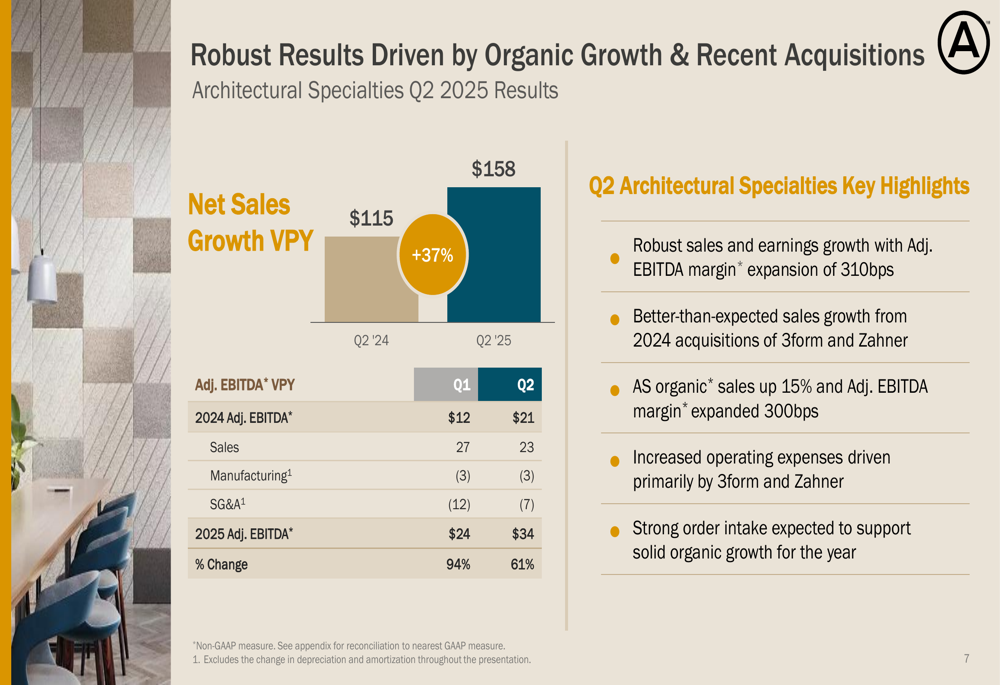

The Architectural Specialties segment delivered even more robust results, with net sales growth of 37% year-over-year. This exceptional performance was driven by both organic growth of 15% and better-than-expected contributions from the 2024 acquisitions of 3form and Zahner. The segment’s adjusted EBITDA margin expanded 310 basis points to 21.5%, with organic adjusted EBITDA margin reaching 22.1%.

The following chart details the drivers behind the Architectural Specialties segment’s strong performance:

On a consolidated basis, Armstrong World Industries’ adjusted EBITDA increased by $29 million compared to Q2 2024, reaching $154 million. This growth was primarily driven by higher volumes (+$25 million), improved AUV (+$8 million), and increased equity earnings (+$5 million), partially offset by higher manufacturing costs, input costs, and SG&A expenses.

The waterfall chart below illustrates the factors contributing to the adjusted EBITDA growth:

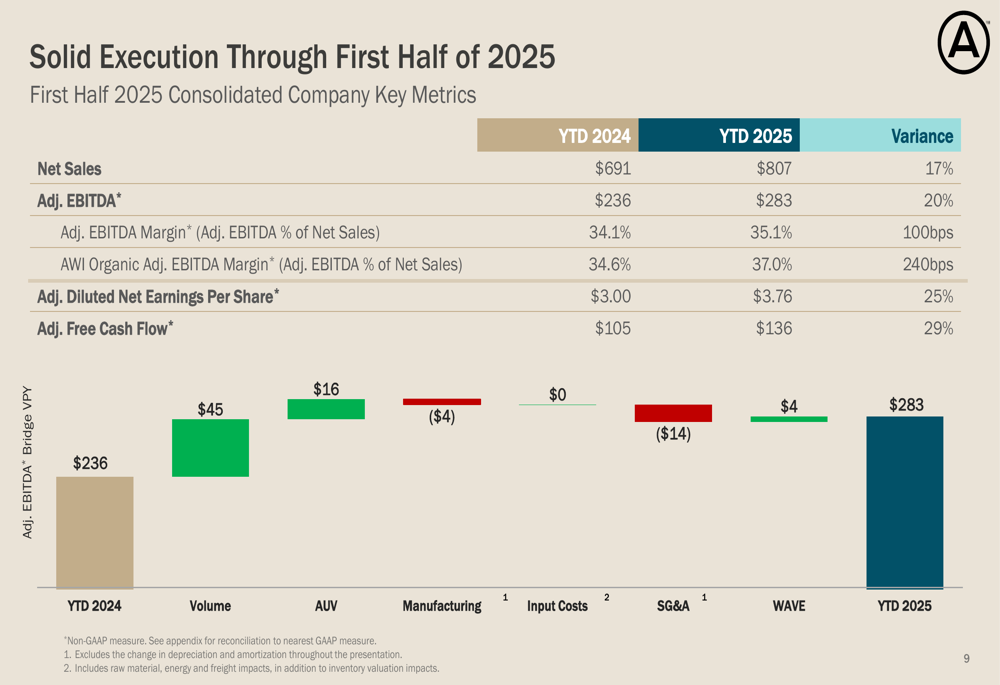

For the first half of 2025, Armstrong World Industries has maintained strong execution, with year-to-date net sales up 17% to $807 million and adjusted EBITDA increasing 20% to $283 million. The company’s adjusted EBITDA margin expanded 100 basis points to 35.1%, while adjusted diluted EPS grew 25% to $3.76.

As shown in this first-half 2025 performance summary:

Strategic Initiatives

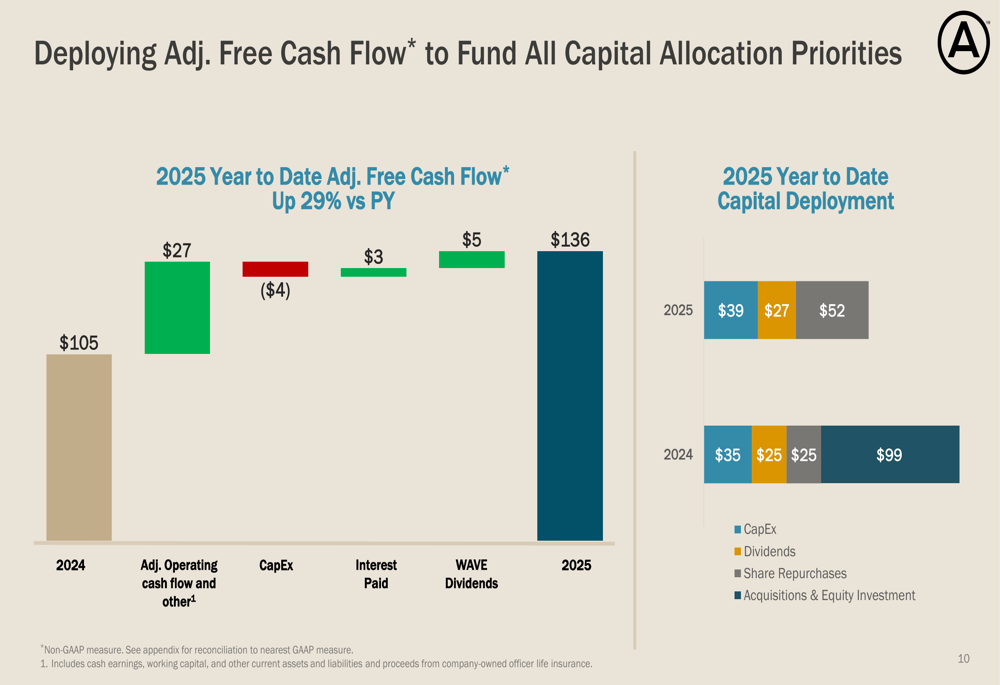

Armstrong World Industries continues to effectively deploy its adjusted free cash flow to fund all capital allocation priorities. For the first half of 2025, adjusted free cash flow increased 29% year-over-year to $136 million. The company has allocated this cash to capital expenditures ($39 million), dividends ($27 million), and share repurchases ($52 million).

The following chart illustrates the company’s cash flow generation and capital deployment:

The strong performance of recent acquisitions, particularly 3form and Zahner, highlights the success of Armstrong World Industries’ inorganic growth strategy. These acquisitions are performing better than expected and contributing significantly to the Architectural Specialties segment’s growth.

Forward-Looking Statements

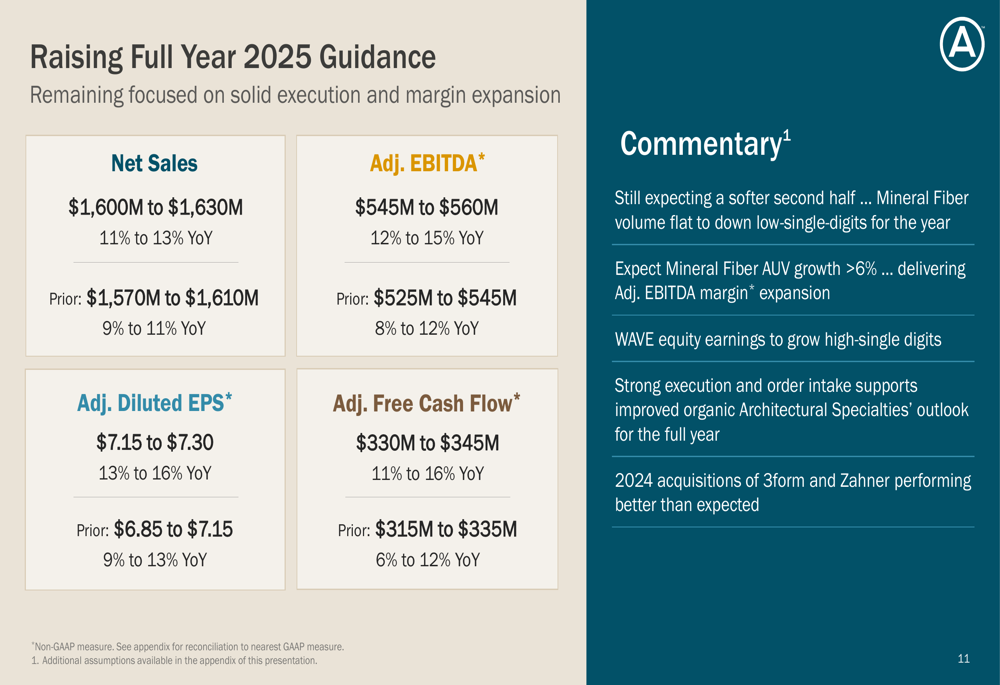

Based on the strong first-half performance, Armstrong World Industries has raised its full-year 2025 guidance across all key metrics. The company now expects net sales of $1,600 million to $1,630 million (11-13% year-over-year growth), adjusted EBITDA of $545 million to $560 million (12-15% growth), adjusted diluted EPS of $7.15 to $7.30 (13-16% growth), and adjusted free cash flow of $330 million to $345 million (11-16% growth).

The updated guidance and management commentary are presented in the following slide:

Despite the raised guidance, management still expects a softer second half of the year, with Mineral Fiber volume projected to be flat to down low-single-digits for the full year. However, this is expected to be offset by Mineral Fiber AUV growth exceeding 6% and continued strong performance in the Architectural Specialties segment. The company also anticipates WAVE equity earnings to grow at high-single digits.

The updated segment assumptions include Mineral Fiber net sales growth of approximately 5% with an adjusted EBITDA margin of around 43%, and Architectural Specialties net sales growth exceeding 25% with an adjusted EBITDA margin of approximately 19%.

Armstrong World Industries’ Q2 2025 results demonstrate the company’s ability to execute effectively in a challenging environment, leveraging pricing power, operational efficiency, and strategic acquisitions to deliver strong financial performance. With raised guidance for the full year, the company is well-positioned to continue its growth trajectory through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.