Avidia Bancorp CEO Cozzone buys $49,986 in shares

Array Technologies Inc (NASDAQ:ARRY) reported substantial revenue growth in its first quarter 2025 earnings presentation on May 6, showing strong momentum after a challenging previous quarter. The solar tracking systems manufacturer posted a 97% year-over-year revenue increase while maintaining its full-year guidance despite ongoing industry uncertainties.

Quarterly Performance Highlights

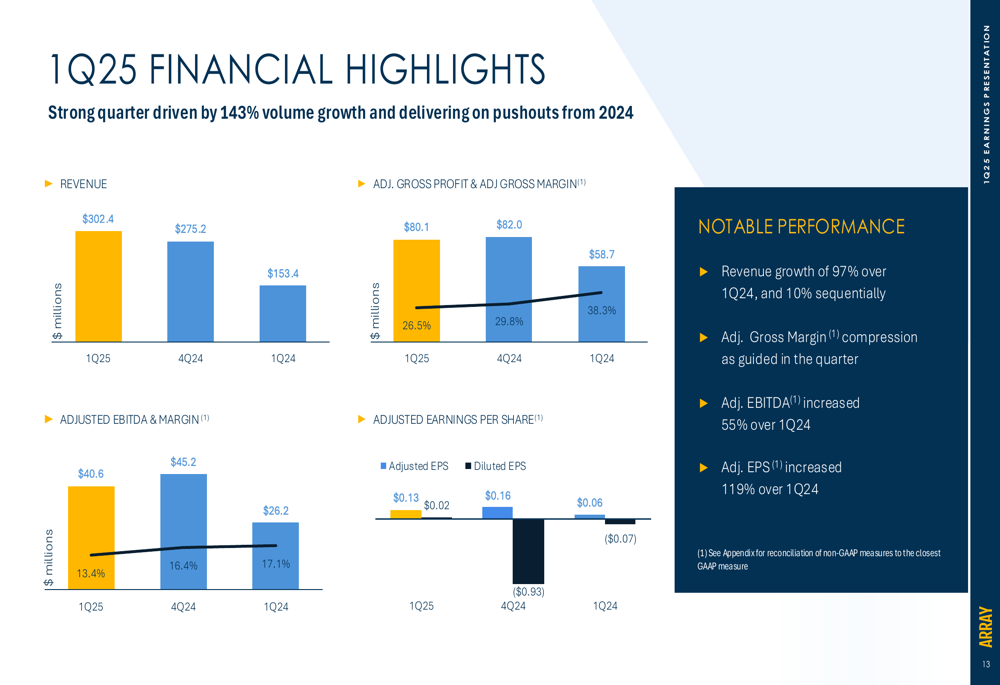

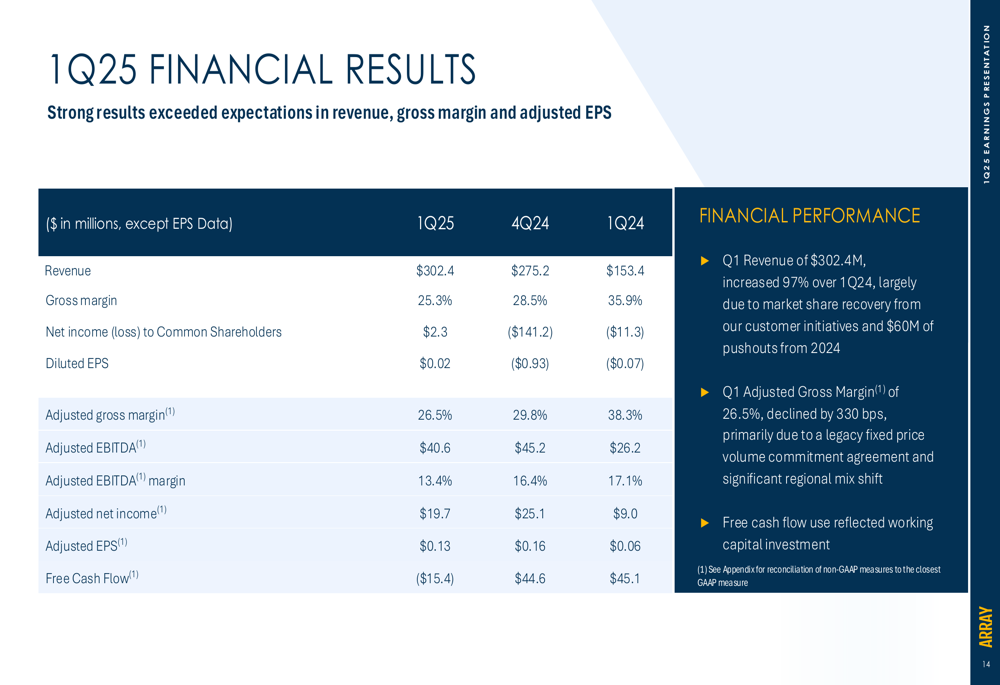

Array reported Q1 2025 revenue of $302.4 million, representing a 97% increase from Q1 2024 and a 10% sequential improvement from Q4 2024. Adjusted earnings per share reached $0.13, up 119% from the same period last year. However, adjusted gross margin compressed to 26.5% compared to 38.3% in Q1 2024, which the company attributed to lower margin project mix.

As shown in the following financial highlights chart, the company maintained strong growth momentum while navigating margin pressures:

The detailed financial results table below shows that while revenue significantly increased, adjusted EBITDA margin declined to 13.4% from 17.1% in the prior year period:

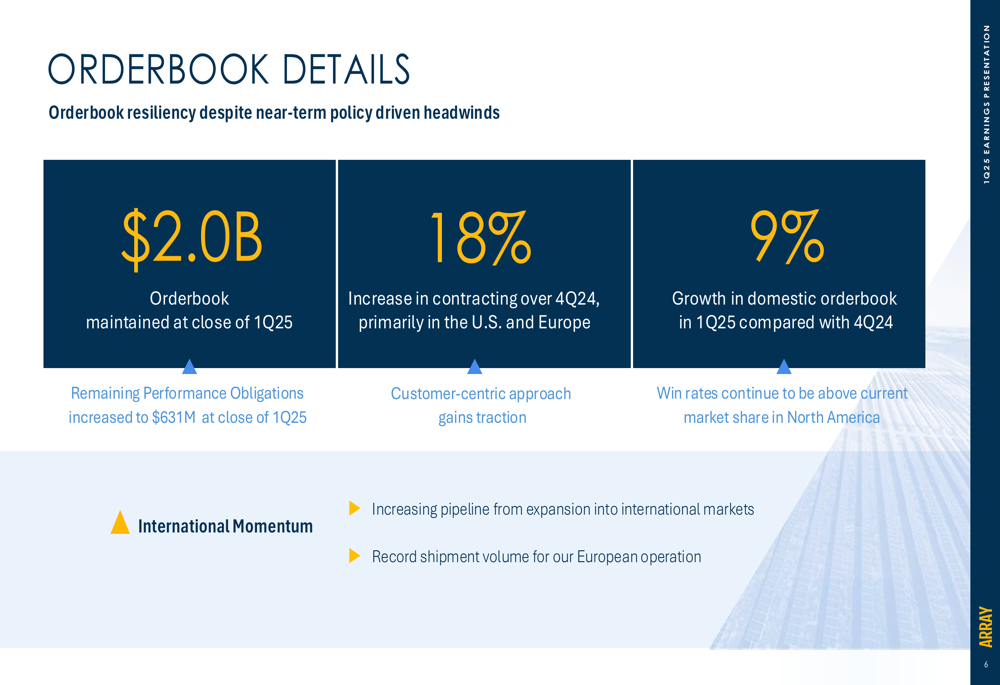

Array’s orderbook remained steady at $2.0 billion at the close of Q1 2025, with an 18% increase in contracting compared to Q4 2024. The company noted this resilience occurred despite policy-driven headwinds, with particular growth in U.S. and European markets.

The following chart illustrates the company’s orderbook performance:

Market Dynamics and Strategic Response

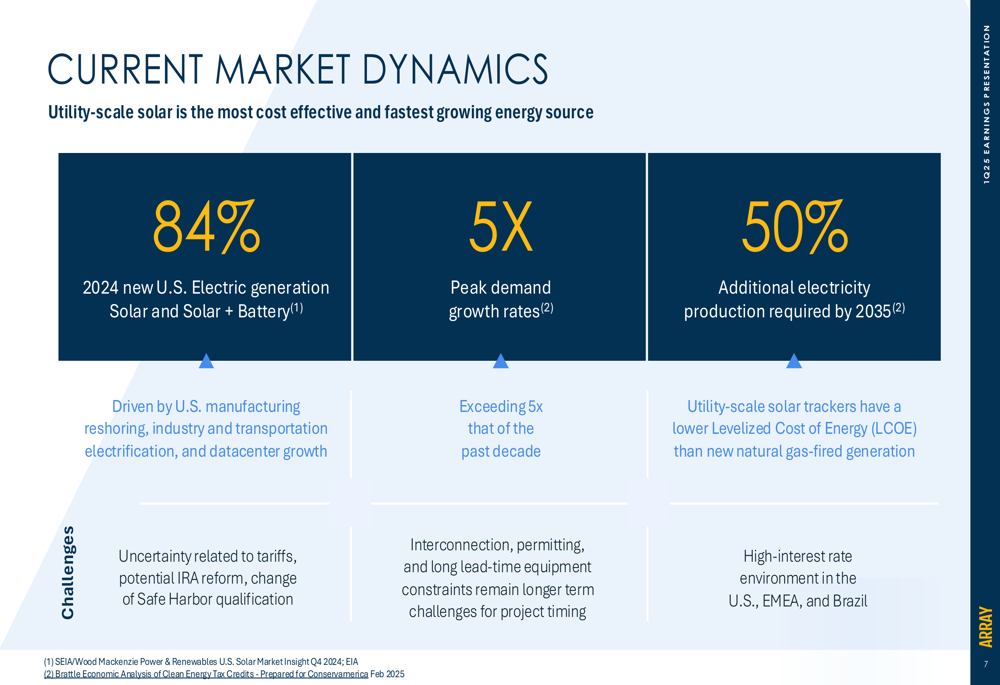

Array’s presentation highlighted both near-term uncertainties and long-term confidence in the utility-scale solar market. The company noted that 84% of 2024 new U.S. electric generation is solar and solar plus battery storage, with utility-scale solar positioned as the most cost-effective and fastest-growing energy source.

As illustrated in the market dynamics overview:

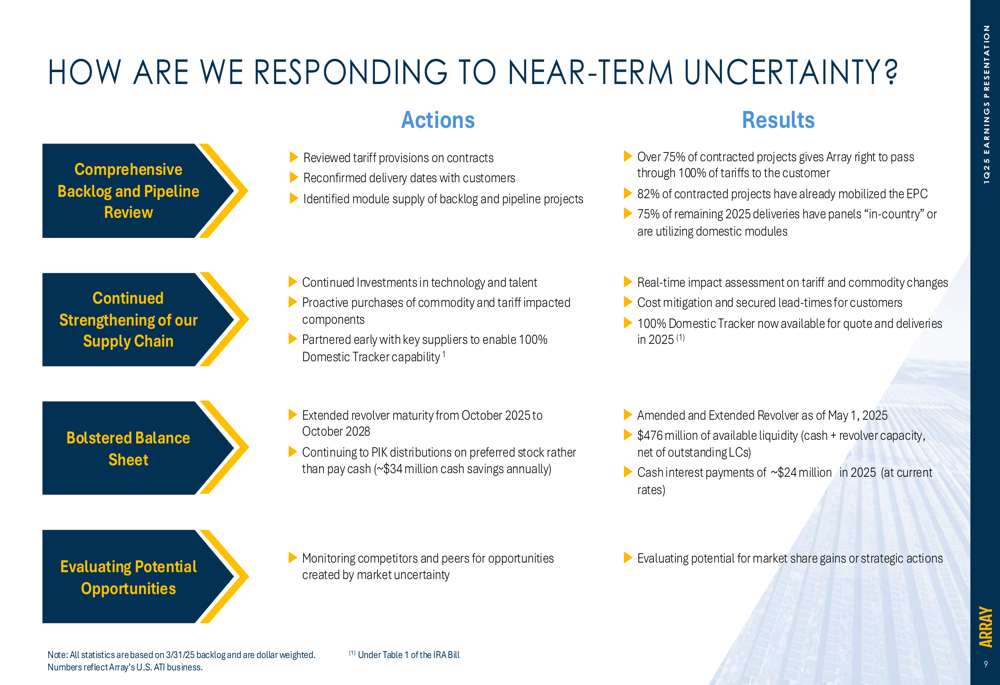

However, Array acknowledged several challenges, including tariff uncertainties, potential IRA reform, interconnection issues, and a high-interest rate environment. In response, the company has implemented a comprehensive strategy to mitigate these risks.

The following slide details Array’s response to market uncertainties:

Kevin G. Hostetler, Chief Executive Officer, emphasized the company’s strategic positioning: "Utility scale solar remains the cheapest and fastest growing energy source," a statement that aligns with the company’s presentation of market growth projections showing power demand expected to grow 17% from 2024-2034.

Supply Chain and Product Innovation

Array highlighted its regionally tailored supply chain as a competitive advantage, particularly in navigating potential tariff impacts. The company now offers 100% Domestic Content Trackers under Table 1 of the IRA, with orders received capable of being delivered in 2025. This positions Array to benefit from domestic content requirements in the Inflation Reduction Act.

On the product innovation front, Array reported progress with several key initiatives:

- SkyLink: Launched in Q3 2024 with first commercial installation underway in Arizona

- SmarTrack & Hail Alert Response: Nearly 3.5x growth in installations since 2023, surpassing 5 GW

- 2000V capability: Full evaluation completed in April 2025, increasing power density and lowering BOS costs

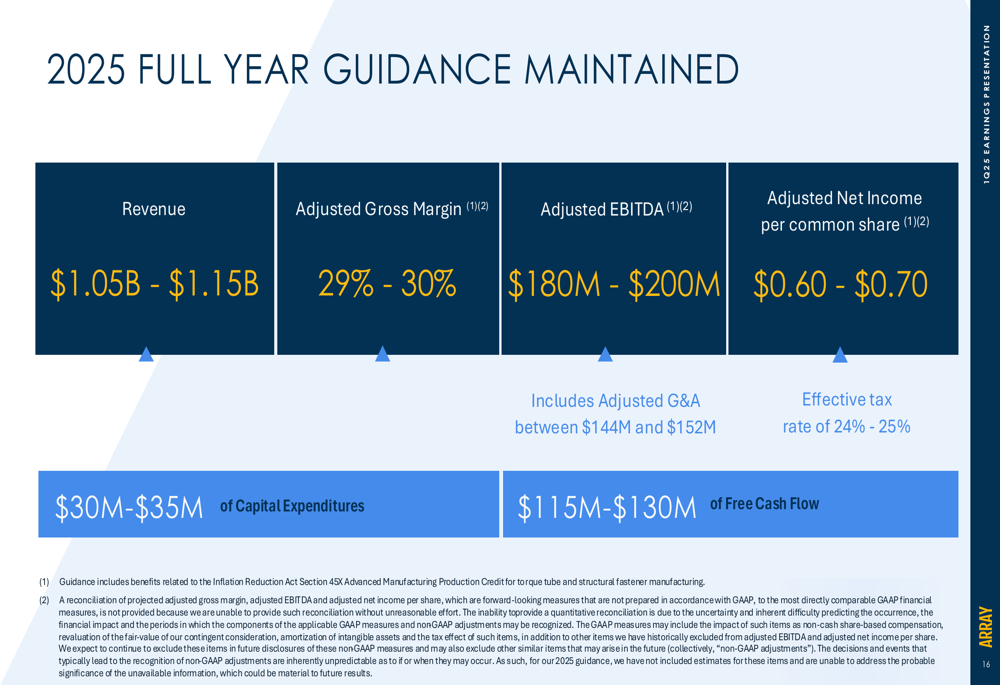

Financial Position and 2025 Outlook

Array maintained a strong financial position with $348.3 million in cash and cash equivalents as of March 31, 2025, representing a 21% increase from Q1 2024. The company reported total available liquidity of $509.6 million including its revolving credit facility.

The company reaffirmed its full-year 2025 guidance:

H. Keith Jennings, Chief Financial Officer, noted during the previous earnings call that the company has "no explicit arrangements to share 45x with any customers," referring to tax credits under the Inflation Reduction Act, which should support margin performance.

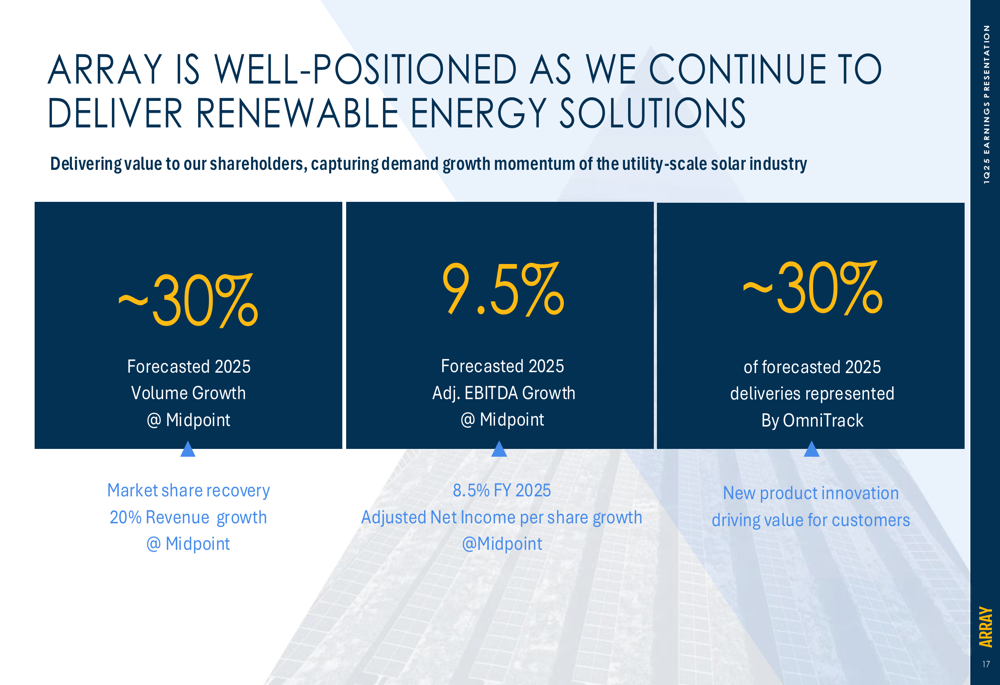

Array’s presentation concluded with a slide highlighting its positioning for future success:

The stock showed positive momentum following the earnings release, with premarket trading up 8.52% to $5.35, according to available data. This represents a significant reversal from the negative reaction to the company’s Q4 2024 results, when the stock dropped nearly 13% after missing EPS expectations.

While free cash flow was negative at $15.4 million for Q1 2025 compared to positive $45.1 million in Q1 2024, management attributed this to working capital investments needed to support the company’s growth trajectory.

Array’s presentation suggests the company has stabilized after a challenging 2024 and is positioned for growth, though investors will likely continue monitoring margin performance and the impact of potential policy changes on the solar industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.